Stripping away the veneer of stablecoins and tokenization, accelerating the flow of dollars is the essence

TechFlow Selected TechFlow Selected

Stripping away the veneer of stablecoins and tokenization, accelerating the flow of dollars is the essence

Accelerating the velocity of money is a core application of cryptocurrencies, and tokenizing RWAs aligns perfectly with this trend.

Author: Sumanth Neppalli

Compiled & Translated: TechFlow

Stablecoins have recently become a hot topic in the cryptocurrency space. Some view them as the best invention since sliced bread, while others—myself included—see them merely as an elegant mechanism for exporting the U.S. dollar. As tokenization reshapes our financial landscape, we’ve been pondering how financial markets will evolve in response. This article begins by reviewing the historical backdrop of stablecoins before delving into the potential market impacts of tokenization.

In July 1944, representatives from 44 Allied nations gathered at a ski resort in Bretton Woods, New Hampshire, to redesign the global monetary system. They decided to peg national currencies to the U.S. dollar, which in turn was tied to gold. Designed by British economist John Maynard Keynes, this framework ushered in a new era of stable exchange rates and smooth international trade.

If we likened that summit to a GitHub project, the White House would be the one who created the branch; the Treasury Secretary submitted pull requests, and finance ministers from other countries approved the changes—effectively hardcoding the dollar into every future trade transaction. In today’s digital age, stablecoins represent the merged version of that code, while other nations scramble to rebase their own “codebases” in preparation for a future that may not rely on the dollar.

Within 72 hours of returning to the Oval Office, President Trump signed an executive order that sounded more like science fiction dreamed up by crypto enthusiasts than traditional fiscal policy: "Promote and protect the sovereignty of the dollar, including through legally compliant, dollar-backed stablecoins used globally."

Shortly after, Congress introduced the GENIUS Act—short for "Guiding and Establishing National Innovation for U.S. Stablecoins." This is the first legislation to establish foundational rules for stablecoins while encouraging their global use in payments.

The bill is currently being debated in the Senate, with a vote expected this month. Staffers indicate the latest draft has incorporated multiple suggestions from Democratic lawmakers, significantly increasing its chances of passage.

So why is Washington so interested in stablecoins? Is this just political theater, or does it reflect a deeper strategic agenda?

Why Foreign Demand Still Matters

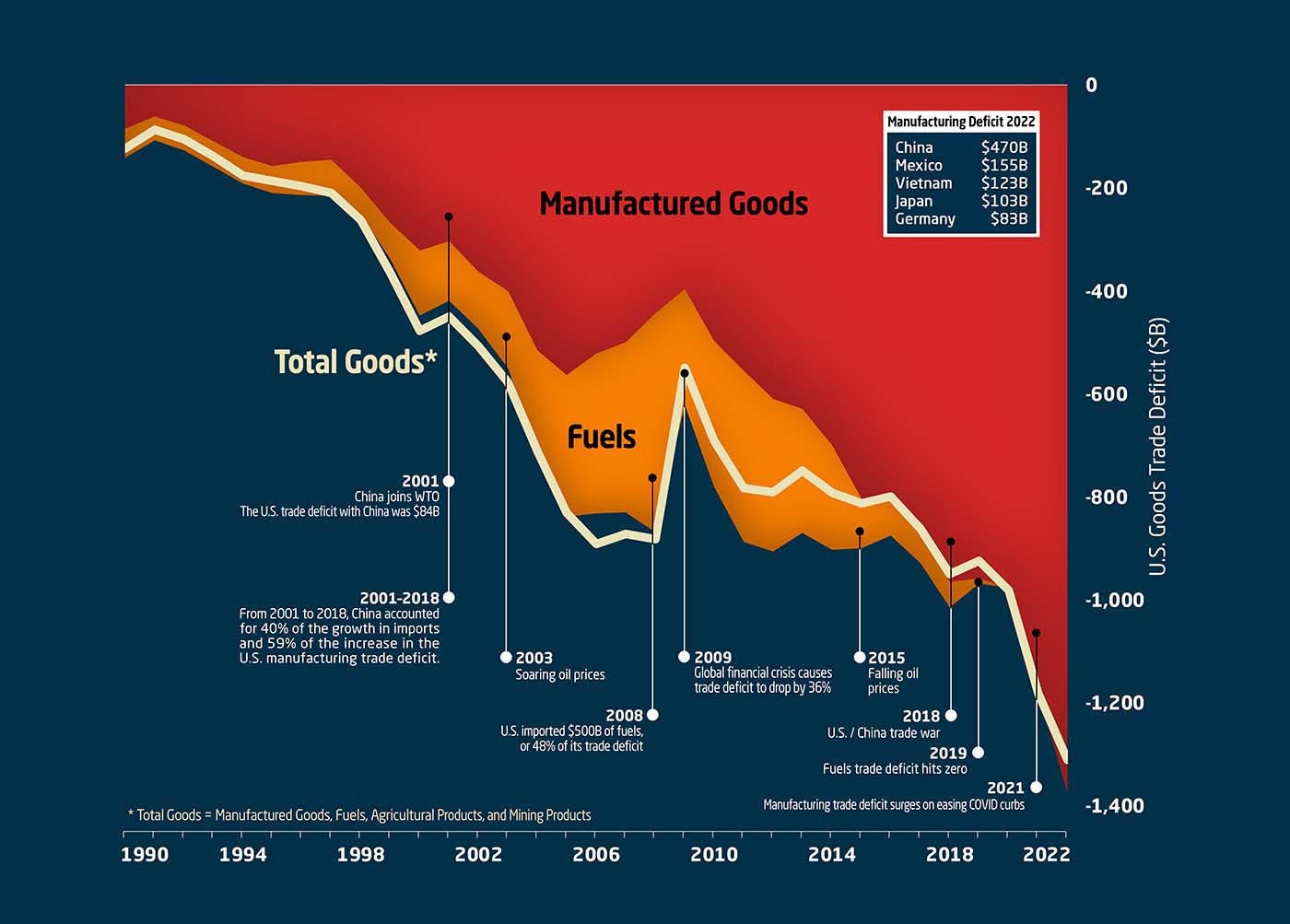

Since the 1990s, the United States has outsourced much of its manufacturing to China, Japan, Germany, and Gulf states, paying for these imports with newly printed dollars. Because imports far exceed exports, the U.S. has long run massive trade deficits. A trade deficit refers to the gap between what a country spends on global goods versus what it earns from exports.

Source: Visual Capitalist

Exporting countries face a dilemma: if they convert their earned dollars back into local currency, their exchange rate rises, undermining the competitiveness of their exports. To avoid this, central banks typically reinvest those dollars into U.S. Treasury securities. This stabilizes foreign exchange markets, earns interest income, and carries credit risk nearly identical to holding physical dollars.

This creates a self-reinforcing cycle: export goods to the U.S., earn dollars, then invest those dollars in Treasuries to generate returns. To sustain this loop, exporting nations deliberately keep their currencies undervalued, further boosting exports.

This "export-financing cycle" helps the U.S. fund part of its debt burden. About a quarter of America’s $36 trillion debt is financed this way. But if a prolonged trade war disrupts this cycle, one of America’s cheapest sources of funding could dry up.

-

Financing the deficit: The U.S. government consistently spends more than it earns, operating under persistent budget deficits. By selling Treasury bonds abroad, the U.S. shares the burden of its deficit. Short-term bills mature within a year, while long-term bonds can extend 20–30 years.

-

Maintaining low interest rates: Strong foreign demand keeps Treasury yields (interest rates) low. When buyers like China push bond prices higher, yields fall—lowering borrowing costs for governments, businesses, and consumers. Cheap credit fuels economic growth and funds expansive fiscal policies.

-

Dollar’s global status: The dollar's role as the world’s reserve currency depends on international trust in the U.S. economy and assets. Foreign-held Treasuries symbolize this confidence, ensuring continued use of the dollar in global trade, oil pricing, and foreign reserves. This privilege allows the U.S. to borrow cheaply and maintain geopolitical influence.

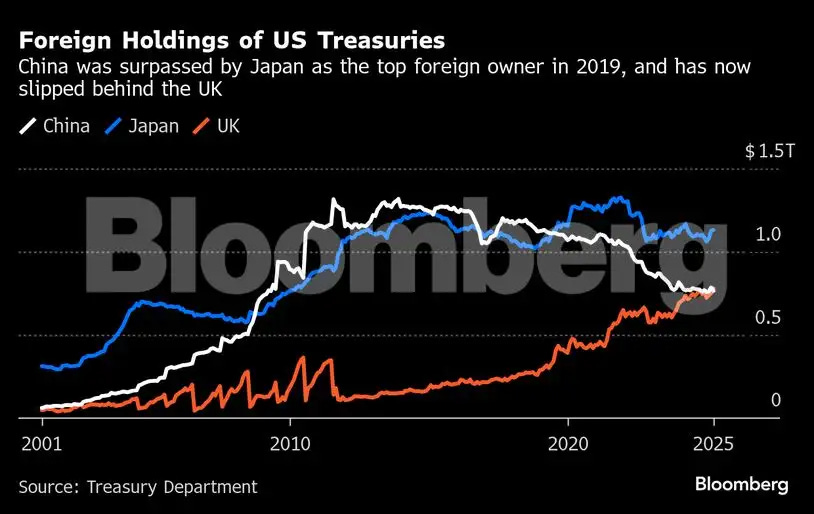

However, if this demand weakens, the U.S. could face higher borrowing costs, a weaker dollar, and diminished geopolitical clout. Warning signs are already emerging. Upon leaving office, Warren Buffett expressed concern about an impending dollar crisis. Recently, the U.S. lost its AAA credit rating across all major rating agencies. The AAA rating, considered the “gold standard” in bond markets, signifies near-zero default risk. After the downgrade, the U.S. Treasury had to offer higher yields to attract investors—increasing interest expenses at a time when national debt continues to grow.

If traditional Treasury buyers begin exiting, who will absorb the next wave of multi-trillion-dollar debt issuance? Washington’s strategy is to open new capital channels via a wave of regulated, fully dollar-backed stablecoins. The GENIUS Act mandates that stablecoin issuers must purchase U.S. Treasuries. That explains why the government takes a tough stance on trade while simultaneously pushing forward digital dollar initiatives.

The Legacy of Eurodollars

TechFlow Note: Eurodollar refers to U.S. dollar deposits held in banks outside the United States, particularly in Europe. These deposits operate outside U.S. regulatory oversight, allowing different interest rates and operational practices compared to domestic banking systems.

Detailed Explanation

Financial innovation is nothing new to the U.S. The $1.7 trillion eurodollar system once evolved from complete rejection to broad acceptance. Eurodollars are dollar-denominated deposits held overseas, primarily in European banks, and are not subject to U.S. banking regulations.

The eurodollar system emerged in the 1950s when the Soviet Union deposited dollars in European banks to evade U.S. jurisdiction during the Cold War. It grew rapidly—from a few billion to $50 billion by 1970, a fiftyfold increase in just ten years.

The U.S. initially viewed the system with suspicion. French Finance Minister Valéry Giscard d'Estaing famously called it a “monster with two heads,” highlighting its complexity and risks. However, the 1973 oil crisis eased concerns. OPEC quadrupled the value of global oil trade in months, creating urgent demand for a stable currency—making the dollar indispensable.

The eurodollar system significantly enhanced U.S. non-military global influence. As international trade expanded and Bretton Woods cemented dollar dominance, the network grew. Although eurodollar transactions occurred between foreign entities, they flowed through correspondent banking networks ultimately clearing through U.S. banks.

This gave the U.S. a pivotal role in global finance, enabling powerful tools for national security. The U.S. could not only block direct transactions but also exclude “bad actors” from the entire global dollar ecosystem. As a clearing hub, it could track money flows and impose financial sanctions on entire nations.

A New Era for Stablecoins

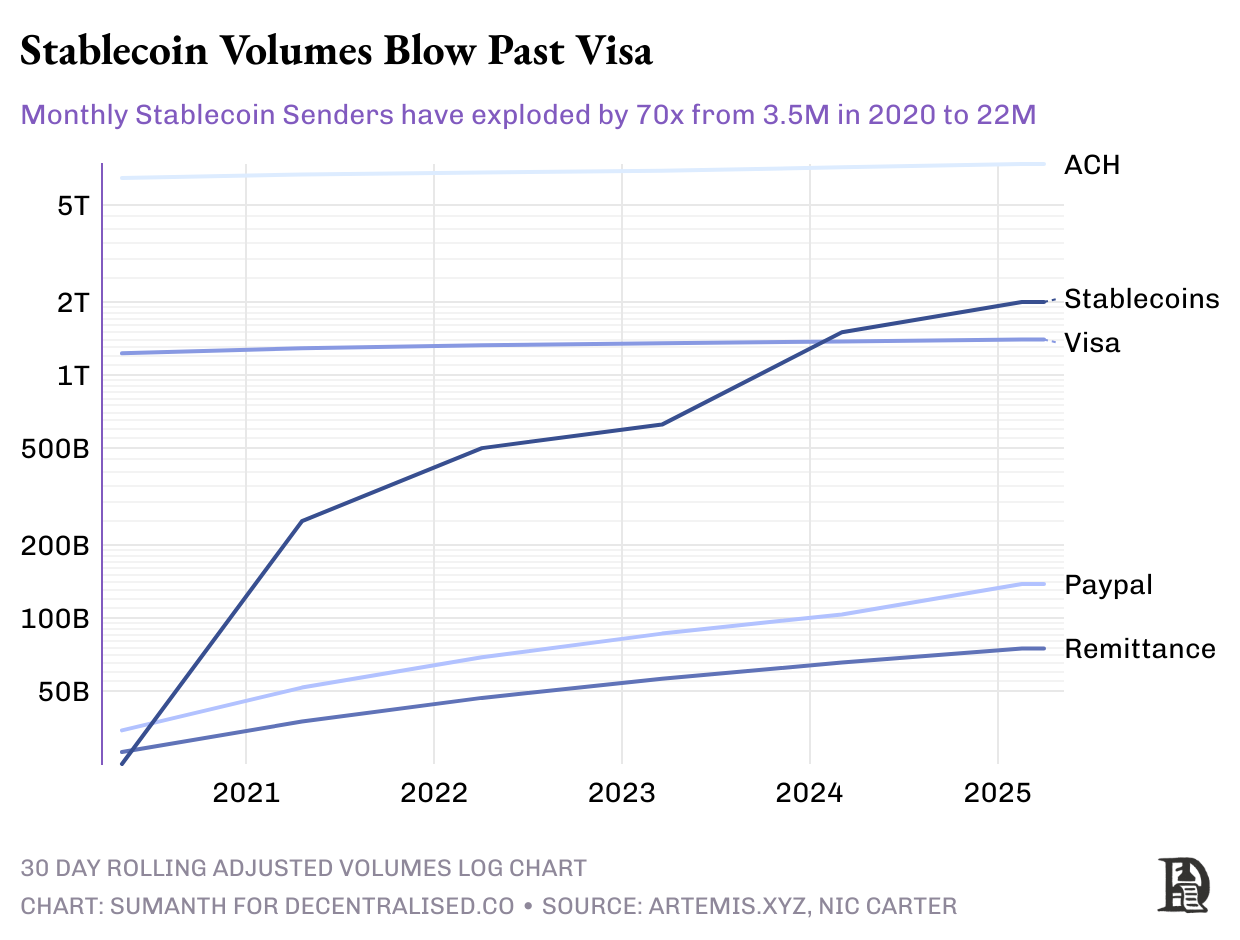

Modern stablecoins resemble eurodollars—but with publicly transparent blockchain explorers. Instead of storing dollars in vaults in London, dollars are now “tokenized” and circulated via blockchain technology. This innovation brings massive scale: in 2024, dollar-denominated stablecoins settled approximately $15 trillion on-chain—slightly surpassing Visa’s payment network volume. Circulating stablecoin supply now totals $245 billion, with 90% fully collateralized and pegged to the dollar.

Over time, demand for stablecoins has grown steadily. Investors seek stable assets to hedge against market volatility. Unlike the wild swings of crypto markets, stablecoins’ expanding use cases show they’re evolving beyond simple transaction tools into critical financial infrastructure.

Demand for stablecoins traces back to 2014, when Chinese crypto exchanges needed a bank-independent way to move dollars between order books. They adopted Realcoin—a dollar token built on Bitcoin using the Omni protocol.

Realcoin (later renamed Tether) relied on Taiwan-based banks for fiat inflows and outflows. This worked until Wells Fargo severed correspondent relationships due to regulatory concerns over Tether’s rapid growth. In 2021, the U.S. Commodity Futures Trading Commission (CFTC) fined Tether $41 million for misrepresenting reserves, alleging its tokens weren’t fully backed.

Tether operates much like a traditional bank: accepting deposits, investing float, and earning interest. Roughly 80% of its issuance proceeds are invested in U.S. Treasuries. With short-term Treasury yields around 5%, its $120 billion in assets generates ~$6 billion annually. In 2024, Tether reported $13 billion in net profit. For comparison, Goldman Sachs earned $14.28 billion in net income the same year. Notably, Tether employs about 100 people, versus ~46,000 at Goldman Sachs. On a per-employee basis, Tether generated $130 million in profit per employee, compared to $310,000 at Goldman.

To build trust, some competitors emphasize transparency. Circle, for example, publishes monthly audits of USDC, detailing every mint and redemption. Yet the industry still relies on issuer credibility. In March 2023, Silicon Valley Bank’s (SVB) collapse temporarily froze $3.3 billion of Circle’s reserves, causing USDC to drop to 88 cents before the Fed stepped in to cover SVB depositors.

The U.S. government is now developing a clear regulatory framework. The GENIUS Act proposes key rules:

-

Reserves must be 100% backed by high-quality liquid assets (HQLA), such as U.S. Treasuries and reverse repurchase agreements.

-

Real-time auditing via licensed oracles.

-

Regulatory tools: include issuer freezing capabilities and compliance with FATF (Financial Action Task Force) standards.

-

Compliant stablecoins gain access to Federal Reserve master accounts and liquidity support via reverse repo facilities.

Under this model, a graphic designer in Berlin no longer needs a U.S. or German bank account or cumbersome SWIFT procedures to hold dollars. With just a Gmail address and quick KYC verification—and assuming Europe doesn’t mandate its own euro CBDC—he can participate. Funds are shifting from traditional bank ledgers to wallet-based apps, whose operators function increasingly like global banks without physical branches.

If this framework becomes law, existing stablecoin issuers face a choice: register in the U.S., undergo quarterly audits, anti-money laundering checks, and proof-of-reserves—or watch American platforms migrate to compliant alternatives. Circle already holds most of USDC’s backing assets in SEC-regulated money market funds, giving it a competitive edge.

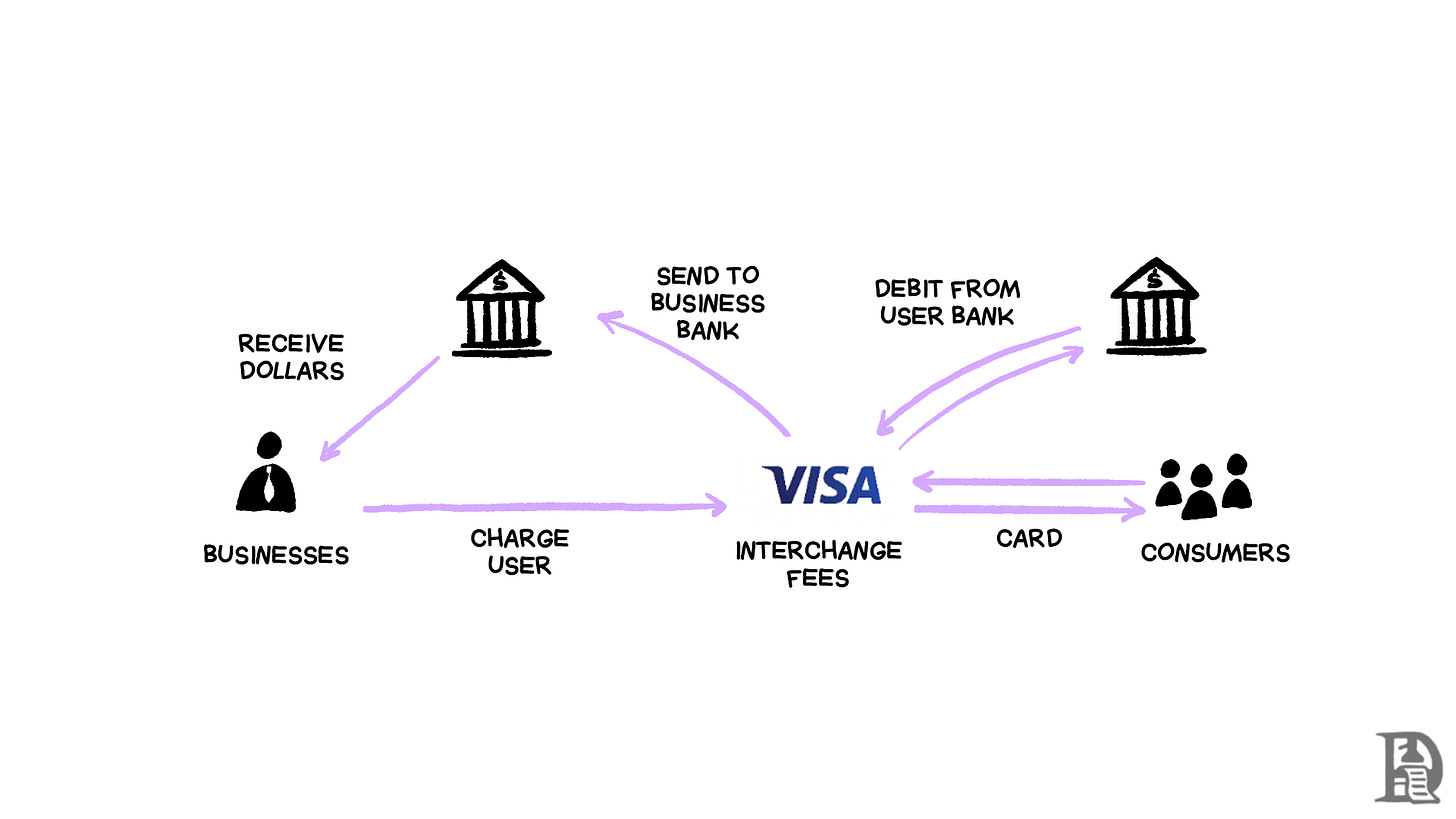

Tech giants and Wall Street are rushing into stablecoins. Imagine Apple Pay launching “iDollars”: users deposit $1,000 and earn rewards while spending anywhere contactless payments are accepted. The core appeal? Interest from idle cash balances exceeds current card swipe fees, reducing reliance on traditional financial intermediaries. This might explain Apple’s decision to end its credit card partnership with Goldman Sachs. When payments occur via “on-chain dollars”—blockchain-based dollar tokens—the traditional 3% transaction fee drops to mere cents in fixed blockchain costs.

Major U.S. banks are accelerating efforts too. Bank of America, Citibank, JPMorgan Chase, and Wells Fargo are jointly exploring stablecoin issuance. Notably, the GENIUS Act explicitly prohibits stablecoin issuers from sharing interest income with users—a provision likely welcomed by banking lobbyists. Think of these stablecoins as a new kind of “super-cheap checking account”: instant, global, and available 24/7.

Traditional financial players are adapting quickly. Mastercard (Mastercard) and Visa have launched dedicated stablecoin settlement networks. PayPal has issued its own stablecoin, and Stripe completed its acquisition of Bridge—now the largest crypto transaction ever. These moves signal widespread recognition of stablecoins’ future importance in finance.

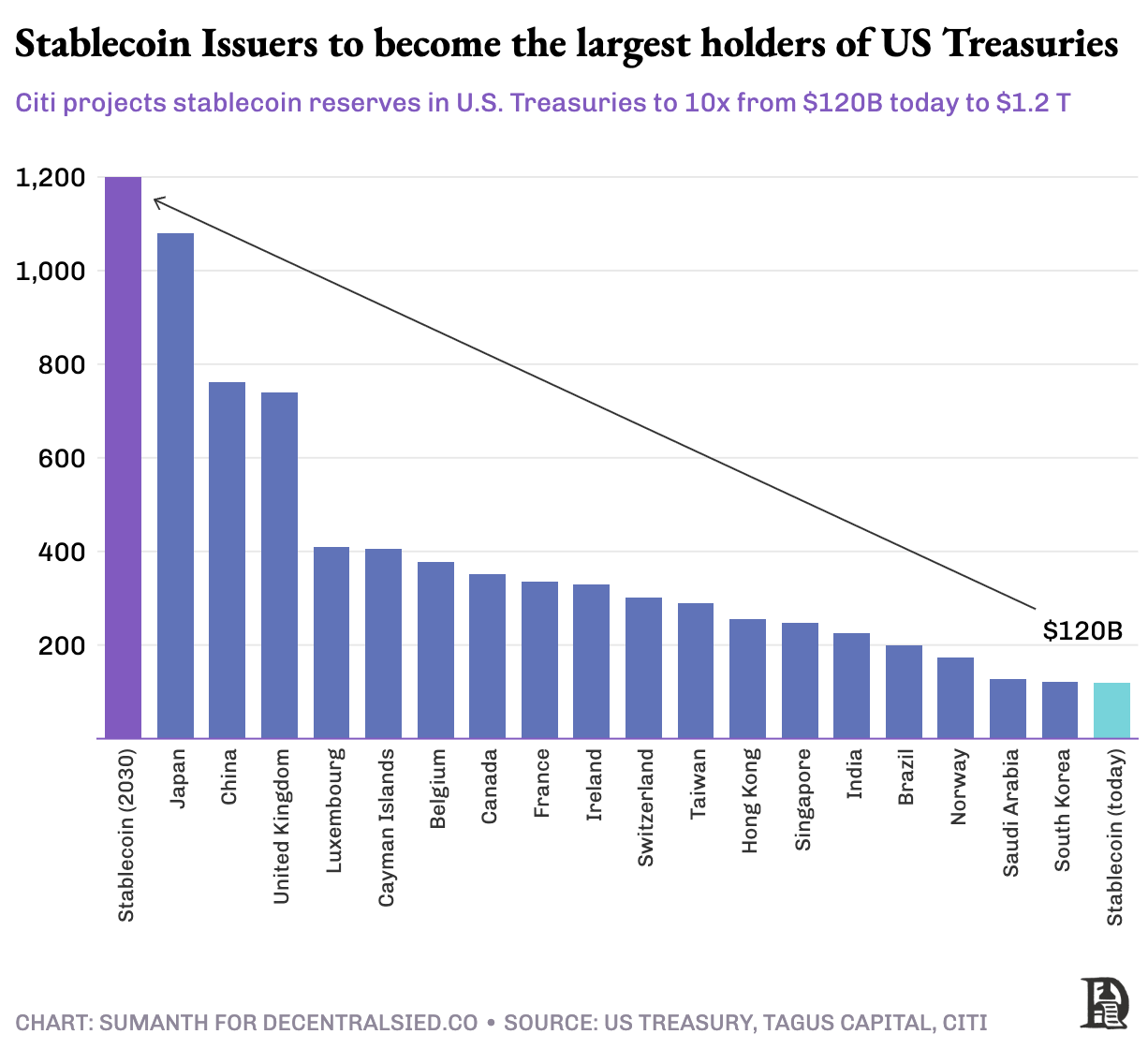

Meanwhile, Washington watches closely. Citi forecasts that under baseline assumptions, the stablecoin market will grow sixfold to $1.6 trillion by 2030. The U.S. Treasury’s research is even more optimistic, projecting $2 trillion by 2028. If the GENIUS Act requires 80% of stablecoin reserves to be invested in U.S. Treasuries, stablecoin issuers could replace China and Japan as the largest holders of U.S. debt. This shift would reinforce the dollar’s global standing and reshape the world’s financial architecture.

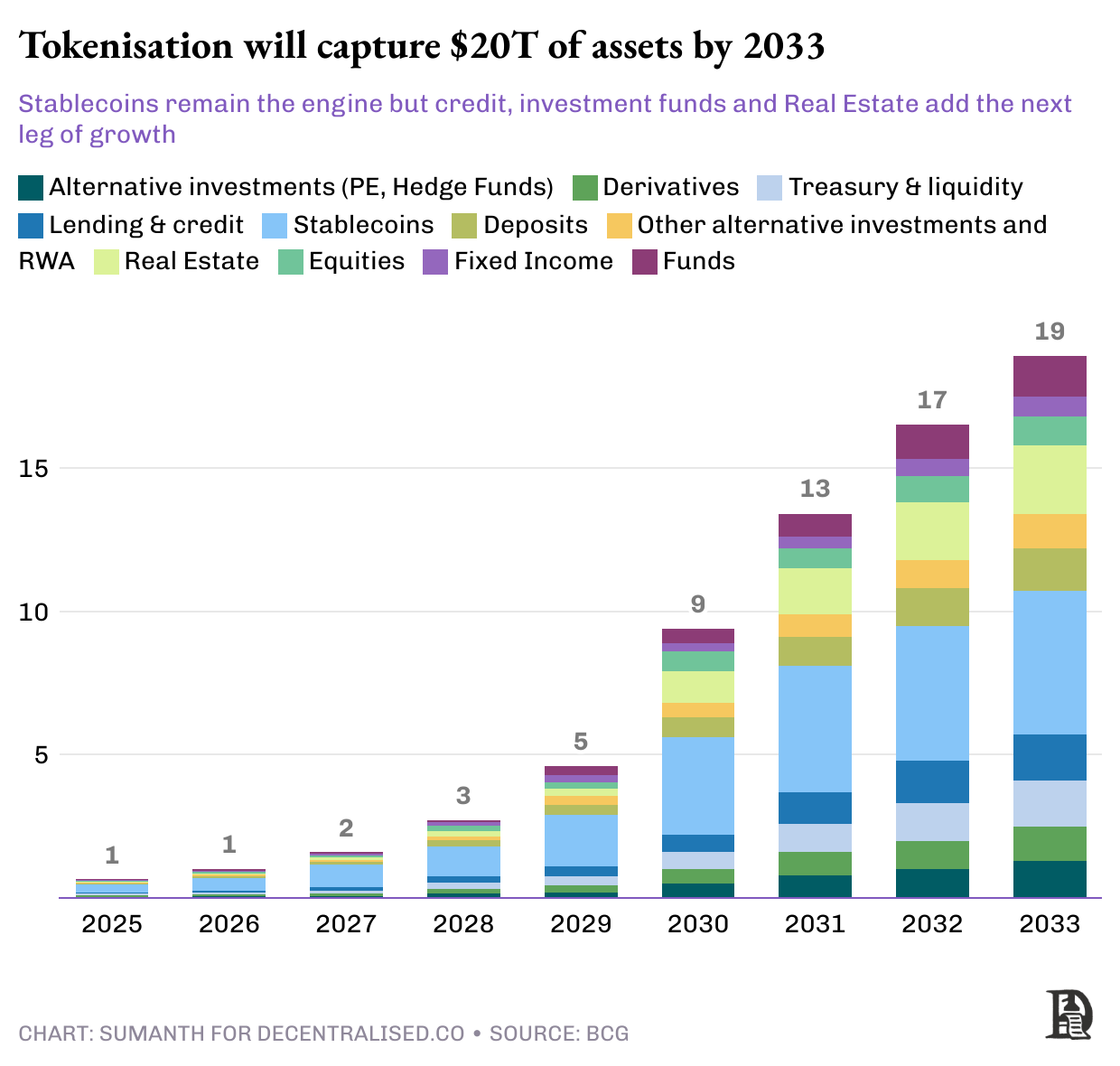

Applications and Advantages of Tokenized Assets

As “stabledollars” gain traction, they’re becoming the lifeblood powering the entire token economy. Once cash is tokenized, people treat it like traditional money—saving, lending, or using it as collateral—but at internet speed, not bank speed. This fast-moving capital drives more “real-world assets” (RWAs) onto blockchains, offering key advantages:

-

24/7 settlement: The traditional T+2 settlement cycle becomes obsolete, as blockchain validators confirm transactions in minutes. For instance, a trader in Singapore could buy a tokenized apartment in New York in the evening and confirm ownership before dinner.

-

Programmability: Smart contracts embed complex financial logic directly into assets—automated coupon payments, yield distribution rules, and built-in compliance parameters.

-

Composability: Tokenized assets can be flexibly combined. A tokenized Treasury bond can serve as loan collateral while distributing interest to multiple holders. An expensive beachfront villa can be split into 50 shares, co-owned by investors and leased to a hotel operator managed via Airbnb.

-

Transparency: Blockchain visibility allows regulators to monitor collateral ratios, systemic risks, and market dynamics in real time—preventing opaque derivative crises like the 2008 financial meltdown.

As BlackRock CEO Larry Fink stated: “Every stock, every bond, every fund—every asset—can be tokenized.”

The main obstacle remains regulatory clarity. Investors know what to expect on traditional exchanges because rules were forged through painful lessons.

Take the 1987 “Black Monday” stock crash, when the Dow plunged 22% in a day due to automated sell-offs triggered by falling prices, sparking a cascade. The SEC responded with circuit breakers—pausing trading so investors could reassess. Today, if the NYSE drops 7%, trading halts for 15 minutes.

Tokenizing assets is relatively straightforward—the issuer guarantees the token represents rights to an underlying real-world asset. The hard part is ensuring all rules are followed both on-chain and off-chain. This means embedding whitelisted wallets, national identity flows, cross-border KYC/AML requirements, citizen holding caps, and real-time sanctions screening—all into code.

Europe’s Markets in Crypto-Assets (MiCA) regulation offers a comprehensive manual for digital assets, while Singapore’s Payment Services Act serves as an Asian starting point. But the global regulatory map remains fragmented.

Adoption will almost certainly proceed in phases.

-

Phase One: The first assets to go on-chain will be highly liquid and low-risk instruments like money market funds and short-term corporate bonds. Benefits are immediate: settlement times shrink instantly, and compliance is simpler.

-

Phase Two: Risk increases with higher-yield products like private credit, structured finance, and long-term bonds. The goal shifts from efficiency to unlocking liquidity and enabling composability.

-

Phase Three: Expansion into illiquid assets—private equity, hedge funds, infrastructure, and real estate-backed debt. Reaching this stage requires broad acceptance of tokenized assets as collateral and cross-industry tech stacks capable of supporting them. Banks and institutions must custody these RWAs and provide credit lines.

While timelines vary across asset classes, the direction is clear. Every new batch of stabledollars pushes the token economy forward another step.

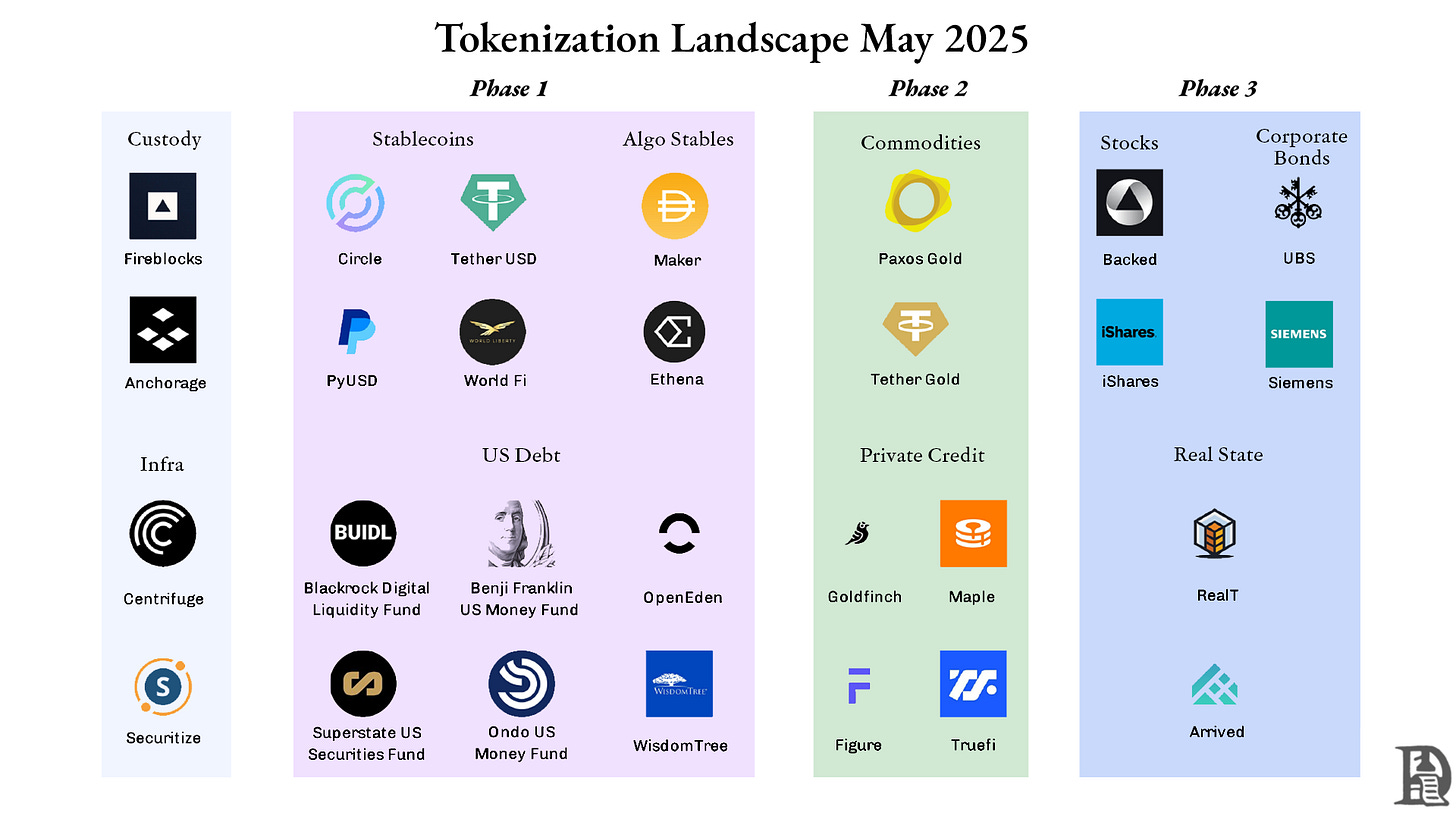

Stablecoins

The dollar-pegged token market is currently dominated by two giants: Tether (USDT) and Circle (USDC), together controlling 82% of the market. Both are fiat-collateralized stablecoins—each circulating token backed by fiat deposits (e.g., euro-denominated stablecoins backed by euros held in banks).

Beyond fiat models, developers are experimenting with two decentralized approaches to maintain price stability without relying on off-chain custodians:

-

Crypto-collateralized stablecoins: Backed by other cryptocurrencies, often overcollateralized to withstand volatility. MakerDAO’s DAI is the leading example, with $6 billion in circulation. After the 2022 bear market, MakerDAO shifted over half its collateral to tokenized Treasuries and short-term bonds, reducing exposure to ETH volatility while earning steady yields. These assets now contribute about 50% of the protocol’s revenue.

-

Algorithmic stablecoins: Rely on algorithmically controlled minting and burning mechanisms instead of collateral. Terra’s UST once reached a $20 billion market cap but collapsed when it lost its peg, triggering a loss of confidence and mass sell-offs. Though newer projects like Ethena have improved models and achieved $5 billion in market cap, broader acceptance will take time.

If the U.S. government restricts the term “qualified stablecoin” to fully fiat-backed tokens, other types may be forced to drop “USD” from their names. The future of algorithmic stablecoins remains uncertain—the GENIUS Act directs the Treasury to study these protocols within one year before making final decisions.

Money Markets

Money markets consist of highly liquid, short-term assets such as Treasuries, cash, and repos. On-chain funds “tokenize” these by packaging ownership into ERC-20 or SPL tokens. These instruments enable 24/7 redemptions, automatic yield distribution, seamless payment integration, and easy collateral management.

Asset managers retain traditional compliance processes (AML/KYC, qualified investor restrictions), but settlement drops from days to minutes.

BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) leads the space. The firm uses Securitize—an SEC-registered transfer agent—for KYC onboarding, token minting and redemption, FATCA/CRS tax reporting, and shareholder registry management. Investors need at least $5 million in investable assets, but once whitelisted, they can subscribe, redeem, or transfer tokens anytime—something impossible with traditional money market funds.

BUIDL has grown into a $2.5 billion fund spread across 70+ whitelisted holders on five blockchains. Around 80% of assets are in short-term Treasuries (1–3 months), 10% in long-term Treasuries, and the rest in cash.

Platforms like Ondo (OUSG) act as investment pools allocating capital across tokenized money market funds from BlackRock, Franklin Templeton, and WisdomTree, offering free stablecoin entry and exit.

Though $10 billion pales against the $26 trillion Treasury market, the trend is significant: Wall Street’s biggest asset managers are choosing public blockchains as distribution channels.

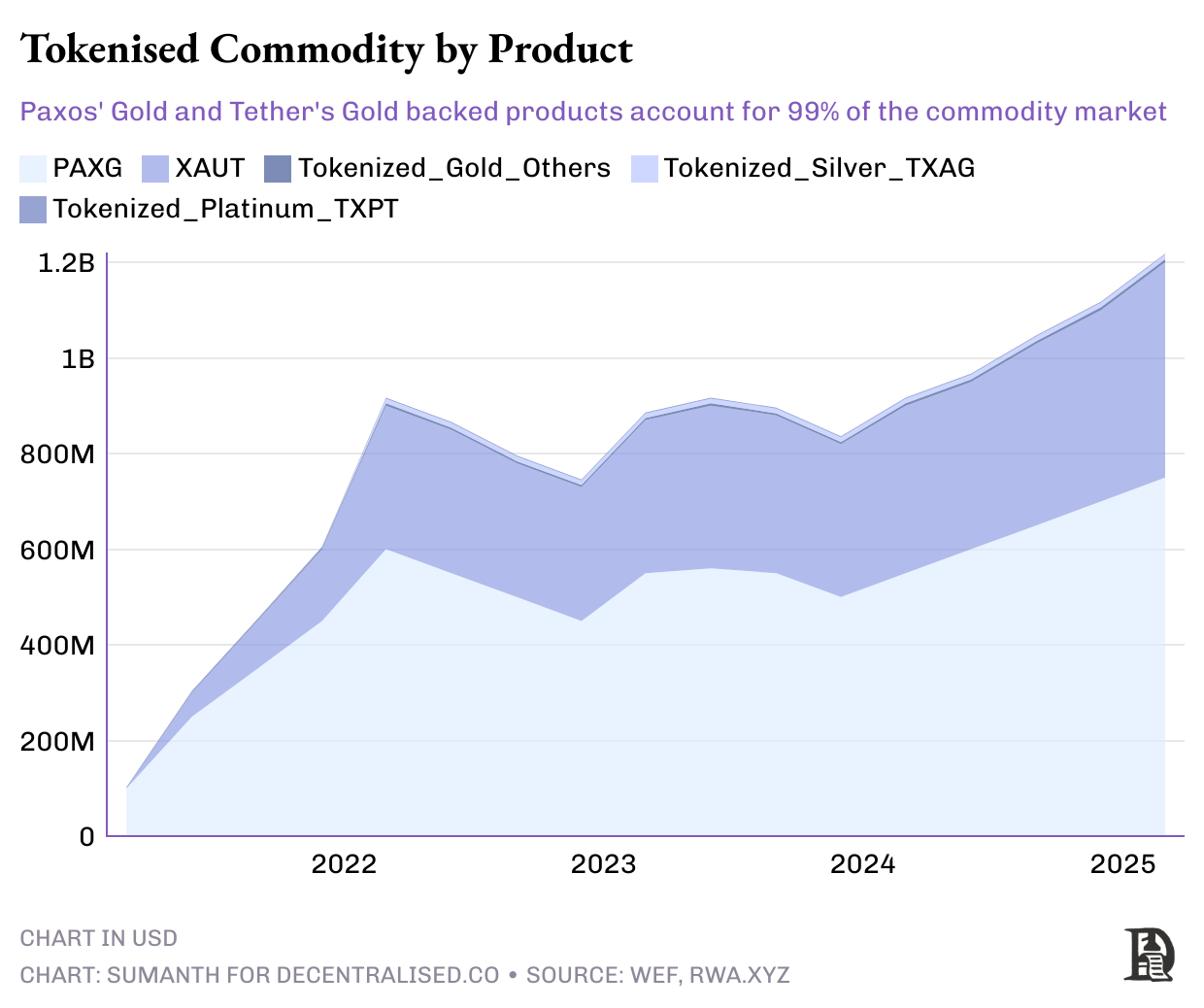

Commodities

Tokenizing hard assets is transforming these markets into 24/7, click-to-trade platforms. Paxos Gold (PAXG) and Tether Gold (XAUT) let anyone own fractional shares of tokenized gold bars. Venezuela’s PETRO experiment tokenized crude oil barrels; smaller pilots link tokens to soybeans, corn, or even carbon credits.

Current operations still depend on legacy infrastructure: gold bars stored in vaults, oil in tanks, auditors verifying reserves monthly. This custodial model introduces centralization risks, and physical redemption isn’t always feasible.

The benefit lies in divisible ownership, making traditionally illiquid physical assets easier to use as collateral. The market has reached $145 billion, almost entirely gold-backed. Compared to the $5 trillion physical gold market, there’s vast room for growth.

Lending and Credit: DeFi’s New Frontier

DeFi lending began with overcollateralized crypto loans. Users lock $150 worth of ETH or BTC to borrow $100—similar to gold-backed loans. Holders want to retain digital assets (believing they’ll appreciate) yet need liquidity for bills or new investments. Currently, Aave has ~$17 billion in total borrowing, nearly 65% of the entire DeFi lending market.

In traditional credit markets, banks dominate via long-tested risk models and strict capital rules. Private credit, a rising asset class, now manages $3 trillion globally, rivaling traditional lending. Companies issue high-risk, high-yield loans to attract institutional investors seeking better returns—like private equity firms and asset managers.

Bringing credit on-chain expands lender pools and boosts transparency. Smart contracts automate the full loan lifecycle—disbursement, interest collection, and transparent enforcement of liquidation terms.

Two On-Chain Private Credit Models

-

Retail-focused direct lending

-

Platforms like Figure tokenize home improvement loans and sell fractional notes to global retail investors—essentially crowdfunding for debt. Homeowners get cheaper financing via fractionation, while retail investors earn monthly returns, all managed automatically by the protocol.

-

Pyse and Glow tokenize power purchase agreements (PPAs) from solar projects, handling all operations—panel installation, meter readings. Investors simply contribute capital and receive 15–20% annual percentage yield (APY) from monthly electricity revenues.

-

Institutional liquidity pools: Transparent on-chain private credit

-

On-chain private credit pools offer transparent environments. Protocols like Maple, Goldfinch, and Centrifuge pool borrower demands into on-chain credit pools managed by professional underwriters. Depositors include accredited investors, DAOs, and family offices. They track performance via public ledgers and earn floating yields of 7–12%.

-

Cost-efficient on-chain credit protocols

-

These protocols reduce costs by using on-chain underwriters to conduct due diligence and disburse loans within 24 hours. For example, Qiro leverages a network of underwriters, each with proprietary credit models, rewarded based on analysis accuracy. However, due to higher default risks, growth lags behind secured lending. When defaults occur, these protocols lack legal recourse and must rely on traditional collection agencies—adding hidden costs.

As underwriters, auditors, and collection agents move on-chain, credit market operating costs will decline further, attracting more lenders.

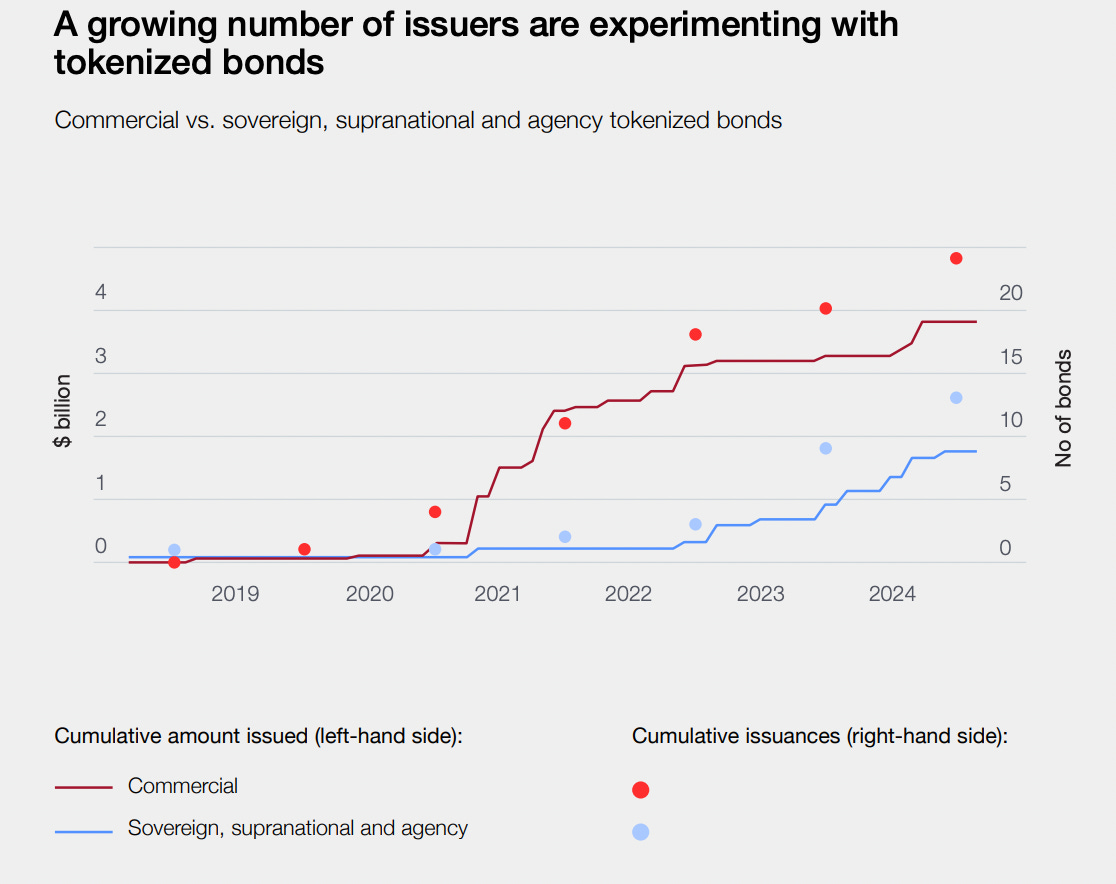

Tokenized Bonds: The Future of Debt Markets

Bonds and loans, though both debt instruments, differ in structure, standardization, and issuance/trading methods. Loans are typically “one-on-one” agreements, whereas bonds are “one-to-many” instruments with fixed formats. For example, a 10-year bond with a 5% annual coupon is easier to rate and trade on secondary markets. As public financial instruments, bonds are regulated and usually rated by agencies like Moody’s.

Bonds meet large-scale, long-term capital needs. Governments, utilities, and blue-chip firms issue bonds to fund budgets, factory construction, or short-term financing. Investors receive regular coupon payments and principal repayment at maturity. This market is enormous: as of 2023, global bond markets totaled $140 trillion in notional value—about 1.5x global stock market capitalization.

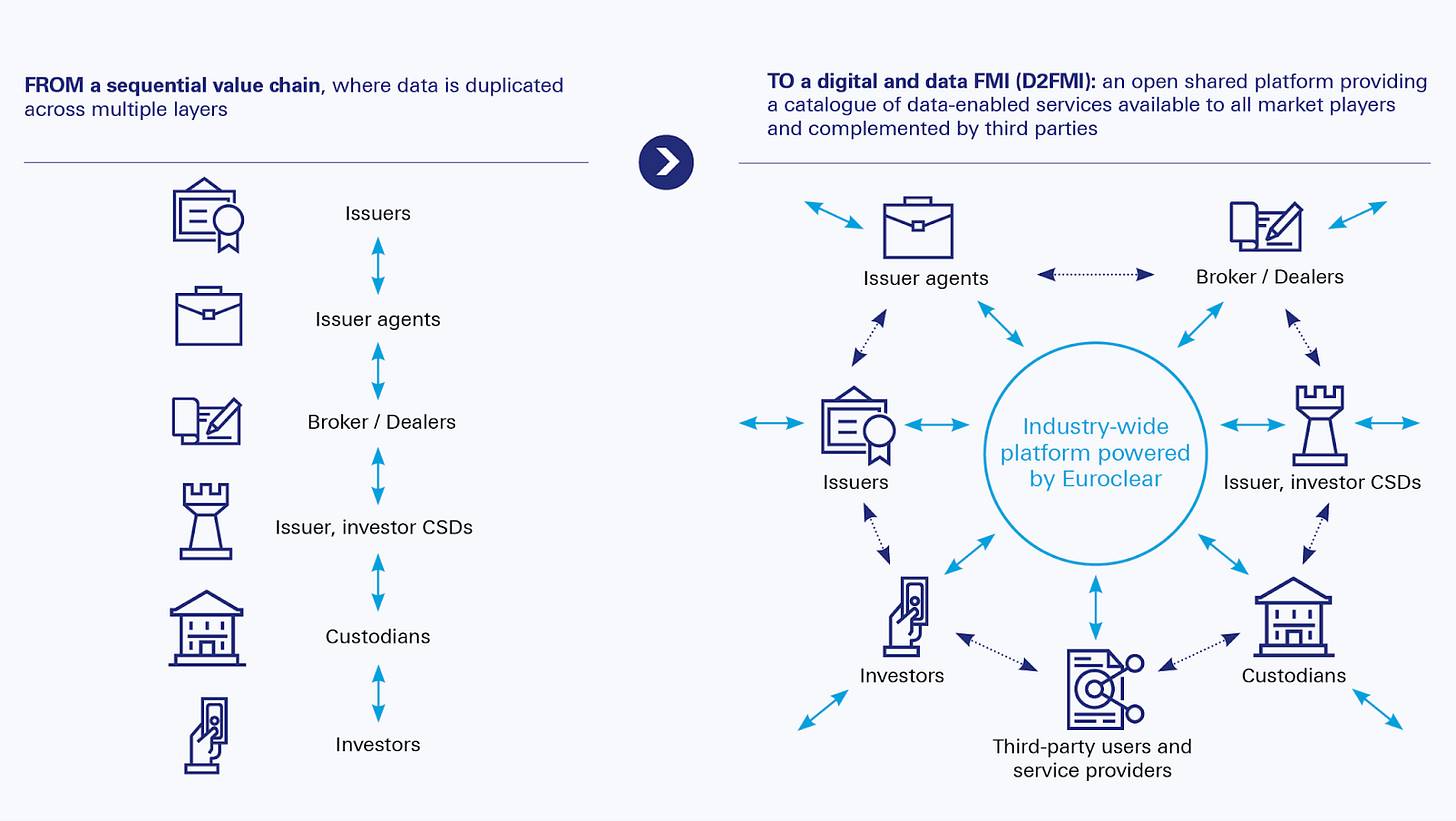

Yet today’s bond markets still rely on 1970s-era clearing systems. Clearinghouses like Euroclear and DTCC require multiple intermediaries, causing delays and resulting in T+2 settlement. Smart contract bonds, however, can achieve atomic settlement in seconds and distribute coupons automatically to thousands of wallets. They can embed compliance logic and tap into global liquidity pools.

Each smart contract bond issuance saves 40–60 basis points in operational costs. Additionally, treasurers gain a 24/7 secondary market without exchange listing fees. Euroclear, Europe’s core settlement and custody network managing €40 trillion in assets across 2,000+ participants in 50 markets, is building a blockchain-based platform connecting issuers, brokers, and custodians—to eliminate redundancies, reduce risk, and deliver real-time digital workflows.

Source: Euroclear

Companies like Siemens and UBS have issued on-chain bonds in ECB trials. Japan is testing the waters, partnering with Nomura to tokenize bonds.

Source: WEF Insights

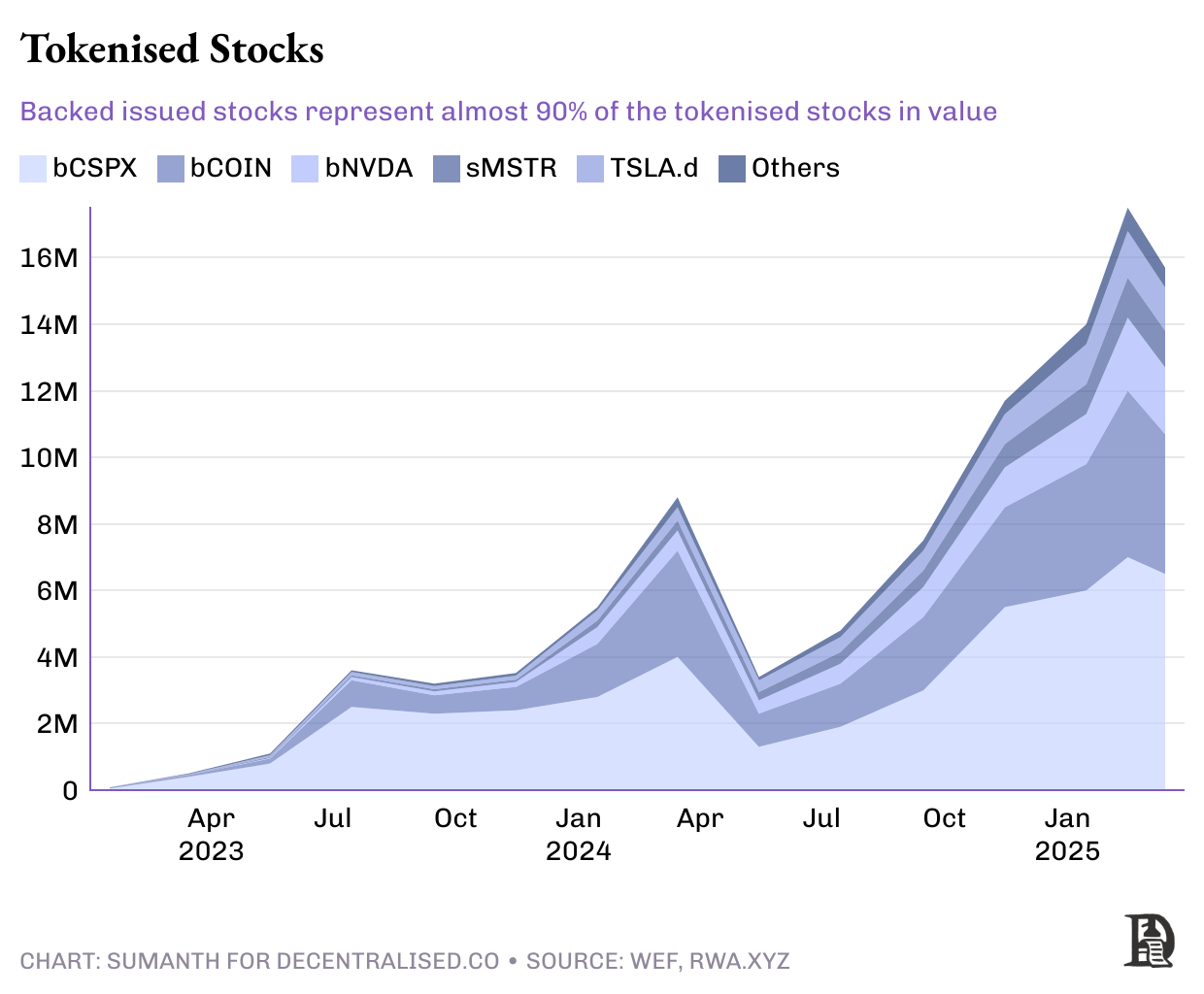

Stock Markets

This area naturally appears promising, having already attracted many retail investors. Tokenization could create a 24/7 “internet capital market.”

Current barriers are regulatory. SEC custody and settlement rules were written before blockchains existed, requiring intermediaries and T+2 settlement.

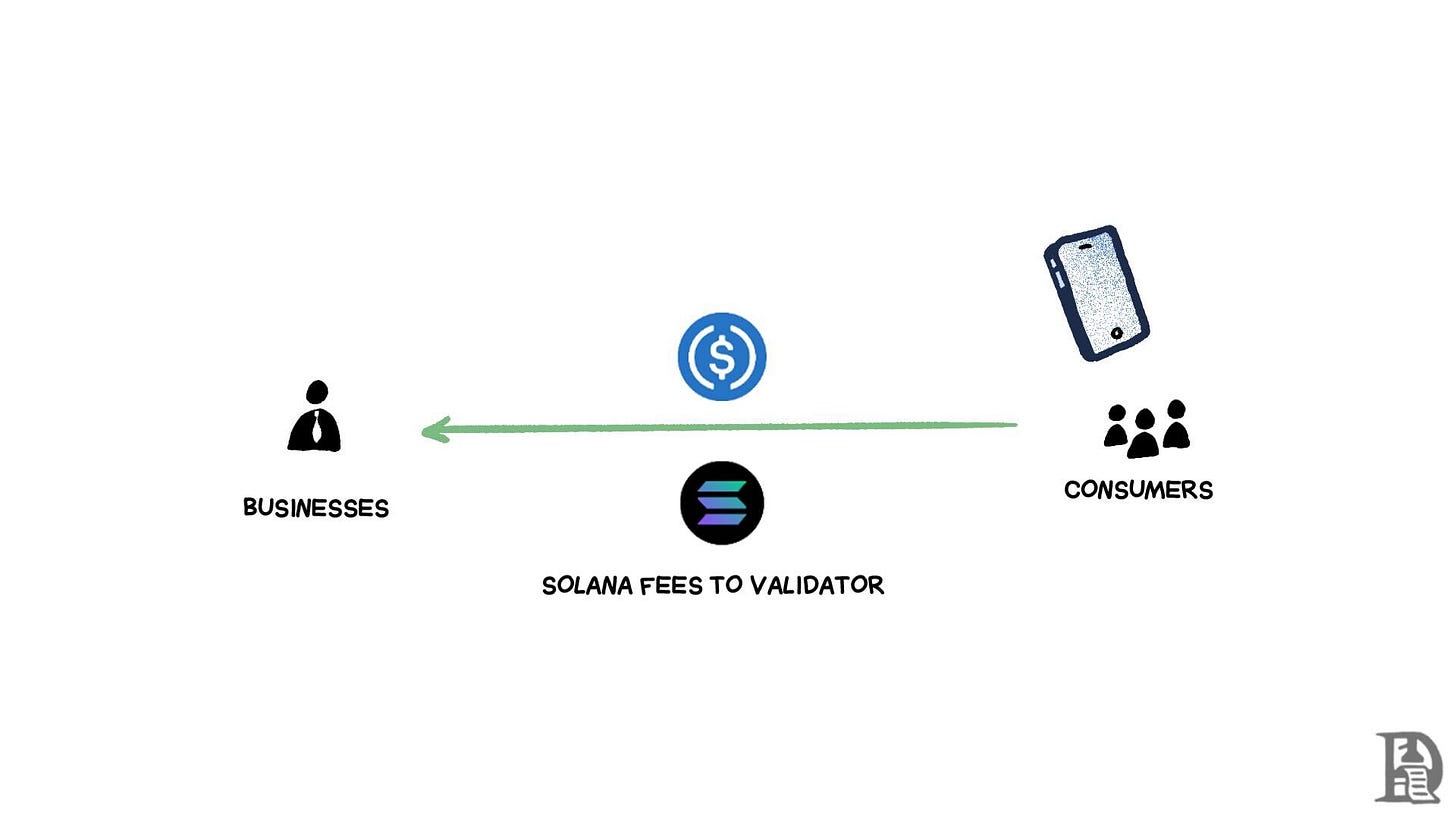

But change is coming. Solana has applied to the SEC for approval to conduct on-chain stock issuance, offering full services including KYC, investor education, broker custody, and instant settlement.

Robinhood has filed a similar request, asking the SEC to treat tokens representing U.S. Treasuries or Tesla shares as securities themselves—not synthetic derivatives.

Outside the U.S., demand is stronger. Without strict limits, foreign investors already hold about $19 trillion in U.S. stocks. Traditional access involves domestic brokers like eTrade working with U.S. financial institutions—but with high forex spreads.

Startups like Backed offer alternatives via synthetic assets. Backed buys equivalent underlying stocks in U.S. markets, completing $16 million in trades. Kraken recently partnered with Backed to offer U.S. stock trading to non-U.S. traders.

Real Estate and Alternative Assets

Real estate is among the most paper-dependent asset classes. Each deed must be recorded in a government registry; every mortgage sits in a bank vault. Unless registries accept cryptographic hashes as legal proof of ownership, mass tokenization remains impractical. That’s why only about $20 billion of the world’s $400 trillion real estate is currently on-chain.

The UAE is a regional leader, with $3 billion in property deeds registered on-chain. In the U.S., startups like RealT and Lofty AI have tokenized over $100 million in residential properties, streaming rental income directly to investor wallets.

Money Wants to Move

Cypherpunks see “stabledollars” as a regression—returning to bank custody and permissioned whitelists. Regulators, meanwhile, distrust permissionless blockchain systems capable of moving billions in a single block. In reality, blockchain adoption thrives precisely at the intersection where these extremes meet discomfort.

Purists may continue to complain, just as early internet advocates once opposed centrally issued TLS certificates. Yet it was HTTPS that enabled our parents to safely use online banking. Similarly, while stabledollars and tokenized Treasuries may seem “impure,” they are the gateway for billions to experience blockchain through applications that never mention the word “crypto.”

The Bretton Woods system bound the global economy to a single currency framework. Blockchain breaks that constraint by accelerating money’s velocity. Every time we move an asset on-chain, we save settlement time, free up collateral stuck in clearinghouses, and allow the same dollar to facilitate three transactions before lunch.

At Decentralised.co, we stand by one principle: Speeding up money movement is crypto’s killer app, and bringing real-world assets (RWA) on-chain perfectly aligns with this trend. The faster value clears, the more frequently capital can be redeployed—expanding the overall economy. When dollars, debts, and data flow at network speed, business models will no longer depend on charging for the “movement” process, but instead generate new revenue from the “momentum” effect.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News