The Stablecoin Era Has Arrived: How Will China and the U.S. Compete?

TechFlow Selected TechFlow Selected

The Stablecoin Era Has Arrived: How Will China and the U.S. Compete?

It's not yet time for great power rivalry.

Author: Lu Aifang

On June 5, Circle, the issuer of the world's second-largest stablecoin USDC, listed on the New York Stock Exchange, with its share price surging 168% on the first day, becoming the new darling of capital markets.

Just at the end of May, both the United States and Hong Kong passed stablecoin bills in succession, introducing clear regulatory policies for stablecoins, allowing fiat-backed stablecoins—long operating in a gray area—to gain legal status and integrate with traditional finance.

Long-marginalized stablecoins have finally won mainstream acceptance, officially stepping onto the global economic stage. The era of stablecoins has truly arrived!

This article will explore: What is the current state of global stablecoin development and why are they rising so rapidly? How do the U.S. and Hong Kong stablecoin bills differ, reflecting their respective development strategies? And how will they compete?

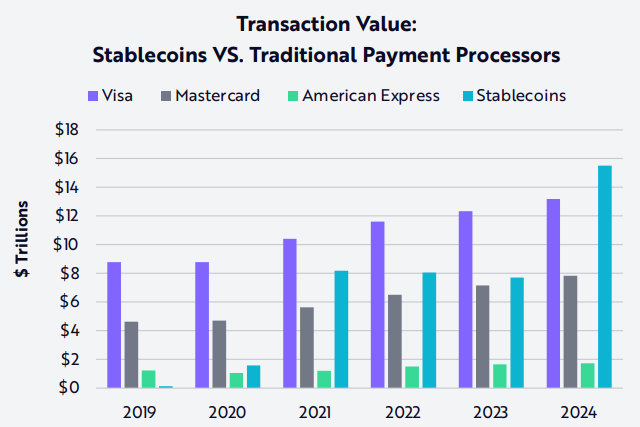

A key metric for measuring stablecoins is transaction volume, but data from different institutions vary:

ARK Invest’s February 2025 report, *Big Ideas 2025*, showed that stablecoin transaction volume reached $15.6 trillion in 2024—equivalent to 119% of Visa’s and 200% of Mastercard’s transaction volumes.

However, Visa’s CEO stated in a public speech that Visa’s transaction volume for 2024 was $16 trillion, suggesting that stablecoin transaction volume is already on par with Visa.

Another joint report by analytics firms Dune and Artemis indicated that between February 2024 and February 2025, total stablecoin transaction volume exceeded $35 trillion. However, after excluding inflated trading and bot activity, real stablecoin transaction volume was $5.6 trillion—about 40% of Visa’s volume.

Regardless of which dataset is used, they all demonstrate how fast stablecoins are growing. After all, it has only been ten years since Tether invented the first dollar-pegged stablecoin, USDT. In contrast, Visa, as a global payment network, has nearly 70 years of history and cooperates with over 20,000 banks worldwide.

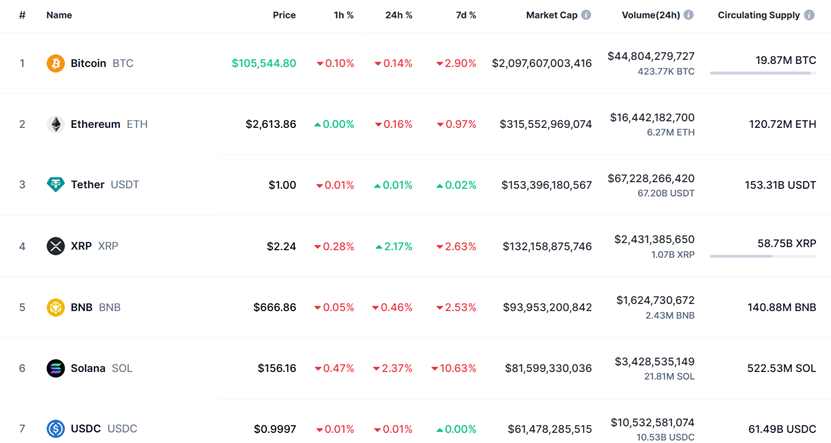

USDT is currently the largest stablecoin globally and the third-largest cryptocurrency overall, ranking behind only Bitcoin and Ethereum. As of 11 a.m. on June 4, USDT’s global circulation stood at $153.3 billion, with a 24-hour trading volume of $67.2 billion—the highest among all cryptocurrencies.

USDT is essentially a money-printing machine: the company has fewer than 200 employees and generated a profit of $13.7 billion in 2024. However, it has long faced controversy due to lack of transparency in reserve assets and absence of independent audits.

The second-largest stablecoin is USDC, issued by Circle, which recently went public. It has a global circulation of $61.5 billion and a 24-hour trading volume of $10.5 billion, ranking seventh among cryptocurrencies.

USDC has pursued a compliance-first strategy, backed by U.S. dollars and Treasury bonds, and subject to KYC, anti-money laundering (AML), and audit regulations. However, its profitability pales in comparison to USDT. Circle reported revenue of $1.676 billion and net profit of $156 million in 2024, having incurred losses during 2021–2022.

Together, USDT and USDC dominate 95% of the stablecoin market, leaving other fiat-backed stablecoins far behind, including:

USD1, launched in April by the Trump family, with a circulation of $2.18 billion and a 24-hour trading volume of $219 million.

FDUSD, issued in July 2023 by Hong Kong-based First Digital, with a circulation of $1.59 billion and a 24-hour trading volume of $459 million.

PYUSD, launched by PayPal at the end of 2023, with a circulation of $979 million and a 24-hour trading volume of $8 million.

A 2025 report by Investing.com noted that the number of active on-chain addresses for stablecoins has surpassed 300 million, indicating deep integration of stablecoins into the global financial system.

What drives the rapid rise of stablecoins? Consider this true story to understand their value for ordinary people: During Lebanon’s conflict a few years ago, the government imposed financial controls limiting bank withdrawals to $200 per day. Some individuals, desperate to access funds for medical emergencies, resorted to threatening banks with firearms to retrieve their own money.

Your money in a bank is just a number—you still need the bank’s permission to use it. This is a flaw of traditional finance. Cryptocurrency, however, exists on-chain: as long as you have internet access, you can freely control your funds anytime. This is one of the core appeals of stablecoins.

What other benefits do stablecoins offer? In countries like Argentina and Nigeria, where inflation reaches tens or even hundreds of percent annually, local currencies can become worthless overnight. For locals, holding dollar-pegged stablecoins is one way to hedge against inflation and currency devaluation.

In fact, in Latin America, stablecoins have become the primary currency for daily payments and savings. Of the $30 trillion in stablecoin transactions in 2024, Latin America accounted for about 10%, or $3 trillion.

Another major driver of stablecoin growth is cross-border payments. Traditional international remittances rely on SWIFT, taking days and incurring high fees. Stablecoins enable peer-to-peer transactions without intermediaries, significantly lowering costs. For example, cross-border payments via Visa typically take 1–3 days and cost an average of 6.35% of the transaction amount. In contrast, USDC settles in seconds, with fees as low as 0.1%–0.3%.

Sub-Saharan Africa and Latin America are the main recipients of stablecoin remittances.

Chainalysis research found that in Ethiopia, which enforces strict capital controls, demand for USDC and USDT surged following the local currency’s depreciation in 2023, with annual growth in retail stablecoin transfers reaching 180%.

From July 2023 to June 2024, Latin American countries received $415 billion in cryptocurrency, a year-on-year increase of approximately 42.5%. In Mexico, annual remittances from the U.S. exceed $60 billion, with an increasing share now flowing through stablecoins. Some analysts predict that within the next three to five years, about 30% of U.S.-Mexico remittances will be conducted via stablecoins.

A significant trend is that businesses in Latin America and Africa are increasingly adopting stablecoins to reduce cross-border payment costs. In Brazil, corporate usage of stablecoins for cross-border payments has risen sharply. By the end of 2023, large-value transactions exceeding $1 million grew by about 29%.

Analysts project that by the end of 2026, stablecoin transaction volume for trade finance and payment processing could reach $1 trillion, capturing over 1% of the global cross-border B2B payments market.

Moreover, with the rapid advancement of AI, stablecoins—as programmable money—will further reshape payments and finance when combined with AI capabilities. In future global economic activities, stablecoins will play an increasingly important role. Precisely because of this, stablecoins have become a focal point for innovation, regulation, and geopolitical competition among nations.

In 2024, the European Union began implementing the Markets in Crypto-Assets Regulation (MiCA), prohibiting the issuance or offering of stablecoins in the EU without authorization. The recent stablecoin bills in the U.S. and Hong Kong introduce more specific regulatory measures.

Both jurisdictions require stablecoin issuers to maintain 1:1 fiat backing, disclose reserve composition monthly, undergo audits, and strictly comply with anti-money laundering (AML) and know-your-customer (KYC) requirements.

Key differences include:

1. The U.S. approach is stricter: The U.S. government will create a non-compliance list for dollar stablecoins that do not hold U.S. Treasuries as reserves or fail to comply with U.S. AML/KYC regulations, restricting their trading in the U.S. market.

In 2024, North America accounted for 40% of global stablecoin transaction volume, making this restriction highly impactful. The biggest affected player is likely USDT. 2024 may mark Tether’s most profitable year, as future compliance will significantly increase its operational costs.

Hong Kong, by contrast, focuses on regulating Hong Kong dollar-pegged stablecoins. Any HKD-pegged stablecoin, whether issued in Hong Kong or abroad, falls under regulatory oversight. For non-HKD stablecoins, the rules are more lenient: they can be offered to retail investors in Hong Kong upon obtaining a license from the Monetary Authority; unlicensed issuers may only serve institutional investors.

2. Hong Kong requires stablecoin issuers to have a minimum registered capital of HK$25 million (approximately $3.2 million). The U.S. does not specify a capital requirement but mandates adherence to banking-level regulatory standards, which—given high compliance costs—is also extremely challenging for small and medium-sized issuers.

3. Hong Kong places greater emphasis on investor protection, mandating redemption rights for users.

The differing stablecoin bills reflect distinct strategic visions between the U.S. and China: The U.S. views stablecoins as an extension of dollar dominance into the digital realm. By tying dollar stablecoins to the U.S. dollar, it aims to reinforce the dollar’s position as the world’s primary reserve currency and ensure stablecoins become a global financial tool centered around the U.S.

The reserve asset requirements boost demand for U.S. Treasuries. On May 23, U.S. Treasury Secretary Bessent openly stated: “Stablecoins could increase demand for U.S. Treasuries and short-term bills by $2 trillion in the near term. For reference, the current figure is around $300 billion.”

China, while banning cryptocurrencies on the mainland, is using Hong Kong as a testing ground for stablecoin innovation, actively exploring and positioning itself in this space. HKD-pegged stablecoins aim to provide infrastructure for Hong Kong’s Web3 ecosystem and establish alternative payment channels bypassing the Western-dominated traditional financial system.

Alongside stablecoin legislation, the Hong Kong Monetary Authority launched a stablecoin sandbox program in March 2024, with participants including JD Digits, Monet, and Standard Chartered Bank. These projects remain in the testing phase, and HKD-pegged stablecoin transaction volumes are still limited. Currently, USDT and USDC continue to dominate the Hong Kong market.

Stablecoins are just one component of Hong Kong’s broader Web3 ecosystem. On October 31, 2022, Hong Kong’s Financial Services and the Treasury Bureau released its *Policy Statement on the Development of Virtual Assets in Hong Kong*, declaring its ambition to become a global Web3 hub. Over the past few years, the Hong Kong government has been quietly building this foundation.

2023:

Hong Kong issued the world’s first tokenized government green bond;

The government allocated HK$50 million (approximately $6.4 million) to develop the Web3 ecosystem, supporting enterprises, technology R&D, and community initiatives;

The Securities and Futures Commission (SFC) formally implemented a regulatory framework for virtual asset trading platforms, granting licenses to platforms such as HashKey and increasing the number of compliant exchanges.

2024:

The Hong Kong Stock Exchange listed six spot virtual asset ETFs in Asia, including Bitcoin and Ethereum ETFs—the largest such offering in Asia;

The SFC approved seven virtual asset trading platforms (including OSL, HashKey, and HKVAX) and expanded oversight to cover over-the-counter (OTC) trading, custody services, and staking;

The Monetary Authority launched the "Ensemble" tokenized asset sandbox initiative, supporting real-world asset (RWA) tokenization experiments, attracting institutions such as Ant Group and Standard Chartered Bank;

Promoted collaboration between public blockchain platforms like Zetrix and Web3Labs and Summer Capital to advance blockchain infrastructure for government and enterprise applications.

2025:

The SFC released the "ASPIRe" roadmap, focusing on market access, investor protections, product offerings, infrastructure, and relationships, aiming to promote transparency in the Web3 market through enhanced disclosure and streamlined securities issuance;

Hong Kong hosted the "Consensus Hong Kong 2025" conference, emphasizing the convergence of AI and Web3, exploring emerging areas like decentralized AI networks and AI agent platforms, attracting global Web3 professionals;

Cyberport attracted over 270 Web3-related enterprises, spanning blockchain gaming, DeFi, infrastructure, and decentralized science (DeSci);

The Monetary Authority deepened its e-HKD policy, exploring central bank digital currency (CBDC) applications in cross-chain payments and cross-border trade within the Web3 context.

While Hong Kong has yet to achieve standout success in becoming a Web3 hub, it has largely completed its strategic layout and established a clear roadmap.

Overall, the U.S. seeks financial hegemony in the digital world, while Hong Kong’s strategic focus lies in building a Web3 industry. HKD-pegged stablecoins remain in their infancy. The great power contest has not yet fully begun.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News