Huobi Growth Academy | Cryptocurrency Market Macro Research Report: Turning Point Approaching, Macro Signals Emerge, Market Poised to Reconstruct Pricing Logic

TechFlow Selected TechFlow Selected

Huobi Growth Academy | Cryptocurrency Market Macro Research Report: Turning Point Approaching, Macro Signals Emerge, Market Poised to Reconstruct Pricing Logic

The current cycle remains in a "mid-bull market correction phase," but structural opportunities are quietly emerging, and the pricing anchor is undergoing macro-level shifts.

1. Introduction

In Q2 2025, the crypto market transitioned from a high-heat rally into a short-term correction. While sectors such as Memes, AI, and RWA continued to rotate and repeatedly drive sentiment, the macro ceiling of suppression has gradually become evident. Amid global trade volatility, fluctuating U.S. economic data, and ongoing speculation around Federal Reserve rate cuts, the market has entered a critical window of "awaiting a reconstruction of pricing logic." At the same time, marginal shifts in policy dynamics have begun to emerge: positive statements on cryptocurrencies from the Trump camp have triggered early market pricing of the “Bitcoin as national strategic reserve asset” narrative. We believe the current cycle remains in a "mid-cycle bull market pullback," yet structural opportunities are quietly emerging, with valuation anchors undergoing macro-level realignment.

2. Macro Variables: The Breakdown of Old Logic, New Anchors Undetermined

By May 2025, the crypto market stands at a pivotal juncture of macro-level paradigm reconstruction. Traditional pricing frameworks are rapidly disintegrating, while new valuation anchors have yet to form—placing the market in a state of "ambiguous tension." Macroeconomic indicators, central bank policy directions, and marginal shifts in global geopolitical and trade relations are collectively shaping crypto market behavior under an emerging pattern of "new order within instability."

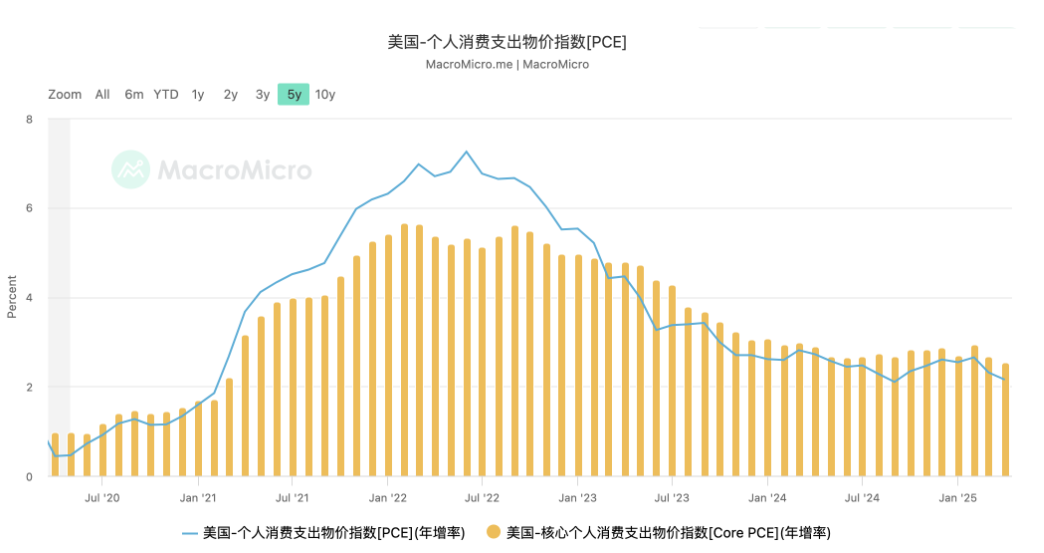

First, the Federal Reserve's monetary policy is shifting from "data dependency" to a new phase defined by the interplay of political pressure and stagflation concerns. CPI and PCE data released in April and May indicate that although inflationary pressures have eased slightly, underlying stickiness persists—particularly in service-sector prices, which remain rigid due to structural labor shortages. Despite a marginal rise in unemployment, it remains far from the threshold needed to trigger a policy reversal by the Fed. As a result, market expectations for rate cuts—once pointing to June—have now been pushed back to Q4 or later. While Fed Chair Powell hasn't ruled out rate cuts this year, his public remarks emphasize "cautious observation" and "commitment to long-term inflation targets," making near-term liquidity easing appear increasingly distant.

This uncertain macro environment directly impacts the fundamental basis for pricing crypto assets. Over the past three years, crypto enjoyed valuation premiums amid a backdrop of zero interest rates and abundant liquidity. Now, in the latter stage of a high-rate, slow-declining cycle, traditional valuation models face systemic failure. Although Bitcoin maintains an upward oscillation driven by structural capital flows, it has consistently failed to generate momentum strong enough to break through the next key resistance level—indicating its alignment path with traditional macro assets is unraveling. The market is no longer mechanically equating "Nasdaq up = BTC up." Instead, there’s growing recognition that crypto assets require independent policy and functional anchors.

Meanwhile, geopolitical variables influencing the market since the beginning of the year are undergoing significant changes. The previously escalating U.S.-China trade tensions have notably cooled. Recent shifts in the Trump team’s focus toward "manufacturing repatriation" suggest that neither side intends to intensify conflict in the short term. This has weakened the "geopolitical hedge + Bitcoin as risk-resistant asset" narrative, leading markets to withdraw premium valuations based on Bitcoin's role as a safe haven. Investors are now seeking fresh policy support and narrative drivers. This shift explains why the crypto market, after a structural rebound in mid-May, turned into a high-range consolidation phase—with even some outflows from on-chain assets.

At a deeper level, the global financial system is undergoing a systemic process of "anchor reconstruction." The U.S. dollar index trades sideways at elevated levels; correlations among gold, Treasury bonds, and U.S. equities have broken down. Crypto assets find themselves caught in between—lacking both central bank backing like traditional safe-haven assets and full integration into mainstream institutional risk frameworks. This ambiguous state of being "neither risky nor risk-free" places BTC, ETH, and other primary assets in a "valuation gray zone." This unclear macro anchor then cascades down to the ecosystem level, causing sub-narratives like Memes, RWA, and AI to flare up briefly but fail to sustain momentum. Without inflows of macro-level incremental capital, localized booms on-chain easily fall into a "quick ignition → rapid burnout" rotation trap.

We are entering a turning point dominated by macro variables—a phase of "de-financialization." In this stage, market liquidity and trends will no longer be driven simply by cross-asset correlations, but rather by the re-allocation of policy authority and institutional roles. For the crypto market to experience its next round of systemic repricing, it must await the emergence of a new macro anchor—this could be the official adoption of "Bitcoin as a national strategic reserve asset," the clear initiation of the Fed's rate-cutting cycle, or widespread governmental acceptance of on-chain financial infrastructure across multiple countries. Only when such macro-level anchors materialize will we see a broad return of risk appetite and synchronized price appreciation across assets.

For now, the crypto market should stop clinging to outdated paradigms and instead calmly identify early signals of new anchor formation. Capital and projects that can recognize structural macro shifts and position themselves ahead of these new anchors will gain the upper hand in the next genuine bull run.

3. Policy Variables: GENIUS Act Passed, State-Level Bitcoin Reserves Launched, Sparking Structural Expectations

In May 2025, the U.S. Senate officially passed the GENIUS Act (Guaranteed Electronic Network for Uniform and Interoperable Stablecoins Act), marking one of the most institutionally influential stablecoin regulatory frameworks globally since MiCA. The passage of this bill not only establishes a formal regulatory framework for USD-backed stablecoins but also sends a clear signal: stablecoins are no longer mere technological experiments or gray-market financial instruments—they are becoming integrated into the core of sovereign finance, serving as organic extensions of digital dollar influence.

The GENIUS Act centers on three key aspects: First, it grants federal reserve and financial regulators licensing authority over stablecoin issuers, imposing bank-equivalent requirements for capital adequacy, reserves, and transparency. Second, it provides a legal foundation and standardized interfaces for interoperability between stablecoins, commercial banks, and payment institutions, promoting broader applications in retail payments, cross-border settlements, and financial interoperability. Third, it introduces a "regulatory sandbox" exemption mechanism for decentralized stablecoins (e.g., DAI, crvUSD), preserving space for open finance innovation within a compliant and controllable framework.

From a macro perspective, the passage of this act triggers three structural shifts in market expectations. First, the international expansion of the dollar system gains a new paradigm—"on-chain anchoring." As digital-age "federal checks," stablecoins’ on-chain circulation capabilities serve not only Web3-native payments but may also function as conduits for U.S. monetary policy transmission, strengthening the dollar’s competitive edge in emerging markets. This signifies that rather than merely suppressing crypto, the U.S. is now selectively incorporating certain "channel rights" into its fiscal architecture—legitimizing stablecoins while positioning the dollar strategically for future digital financial competition.

Second, the legalization of stablecoins drives a structural revaluation of on-chain finance. Compliant stablecoins such as USDC and PYUSD are poised for a liquidity surge, further activating DeFi and RWA bridging use cases related to on-chain payments, credit, and ledger restructuring. Particularly against the backdrop of high interest rates, inflation, and regional currency volatility, stablecoins’ role as "cross-regime arbitrage tools" will continue attracting users from emerging markets and on-chain asset managers. Within two weeks of the GENIUS Act’s passage, Coinbase and other platforms reported stablecoin daily trading volumes reaching their highest levels since 2023, with USDC’s circulating market cap rising nearly 12% MoM—marking a visible shift in liquidity from Tether toward regulated assets.

Even more structurally significant is the wave of state governments announcing Bitcoin strategic reserve programs following the bill’s approval. By late May, New Hampshire had passed legislation establishing a Bitcoin strategic reserve, while Texas, Florida, and Wyoming announced plans to allocate portions of their fiscal surpluses into Bitcoin holdings—citing reasons including inflation hedging, fiscal diversification, and local blockchain industry support. In essence, this marks a shift where Bitcoin transitions from a "community consensus asset" to one formally recognized on "state balance sheets"—a digital reimagining of the historical precedent of state gold reserves. Though still small in scale and unstable in mechanism, the political signal outweighs the actual asset size: Bitcoin is becoming a "government-grade choice."

Together, these policy developments paint a new structural picture: stablecoins as "on-chain dollars," Bitcoin as "digital gold at the state level." One regulated, one frontier—these dual pillars engage with the traditional monetary system through both symbiosis and counterbalance. In the context of 2025’s fragmented geo-finance landscape and declining institutional trust, this duality offers an alternative anchoring logic. It also explains why the crypto market maintained resilience during mid-May’s weak macro data (persistent high rates, CPI rebound)—because structural policy shifts provided long-term certainty, forming a foundational floor beneath the market.

Post-GENIUS, renewed market evaluation of the "Treasury yield vs. stablecoin yield" model will accelerate product evolution toward "on-chain T-Bills" and "on-chain money market funds." In a sense, part of America’s future digital debt structure may eventually be custodied via stablecoins. The prospect of tokenized Treasuries is now becoming increasingly tangible through the institutionalization of stablecoins.

4. Market Structure: Intense Sector Rotation, No Clear Main Theme Yet

The second quarter of 2025 reveals a highly strained structural contradiction in the crypto market: macro-level policy sentiment is warming, with stablecoins and Bitcoin moving toward "institutional embedding"; yet at the micro level, there remains no truly consensus-driven "main theme." This results in frequent sector rotations, weak sustainability, and temporary "idle circulation" of liquidity. In other words, capital continues flowing across chains, but directional clarity and conviction remain unformed—contrasting sharply with earlier cycles like 2021 or 2023, characterized by dominant single-theme rallies (e.g., DeFi Summer, AI narrative explosion, Meme Season).

From a sector performance standpoint, May 2025 saw extreme fragmentation. Solana Memes, AI+Crypto, RWA, and DeFi took turns experiencing brief surges—each lasting less than two weeks before fading quickly. For instance, Solana Memes sparked a new wave of FOMO, but collapsed rapidly due to shallow community consensus and exhausted sentiment. AI tokens like $FET, $RNDR, and $TAO exhibited "high beta, high volatility" behavior, heavily influenced by sentiment in U.S. AI equities, lacking self-sustaining on-chain narratives. Meanwhile, the RWA sector led by ONDO, despite strong fundamentals, entered a "price-value divergence" consolidation phase after partial realization of airdrop expectations.

Fund flow data shows this rotation reflects structural liquidity abundance—not the onset of a structural bull market. Since mid-May, USDT’s market cap growth has stalled, while USDC and DAI saw slight rebounds. Daily DEX trading volume remained in the $25–30 billion range, nearly 40% below March highs. There’s no sign of significant new capital inflow—only existing capital chasing short-term opportunities with "high volatility + high emotion." Under these conditions, frequent sector switches fail to generate sustained momentum and instead amplify a "musical chairs"-style speculative rhythm, dampening retail participation and widening the gap between trading activity and social engagement.

Valuation stratification has also intensified. Top-tier blue-chip projects command clear valuation premiums, with ETH, SOL, and TON continuing to attract large-scale capital. Long-tail projects, however, remain stuck in a limbo of "undervalued fundamentals and unmet expectations." Data indicates that by May 2025, the top 20 cryptocurrencies accounted for nearly 71% of total market cap—the highest level since 2022—mirroring the "concentration rebound" seen in traditional capital markets. In the absence of broad-based rallies, liquidity and attention are concentrated in a few core assets, further squeezing survival space for new projects and narratives.

On-chain behavior is also evolving. Ethereum’s active address count has stabilized around 400,000 monthly, yet DeFi protocol TVL has not risen correspondingly—highlighting increasing "fragmentation" and "de-financialization" in on-chain interactions. Non-financial activities such as meme trading, airdrop farming, domain registration, and social protocols are becoming mainstream, signaling a user base shifting toward "light interaction + emotional engagement." While these behaviors generate short-term buzz, they impose growing monetization and retention challenges for protocol builders, constraining innovation incentives.

From an industry perspective, the market currently sits at a tipping point of multiple coexisting themes without a dominant trend: RWA retains long-term potential but awaits clearer regulatory clarity and organic ecosystem growth; Memes can ignite emotions but lack cultural flagship projects like DOGE or PEPE capable of uniting communities; AI+Crypto holds vast promise, yet technical implementation and token incentive mechanisms remain unresolved; Bitcoin’s ecosystem is gaining scale but still in the early "trial-and-error + positioning" phase due to immature infrastructure.

In short, the current market structure can be summarized in four keywords: rotation, fragmentation, concentration, and probing. Increased rotation raises trading difficulty; fragmentation narrows medium-to-long-term positioning space; concentration pulls valuations toward top players, leaving long-tail projects behind; and all current hotspots are essentially market probes testing whether new paradigms and themes can achieve dual validation through "consensus + capital."

Whether a dominant theme emerges will largely depend on convergence across three factors: first, whether there arises a native on-chain breakthrough innovation akin to DeFi in 2020 or Memes in 2021; second, whether regulatory progress continues to deliver structural tailwinds favorable to long-term crypto valuation (e.g., tokenized Treasuries, federal BTC reserve adoption); third, whether secondary markets see a return of mainstream capital to reignite fundraising and ecosystem development in primary sectors.

This phase resembles a deep-water "pressure test": sentiment isn’t poor, policy warmth exists, but a main theme is missing. The market needs a new core narrative to unify minds, capital, and computational power. And that may well become the decisive variable shaping the second half of 2025.

5. Outlook and Strategic Recommendations

Looking back from mid-2025, we have gradually moved beyond the红利 period of "halving + elections + rate cuts," yet the market has not yet established a durable, confidence-inspiring long-term anchor. Historically, if no strong thematic consensus forms in Q3, the market is highly likely to enter a moderate structural consolidation phase—characterized by increasingly fragmented热点, rising trading difficulty, and clearly stratified risk appetites—creating a "low-volatility window amid policy upswing."

From a medium-term view, the drivers of H2 price action are shifting from "macro interest rates" to "institutional implementation + structural narratives." With U.S. PCE and CPI showing continued declines and internal Fed discussions leaning toward two rate cuts this year, downside risks are marginally receding. Yet the crypto market hasn’t responded with massive inflows—indicating participants now prioritize long-term institutional backing over short-term monetary stimulus. We interpret this as evidence that crypto assets are transitioning from "high-beta risk assets" to "institutionally contested equity-like assets," reflecting a fundamental transformation in pricing mechanics.

The passage of the GENIUS Act and pilot state-level Bitcoin reserve programs may mark the beginning of this institutional floor. If more states begin allocating BTC into their fiscal reserves, crypto will truly enter a "quasi-sovereign endorsement" era. Combined with post-November election expectations for federal policy recalibration, this could serve as a structural catalyst more powerful than the halving. However, such processes are not instantaneous—any delay in policy momentum or reversal in electoral outcomes could trigger sharp corrections due to dashed institutional expectations.

Strategically, the current environment favors neither full-scale offense nor passive withdrawal, but rather "patient defense with opportunistic strikes." We recommend a "three-layer strategy":

Core holdings in sovereign-anchored assets: BTC and ETH as "emerging institutional assets" will continue attracting major capital. These should form the bedrock of portfolio allocation—prioritizing assets with low supply elasticity, minimal regulatory risk, and clear valuation frameworks.

Tactical participation in structural hotspots: For sectors like RWA, AI, and Memes, adopt tactical positioning—using time horizons to manage risk and liquidity strength to guide entry/exit decisions. Pay close attention to signs of on-chain behavioral breakthroughs or capital inflows.

Monitoring native innovation in the primary market: Every transformative wave in crypto stems from the dual engine of "on-chain mechanism innovation + community consensus." Shift focus gradually toward early-stage projects to capture emerging paradigms (e.g., chain abstraction, MCP protocol clusters, native user-layer protocols) and build long-term positions during ecosystem infancy.

Additionally, we highlight three potential inflection points that may shape H2 structural trends:

Whether the Trump administration delivers systemic policy tailwinds such as federal Bitcoin strategic reserves, tokenized Treasuries, ETF expansions, or regulatory exemptions;

Whether Ethereum’s Petra upgrade drives real user growth, whether L2/LRT mechanisms achieve paradigm shifts, and whether corporations follow the Strategy model of continuously buying BTC by initiating similar ETH accumulation programs;

In short, H2 2025 will be a transitional window shifting from "policy vacuum" to "policy博弈." While the market lacks a dominant theme, it has not lost momentum—remaining in a state of "deep squat before explosive lift-off." Assets capable of transcending cycles won’t peak during surface-level hype, but instead lay foundations in chaos and rise with certainty when policy and structure align.

During this process, we urge the community to abandon fantasies of instant riches and instead build a coherent, multi-cycle investment and research framework—one that identifies true "breakthrough points" through project fundamentals, on-chain behavior, liquidity distribution, and policy trajectories. Because the next real bull market won’t stem from any single sector’s rise, but from a paradigm shift where crypto is widely accepted as an institutional asset, backed by sovereigns, and adopted by real users.

6. Conclusion: The Winners Will Be Those Who Wait for the "Turning Point"

The current crypto market resides in a foggy interim: macro logic remains unsettled, policy variables are in flux, market热点 rotate rapidly, and liquidity has not fully shifted into risk assets. Yet beneath the surface, a systemic repricing is taking shape—one anchored in institutional transformation and nation-state博弈. We believe the true bull market breakout will not be driven by simple bull-bear cycles, but by the formal recognition of crypto’s political role triggering comprehensive revaluation. The turning point is approaching. Victory will belong to those who understand the macro landscape and position themselves with patience.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News