Escalation of the U.S.-Iran Conflict: How Prediction Markets Price War Risk Before Oil Prices Do

TechFlow Selected TechFlow Selected

Escalation of the U.S.-Iran Conflict: How Prediction Markets Price War Risk Before Oil Prices Do

Geopolitics is being financialized in real time; markets do not merely react passively to events but actively participate in pricing the risks themselves as those events unfold.

Author: CoinW Research Institute

Executive Summary

This article uses the escalation of U.S.-Iran tensions as a starting point to analyze how a geopolitical event can rapidly transform into a global risk variable within today’s financial system. Since the incident occurred over the weekend—when traditional financial markets were closed—on-chain markets remained operational. Cryptocurrencies and on-chain commodity derivatives were the first to exhibit sharp volatility, delivering the initial expression of risk; prediction markets, meanwhile, directly probabilized war and political developments, enabling real-time pricing of potential event trajectories. When traditional markets reopened on Monday, energy prices, the U.S. dollar, U.S. Treasuries, and risk assets collectively confirmed the risk—transmitting the risk premium systematically across macroeconomic channels. The article argues that in a 7×24 digital market environment, risk is no longer priced only upon the opening bell. Geopolitics is being financialized in real time: markets are not merely reacting passively to events—they actively participate in pricing risk *as events unfold*.

1. Escalation of Conflict: How a Geopolitical Event Becomes a Global Risk Variable

Recently, tensions between the U.S. and Iran escalated sharply. Multiple media outlets reported that Ayatollah Ali Khamenei, Iran’s Supreme Leader, was killed in an airstrike—triggering a rapid deterioration in regional stability. The combination of military action and hardline rhetoric quickly transformed localized friction into a globally watched crisis.

Subsequently, the Islamic Revolutionary Guard Corps (IRGC) announced restrictions on vessel passage through the Strait of Hormuz. As one of the world’s most critical energy transport corridors—carrying roughly one-fifth of global crude oil and liquefied natural gas shipments—the strait faced serious disruption risks. Several shipping companies suspended transit or opted for alternative routes.

The conflict’s impact now extends well beyond the military domain. As the core region for global energy supply, any disturbance in the Strait of Hormuz directly elevates the energy risk premium—and transmits swiftly to global markets via oil prices, inflation expectations, and capital flows.

Hence, this conflict has become a systemic global risk variable—not only reshaping regional security architecture but also disrupting energy supply-demand equilibrium, the U.S. dollar’s liquidity environment, and the valuation framework for risk assets.

When war rises to the level of systemic risk—where is that risk first traded? In a structural context where traditional markets operate on fixed hours while on-chain markets run continuously, the sequence of price discovery is shifting.

2. The Weekend Window: On-Chain Markets Complete First-Round Price Discovery

Notably, this escalation occurred over the weekend. When news broke, most traditional financial markets worldwide were already closed: spot gold trading paused, crude oil futures halted, and equity markets shut down. Risk had emerged—but the traditional system could not price it instantaneously. On-chain markets, however, remained open, absorbing risk sentiment into an active pricing venue.

Cryptocurrencies Lead with Sharp Volatility

Following the news, Bitcoin’s price briefly approached $63,000 before rebounding near $66,000—completing pronounced intraday swings. This volatility was neither simple safe-haven buying nor panic selling; rather, it reflected concentrated market consensus on risk expectations in the absence of traditional anchors like gold or crude oil. When other assets were unavailable for trading, crypto markets served as one key outlet for expressing risk sentiment.

On-Chain Commodity Derivatives: Instant Risk Premium Formation

Over the weekend, multiple media reports indicated significant price increases for perpetual contracts linked to crude oil, gold, and silver on Hyperliquid: crude oil perpetuals rose ~5% to ~$70.60/barrel; gold perpetuals rose ~1.3% to ~$5,323/oz; silver perpetuals rose ~2% to ~$94.90/oz. Trading volumes also expanded notably: silver contracts recorded over $227 million in 24-hour volume, while gold contracts reached ~$173 million—demonstrating genuine capital participation. These are real prices formed on 24/7 on-chain markets, reflecting participants’ immediate assessment of supply risks and geopolitical premiums during traditional market closures.

Monday Open: Traditional Markets “Catch Up”

Upon reopening, traditional markets rapidly adjusted toward weekend on-chain levels. International oil prices opened higher on Monday—Brent crude briefly hit $82.37/barrel, while WTI surged above $75/barrel; spot gold breached $5,300/oz; major global equity index futures broadly weakened, pressuring risk assets. Prices followed a clear temporal sequence: risk emerges over the weekend; on-chain markets move first; traditional markets confirm and amplify the signal on Monday.

During traditional market closures, on-chain markets absorbed the first wave of risk expression. This structural timing gap is altering the global rhythm of risk-event pricing.

3. Prediction Markets: War Is Priced in Real Time—For the First Time

Polymarket: Explosive Pricing at Conflict Inflection Points

In this episode, trading volume surged markedly for conflict-related contracts on the on-chain prediction platform Polymarket.

The series of contracts titled “Will the U.S. or Israel strike Iran by…?” (U.S./Israel strike Iran by…?) accumulated over $500 million in total trading volume—with ~$90 million traded alone on the day of the airstrike—making it among the largest geopolitical markets in the platform’s history.

After confirmation of the Supreme Leader’s death, the contract “Will Khamenei lose his position as Supreme Leader of Iran by March 31?” (Khamenei will lose position by March 31?) settled rapidly, with ~$57 million in trading volume. Longer-term political trajectory contracts—including “Will the Iranian regime fall by June 30?” (Iran regime collapse by June 30?)—saw their implied probability spike close to 50%, indicating markets were already pricing deeper institutional risk. These figures suggest betting activity was not fragmented but instead represented concentrated, high-intensity capital participation.

Source: https://polymarket.com/event/khamenei-out-as-supreme-leader-of-iran-by-march-31

Opinion: Multi-Dimensional Pricing of Conflict Pathways and Institutional Risk

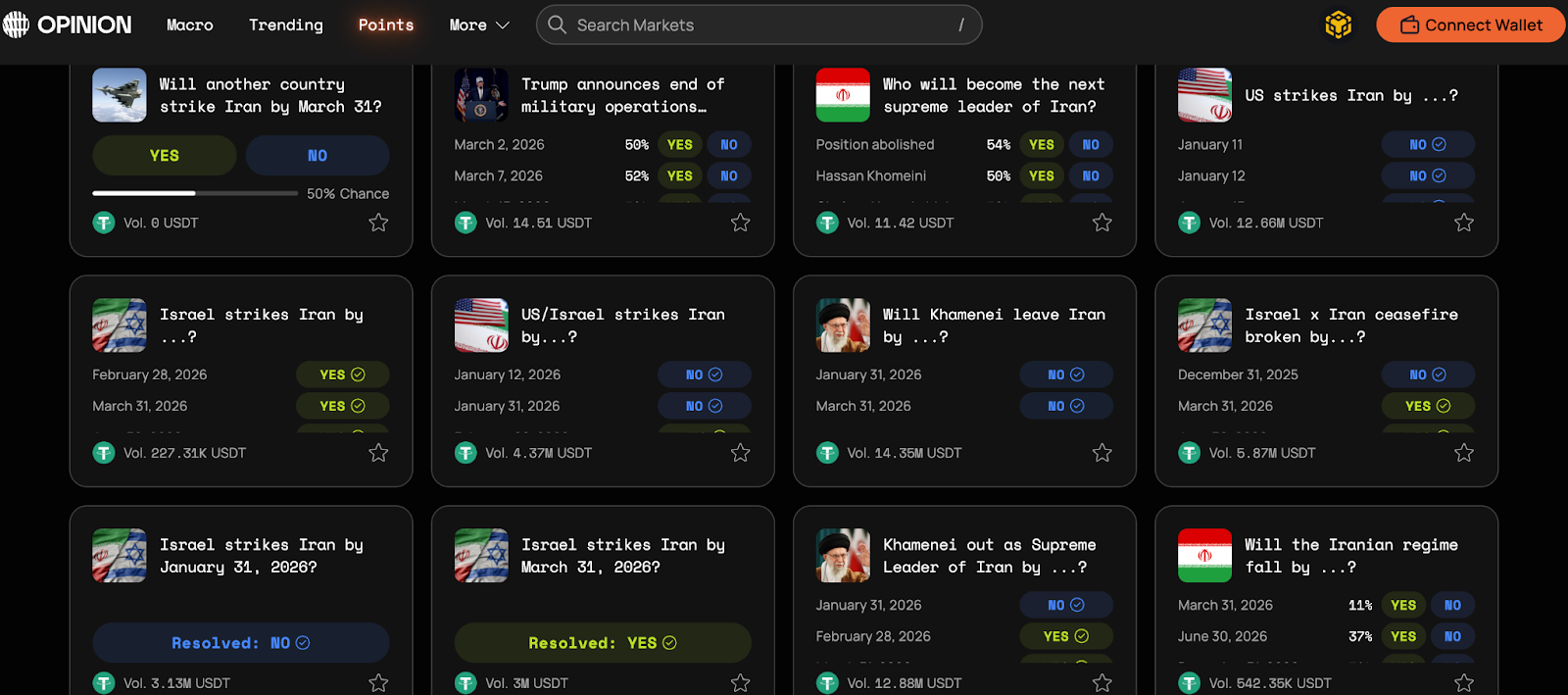

On Opinion, contracts related to the U.S.-Iran conflict likewise showed elevated activity. One category precisely defines military triggers. For example, the contract “US strikes Iran by …?” specifies that “Yes” is triggered only if U.S. forces physically strike Iranian territory or official diplomatic premises using drones, missiles, or aerial bombardment—intercepted weapons or other forms of military activity do not count. This contract has already traded over $12.6 million, revealing intense market focus on specific military thresholds.

Source: https://app.opinion.trade/search?q=Iran

A second category focuses on institutional risk. The contract “Khamenei out as Supreme Leader of Iran by …?” prices whether Ali Khamenei loses power within a specified timeframe. Settlement rules include resignation, detention, removal from office, or incapacity to perform duties—and rely on credible media consensus for final determination. Its trading volume stands at ~$12.9 million. Similarly, markets such as “Will the Iranian regime fall by …? (‘Will the Iranian regime fall before [date]?’)” and “Israel × Iran ceasefire broken by …? (‘Will the Israel-Iran ceasefire be broken before [date]?’)” probabilistically express regime stability and ceasefire durability, respectively.

Although the number of contracts and aggregate trading volume on Opinion remain lower than those on Polymarket, Opinion displays a clearer risk-layering structure: military action, ceasefire status, leadership continuity, and regime trajectory are decomposed into distinct, concurrently priced variables. War is thus no longer a binary “will it happen?” question—but a segmented, quantifiable, and continuously updated risk pathway. Prediction markets here function as real-time measurement tools for sovereign and institutional stability.

Probability Curves as a “Risk Thermometer”

Unlike crude oil or gold, prediction markets do not indirectly express risk through asset prices—they directly probabilize the occurrence of events. When escalation probability rises, odds jump; when tensions ease, probabilities decline. The odds curve itself becomes an instantaneous gauge of risk sentiment. Analysis suggests that several hours before widespread dissemination of the airstrike news, a small cluster of new wallets collectively purchased relevant contracts—and exited profitably after event confirmation. This pattern has sparked debate over whether information leaked into markets early—and underscored the exceptional time sensitivity of prediction markets.

Traditional markets typically reflect outcomes via rising oil prices or falling equities; prediction markets trade directly on “Will it escalate?” or “Will it spread?” The former prices consequences; the latter prices pathways. While traditional markets remain closed, risk is already quantified and wagered on-chain.

4. Traditional Asset Opening Confirmation: How Does the Risk Premium Transmit?

While on-chain markets move first, true cross-asset linkage occurs only after traditional markets reopen.

Energy: The First Stop for Risk Premium

Energy remains the first stop for risk premium transmission. With the Strait of Hormuz handling ~20% of global crude oil shipments, any market concern about disrupted supply immediately feeds into oil prices. Conflict escalation pushes oil higher, lifting inflation expectations—and thereby influencing monetary policy and corporate cost structures.

U.S. Dollar and U.S. Treasuries: The Tug-of-War Between Safety and Inflation

Under rising uncertainty, capital typically flows toward the most liquid assets—boosting short-term demand for the U.S. dollar and Treasuries. A stronger dollar and temporarily lower Treasury yields reflect heightened safe-haven demand. Yet if conflict persists and inflates inflation expectations, Treasury yields may face competing pressures—safe-haven buying versus inflation-driven sell-offs.

Risk Assets and Bitcoin’s Positioning

Gold fulfills its traditional safe-haven role; crude oil reflects risk premium; Treasuries offer liquidity safety. Bitcoin’s behavior, however, aligns more closely with highly elastic risk assets. Early in the conflict, it did not rise unidirectionally—it oscillated violently, signaling acute sensitivity to both liquidity conditions and risk appetite. Thus, in the earliest phase of extreme uncertainty, Bitcoin behaves more like a high-beta risk asset than a pure safe-haven instrument.

Overall, on-chain markets lead risk expression; prediction markets probabilize risk; traditional assets confirm systemically upon reopening. The risk premium then propagates layer by layer—from energy, to interest rates, to asset valuations—culminating in coordinated global market reactions.

5. Structural Shift: Is the Risk-Pricing Mechanism Migrating?

The significance of this event may lie less in the conflict itself—and more in *how* risk is being priced.

Geopolitics Is Being Financialized in Real Time

In the past, geopolitics resided largely in news headlines and diplomatic forums. Today, it is being financialized in real time: whether war escalates, sanctions land, or elections evolve—all can be wagered on, hedged against, and probabilized. Risk is no longer interpreted only after the fact—it is traded *as it unfolds*.

On-Chain Markets Are Becoming 7×24 Risk Buffers

On-chain markets are assuming a new functional role. Traditional markets observe weekends and holidays—creating periodic gaps where major events cannot be priced instantly. On-chain markets, operating 7×24, absorb the first wave of emotional release. Prices and probabilities shift there first—then traditional markets confirm and scale the reaction upon reopening.

Price Discovery Authority Is Marginally Shifting

This temporal asymmetry is driving a deeper structural change: a marginal migration of price discovery authority. If on-chain contracts move first—if prediction-market odds curves jump ahead of oil prices and equity indices—will institutional investors begin monitoring these signals? Will macroeconomic models incorporate on-chain volatility as a reference variable? Will journalists and traders treat prediction-market probabilities as early-warning risk indicators?

No definitive answers exist yet—but the direction is clear. The “first expression” of risk is shifting away from the opening bell of traditional exchanges—and toward always-on digital markets. When war becomes tradable in real time, markets cease being passive responders to event outcomes—and instead actively co-author the pricing of risk itself.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News