GENIUS Act Stablecoin Bill Passes Vote: Which Crypto Assets Will Benefit?

TechFlow Selected TechFlow Selected

GENIUS Act Stablecoin Bill Passes Vote: Which Crypto Assets Will Benefit?

The passage of the GENIUS Act provides a new pathway for extending dollar hegemony while driving comprehensive prosperity in the crypto ecosystem.

Author: TechFlow

Market sentiment in crypto has once again focused on regulatory developments.

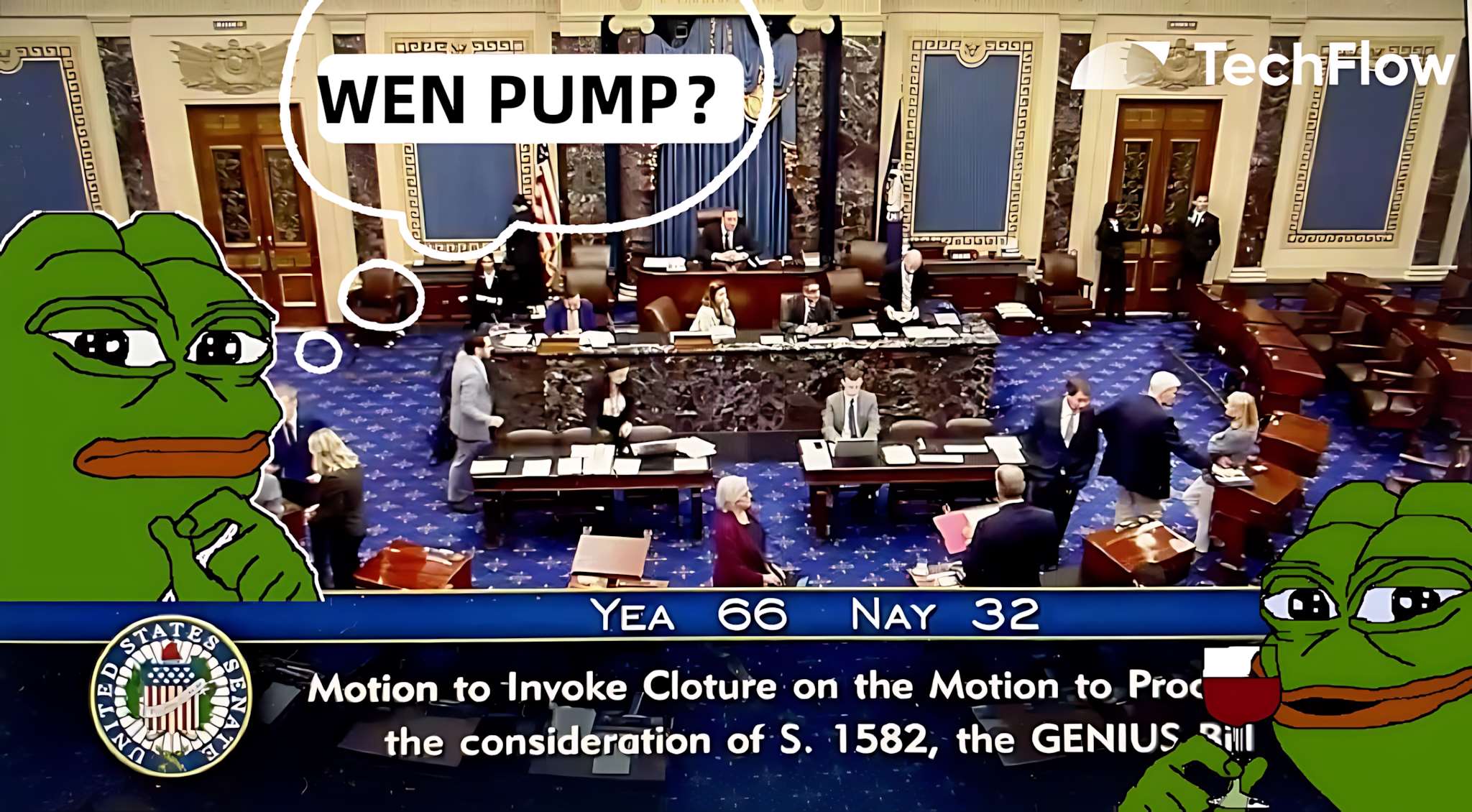

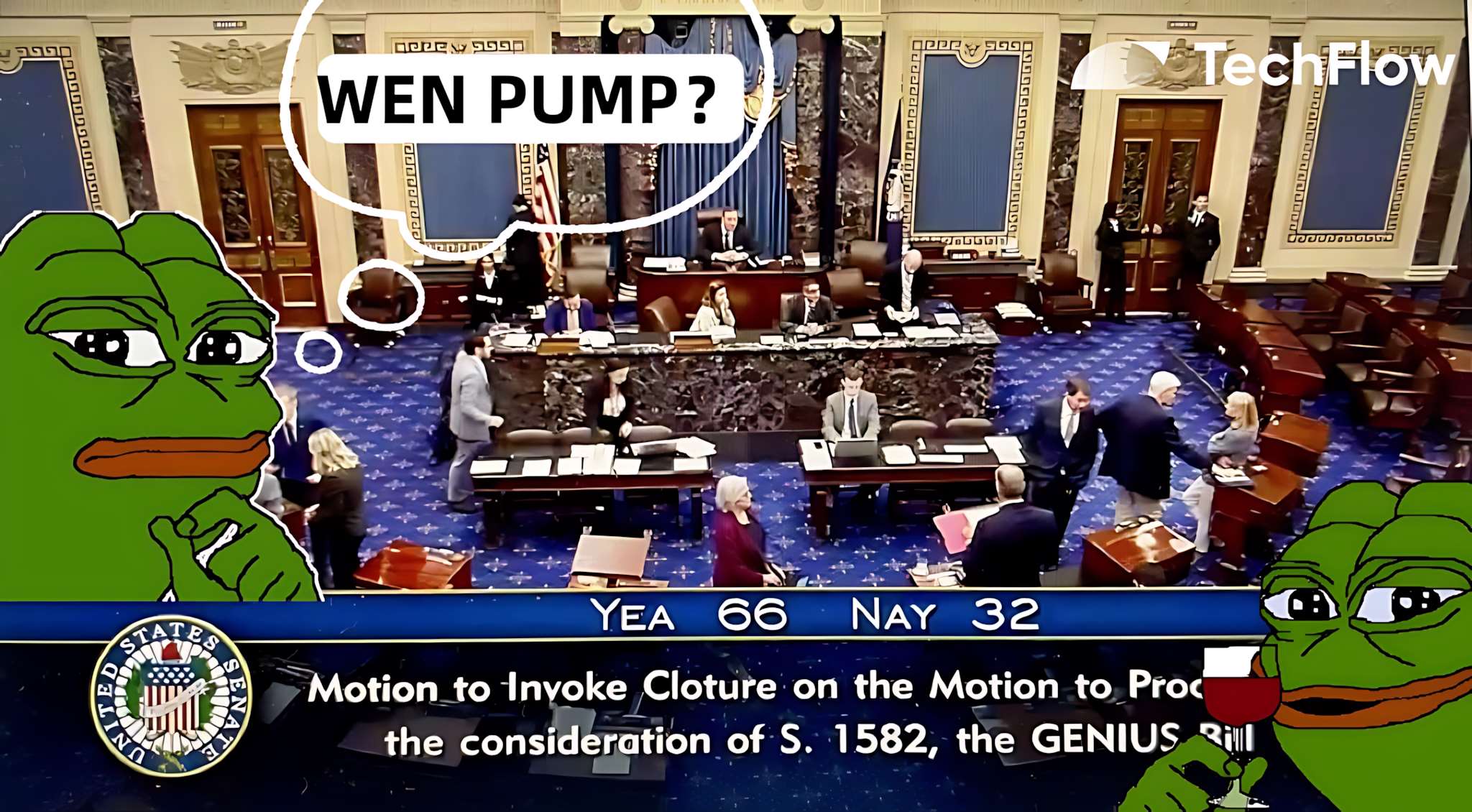

On May 19, the U.S. Senate passed a procedural vote on the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025) by a margin of 66-32. This milestone marks the imminent establishment of a federal regulatory framework for stablecoins in the United States.

As the first comprehensive federal stablecoin regulation in U.S. history, the rapid advancement of the GENIUS Act has triggered strong reactions in the crypto market, with DeFi and RWA sectors linked to stablecoins leading today’s market gains.

Could the GENIUS Act become the catalyst for a new bull run?

Citibank forecasts that the global stablecoin market could reach $1.6–3.7 trillion by 2030. The passage of this bill further legitimizes stablecoins under “compliance,” offering clearer room for development and providing traditional companies with stronger incentives to enter the space.

The market also anticipates an influx of capital—“a flood of liquidity”—that could inject fresh liquidity into related crypto assets.

However, before that happens, it's essential to understand what exactly is in this legislation and the motivations behind it, so you can make more compelling investment decisions regarding relevant crypto assets.

From “Wild West” Growth to Regulation

GENIUS Act literally translates to “Genius Act,” but it is actually an acronym for the Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025.

In simple terms, it is an official legislative document issued at the national level in the U.S.

The reason the market is paying attention is that it represents the first comprehensive federal regulatory bill targeting stablecoins in American history. Prior to this, stablecoins and cryptocurrencies have existed in a gray area:

Not explicitly banned, yet lacking clear rules on how they should operate.

The goal of the GENIUS Act is to establish a clear regulatory framework, providing legitimacy and security to the stablecoin market while reinforcing the dollar’s dominance indigital finance.

In summary, key provisions of the bill include:

-

Reserve Requirements: Stablecoin issuers must maintain full 100% backing, with reserves composed of highly liquid assets such as U.S. dollars or short-term U.S. Treasury securities, and must disclose reserve composition monthly.

-

Tiered Regulation: Large issuers with market capitalization exceeding $10 billion (e.g., Tether, Circle) will be directly regulated by the Federal Reserve System or the Office of the Comptroller of the Currency (OCC), while smaller issuers may fall under state-level oversight.

-

Transparency and Compliance: Prohibits misleading marketing claims (such as implying U.S. government backing), requires adherence to anti-money laundering (AML) and know-your-customer (KYC) regulations, and mandates annual financial audits for issuers with market caps over $50 billion to ensure transparency.

This implies that the U.S. takes a fundamentally favorable stance toward stablecoins—as long as they are backed by the U.S. dollar and meet requirements for public transparency.

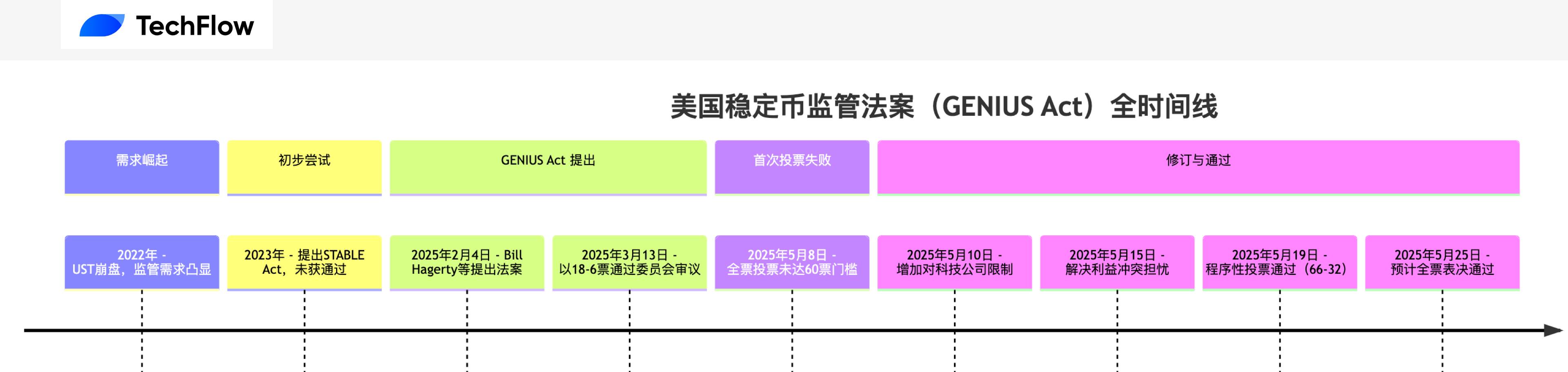

Looking back, the emergence of the GENIUS Act was not sudden, but rather the culmination of years of regulatory exploration in the U.S. We’ve summarized the full timeline of the bill to help you quickly grasp its background and intent:

The stablecoin market has grown rapidly, but risks arising from regulatory gaps have become increasingly evident—for example, the collapse of algorithmic stablecoin UST in 2022 highlighted the urgent need for clear regulation.

As early as 2023, the House Financial Services Committee proposed the STABLE Act to create a regulatory framework for stablecoins, but it failed to pass in the Senate due to partisan disagreements.

On February 4, 2025, Senator Bill Hagerty, jointly with bipartisan lawmakers Kirsten Gillibrand and Cynthia Lummis, officially introduced the GENIUS Act, aiming to balance innovation and regulation. On March 13, the bill passed the Senate Banking Committee by a vote of 18-6, demonstrating strong bipartisan support.

However, the first full chamber vote on May 8 failed to reach the 60-vote threshold (48-49), as some Democratic senators (e.g., Elizabeth Warren) expressed concerns that the bill might benefit Trump-affiliated crypto projects (such as the USD1 stablecoin), raising conflict-of-interest issues.

After revisions adding restrictions on big tech companies, concerns about conflicts of interest were alleviated, and the bill ultimately passed the procedural vote on May 19 by 66-32. It is expected to soon pass final Senate approval by simple majority.

So, what does this legislative progress mean?

First, the market craves certainty. The passage of the bill essentially marks the transition of the U.S. stablecoin market from unregulated growth to formalization, filling a longstanding regulatory void and providing clarity.

Second, it openly signals an intent to reinforce the dollar’s global position through stablecoins—particularly amid competitive pressures from China’s digital yuan and the EU’s MiCA regulations.

Finally, the advancement of the GENIUS Act could pave the way for broader crypto legislation (such as market structure bills), accelerating the integration of the crypto industry with traditional finance and providing a legal foundation for mainstream adoption.

Crypto Assets with Stakes in the Game

The core provisions of the GENIUS Act directly impact the stablecoin ecosystem and, through ripple effects, influence the broader crypto market. This regulatory framework will not only reshape the stablecoin industry but also affect multiple crypto sectors—including DeFi, Layer 1 blockchains, and RWA—due to the widespread use of stablecoins.

Some projects in these sectors do not fully comply with the bill’s requirements. If the bill is viewed as beneficial, adjustments in product design and operations will be necessary.

We’ve compiled a list of major projects, outlining their potential benefits and required adjustments.

-

Centralized Stablecoin Issuers:

The bill’s reserve requirements (100% liquid assets, including U.S. Treasuries) and transparency mandates (e.g., monthly disclosures) favor centralized stablecoins. These issuers already largely meet the criteria, and regulatory clarity will attract more institutional capital, expanding their usage in trading and payments.

$USDT (Tether): USDT is the largest stablecoin by market cap (~$130 billion in 2025), with approximately 60% of its reserves in short-term U.S. Treasuries (~$78 billion) and 40% in cash and cash equivalents (source: Tether Q1 2025 Transparency Report).

The GENIUS Act’s emphasis on Treasury-backed reserves aligns well with Tether’s current setup, and its transparency practices (e.g., quarterly audits) meet the bill’s standards. However, USDT’s historical association with gray-market activities (e.g., fraud) means business model adjustments may be needed to fully comply with regulations.

$USDC (Circle): USDC has a market cap of ~$60 billion, with 80% of reserves in short-term U.S. Treasuries (~$48 billion) and 20% in cash (source: Circle Monthly Report, May 2025). Circle is already registered in the U.S. and actively cooperates with regulators (e.g., filed for IPO in 2024), and its reserves fully comply with the bill. Passage of the act may solidify USDC as the preferred institutional stablecoin, especially in DeFi (where USDC accounted for 30% of usage in 2025), potentially increasing its market share.

-

Decentralized Stablecoins:

$MKR (MakerDAO, issuer of DAI): DAI is the largest decentralized stablecoin (market cap ~$9 billion), minted through over-collateralization of crypto assets like ETH. About 10% of its reserves (~$900 million) are in U.S. Treasuries, with the rest primarily in crypto collateral (source: MakerDAO Report, May 2025).

The strict reserve requirements in the GENIUS Act could pose challenges for DAI, but if MakerDAO increases its Treasury holdings, it could benefit from overall market growth. $MKR holders may profit from increased DAI usage (MakerDAO protocol revenue reached ~$200 million annually in 2025).

$FXS (Frax Finance, issuer of FRAX): FRAX has a market cap of ~$2 billion and uses a hybrid mechanism (50% collateralized, 50% algorithmic), with ~15% of collateral (~$300 million) in U.S. Treasuries. If Frax shifts to full collateralization and increases Treasury exposure, it could benefit from market expansion, though its algorithmic component may face regulatory scrutiny, as the bill does not protect algorithmic stablecoins.

$ENA (Ethena Labs, issuer of USDe): USDe has a market cap of ~$1.4 billion and relies on ETH hedging and yield strategies, with only 5% of reserves (~$70 million) in U.S. Treasuries.

Ethena’s strategy may require significant adjustments to meet compliance, but if successful, it could gain from market growth—though risks remain.

-

DeFi Trading/Lending

$CRV (Curve Finance): Curve specializes in stablecoin trading (TVL ~$2 billion in 2025), with 70% of its liquidity pools consisting of stablecoin pairs (e.g., USDT/USDC).

Increased stablecoin usage driven by the GENIUS Act will directly boost Curve’s trading volume (currently averaging ~$300 million daily). $CRV holders benefit from trading fees (yielding ~5% APY) and governance rights. If the stablecoin market grows as Citibank predicts, Curve’s TVL could rise another 20%.

$UNI (Uniswap): Uniswap is a general-purpose DEX (TVL ~$5 billion in 2025), with stablecoin pairs (e.g., USDC/ETH) accounting for 30% of its liquidity. Rising stablecoin transaction activity will indirectly benefit Uniswap, though less so than Curve due to its diversified business. $UNI holders earn from trading fees (~3% APY).

$AAVE (Aave): Aave is the largest lending protocol (TVL ~$10 billion in 2025), with stablecoins (e.g., USDC, DAI) making up ~40% of its lending pools.

The bill will likely encourage more users to borrow/lend using stablecoins (e.g., collateralizing USDC to borrow ETH), further increasing deposit and loan volumes. $AAVE holders benefit from protocol revenue (~$150 million annually in 2025) and potential token appreciation.

$COMP (Compound): Compound has a TVL of ~$3 billion, with ~35% in stablecoin lending. Similar to Aave, increased stablecoin borrowing will benefit Compound, but its slower innovation and smaller market share suggest $COMP’s upside may be more limited.

-

Yield Protocols

$PENDLE (Pendle): Pendle focuses on yield tokenization (TVL ~$500 million in 2025), with stablecoins commonly used in yield strategies (e.g., USDC yield pools currently yielding ~3% APY). Growth in the stablecoin market will expand Pendle’s yield opportunities (potentially rising to 5% APY), benefiting $PENDLE holders through increased protocol revenue (~$30 million annually in 2025).

-

Layer 1 Blockchains

$ETH (Ethereum): Ethereum hosts 90% of stablecoin and DeFi activity (DeFi TVL exceeding $100 billion in 2025). Increased stablecoin usage will drive higher on-chain transaction volume (Gas fee revenue ~$2 billion annually), potentially boosting $ETH value due to rising demand.

$TRX (Tron): Tron is a major network for stablecoin circulation. Public data shows ~$60 billion of USDT in circulation on Tron in 2025, representing 46% of total USDT supply. Increased stablecoin usage may further boost Tron’s on-chain activity.

$SOL (Solana): Solana’s high throughput and low cost make it a key platform for stablecoins and DeFi (TVL ~$8 billion in 2025, ~$5 billion of USDC in circulation). Rising stablecoin usage will fuel DeFi activity (current daily trading volume ~$1 billion), benefiting $SOL as on-chain activity grows.

$SUI (Sui): Sui is an emerging Layer 1 (TVL ~$1 billion in 2025), supporting stablecoin applications (e.g., Thala’s stablecoin and DEX). Growth in the stablecoin ecosystem may attract more projects to deploy on Sui, benefiting $SUI as ecosystem activity increases (current daily active users ~500k).

$APT (Aptos): Aptos is another emerging Layer 1 (TVL ~$800 million in 2025), with ecosystem support for stablecoin payments. Increased stablecoin circulation may drive adoption of payment and DeFi apps on Aptos, benefiting $APT as user numbers grow.

-

Payments Sector

$XRP (Ripple): XRP focuses on cross-border payments (average daily trading volume ~$2 billion in 2025). Its low cost and high efficiency complement stablecoins. Rising demand for stablecoin-based cross-border payments (e.g., USDC for international settlements) may expand XRP’s use cases (e.g., as a bridge currency), benefiting $XRP as payment demand grows.

$XLM (Stellar): Stellar also specializes in cross-border payments (average daily trading volume ~$500 million in 2025) and previously partnered with IBM on the World Wire project, using stablecoins as bridge assets.

-

Oracles

$LINK + $PYTH: Oracles provide price data for stablecoins and DeFi. The expansion of the stablecoin market under the GENIUS Act will increase demand for real-time pricing data, driving higher on-chain data call volumes.

However, this is more of a sector-wide benefit rather than a direct, strong correlation.

-

RWA

$ONDO (Ondo Finance): Focuses on tokenizing fixed-income assets like U.S. Treasuries. Its flagship product USDY (a Treasury-backed yield-bearing stablecoin) is already live on chains like Solana and Ethereum (USDY circulating supply ~$500 million in 2025). The GENIUS Act’s requirement for stablecoin reserves to hold U.S. Treasuries directly benefits Ondo’s tokenization business, potentially making USDY a preferred reserve asset for stablecoin issuers. Additionally, increased stablecoin circulation may drive retail and institutional investors to purchase USDY using USDC, boosting demand for Ondo’s asset tokenization services and benefiting $ONDO holders.

Dollar: The Bigger Play

The U.S. push for stablecoin legislation is essentially an open “grand strategy.”

On one hand, the U.S. favors a weaker dollar policy to boost exports; on the other, it refuses to relinquish the dollar’s global monetary dominance.

By supporting stablecoin development, the U.S. extends the dollar’s global reach digitally—without increasing the Fed’s liabilities. Currently, 99% of stablecoins are pegged to the dollar.

Moreover, the regulatory mandate requiring stablecoins to hold U.S. short-term Treasuries cleverly creates new buyers for U.S. debt—Tether’s Treasury holdings alone now exceed those of many developed nations.

This policy achieves two goals at once: maintaining the dollar’s global supremacy while securing reliable buyers for America’s massive debt burden.

The passage of the GENIUS Act is undoubtedly a milestone for the crypto market. By tying stablecoins to the dollar and U.S. Treasuries, it opens a new path for sustaining dollar hegemony while driving broad prosperity across the crypto ecosystem.

Yet this “grand strategy” is a double-edged sword—while creating opportunities, its heavy reliance on U.S. debt, potential constraints on DeFi innovation, and global competitive uncertainties could all become future risks.

Still, uncertainty has always been the ladder upon which the crypto market advances.

Risks may be uncertain, but participants are all waiting for a certain bull market to arrive.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News