Airwallex CEO's Stand Against Stablecoins Sparks Backlash from Crypto Community: Who's Losing Out?

TechFlow Selected TechFlow Selected

Airwallex CEO's Stand Against Stablecoins Sparks Backlash from Crypto Community: Who's Losing Out?

Stablecoins have become a hot topic in the global financial world, and the founder of a cross-border payment unicorn, tired of being repeatedly questioned by investors, launched a direct attack on stablecoins—prompting swift rebuttals from multiple parties in the crypto community.

By Nancy, PANews

Stablecoins have become a hot topic in global finance, and the founder of a cross-border payments unicorn has lashed out at them after growing tired of investor questions.

Recently, a tweet from Airwallex CEO ignited a firestorm in the crypto community. In his statement, this traditional finance veteran questioned stablecoins' value in reducing foreign exchange costs, improving settlement efficiency, and practical applications in mainstream markets—revealing clear skepticism toward this emerging payment tool.

Unexpectedly, the remarks quickly drew sharp rebuttals from across the crypto space. From on-chain settlement efficiency to financial freedom in emerging markets and compliance progress, the comment section turned into a battleground between old and new payment systems.

This isn't just a clash of opinions—it reveals an accelerating restructuring of financial infrastructure. Stablecoins are no longer niche tools within crypto circles; they're now actively entering core scenarios of traditional finance, reshaping cost structures and settlement mechanisms while challenging the entrenched interests of intermediaries.

Airwallex CEO Publicly Questions Stablecoin Value, Faces Widespread Backlash

On June 8, Airwallex co-founder and CEO Jack Zhang openly expressed deep skepticism about the value of stablecoins.

"Investors keep asking me about stablecoins and how they can reduce FX fees—but if you’re sending USD to EUR and the recipient still needs euros deposited into their bank account, I don’t see how stablecoins reduce costs. Converting stablecoins to fiat off-ramps is often more expensive than traditional interbank FX rates," Zhang said in his post.

Zhang further admitted he’s never truly understood the cryptocurrency space, saying that unlike AI and other technologies, he hasn’t seen a single real-world use case for crypto in the past 15 years. To him, these purely financial products create no real societal value and amount to little more than zero-sum games. Even with lower volatility, he doesn’t believe stablecoins help B2B transactions—unless dealing with very obscure currencies that already suffer from poor liquidity.

He argued that for G10 currency transfers, existing financial systems like bank wires are already highly efficient, nearly free, and real-time, making it hard for stablecoins to offer competitive advantages. The cost of converting stablecoins into recipients’ local currencies far exceeds interbank FX transaction costs. While stablecoins might offer regulatory arbitrage opportunities in regions like Latin America or Africa, their edge in major currency transactions remains limited.

In response, Simon Taylor, Head of Strategy at compliance platform Sardine, countered that Zhang only sees surface-level fee comparisons and misses the bigger picture. According to Taylor, the value of stablecoins isn’t about lowering off-ramp or last-mile costs—they’re not just cheaper, but better. While stablecoins aren’t yet transformative financial infrastructure, they represent another viable option. He believes upcoming U.S. regulation could be the turning point that establishes stablecoins as legitimate financial rails.

Richard Liu, co-founder of Huma Finance, acknowledged that from the perspective of optimizing current FX flows, stablecoins may not add much. But he sharply pointed out: "Don’t fool yourselves into thinking you’ve minimized FX costs. Your customers still face high fees and access barriers—problems rooted in the system you rely on: an outdated and predatory banking infrastructure. Blockbuster once thought its cost structure was optimized too, but its business model was built on the wrong foundation—physical logistics. We all know how that ended. Stablecoins will drive the next wave of global payments—not as tweaks to legacy rails, but as a new paradigm built on entirely different architecture. Their rise doesn’t depend on participation from incumbents like Airwallex."

Matt Sorg, Technical Lead at Solana Foundation, shared real-world progress: euro-denominated stablecoins are gaining traction. Swapping USD to EUR stablecoins on-chain now costs only a few basis points. Issuers are building low-cost bridges from euro stablecoins to traditional bank accounts. While some intermediaries remain expensive, cheaper options exist—if you know where to look. Essentially, different players are tackling cost issues at every stage.

"You could even issue your own stablecoin. The revenue potential from stablecoins allows you to easily subsidize zero-fee on- and off-ramps while still making profits. Moreover, a parallel economic system already exists within crypto. Once dollars go digital, people can increasingly spend and use them directly in the crypto ecosystem. Many merchants are happy to accept USDC or USDT. Eventually, there’s no need to convert back to fiat. Transaction fees within this parallel system are also lower," suggested Stijn Paumen, co-founder and CEO of Helio.

Helio CEO mert shared his personal experience: a frustrating early encounter with Airwallex’s API for cross-border transfers pushed him toward crypto, reinforcing his belief in stablecoins as a viable alternative.

"When we offer 4% annual yield on stablecoins (risk-free), users lose incentive to cash out into fiat. This increases demand for dollars and weakens demand for euros. As the euro depreciates further, people prefer holding dollars—eventually creating a downward spiral until everyone uses only dollars. In the end, the euro becomes something Europeans buy only to pay taxes," said Mike Belshe, CEO of crypto custodian BitGo, highlighting what he sees as an enhanced dollar dominance effect driven by stablecoins.

Nic Carter, founding partner at Castle Island Ventures, directly criticized Zhang for having a shallow understanding of stablecoins, lacking both curiosity and basic comprehension.

Facing intense backlash from the crypto community, Jack Zhang later responded, acknowledging that stablecoin wallets can serve as alternative payment methods and improve liquidity in emerging markets—admitting they do have a place in finance. However, he maintained they lack disruptive significance at any level.

From Regulatory Periphery to Mainstream Stage: The Traditional Financial Pie Is Shrinking

Zhang’s critique actually reflects the broader confusion and instinctive resistance many traditional finance professionals feel toward the crypto world. To them, stablecoins aren’t quite money, nor clearly defined assets—they appear instead as ambiguous tools operating on the fringes of regulation. Yet this seemingly marginal instrument is rapidly stepping into the mainstream spotlight, beginning to erode the very foundations upon which traditional finance depends.

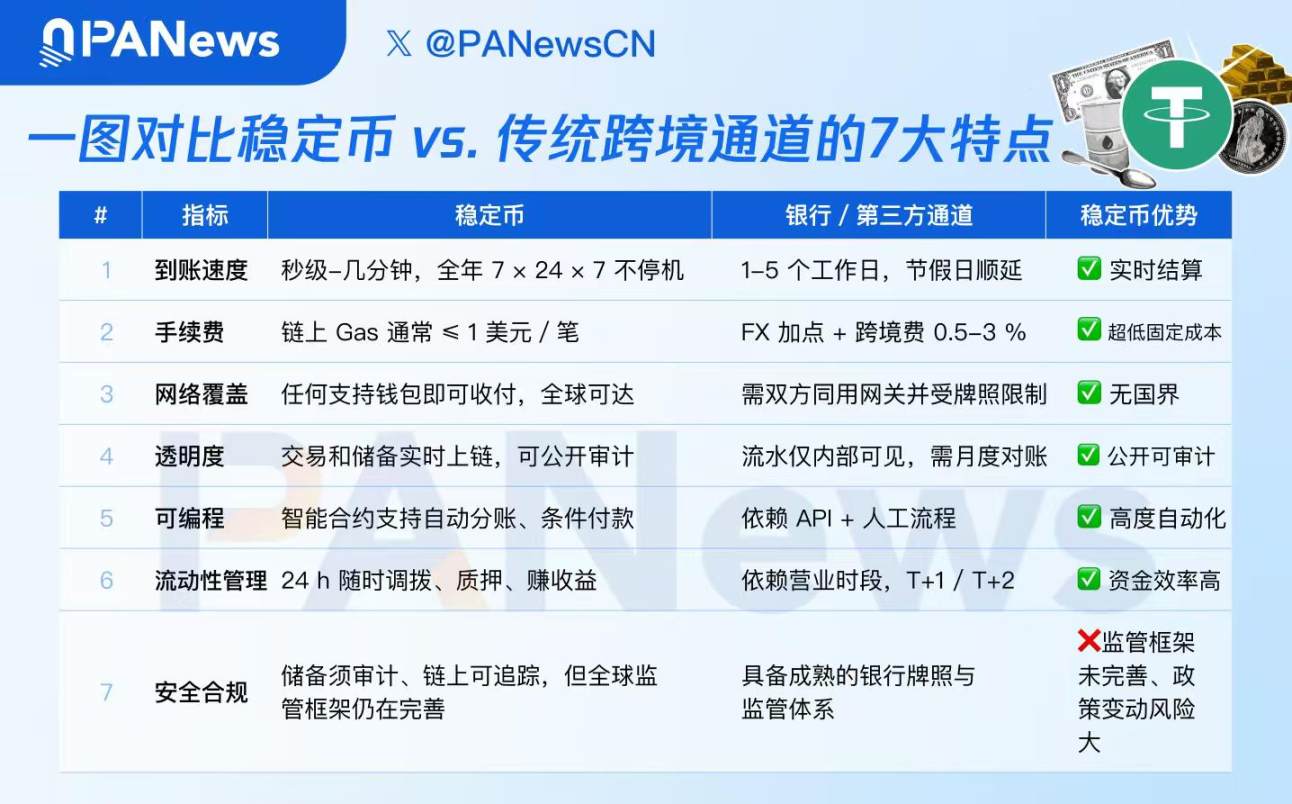

The core value of stablecoins goes beyond price pegging—it lies in the structural transformation they trigger. With features like instant on-chain settlement, global portability, and programmability, stablecoins inherently challenge the traditional “account-bank-clearing network” financial model through a form of technological disruption.

The impact on legacy systems is evident when examining cross-border payments. Traditional international transfers must navigate multiple banks, clearing networks, and FX markets, often taking days, costing significantly, and lacking transparency. In contrast, stablecoins enable peer-to-peer on-chain transfers and smart contract-based settlements, achieving real-time confirmation and full transaction visibility. This isn’t merely incremental improvement—it’s a paradigm shift: funds no longer depend on sovereign-backed banking networks but move directly between blockchain addresses on open networks.

More importantly, stablecoins break down geographic and accessibility barriers in financial services. Due to compliance costs, risk controls, and commercial constraints, over one billion people globally remain unbanked. Stablecoins empower individuals via the simple combination of smartphones, digital wallets, and internet access—granting rights to store value, make payments, conduct cross-border transfers, and participate in global finance. This enables true decentralized financial inclusion. Across Latin America, Africa, and Southeast Asia, growing numbers of users now rely on USDT and USDC for daily savings, salary disbursements, purchases, and small remittances. This is not merely "regulatory arbitrage," as Zhang suggests, but evidence of a new financial order taking root in underserved regions.

For this reason, the threat stablecoins pose to traditional fintech firms is fundamental.

Airwallex, for example, builds its business model around integrating into existing financial networks—leveraging bank accounts, SWIFT, clearing houses, and FX markets to route payments. Stablecoins bypass this entire framework, dismantling from the ground up the reliance on bank accounts, clearing institutions, and currency exchange networks. This means stablecoins are gradually compressing fintech profit margins—and once global compliance frameworks mature, the disruption will become systemic and irreversible.

Meanwhile, the global trend toward stablecoin regulation is turning them into legitimate competitors within traditional finance. Jurisdictions including the U.S., Hong Kong, Singapore, and the UAE are accelerating efforts to establish regulatory standards. For instance, the U.S. is advancing the GENIUS Stablecoin Act to formalize oversight; Hong Kong’s Stablecoin Ordinance takes effect August 1, marking a milestone for sustainable growth of its stablecoin and digital asset ecosystem. In this process, native-compliant crypto firms like Circle gain first-mover advantage, while traditional institutions lag due to rigid internal structures and technological shortcomings.

Equally significant is the rapid youth adoption of stablecoins. Gen Z and millennials, raised in digital-native environments, naturally embrace wallet usage, stablecoin payments, and smart contract interactions. These behavioral shifts are steadily eroding the moats long enjoyed by incumbent institutions.

Nonetheless, increasing numbers of traditional financial and tech giants are proactively embracing stablecoins. Deutsche Bank is exploring stablecoins and tokenized deposits, considering issuing tokens or joining industry consortia. Tech giants like Apple, X, and Airbnb are engaging with crypto firms to discuss stablecoin payment integrations. Uber is evaluating stablecoins to cut cross-border payment costs. Payment processor Stripe is working with banks to advance stablecoin payments. Spain’s Santander Bank plans to launch its own stablecoin and expand crypto offerings. These developments signal that stablecoins may become a pivotal force in the next phase of financial restructuring.

In summary, the debate sparked by Airwallex’s criticism highlights the intensifying clash between traditional and crypto finance. As regulatory progress accelerates and mainstream institutions begin active experimentation, stablecoins are evolving from fringe tools into a major force shaping the future of finance.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News