Bitget UEX Daily Report | U.S. Temporarily Lifts Oil Sanctions on Iran; Semiconductor Sector Strong but Warning Signs Emerge; SpaceX Pullback Weighs on Tech Stocks

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S. Temporarily Lifts Oil Sanctions on Iran; Semiconductor Sector Strong but Warning Signs Emerge; SpaceX Pullback Weighs on Tech Stocks

Overall, geopolitical easing and the Federal Reserve’s policy path are key variables; investors should focus on data-driven validation and divergent opportunities.

I. Top News

Federal Reserve Dynamics: RBC Strategist Says U.S. Equities Can Withstand Moderate Rate Hikes

- Lori Calvasina, Head of U.S. Equity Strategy at RBC Capital Markets, stated that equity markets should remain resilient if the Federal Reserve implements approximately two 25-basis-point rate hikes over the next 12 months. New Fed Chair Kevin Warsh emphasized that high inflation would not be tolerated—yet markets continued to post consecutive gains.

- U.S. equities rebounded during a shortened trading week; the S&P 500 has risen roughly 18% from its late-March lows. Market impact: Moderate tightening expectations have not significantly dampened risk appetite, but investors should remain vigilant for further guidance on policy trajectory from upcoming inflation data.

Global Commodities: U.S. Temporarily Lifts Iran Oil Sanctions for 60 Days

- U.S. Treasury Secretary Janet Yellen announced on June 22 that, as part of the U.S.-Iran negotiation framework, the Treasury Department issued a 60-day general license exempting production, delivery, sale, and import restrictions on Iranian crude oil, petrochemicals, and petroleum products—effective until August 21, 2026.

- This marks the first return of Iranian crude to the U.S. market in 35 years, potentially increasing global supply and easing Middle East tensions. Market impact: Short-term oil prices face downward pressure; hedge funds increased net short positions on WTI to near a five-month high, underscoring expectations of supply re-entry—and injecting a new variable into energy markets.

Macroeconomic Policy: Trump Signs Executive Orders to Accelerate Quantum Computer Development

- Trump signed two executive orders directing federal agencies to collaborate with the private sector to deploy quantum computers for scientific research by 2028 and strengthen quantum system security readiness against cryptographic threats. Market impact: Boosts long-term outlook for tech infrastructure and may benefit related supply chains, though it could cause thematic divergence in traditional semiconductor stocks in the near term.

II. Market Recap

Commodities & FX Performance (Real-Time Updates)

- Spot Gold: ~$4,200/oz, 24h change: ~–0.2%

- Spot Silver: ~$65/oz, 24h change: ~–0.5%

- WTI Crude: ~$74/bbl, 24h change: ~+0.4%

- Brent Crude: ~$78/bbl, 24h change: ~+0.3%

- U.S. Dollar Index (DXY): ~101.0, 24h change: ~+0.1%

Driving Factors Analysis: The U.S.-Iran interim peace agreement and 60-day oil sanctions relief open the door for restored shipping through the Strait of Hormuz and increased supply. Hedge funds significantly increased net short positions on WTI to near a five-month peak, pressuring oil prices downward in the short term—though volatility is intensifying. Hawkish comments from new Fed Chair Warsh supported modest dollar strength, and combined with inflation expectations, triggered profit-taking in precious metals—causing slight pullbacks in gold and silver prices. While AI-driven industrial demand provides long-term support for commodities like copper, current geopolitical easing and dollar trends dominate short-term correlations. Investors including Rick Rule note that physical resource bottlenecks may become an invisible constraint on AI expansion; near-term focus remains on how U.S.-Iran negotiations continue to influence energy pricing. Overall, inter-asset correlations reflect renewed risk appetite—but with persistent caution—and the classic oil-gold negative correlation has re-emerged.

Cryptocurrency Performance

- BTC: ~$64,190 (+0.35%)

- ETH: ~$1,730 (+0.32%)

- Total Crypto Market Cap: ~$2.28 trillion (+0.1%)

- 24h Liquidations: ~$368 million total; long liquidations: ~$203 million

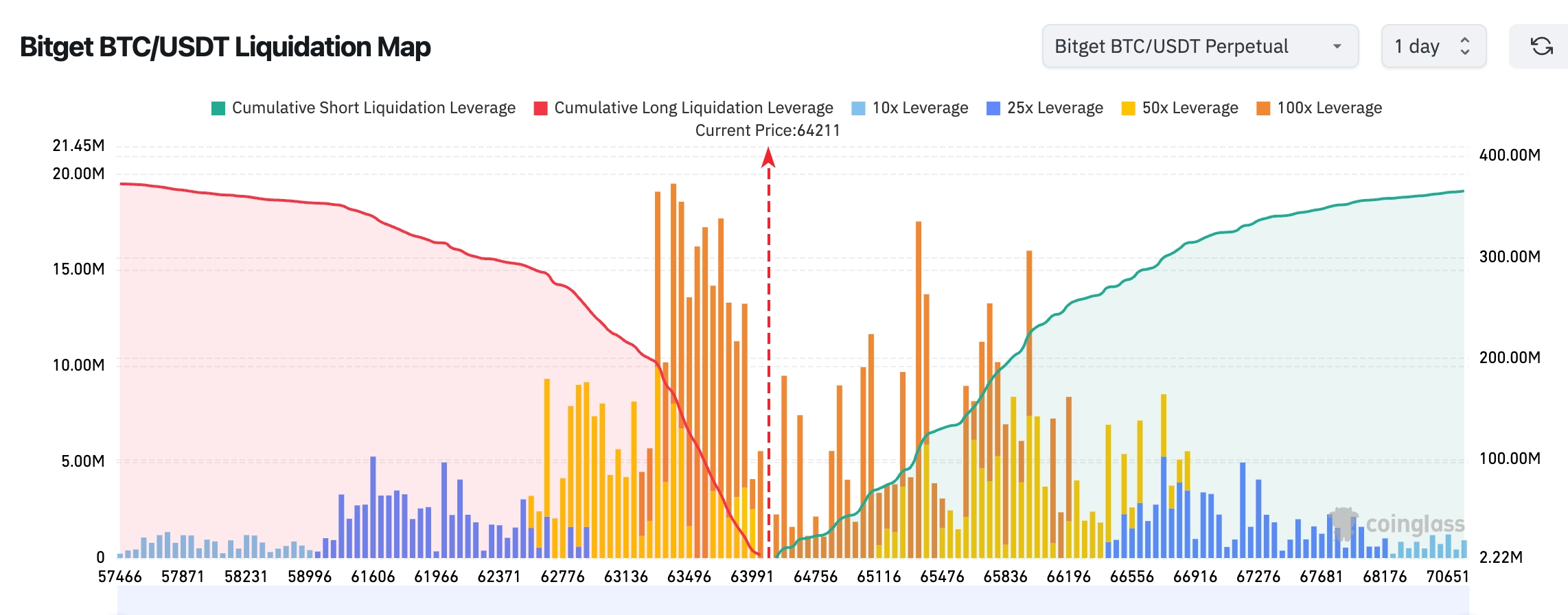

- Bitget BTC/USDT Liquidation Heatmap: Current BTC price ~$64,211. A dense cluster of long liquidation orders lies between $63,200–$64,000—if price falls into this zone, cascading long liquidations and amplified downside volatility may occur. Above, a denser concentration of short liquidation pressure exists between $65,300–$66,000; if BTC continues rising, short squeezes could push price further upward toward $66,500+

- Spot ETF Net Inflows/Outflows: BTC spot ETFs recorded ~$100 million net inflow yesterday

Driving Factors Analysis: Progress in U.S.-Iran peace talks eased geopolitical risk, while relatively stable macro conditions provided mild support to crypto markets—driving modest rebounds in BTC and ETH and a steady uptick in total market cap. ETF flows continued net inflows, signaling sustained institutional allocation interest—yet leveraged liquidation data indicates ongoing pressure to take profits at elevated levels. Major holders such as MicroStrategy continue accumulating Bitcoin; technically, BTC is consolidating around key ranges, diverging somewhat from ETH. Overall trend remains range-bound, with macro dollar strength and risk sentiment remaining dominant drivers. Investors should monitor how deepening geopolitical negotiations affect safe-haven assets—and watch the pace of leverage reduction.

U.S. Equity Index Performance

- Dow Jones Industrial Average: ~51,637 points (+0.29%)

- S&P 500: ~7,471 points (–0.37%)

- Nasdaq Composite: ~26,167 points (–1.32%)

Tech Giants’ Updates

- NVDA: ~$208.65 (–0.97%)

- AAPL: ~$297.01 (–0.34%)

- MSFT: ~$367.34 (–3.18%)

- GOOGL: ~$349.68 (–4.99%)

- AMZN: ~$232.79 (–4.75%)

- META: ~$563.85 (–2.32%)

- TSLA: ~$405.05 (+1.14%)

Performance Summary & Drivers Analysis: U.S. equity indices showed mixed performance—Dow exhibited relative resilience, while the Nasdaq faced pronounced pressure; tech giants displayed significant divergence. The semiconductor sector broadly outperformed, with the Philadelphia Semiconductor Index (SOX) hitting record highs. Micron (MU) surged past $1,200 for the first time, yet BTIG warned such historical patterns often appear near market tops. GOOGL plunged sharply after AI key talent John Jumper departed for Anthropic; AMZN followed suit. Conversely, AI-core names like NVDA saw capital flow back in, while TSLA held up relatively well. SpaceX’s stock plummeted over 16%, wiping out $400 billion in market value and falling below its IPO debut closing price—further weighing on sentiment. Overall, AI theme热度 remains strong, but valuation pressures and company-specific events—including talent movement—are amplifying stock-level divergence; geopolitical easing provides a macro buffer.

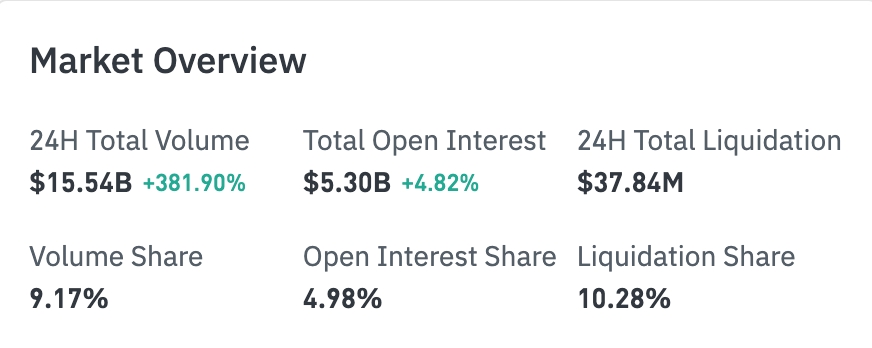

Crypto Stock Perpetual Contracts Overview

24H Total Turnover: $15.54 billion (+381.90%)

Total Open Interest: $5.30 billion (+4.82%)

24H Total Liquidations: $37.84 million

Share: Turnover 9.17%, Open Interest 4.98%, Liquidations 10.28%

Sectoral Open Interest Breakdown (Major Sectors)

Technology: $2.68 billion

Financials: $164 million

Consumer: $78.89 million

Industrials: $30.65 million

Biotech: $15.82 million

Trend observation: Technology sector open interest continues expanding and maintains absolute leadership—market capital remains heavily concentrated in AI- and semiconductor-related names.

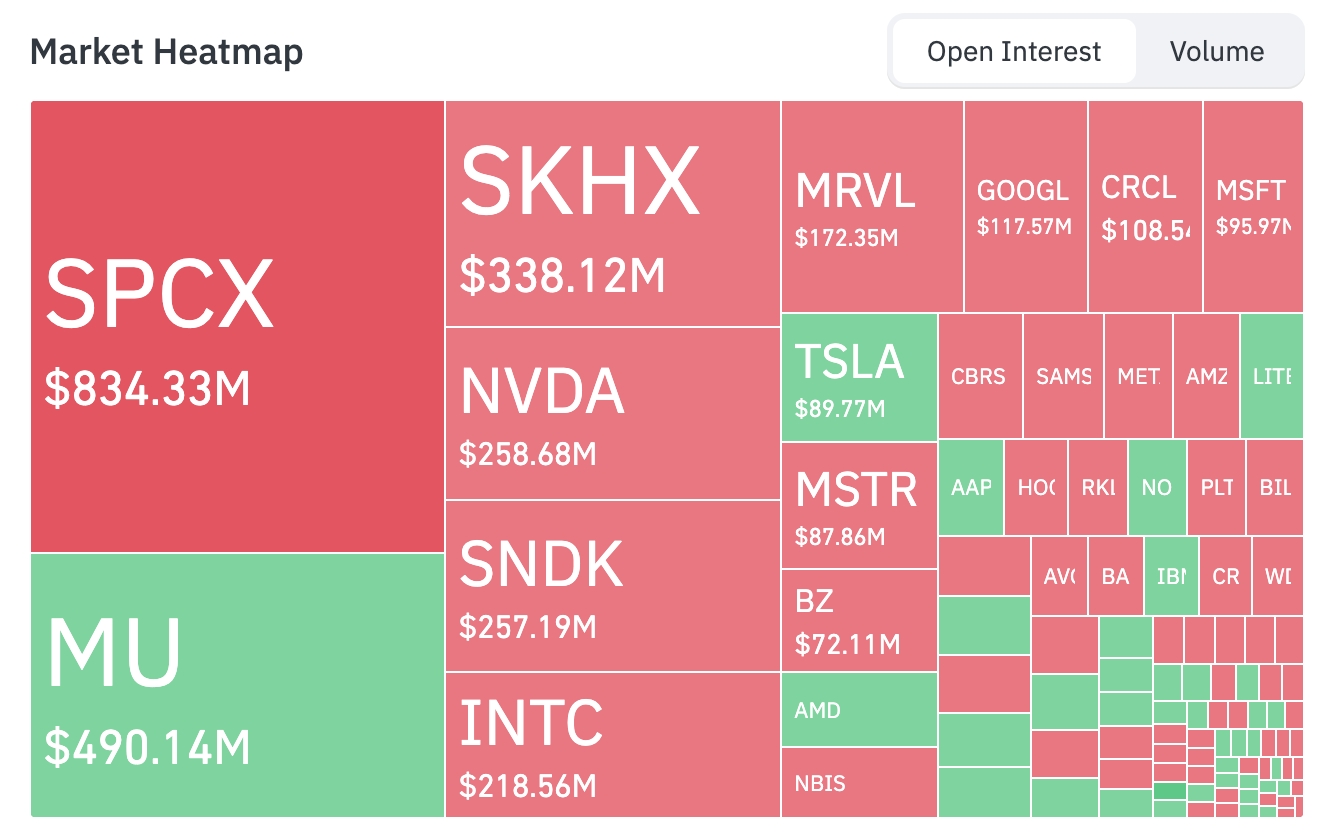

Market Heatmap (Open Interest Focused)

Top Asset Open Interest Ranking (in USD billions):

SPCX: $0.834B — Largest current open interest

MU: $0.490B

SKHX: $0.338B

NVDA: $0.259B

SNDK: $0.257B

INTC: $0.219B

MRVL: $0.172B

GOOGL: $0.118B

CRCL: $0.109B

MSFT: $0.096B

TSLA: $0.090B

MSTR: $0.088B

BZ: $0.072B

In terms of fund flows, MU, TSLA, LITE, AAPL, and AMD showed signs of position accumulation; whereas SPCX, SKHX, NVDA, MRVL, GOOGL, CRCL, MSFT, and MSTR experienced position reduction or capital outflow.

Sectoral Volatility Observations

Semiconductor Sector shows standout strength

- Key stocks: Micron Technology (MU) +6%+, Intel (INTC) +5%+, and other chipmakers including SanDisk posted positive performance.

- Drivers: Robust demand for high-bandwidth memory (HBM) and advanced-process chips from AI data centers continues to materialize—combined with SOX hitting record highs again—propelling sector-wide gains. As a memory leader, Micron directly benefits from the AI compute expansion cycle. However, Jonathan Krinsky, BTIG’s Chief Technical Strategist, warns that SOX’s relative strength versus the Nasdaq-100 has approached historic extremes (similar to the 2000–2001 tech bubble), with multiple single-day surges exceeding 5% over the past 60 trading days—an abnormal pattern signaling technical correction risk worth monitoring. Near-term, the sector may oscillate between AI-theme support and profit-taking pressure; investors should assess valuation alignment and macro liquidity shifts.

1. SpaceX (SPCX.US) – Sharp Correction Overview: SpaceX shares plunged over 16% Monday, instantly erasing ~$400 billion in market value and falling below its record-breaking IPO debut closing price. Prior to this, the company completed a $75-billion U.S. IPO—the largest ever—drawing intense market attention. Concurrently, SpaceX signed a multi-billion-dollar compute agreement with open-source AI startup Reflection AI, granting access to Colossus supercluster’s NVIDIA GB300 chips; Reflection will pay $150 million monthly starting July 2026 (totaling ~$6.3 billion if fully executed). Additionally, bankers are advancing SpaceX’s inaugural investment-grade bond issuance—covering maturities of 5–30 years—to finance long-term AI infrastructure expansion. Market Interpretation: Investors took profits on high-valuation pure-play AI/space stocks amid broader tech sector divergence and a shift in risk appetite driven by geopolitical easing. Some institutions argue that SpaceX, as a non-traditional public company, has already priced in its high-growth narrative—making short-term valuation corrections consistent with profit-taking logic. Yet its AI compute agreements and bond financing plans signal accelerating integration of space technology with AI infrastructure—reinforcing long-term narrative resilience. Investment Implications: Short-term volatility has surged significantly—investors should closely track bond roadshow progress and AI compute deployment milestones. For long-term investors, this pullback may offer a window to assess capital expenditure efficiency and execution capability—but high-leverage valuations remain vulnerable under macro tightening conditions.

2. Alphabet (GOOG.US) – AI Talent Mobility Overview: John Jumper, DeepMind’s core scientist and 2024 Nobel Prize in Chemistry laureate, announced via X last Friday that he was leaving Google after nine years to join rival Anthropic. His AlphaFold tool has predicted over 200 million protein structures, transforming biomedical research paradigms globally—and benefiting over 2 million scientists across 190+ countries. This event is viewed as a landmark case signaling a new phase in the U.S. AI talent war. Market Interpretation: Institutions widely express concern about potential long-term competitive impacts from top-tier talent attrition—especially against rivals like OpenAI and Anthropic, who are rapidly gaining ground. DeepMind had been Google’s crown jewel in AI; this departure intensified market discourse on “big-tech retention challenges” and fading innovation vitality—pushing GOOG shares down over 5% intraday. However, Google simultaneously announced partnerships with AI firms including 24A and ongoing investments, indicating efforts to mitigate talent risk via ecosystem strategy. Investment Implications: Talent dynamics are becoming a critical catalyst for valuation divergence among tech giants—investors should compare R&D retention rates and patent output across peers. For Alphabet, short-term pressure may reverse if rapid leadership replacement or strengthened open-source/cooperation strategies restore confidence.

3. Micron Technology (MU) – Breakout Event Overview: Micron Technology (MU) shares crossed above $1,200 for the first time, surging over 6% in a single day—standing out in the semiconductor sector. Meanwhile, the Philadelphia Semiconductor Index (SOX) repeatedly hit new all-time highs, and peers including Intel and SanDisk also posted strong gains—reflecting surging AI-driven demand for high-performance memory and storage. Market Interpretation: Explosive demand for HBM and advanced DRAM/NAND from AI data centers is the core engine behind Micron’s earnings and valuation uplift. Institutional analysis suggests that amid global tech giants’ trillion-dollar AI capex wave, memory bottlenecks have emerged as a key constraint—making Micron a direct beneficiary as a critical supplier. Resource investors including Rick Rule highlight that AI’s physical-world enablers—such as copper and chip materials—remain underappreciated by markets, further reinforcing structural opportunities in semiconductor downstream segments. Yet technical analysts like BTIG warn that the sector’s extreme strength is nearing historic bubble levels—warranting caution regarding correction risks. Investment Implications: Monitor synchronization between AI capex cycles and Micron’s capacity expansion—valuations must align with actual revenue growth, not just sentiment. Mid-term, if geopolitical easing reduces supply-chain risk, MU may sustain structural outperformance—but disciplined profit-taking is advised to manage technical cooling.

4. Semtech (SMTC) – AI Edge Computing Beneficiary Overview: As an analog and mixed-signal semiconductor supplier, Semtech delivered strong performance in AI-related applications, riding the broader sector rally. Its products serve edge computing, data center interconnect, and IoT use cases—benefiting from AI infrastructure’s evolution from cloud-centric to edge-distributed deployment. Market Interpretation: As AI model deployment shifts from centralized data centers to real-time edge inference, demand for Semtech’s signal chain solutions has risen markedly. Analysts note its expertise in low-power, high-performance analog chips makes it indispensable within the AI ecosystem—gaining investor attention amid the broader semiconductor index’s record highs. Yet overall sector valuation pressure also transmits to mid- and small-cap names, warranting vigilance against amplified volatility. Investment Implications: Suitable for investors focused on AI themes extending from core compute to peripheral infrastructure. Track quarterly order guidance and gross margin improvement to gauge sustainability of growth.

5. Coherent (COHR) – Optical Communications & Laser Tech Highlights Overview: Coherent holds a leading position in data center optical modules and high-power lasers—posting strong performance amid the semiconductor/AI infrastructure boom. Its products directly serve ultra-high-bandwidth, low-latency optical interconnect and advanced manufacturing needs. Market Interpretation: Surging AI training and inference demand for ultra-high-bandwidth, low-latency optical communications has significantly benefited Coherent as a key supplier. Consensus views indicate that data center upgrade cycles—combined with optoelectronic integration trends—provide medium- to long-term growth support. Meanwhile, sector strength has led to clear stock-level divergence, with execution-strong optoelectronics players commanding premium valuations. Geopolitical supply-chain risks and macro interest-rate environments remain potential constraints. Investment Implications: Structural opportunity persists under sustained AI capex; investors may track optical module shipment volumes and new customer acquisition as leading indicators—and adopt balanced allocations to mitigate systemic sector risk.

IV. Project & Market Updates

1. Trump signed two executive orders to accelerate development of advanced quantum computers.

2. 21Shares co-founder: Tokenization hype is ahead of Wall Street’s actual readiness.

3. Jeff Walton, Chief Risk Officer at Strive, stated that digital credit products linked to the Strategy Bitcoin ecosystem (STRC and SATA) rebounded partially after suffering sharp sell-offs last week—attributed to leveraged liquidations and heavy selling pressure—not deterioration in underlying credit quality.

4. The U.S. Senate passed a housing bill 85–5, including a four-year ban on central bank digital currency (CBDC) issuance by the Federal Reserve System or its member banks—extending through year-end 2030 and prohibiting creation or issuance of any digital asset substantially similar to a CBDC.

5. SpaceX (SPCX.O) signed a compute agreement with U.S. AI startup Reflection, valued up to $6.3 billion.

6. Alphabet subsidiary Google will invest ~$75 million in independent film studio A24 and establish a new AI research partnership. A24’s recent releases include Backrooms and Marty Supreme.

7. Micron Technology (MU.O) entered a memory and storage supply agreement with Anthropic to advance next-generation AI at scale.

8. Regulatory filings show Strategy issued 2.7148 million MSTR shares between June 15–21, raising net proceeds of ~$335.5 million—used to purchase 520 BTC at a total cost of ~$34.9 million, averaging ~$67,100 per coin. As of June 21, Strategy held ~847,363 BTC, with cumulative purchase costs of ~$64.1 billion and an average buy-in price of ~$75,700 per coin. Concurrently, the company added ~$300 million to its U.S. dollar reserves, bringing them to ~$1.4 billion.

V. Today’s Market Calendar

June 23 (Tuesday)

- U.S. Economic Data: S&P Global Flash Manufacturing & Services PMIs (monitor economic activity resilience).

- U.S. Earnings: FedEx (FDX), Carnival (CCL), KB Home (KBH), etc. (logistics, consumer sectors).

June 24 (Wednesday)

- U.S. Economic Data: May New Home Sales, Leading Indicators, etc.

- U.S. Earnings: Micron Technology (MU) reports after-market hours—a major event (memory chip leader; critical validation of AI server HBM demand); Trip.com Group (TCOM), etc. ★★★★

- Other Key Events: NVIDIA (NVDA) Annual Shareholders Meeting (9:00 AM PT)—focus on Blackwell & Vera architecture ramp-up and AI infrastructure outlook.

June 25 (Thursday)

- U.S. Economic Data: May PCE Price Index (Fed’s preferred inflation gauge; core PCE forecast: +0.3% MoM); Q1 GDP Final Estimate (forecast unchanged at 1.6%); Durable Goods Orders, Initial Jobless Claims, etc.—data-heavy day. ★★★★

- U.S. Earnings: BlackBerry (BB) pre-market earnings

June 26 (Friday)

- U.S. Economic Data: University of Michigan Consumer Sentiment Final Reading; Fed official speeches (Williams, Kashkari, etc.).

*This Week’s Core U.S. Equity Themes:

“AI Validation + Inflation Data Week”: Micron’s earnings will test AI memory/HBM demand strength and Blackwell supply ramp; NVIDIA’s AGM offers capacity and roadmap guidance; PCE data directly influences post-Warsh Fed policy expectations (hot prints may reinforce hawkish signals and delay rate cuts). Combined with post-IPO performance of SpaceX (SPCX), AI, tech infrastructure, and macro sentiment will drive markets.

Institutional Views: Leading investment banks observe that the U.S.-Iran 60-day sanctions exemption has introduced supply relief expectations into oil markets—pushing hedge fund short positions to elevated levels—yet low strategic petroleum reserves and negotiation uncertainty continue to support oil price volatility. Though the tech sector faces talent mobility and valuation headwinds (e.g., SpaceX pullback, GOOGL adjustment), robust AI infrastructure demand and semiconductor index record highs reflect enduring structural strength. RBC and others maintain that U.S. equities can absorb moderate rate hikes—S&P 500’s 18% rebound from lows confirms resilience. Crypto markets trended upward amid ETF inflows and large-holder accumulation, yet liquidation risks signal near-term caution. Overall, geopolitical easing and Fed policy path remain pivotal variables—investors should prioritize data validation and seek opportunities amid growing dispersion.

Disclaimer: The above content was compiled using AI-powered search tools and verified manually prior to publication. It does not constitute investment advice. Data herein may contain unavoidable inaccuracies—please rely on real-time market data for decision-making.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News