Why Isn't the Market Buying Into MicroStrategy's New Preferred Stock STRD?

TechFlow Selected TechFlow Selected

Why Isn't the Market Buying Into MicroStrategy's New Preferred Stock STRD?

What's different about this "new card"?

Author: Fairy, ChainCatcher

Strategy has unveiled a new move.

To continuously increase its Bitcoin exposure, MicroStrategy has frequently resorted to "self-funding" in recent years—issuing common stock, convertible bonds, and preferred shares in parallel, with financing rounds following one after another.

The bull market is far from over, and the筹码 (chips) are doubling. Yesterday, Strategy announced the launch of a new preferred stock product, STRD—another chip placed on the table in its heavy Bitcoin accumulation strategy. What makes this "new card" different? What signals does its structural design, potential risks, and market dynamics send?

STRD: High Yield, But No Guaranteed Payouts

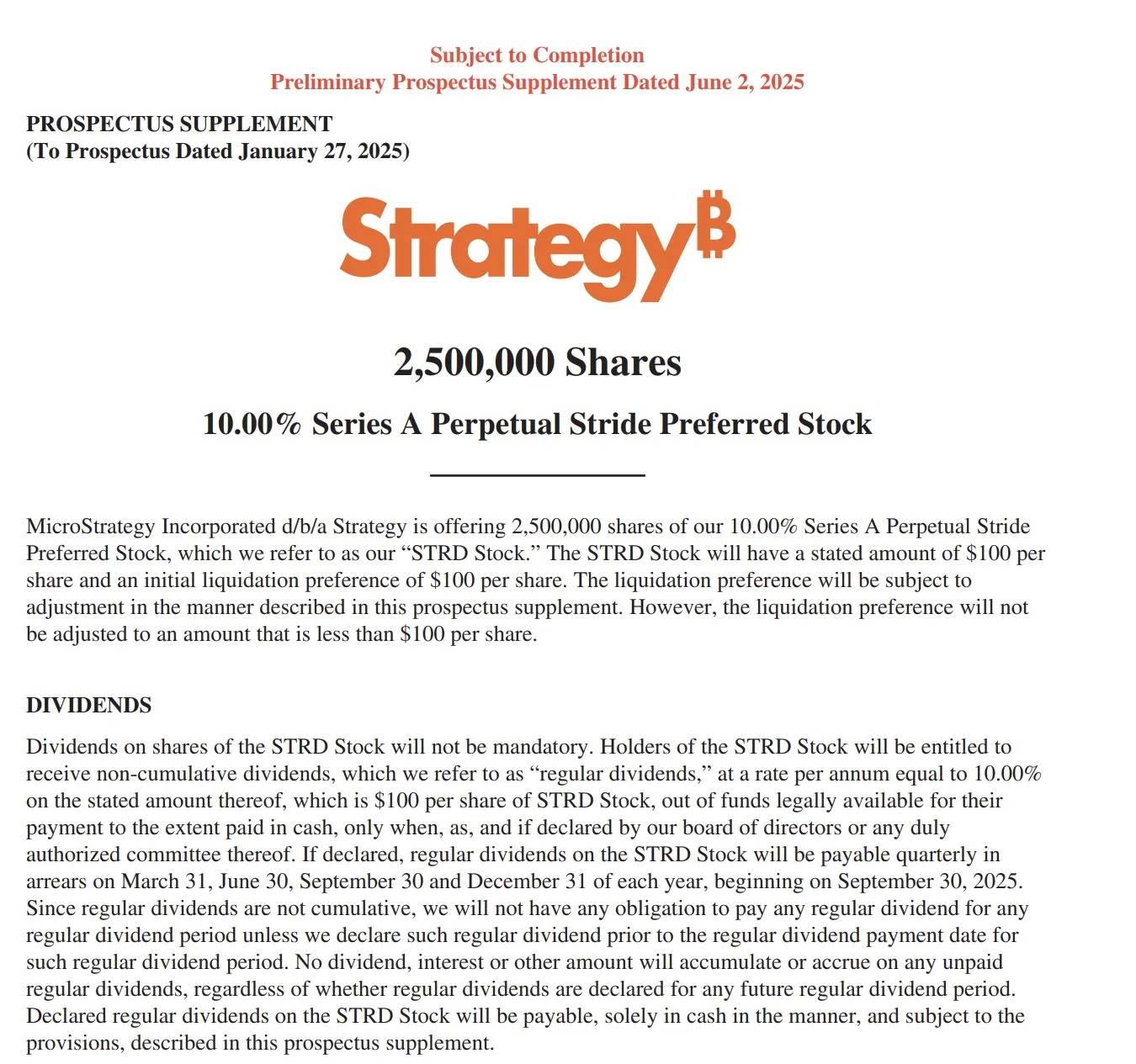

STRD is the third type of preferred stock launched by Strategy, planning to publicly issue 2.5 million shares. The proceeds will primarily fund Bitcoin acquisitions and supplement working capital. At its core, STRD represents yet another structured expression of the BTC bullish strategy, continuing the framework established by STRK and STRF while introducing new designs in profit distribution and exit mechanisms.

Like its predecessors, the underlying asset behind STRD remains Bitcoin. However, this time Strategy has adopted a more "defensive yet offensive" structure: an annual coupon rate of 10%, but without mandatory payment obligations, and unpaid interest does not accumulate.

Crypto KOL Phyrex captured the essence: "STRD is essentially lending money to Strategy at a 10% annual interest rate, but Strategy isn't obligated to pay that 10%. If they don't pay, they won't make up for it later. In their statement, Strategy promises timely distributions—on the condition that corporate profits remain strong."

As for where this interest payment would come from, Strategy theoretically has three possible funding paths:

-

Selling BTC holdings: If Strategy sells part of its Bitcoin position, it could generate cash flow—but this would trigger capital gains taxes and contradict its long-term holding strategy.

-

Rollover financing: Raising funds through new debt or other instruments to cover interest payments—likely Strategy’s current preference.

-

Operating cash flow: Profits from other company operations might also be used to pay interest.

Although Strategy holds the right to withhold interest payments, doing so would carry severe consequences. Once interest payouts stop, the market price of STRD would likely suffer, investor confidence would erode, and future fundraising efforts would face greater resistance. Therefore, the market widely believes that as long as the Bitcoin market remains stable, Strategy will most likely continue making timely payments to preserve its market credibility and sustainable funding pipeline.

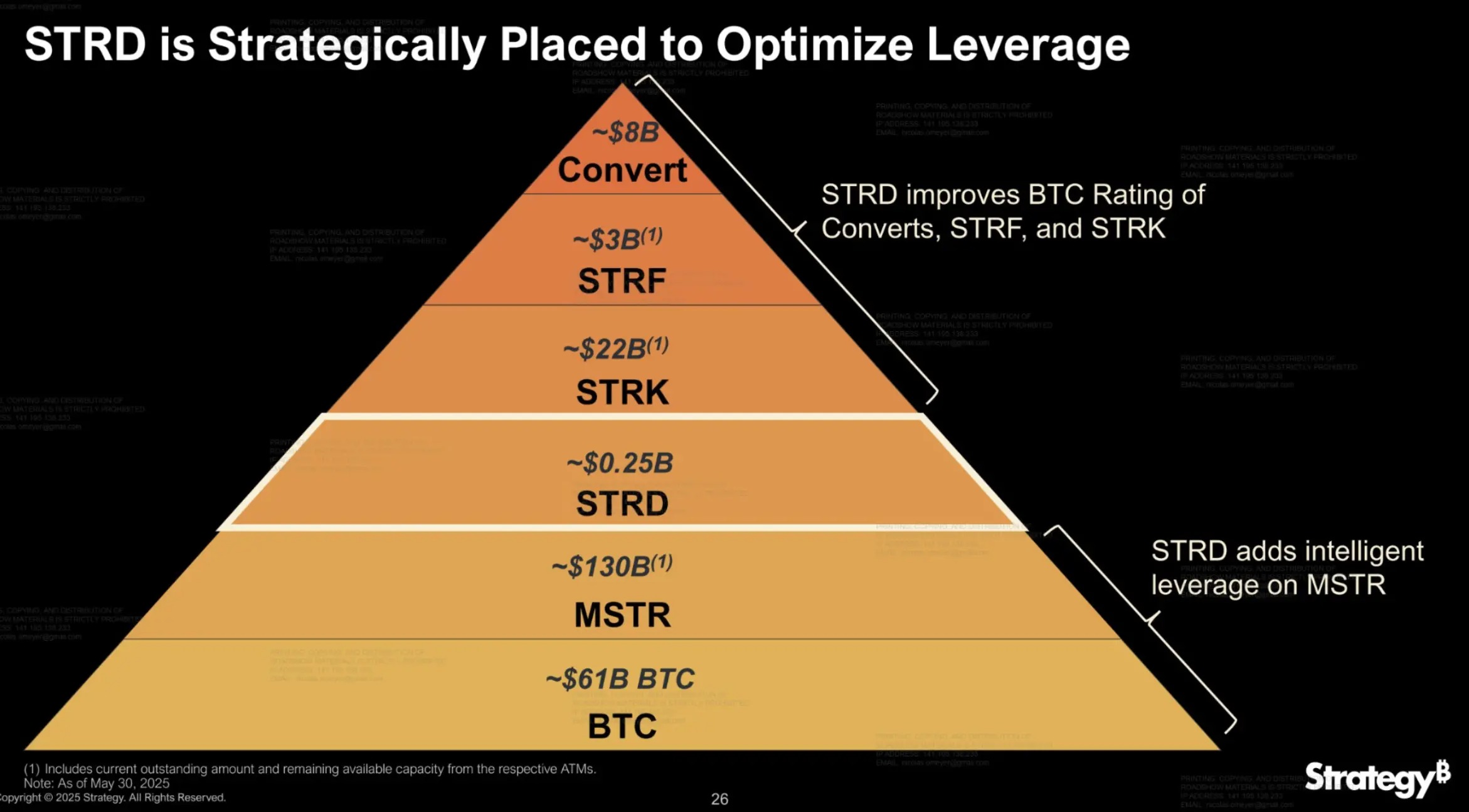

"Triple Threat": Strategy's Multi-Tier Preferred Stock Structure

Having discussed the features of STRD, let's now look back at Strategy’s current trio of preferred stock products. STRK, STRF, and STRD each occupy distinct positions in terms of liquidation priority, yield design, and risk profile, forming key components of Strategy’s layered capital structure. Below is a comparison table compiled by Bitwise Senior Investment Strategist Juan Leon (translated by ChainCatcher):

From an investor suitability perspective, STRK better suits conservative investors seeking stable returns with lower risk tolerance; STRF targets neutral investors who desire higher fixed income but can accept moderate credit risk; STRD appeals to aggressive capital with high risk tolerance.

Beyond product expansion, the launch of STRD may also represent Strategy reinforcing the foundation of its capital structure. As shared by community member @DogCandles in a chart, STRD sits “low in rank” but plays a “crucial role,” enhancing credit support for senior tranches and optimizing the overall capital architecture.

Community Skepticism and Rising Controversy Over STRD

The release of STRD is a carefully calculated move by Strategy, but the community hasn't universally applauded it. Many have directly criticized it as "financial wizardry":

-

@chaojidigua: “Jiang Taigong fishing—those who wish to be hooked will bite.”

-

@MemeSiguoyi: “Don’t think only crypto projects can mint money out of thin air—our stocks have their own form of fictional money creation.”

-

@Softelectrock: “Ponzi nesting doll.”

Adam Livingston, author of *The Bitcoin Age*, cut straight to the point: “STRD is essentially a BTC accumulation option disguised as a yield-generating instrument. When BTC surges, Strategy redeems at par value; when BTC crashes, they simply stop paying interest. Investors are effectively subsidizing his 'ultimate adoption of Bitcoin' belief.”

Dylan LeClair, Bitcoin Strategy Director at Metaplanet, praised the structure as “genius”: “The issuance of STRD actually improves the credit quality of STRF.”

Regarding Strategy’s future trajectory, crypto KOL Phyrex offered a bolder prediction: “It's possible Strategy might start utilizing its Bitcoin inventory—such as lending out BTC or participating in quantitative trading—to maintain cash flow. Strategy might evolve into a bank built on BTC.”

Strategy has placed its chips squarely on the table. Wrapping conviction in structured products, masking one-sided bets within risk-return models, attracting market sentiment with “high yields.”

This financial experiment, grounded in faith, is becoming increasingly complex—and all the more worth watching.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News