Crypto analysts talk: Bitcoin bottom is taking shape, smart money starts buying ahead of the 2026 market

TechFlow Selected TechFlow Selected

Crypto analysts talk: Bitcoin bottom is taking shape, smart money starts buying ahead of the 2026 market

The market may have underestimated the scope for rate cuts, and there will be more rate cuts next year than the market currently expects.

Compilation & Translation: TechFlow

Guest: Fabian, Crypto Analyst

Host: Miles Deutscher

Podcast Source: Miles Deutscher Finance

Original Title: Smart Money Is Front-Running Bitcoin 2026 (You’re Not Bullish Enough)

Air Date: December 6, 2025

Key Takeaways

In this episode of the podcast, Miles Deutscher dives deep into Bitcoin's reaction to market fear sentiment, suggesting it may signal the early stage of a liquidity cycle in 2026. He also explores how institutions, sovereign funds, and major market participants are actively positioning themselves ahead of a potential bull market expansion. Together with Fabian, they analyze the macroeconomic forces driving Bitcoin, Ethereum, and the broader crypto market, uncovering the real competitive advantages quietly forming within the altcoin sector.

Highlights Summary

-

Panic selling in the market is nearing its end.

-

The four-year cycle never truly existed.

-

Rate cuts are essentially a done deal.

-

Some sovereign funds are waiting on standby, gradually accumulating at 120,000 and 100,000; I know they bought more at 80,000.

-

The core driver of the Bitcoin market is liquidity, not lines on technical charts or indicators like the 50-day moving average. Bitcoin is essentially a "liquidity sponge" that absorbs liquidity from the market.

-

The market may be underestimating the room for rate cuts—there will likely be more cuts next year than currently anticipated.

-

Current market performance is more closely tied to macroeconomic conditions than internal Bitcoin events.

-

We are currently in a bottoming phase, and over the coming months or even quarters, the market is more likely to break upward rather than continue declining.

-

After significant market volatility, when prices first rebound to key resistance levels, there will inevitably be selling pressure. What truly matters is how the market reacts to these key levels—not just whether prices break through or fall below them.

-

Banks gradually opening up cryptocurrency access to clients is a long-term global trend.

-

Financial institutions will ultimately have no choice but to compromise and join the crypto trend—it has become inevitable.

-

If you're a nation or sovereign fund looking to accumulate Bitcoin, you certainly wouldn't announce it publicly at first—you'd wait until you're satisfied with your position size, or perhaps never disclose it at all, to avoid being front-run.

-

Bitcoin is increasingly becoming an attractive long-term diversification tool.

-

Bitcoin-backed loans could be a sign of Bitcoin as an asset class gradually gaining legitimacy.

-

The main source of selling pressure for Ethereum comes from treasuries—if they continue holding, ETH may outperform in the short term.

-

A notable advantage of prediction markets is that they allow you to trade the same underlying assets as traditional markets, but without liquidation risk.

-

The trading logic in prediction markets is simply “yes” or “no”—this simplicity lowers the investment barrier and reduces unnecessary risks.

-

Prediction markets represent a very fundamental yet effective form of market trading, especially in areas with lower liquidity such as pre-market trading—they may currently be one of the best examples of product-market fit in the crypto space.

Psychological Characteristics of Bitcoin Bottom Formation & Analysis of Extreme Selling Indicators

Miles: The past week was filled with negative news, yet the market’s reaction remained relatively stable. Typically, FUD often marks the bottom of the crypto market—for example, China banning Bitcoin, negative Tether news, or Bank of Japan policy shifts—these events frequently precede local bottoms. This week, I gathered some evidence showing capital flows seem to have shifted from bearish to bullish. Of course, there are still caveats, such as potential DAT sell-offs and certain macroeconomic factors.

Overall, based on available information and from a probabilistic standpoint, I believe a bottom may have already formed. What do you think—do you believe Bitcoin has bottomed?

Fabian:

My view aligns closely with yours—I believe the peak capitulation (referring to massive panic-driven selling) has passed. We mentioned this during Friday’s livestream as well. In fact, across multiple indicators, we’ve already experienced extreme levels of selling. At the start of this week (Monday), the market saw a slight pullback, dropping to the mid-high 80,000 range, primarily due to another wave of FUD.

Last weekend, concerns emerged over MicroStrategy’s financial health, Japanese government bond yields surged, and there were reports about China reiterating its negative stance on crypto again. These factors caused the market to open lower—but within just one or two days, prices quickly rebounded. As you said, I believe this indicates those who wanted to sell at current prices have largely finished doing so. In other words, panic selling in the market is nearing its end.

However, the bottoming process might be complex. Over the next few weeks or one to two months, prices may retest the lower end of the 80,000 zone, or even slightly break below. Overall, I believe we are currently in a bottoming phase, and over the coming months or even quarters, the market is more likely to break upward rather than continue falling.

Breakthrough and Challenges at Long-Term Resistance Levels

Miles: There are still significant resistance zones above current price levels. If we look at the daily chart, prices are attempting to break through upper moving averages; on the 4-hour chart, the Volume-Weighted Relative Price Point of Control (VRVP POC) remains around 96,000, forming a clear resistance area.

Although the market has seen a modest rebound recently, if we examine weekly charts and indicators like the 50-week simple moving average (SMA), prices remain below key levels near 102,000. Therefore, I consider the 95,000 to 100,000 range a difficult zone to overcome. Until we successfully break and hold above these resistance levels, I won’t fully commit to risk assets or altcoins, nor take on excessive risk. What’s your take?

Fabian:

I completely agree. My usual expectation is that after such large swings, when the market first rebounds to key resistance levels—especially convergence zones like the ones you mentioned—selling pressure is inevitable, at least in the short term. Whether the market can break through these levels in one go isn’t something I have a strong opinion on. However, overall, I believe market performance over the next few weeks or months will be relatively positive—prices may test higher levels before we assess the next move.

Beyond internal crypto catalysts (like turning capital inflows), we’re also seeing traditional finance (TradFi) return to risk-on mode. This provides external tailwinds for Bitcoin. For instance, the VIX index dropped sharply this week, and the dollar index (DXY) pulled back from its structural resistance at 100–101. Meanwhile, retail interest in high-momentum stocks (like Robinhood or robotics-related names) is returning. These signs indicate rising risk appetite. Still, whether Bitcoin can break current resistance in one go remains uncertain.

Miles: I agree. I think the market’s reaction to these key levels will reveal more comprehensive information—not just whether prices break through, but also observing capital inflow/outflow dynamics. For example, are ETFs turning net positive again? Is market sentiment improving? Can we see high-volume candles indicating investor interest at these levels—or is this just a brief “dead cat bounce”? So, what truly matters is how the market reacts to these key levels, not merely whether prices break or fail to break them.

Smart Money Positioning Strategies & Institutional Adoption Trends

Miles: Let’s now discuss major players in the market and the positioning strategies adopted by “smart money.” I’ve found that market positioning for 2026 is becoming particularly interesting—I believe “smart money” is well-prepared for future market developments.

First, let’s start with Bank of America. Recently, they officially recommended clients allocate 4% of their portfolios to Bitcoin and cryptocurrencies. I see this as reflecting a long-term trend: banks and financial institutions are gradually opening up to crypto assets. We’ll later touch on Vanguard’s shift, but overall, this change among banks has been significantly driven by deregulatory policies and the Trump administration. Fabian, what’s your view on banks gradually offering crypto access to clients?

Fabian:

I believe this is a long-term global trend, possibly lasting decades. It’s not just in the U.S.—we’ll see similar news globally. I even believe someday China will change its stance on crypto, though probably not today. Overall, the global adoption trend of Bitcoin and crypto is nearly irreversible—my overall assessment is “only up.” The Pandora’s box has opened, and regardless of future U.S. administrations (whether midterm or presidential elections), this trend won’t reverse.

The core issue now is how this global adoption trend interacts with supply bottlenecks. In Bitcoin’s early days, supply was concentrated among a few large players—early adopters or companies like MicroStrategy. As investors, we’re essentially trading the interplay between these two sources of liquidity. Additionally, I’ve noticed an interesting phenomenon: a divergence in sentiment between Crypto Twitter and traditional finance. Many in the crypto community feel pessimistic, believing the cycle is over, while traditional institutions see the current correction as a “buy-the-dip” opportunity. This long-term perspective is very positive for the market because traditional institutions are now the dominant force.

Miles: I fully agree—that’s why we may see Bitcoin reach new highs next year, possibly even a strong rally. Regarding “smart money” and institutional shifts, I’d specifically highlight Vanguard’s case. In 2024, Vanguard’s CEO explicitly stated they wouldn’t offer Bitcoin ETFs and wouldn’t change that stance. Yet just one year later, with a new CEO, they announced offering Bitcoin ETFs to 50 million clients. For a top-tier global asset manager overseeing $11 trillion, this shift is highly significant. How do you interpret this change?

Fabian:

This is essentially the path all major financial institutions will follow. Even leaders like Jamie Dimon of JPMorgan Chase, who once openly criticized crypto, now have no choice but to accept the trend. It’s effectively a “no-choice choice.” As public companies, their primary duty is to create value for shareholders and pursue profits. Ignoring the crypto market means missing out on enormous current and future revenue potential—and risking losing clients to competitors offering crypto products. So, regardless of political views or personal preferences, they must eventually compromise and join the trend—it has become inevitable.

Sovereign Wealth Fund Accumulation & Bitcoin’s Long-Term Structural Demand

Miles: Let’s talk about sovereign wealth fund positioning—it may be one of Bitcoin’s next major narratives. Today Larry Fink mentioned something about sovereign funds that I find particularly noteworthy.

Larry Fink: I can tell you some sovereign funds are standing by, gradually adding positions at 120,000 and 100,000—I know they bought more at 80,000. They’re building long-term positions.

He said he knows these funds bought heavily around 80,000, which explains the strong market reaction we’ve seen at this level. Clearly, big players have stepped in here.

Regarding the sovereign wealth fund narrative, I think the market talks a lot about ETFs and retail investors—even company ETFs—but hasn’t paid enough attention to sovereign fund accumulation. I’ve heard rumors that the Trump administration might designate Bitcoin as strategic reserves, though that plan hasn’t fully materialized. While they retained seized Bitcoin, there’s no plan to significantly increase reserves.

This leads me to a point: if you’re a nation or sovereign fund wanting to accumulate Bitcoin, you definitely wouldn’t announce it upfront—only once you’re satisfied with your holdings, or perhaps never at all, to avoid being front-run. You’d accumulate quietly. As these funds keep buying, downside moves will gradually shrink and volatility will decline—but they may never admit it. That’s what I find fascinating. Fink knows these big players—maybe some countries are secretly accumulating Bitcoin. What’s your take on this sovereign Bitcoin narrative? I think it’s underdiscussed, yet clearly a major reason why Bitcoin is maturing as an asset and becoming less volatile.

Fabian:

Absolutely—this perspective is very insightful. Over the past few decades, most national central banks and sovereign wealth funds primarily held two types of assets: U.S. assets (like U.S. equities) and government bonds (domestic or foreign, mostly U.S. Treasuries).

Yet both assets’ safety and diversification capabilities have come under scrutiny in recent years. Treasury performance since 2020 has been poor, and countries overly exposed to U.S. assets face systemic risks when the U.S. economy struggles. Hence, we’re seeing increasing numbers of central banks and sovereign funds seeking diversified allocations.

Right now, high-quality alternative assets are limited. Emerging markets carry higher risk and uncertainty, while commodities still see gold as the mainstream choice. However, Bitcoin is gradually becoming an attractive long-term diversification tool. Though sovereign wealth funds may not rapidly scale up Bitcoin holdings like traditional assets, the shift from zero allocation to gradual accumulation has begun—and this trend may continue over the coming years.

Miles: It’s not just BlackRock and Vanguard—even JPMorgan is now offering structured Bitcoin products based on IBIT to institutional clients. These products not only deliver strong returns during major Bitcoin rallies but also include downside protection and risk control parameters. These tools start with Bitcoin ETFs, then evolve into more complex derivatives—such as Bitcoin-backed bonds, a completely new use case we’ve never seen before.

Going further, if these tools mature, could we see Bitcoin-backed mortgage loans? I believe this signals Bitcoin as an asset class gradually gaining legitimacy. While this trend is underway, it evolves slowly, not overnight. You might feel pessimistic when Bitcoin drops to 80,000, 70,000, or 90,000—but long-term, the trend is crystal clear, which is why I remain a steadfast long-term Bitcoin holder.

Fabian:

Absolutely. This reminds me of MicroStrategy’s statement earlier this week—they’re considering borrowing via Bitcoin collateral. Based on that, I believe Bitcoin lending markets could become an entirely new vertical, growing rapidly over the next few years.

Miles: Yes, but do you know why MicroStrategy is doing this? In my view, their goal is to avoid MSCI (MSCI Inc.) downgrade risk—i.e., being removed from relevant indices. Their way of avoiding downgrades is by introducing more sophisticated financial instruments like bonds or lending products, thus no longer appearing as a passive fund. If a company merely holds Bitcoin without revenue-generating operations, it risks being classified as a fund. But by activating part of their Bitcoin holdings, they can be redefined as a revenue-generating business, thereby avoiding downgrade risks.

Fabian:

Another theory is that this gives them greater financing flexibility. If Bitcoin assets face potential downside risk, shifting more debt onto them helps better protect the company. This strategy essentially enhances the firm’s resilience during market volatility.

Macro Factors Favorable to the Crypto Market

Miles: Before diving deeper into core market drivers, I want to share breaking news: Eric Trump’s “American Bitcoin” fund just purchased $34 million worth of 363 Bitcoins. Continued Bitcoin purchases by the Trump family send a clearly positive signal to the market. As long as the Trump family retains political influence, this support will benefit the market.

Fabian:

Exactly—this clearly shows their pro-Bitcoin stance remains unchanged. While this purchase alone isn’t large enough to directly move the market, it sends a clear message: their position hasn’t changed, and I expect this trend to continue as long as they maintain political influence.

Additionally, I believe as midterm elections approach, they may increase supportive rhetoric toward crypto to re-engage voter support. Last year, during their campaign, they tried to win over the crypto community because data showed a significant portion of U.S. voters hold Bitcoin—a group potentially pivotal in election outcomes. Though exact figures may be unclear, the crypto community has gone through a volatile period since then. I expect they’ll boost market confidence by supporting Bitcoin and crypto before the election—we’ll have to wait and see.

Analysis of Macroeconomic Trends in 2026

Miles: Ultimately, the core driver of the Bitcoin market is liquidity, not lines on technical charts or indicators like the 50-day moving average. Bitcoin is essentially a “liquidity sponge” that absorbs market liquidity. In the current environment, Bitcoin remains a risk asset, and risk assets typically perform well when liquidity is abundant and macro conditions favor risk-taking.

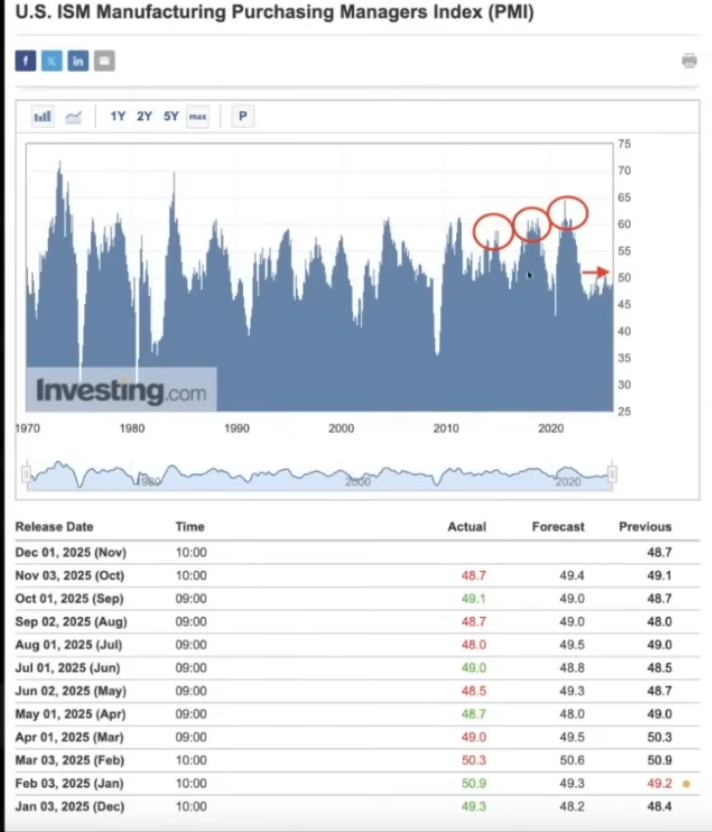

ISM Manufacturing Index & Business Cycle Outlook

Miles: To determine whether the market will be bullish in 2026, we must analyze from a macro perspective. Let’s start with the ISM Manufacturing Index (a key economic indicator tracking the business cycle). Current ISM levels are much lower than in previous cycles, and Bitcoin typically begins rising ahead of ISM improvements. Nevertheless, ISM is expected to rebound in the future. Looking back at the past three cycles, Bitcoin only peaked when ISM exceeded 55—in other words, Bitcoin’s rally hasn’t truly begun yet.

To understand whether 2026 will ultimately be bullish, we need to examine macro positioning—which is your specialty. First, I’d like to discuss ISM. I know Raoul Pal often talks about this—the ISM index is currently much lower than in past cycles, and Bitcoin typically leads ISM, hence its strong performance. But a rebound is expected. Looking at the past three cycles, Bitcoin only topped when ISM surpassed 55. It hasn’t really started its big run yet.

Raoul Pal (CEO of Real Vision) argues that the ISM index will rebound in the first half of 2026, alongside looser liquidity conditions, making this the key trigger for Bitcoin’s next leg up. Do you monitor this indicator?

Fabian:

ISM is a macro indicator I watch very closely. It reflects overall U.S. economic growth and the business cycle, but it’s relatively lagging—and the business cycle itself lags behind the liquidity cycle, which is the leading indicator for all these economic activities. They’re closely linked.

As you mentioned, although there may be some concerns about the liquidity cycle over the next few years, at least in the first half of next year—over the coming quarters—we’re likely to see significant improvement in global liquidity, especially in the U.S. This liquidity expansion usually drives growth and business cycle recovery, eventually flowing into all risk assets including Bitcoin. So I think your view makes sense—at least over the next few quarters, I share your outlook.

Miles: We can observe that Bitcoin prices are typically highly correlated with ISM trends. For example, in the 2018 cycle, Bitcoin topped when ISM did. Although Bitcoin is influenced by other factors, ISM hasn’t reached its peak yet. If ISM starts to rebound, could this become the next catalyst for Bitcoin’s rise? This is one of the indicators we need to watch closely.

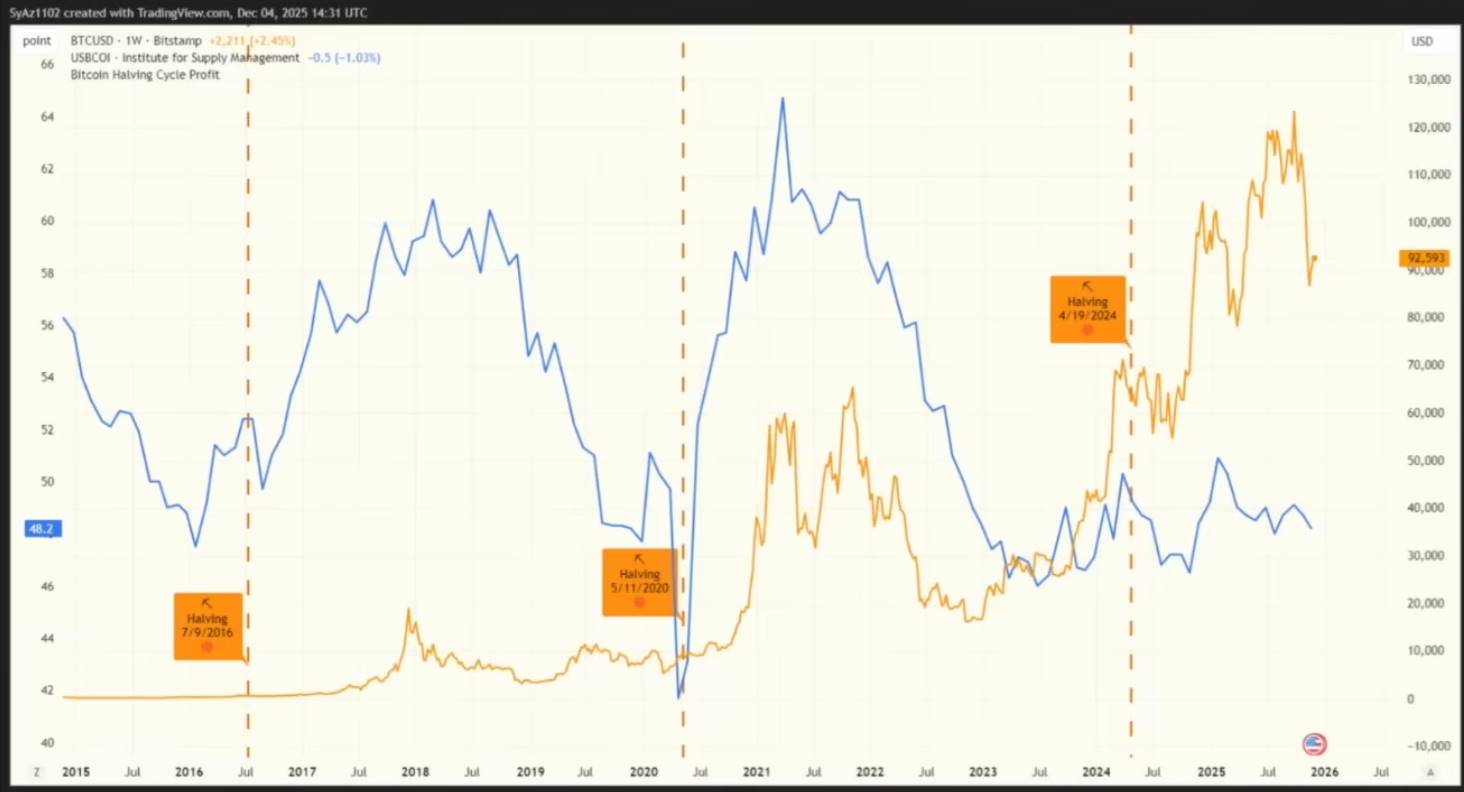

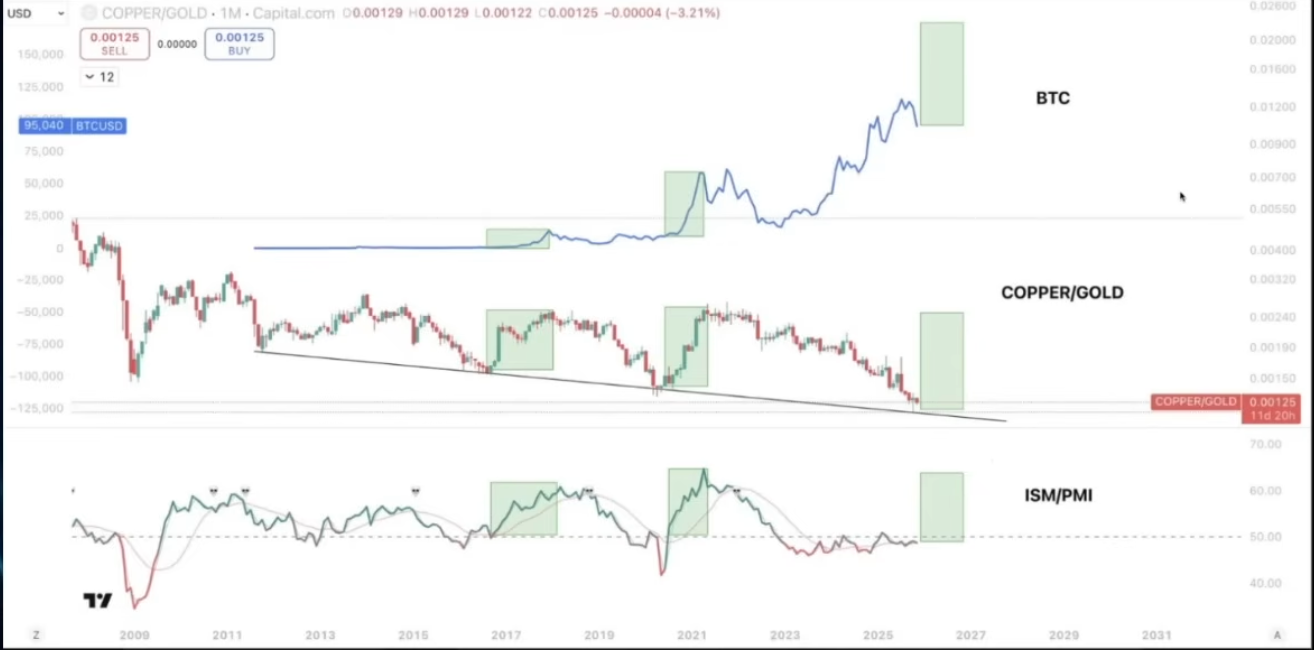

Additionally, other related indicators are worth noting, such as the copper-to-gold ratio, ISM PMI ratio, etc. These all seem to have rebound potential. When you begin analyzing this evidence, you realize the four-year cycle theory doesn’t actually hold. Many believe Bitcoin’s four-year cycle stems from halving events—but if so, why do the S&P 500, copper-to-gold ratio, and ISM all peak around the same time?

If the four-year cycle truly exists, does that mean Bitcoin’s halving cycle is more important than the entire U.S. manufacturing index or business cycle? That clearly defies logic. Bitcoin is just a small part of the business cycle. From my perspective, the four-year cycle never truly existed, and 2026 may prove this, completely dismantling the theory.

If Bitcoin can rebound in the first half of next year, it will fundamentally shift market perception. People will realize Bitcoin is a liquidity-driven asset, not one solely dependent on halving cycles. This cognitive shift could attract more investors, especially skeptics who previously believed in the four-year cycle theory.

Fabian:

In short, markets have never been that simple. We can’t rely on simplistic theories like the “four-year cycle” to predict market trends. As you said, the sample size for the four-year cycle is extremely limited—only two cycles (N=2)—clearly insufficient to draw strong conclusions. Moreover, these cycles coincided precisely with major macro inflection points in liquidity and growth cycles.

Furthermore, over time, the impact of Bitcoin halvings on price has significantly weakened. The supply reduction from halvings represents an ever-smaller proportion of total supply, while the main drivers have shifted to global and institutional capital flows. These flows are increasingly influenced by macroeconomic cycles rather than Bitcoin’s own halving events.

Therefore, I’ve never believed in the four-year cycle theory. Current market performance is more closely tied to macroeconomic conditions than internal Bitcoin events.

Repricing Expectations for Interest Rate Cuts

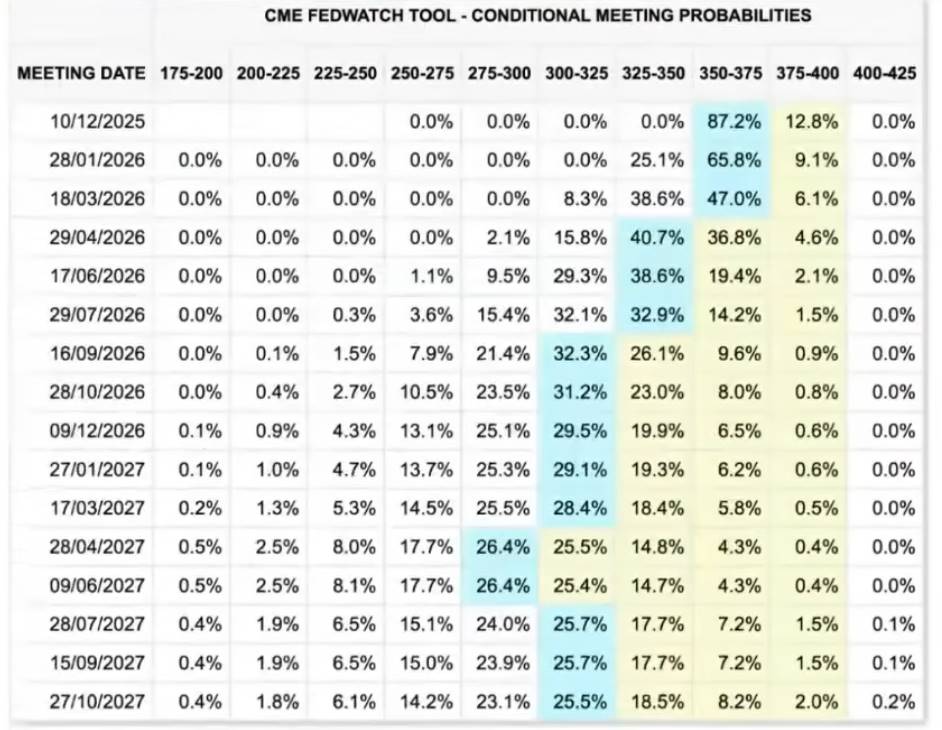

Miles: The probability of rate cuts at the next Fed meeting has risen sharply—almost considered a certainty. Multiple authoritative sources also suggest rate cuts are imminent. Have expectations around rate cuts changed this week? Or do you think this could become another market catalyst?

Fabian:

Rate cuts at this point are essentially a done deal. I had a similar view last week, but typically as we approach decision dates, implied probabilities increasingly lean one way. The Fed usually signals in advance, so we can be more confident about rate cut expectations.

The next question is, how much has the market already priced in this rate cut? Currently, U.S. equities are near all-time highs, while Bitcoin lags slightly—but it has its own unique issues. Therefore, I tend to view U.S. equities as a representative indicator of market pricing.

However, I believe even if the rate cut happens, Powell may take a more hawkish tone during the press conference. After all, at the October FOMC meeting, he stated they weren’t sure about cutting rates without sufficient economic data. Since then, key economic data hasn’t changed much. So to justify this rate cut, Powell might emphasize it’s a forward-looking move, but future cuts require more data. He might send a “hawkish cut” signal, warning the market not to expect too many further cuts.

This “hawkish cut” could cause short-term market volatility, but overall, I remain optimistic about the current setup. According to market pricing, only two more rate cuts are expected by the end of 2026, bringing the federal funds rate to around 3%. However, the Trump administration and potential Fed chair candidates like Bessent and Hasset have indicated they believe the federal funds rate should be closer to 2.5%, meaning the market may be underestimating the room for rate cuts.

Considering next year is a midterm election year, with the Fed board and chair rotating in May, I believe the market may repricing expectations, anticipating more cuts. This repricing would strongly support bullish risk assets. Even if Powell appears more hawkish at this meeting, I still believe there will be more rate cuts next year than currently expected.

Miles: You previously mentioned inflation—it has indeed declined. While YoY data still shows increases, according to True Inflation (a real-time inflation index), inflation has already retreated from local highs. This may also be a key reason behind current rate cuts.

I agree with you. If rate cuts materialize, this could become a potential bullish factor worth watching closely.

Regarding midterms, prediction markets suggest Democrats are more likely to win. From my understanding, Republicans may try to boost markets before midterms to win votes. Does this imply loose policies will persist? If Democrats win the House, what impact would that have? What’s your view?

Fabian:

First, in terms of direct impact, there is indeed a positive correlation between Republican victory odds and Bitcoin price. Republicans are generally seen as more crypto-friendly, pushing crypto-related legislation. If these bills don’t pass before midterms and Republicans lose power afterward, legislative progress could stall.

More interestingly, we do observe a certain synchronicity between changes in Republican victory probability and Bitcoin price. A few months ago, when Bitcoin topped, Republican victory odds also peaked. While other factors were at play, this correlation can’t be ignored.

On a deeper level, I believe the market has already priced in these political risks—perhaps even overreacted due to Bitcoin’s drop. Going forward, the Trump administration will face greater pressure to do everything possible to boost the economy and financial markets before midterms to improve their chances of winning, and these efforts could support risk asset gains in the first half of next year.

My forecast is the market may front-run these expectations, especially with the new Fed chair taking office in May 2026. These factors could become strong drivers for market upside. Of course, as midterms approach, uncertainty-averse markets may see increased volatility. But until then, these factors will provide clear tailwinds.

How the ETH/BTC Price Relationship Affects Other Cryptocurrencies

Miles: We may see Bitcoin peak in the first half of this year, with U.S. equities topping around the same time. What happens next requires us to continuously adjust strategies based on market dynamics. For now, we agree the overall setup is bullish.

Recently, we’ve seen the ETH/BTC exchange rate break upward for the first time in a long while. This is very interesting. More notably, this occurred amid weakening Bitcoin dominance. This is the first time I’ve seen Bitcoin dominance not rise despite weak market performance. What do you make of these two charts together? I think it might mean that even if Bitcoin prices flatline or rise slightly, altcoins could still outperform in this cycle. What’s your take?

Fabian:

This is a very interesting question—honestly, I’m conflicted. I have two seemingly conflicting views.

First, you’re right—ETH has indeed shown relative strength against BTC recently. But is this merely because ETH fell more from its peak than Bitcoin, and is now experiencing mean reversion? That remains to be seen—I currently lean toward viewing it as mean reversion.

That said, we’ve also observed BMNR (Tom Lee’s Ethereum DAT treasury company) buying large amounts of ETH weekly, even surpassing MicroStrategy’s Bitcoin purchases. This trend continues so far. Although I haven’t deeply analyzed BMNR’s specific operations, this sustained accumulation clearly supports ETH’s short-term performance. So as long as this buying persists, I believe ETH may perform exceptionally well in this rebound.

However, from a longer-term perspective, I remain cautious about ETH’s performance. Around 6% to 7% of ETH’s market supply is held by large treasury companies—far exceeding the proportion of Bitcoin held by MicroStrategy. If these treasuries are forced to sell in the future, it could cause a larger market shock. Additionally, ETH is perceived as a more volatile, lower-quality asset, making it less resilient. Thus, long-term, I still favor Bitcoin—I believe it will outperform.

Miles: Long-term, I agree. But from a short-term logic, I think you might also agree: if Bitcoin performs strongly in Q1 and Q2 this year—indicating favorable overall market conditions—then Ethereum may outperform Bitcoin. The reason is that Ethereum has less circulating supply, more supply held by DATs, and these institutions may accumulate more aggressively—this structural advantage could enable ETH to outperform in the short term.

Of course, if market conditions deteriorate, these tailwinds could quickly turn into headwinds—especially if concerns about centralization and potential sell-offs intensify, potentially becoming a catalyst for declines. But this phenomenon is reflexive—it also works during market rises, clearly benefiting alts. I hope we get to see this positive trend unfold.

Fabian:

You’re right—I’m fully open-minded. In the short term, Ethereum could indeed outperform Bitcoin—as long as these DATs don’t sell and continue accumulating, ETH has the potential to shine.

In contrast, Bitcoin currently faces some unique structural challenges. For example, miners may continue selling as they transition into AI data centers. Also, some early investors (OG holders) may keep selling—they tend to believe in the four-year cycle theory.

There are also potential tail risks, like Bitfinex’s Bitcoin debt issue. The U.S. government currently owes Bitfinex about 100,000 Bitcoins, which might be returned at some point. If these Bitcoins are liquidated and distributed to creditors, it would add extra selling pressure to the market.

In comparison, Ethereum’s main source of selling pressure comes from these treasuries—if they continue holding, I agree ETH may outperform in the short term.

Investment Opportunities and Alpha in Prediction Markets

Miles: Regarding prediction markets—this is a topic I plan to explore in depth over the coming weeks, as I’m experimenting with new things myself, like using AI to create automated trading bots, which will soon go public. But I know you’ve already had several months of hands-on experience in prediction markets, especially in pre-market trading. Could you share your experience and explain why you believe this is an investment area worth watching in the coming months?

Fabian:

Prediction markets are a very interesting space. I especially enjoy using them for pre-market trading, particularly in upcoming Pre-TGE (pre-token generation event) token markets. A unique advantage of prediction markets is that they offer investors a low-risk environment—ideal for shorting newly launched tokens that are overvalued by the market.

Based on experience over the past year or longer, we’ve found that pre-market trading often overvalues new tokens—most new tokens typically experience “down-only” price action post-launch, like Plasm recently. Many new tokens are overvalued pre-launch—such as Stable (an upcoming Plasma competitor, a stablecoin chain), ME, Monad (launched last week)—valuations clearly misaligned with market realities.

A key reason for this mispricing is that many investors hesitate to short these tokens in traditional pre-markets. In those markets, short sellers often face short squeezes, leading to massive losses. The advantage of prediction markets is they offer an option-like trading model—specifically put options. You can bet that a token’s price will be lower 24 hours after TGE, without worrying about intraday price swings or liquidation risk. This mechanism makes prediction markets an ideal tool for shorting overvalued tokens.

Over the past month, I’ve executed multiple trades on upcoming new tokens. For example, I bought the “No” option in Stable’s pre-market at 4B and 5B valuations—results were excellent. I also bought “No” options in Me and Monad’s pre-markets. This trading approach exploits mispricing discrepancies—an extremely efficient strategy. While many know how these tokens will perform post-launch, few can effectively act on this knowledge beforehand. Prediction markets offer a unique opportunity to capture this edge.

Miles: In traditional markets, when panic hits, many investors rush to sell positions, causing prices to drop rapidly. But in pre-market trading, investors can’t panic-sell because these trades are contract-based without spot selling mechanisms. Unless many investors enter shorts, pre-market price swings remain relatively small. Even if liquidation spikes occur, they often scare off some participants, further reducing market volatility.

A notable advantage of prediction markets is that they allow you to trade the same underlying assets as traditional markets, but without liquidation risk. I believe this is a crucial feature—and why prediction markets deserve deeper research.

Additionally, I find the simplicity of prediction markets very appealing. Compared to complex options trading on Deribit, prediction markets are far more intuitive. In options markets, you must consider strike prices, expiration times, premium costs, and portfolio structure for appropriate call/put allocation; perpetual contracts require understanding funding rate changes—complex factors unfriendly to average investors, where mistakes easily lead to high trading costs.

In contrast, prediction market trading logic is simply “yes” or “no.” If you believe the market’s implied probability is too low or too high versus your own view, you simply trade based on that—no need to consider other complexities. This simplicity lowers the investment barrier and reduces unnecessary risks.

I believe prediction markets will become a bigger trend in the future. In political and sports betting, they’ve already achieved great success—and in crypto, their potential is equally vast. I believe this is an area worth continued attention, as it offers investors more diverse choices beyond simply holding positions or basic buy/sell actions.

Prediction markets represent a very fundamental yet effective form of market trading, especially in lower-liquidity areas like pre-market trading—they may currently be one of the best examples of product-market fit (Product Market Fit) in the crypto space.

Fabian:

One overlooked advantage of prediction markets is that they can serve not just speculative purposes, but also function as hedging tools in many cases. For example, in pre-market trading, if you’re eligible for a token airdrop and already know the amount, but lack sufficient capital or don’t want to risk liquidation from shorting, you can use pre-market platforms to hedge partial risk. While this hedge may not fully cover exposure, it does offer a flexible and practical risk management method.

Moreover, prediction markets can help investors hedge political or geopolitical risks. For instance, if you believe Bitcoin’s price might be affected by major events, and there are relevant prediction markets—such as “Republicans lose the House in midterms” or “Satoshi transfers funds before 2026”—you can use these markets to hedge potential tail risks.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News