sUSD Depegged by 16%: Is the Stablecoin Myth Shattered or a Golden Opportunity to Buy the Dip?

TechFlow Selected TechFlow Selected

sUSD Depegged by 16%: Is the Stablecoin Myth Shattered or a Golden Opportunity to Buy the Dip?

This issue originated from the transitional period of mechanism adjustments triggered by the SIP-420 proposal, causing sUSD's peg correction mechanism to temporarily fail.

Author: Oliver, Mars Finance

Synthetix's core stablecoin sUSD has recently plunged into a severe depegging crisis. As of April 9, 2025, its price fell to approximately $0.8388, deviating more than 16% from its $1 peg, drawing significant market attention. This crisis began on March 20 and has now lasted over 20 days, with the depegging widening steadily. Meanwhile, Synthetix’s native token SNX has risen逆势, gaining 7.5% in a single day, reflecting complex market sentiment. Kain Warwick (@kaiynne), founder of Synthetix, attributed the depeg to transitional pains from mechanism upgrades and revealed that the protocol had sold 90% of its ETH position and increased SNX holdings to respond.

Timeline: The Gradual Worsening of Depegging

The sUSD depeg did not happen overnight. On March 20, 2025, its price first slightly drifted, initially raising little concern. However, over time, this fluctuation evolved into a sustained downtrend. By April 9, CoinMarketCap data showed sUSD trading at just $0.8388—over 16% below its $1 peg. This prolonged depeg, lasting more than 20 days, exceeds both expected duration and typical market tolerance for stablecoins, revealing the underlying complexity of the issue.

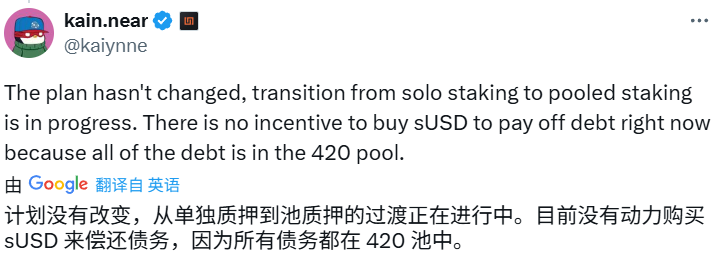

Kain Warwick explained on X that the depeg is an anticipated side effect of SIP-420 implementation. This proposal aims to optimize SNX staking and capital efficiency by introducing a centralized debt pool (the "420 Pool"), but the transition between old and new mechanisms has temporarily disabled sUSD's ability to self-correct its peg. He admitted outright that currently, “there is no incentive for users to buy sUSD to repay debt,” making supply-demand imbalance the direct driver of price decline. Additionally, the protocol's strategy of selling 90% of its ETH position and reallocating into SNX, while intended to strengthen internal support, may have weakened system liquidity and external stability foundations, adding further uncertainty to the market.

Root Causes: Interplay Between Mechanism Transition and Market Feedback

The cause of this depeg is not singular, but rather a convergence of mechanism changes and market behavior, presenting multi-layered challenges.

SIP-420 implementation is the central trigger. Synthetix’s stablecoin relies on over-collateralization of SNX: users mint sUSD by staking SNX and assume exposure to fluctuations in the system’s debt pool. Under the old model, a high collateral ratio (up to 750%) combined with debt repayment incentives maintained sUSD stability. However, SIP-420 shifts from individual staking to a centralized debt pool, aiming to boost SNX staking appeal. While theoretically beneficial for long-term ecosystem growth, this transition disrupts existing equilibrium. Warwick acknowledged that the new mechanism is not yet fully mature, and the previous peg-correction functionality has been temporarily suspended, leaving sUSD without a self-regulating mechanism.

Market reactions further amplified the depeg. Data from X shows users actively swapping sUSD for USDT or USDC on decentralized exchanges like Curve, with sell pressure rapidly draining liquidity pools. In Curve’s DAI-USDC-USDT-sUSD pool, for example, sUSD’s share spiked abnormally, signaling eroding confidence in its stability. With a market cap of only $25 million, sUSD inherently suffers from weak liquidity; any concentrated selling can trigger significant slippage, pushing prices further off-peg.

Protocol-level adjustments also introduced unintended consequences. Selling 90% of ETH and reallocating into SNX strengthens SNX’s dominance within the ecosystem but reduces asset diversification. ETH, as a widely accepted collateral asset, lent external credibility—its removal may weaken trust in sUSD. Meanwhile, SNX’s volatility increases systemic risk concentration. While this strategy might bolster confidence during SNX rallies, under ongoing depeg conditions, it clouds the recovery outlook.

Historical Comparison

This is not the first time sUSD has depegged. On May 16, 2024, sUSD dropped to $0.915 due to a whale dumping sUSD received from sBTC redemptions, suffering an 8.5% deviation. At the time, insufficient liquidity on Curve combined with MEV bot exploitation caused temporary price dislocation. Synthetix responded swiftly by adding ETH, BTC, and USDC as collateral and providing liquidity incentives on Velodrome and Curve, successfully re-pegging within 11 days. That incident was fundamentally an external shock; the core mechanism remained intact, enabling a clear and efficient recovery path.

In contrast, the 2025 depeg presents a starkly different profile. This crisis stems from internal mechanism changes via SIP-420—not a single external sell-off—making the problem significantly more complex. The 2024 event lasted 11 days with an 8.5% drop, whereas the current situation has exceeded 20 days with over 16% deviation, highlighting greater severity and persistence. Moreover, while the 2024 response relied on liquidity incentives and diversified collateral, the 2025 approach focuses on internal restructuring (e.g., selling ETH to buy SNX), whose short-term effectiveness remains unproven. This suggests past experience cannot be directly applied, and the recovery difficulty is far higher than before.

Feasibility Analysis: Is Now a Good Time to Buy the Dip?

With sUSD currently hovering around $0.84, is buying the dip and waiting for re-peg viable? The 2024 episode offers some insight. Back then, sUSD rebounded from $0.915 to $1, delivering ~9% returns within two weeks—the success hinged on rapid incentive deployment and the transient nature of the external shock. Today’s lower price ($0.84) implies higher potential return (~19%), but risks are also magnified.

Bullish factors should not be ignored. SNX’s 7.5% surge indicates market confidence in Synthetix hasn’t collapsed. The team’s proactive communication and plans like the “Debt Jubilee” offer hope for recovery. Given sUSD’s small $25M market cap, minimal capital could move prices if incentives are introduced. Yet risks remain substantial. The depeg has already stretched beyond 20 days with no clear end in sight. If new mechanism tuning is delayed, recovery could take months. Selling pressure persists, Curve pool imbalances may push prices lower, and fading user confidence could suppress demand.

For instance, investing $100,000 at $0.84 buys about 119,000 sUSD. If sUSD re-pegs to $1, profit would be $19,000—a 19% return. However, setting a stop-loss (e.g., $0.75) is advisable, along with close monitoring of official announcements. If Synthetix rolls out incentives similar to those in 2024, the odds of successful dip-buying increase dramatically. If prices stabilize and SNX continues rising, small-scale accumulation may be justified. Compared to the low-risk window in 2024, today’s opportunity offers higher rewards but demands greater tolerance for uncertainty.

Market Reaction and SNX Anomaly

Despite sUSD’s deep depeg, SNX surged 7.5% on April 9—an eye-catching divergence. Market optimism may stem from long-term expectations around SIP-420. If successfully implemented, the new mechanism could enhance SNX staking yields and ecosystem standing, boosting Synthetix’s competitiveness in DeFi. The “Debt Jubilee” debt forgiveness plan mentioned by Warwick may also instill investor confidence, suggesting legacy burdens will be cleared.

Community sentiment is polarized. On X, some users fear sUSD may enter a “death spiral,” questioning the rationale behind the mechanism shift. Others argue that given sUSD’s modest $25M market cap, its impact is limited, and SNX’s rally better reflects true market confidence. Analysts such as The Merkle News note that transition risks from SIP-420 were underestimated, yet SNX’s performance suggests Synthetix still holds turnaround potential.

Conclusion

From an industry perspective, sUSD’s depeg has limited broader implications. Its $25M market cap is negligible compared to giants like USDT or USDC, minimizing spillover effects across DeFi. However, internally, prolonged depegging risks undermining user trust. Continued outflows from liquidity pools could impair sUSD’s utility, weakening its role in synthetic asset trading.

In the short term, worsening depeg could trigger further selling, increasing downward pressure. But SNX’s resilience buys the protocol valuable time. If the new mechanism stabilizes within weeks and is paired with debt relief measures, sUSD still stands a chance of re-pegging. Long-term, Synthetix must learn from this crisis, refining its stablecoin design to avoid repeating such painful transitions. The success of its mechanism overhaul will determine whether it can maintain footing in the fiercely competitive DeFi landscape.

Unlike the exogenous shock of 2024, this crisis is endogenous, making recovery more convoluted. The Synthetix team must simultaneously optimize mechanisms and rebuild market confidence to navigate through. For investors, sUSD at $0.84 represents both risk exposure and potential opportunity. Whether to buy the dip or wait, closely tracking protocol developments will be essential. In this storm of depegging, Synthetix’s future trajectory warrants ongoing scrutiny.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News