Is the Martin Act targeting the crypto world?

TechFlow Selected TechFlow Selected

Is the Martin Act targeting the crypto world?

A truly valuable free market does not fear the sword of the law.

By Daii

Last week (March 24), Galaxy Digital agreed to pay $200 million to settle with law enforcement in order to end an investigation. In fact, this $200 million is a fine—a price paid to persuade the New York Attorney General to cease its inquiry.

I originally intended to dive deep this week into how Galaxy exploited Luna to pump and dump on their followers, because after reviewing documents from the New York Attorney General’s office, I found their investigation into Galaxy's coordinated "pump" and "dump" tactics to be extremely thorough.

Let me start with one detail: the documents meticulously describe how Mike Novogratz, CEO of Galaxy, used tattoos to artificially inflate interest in Luna.

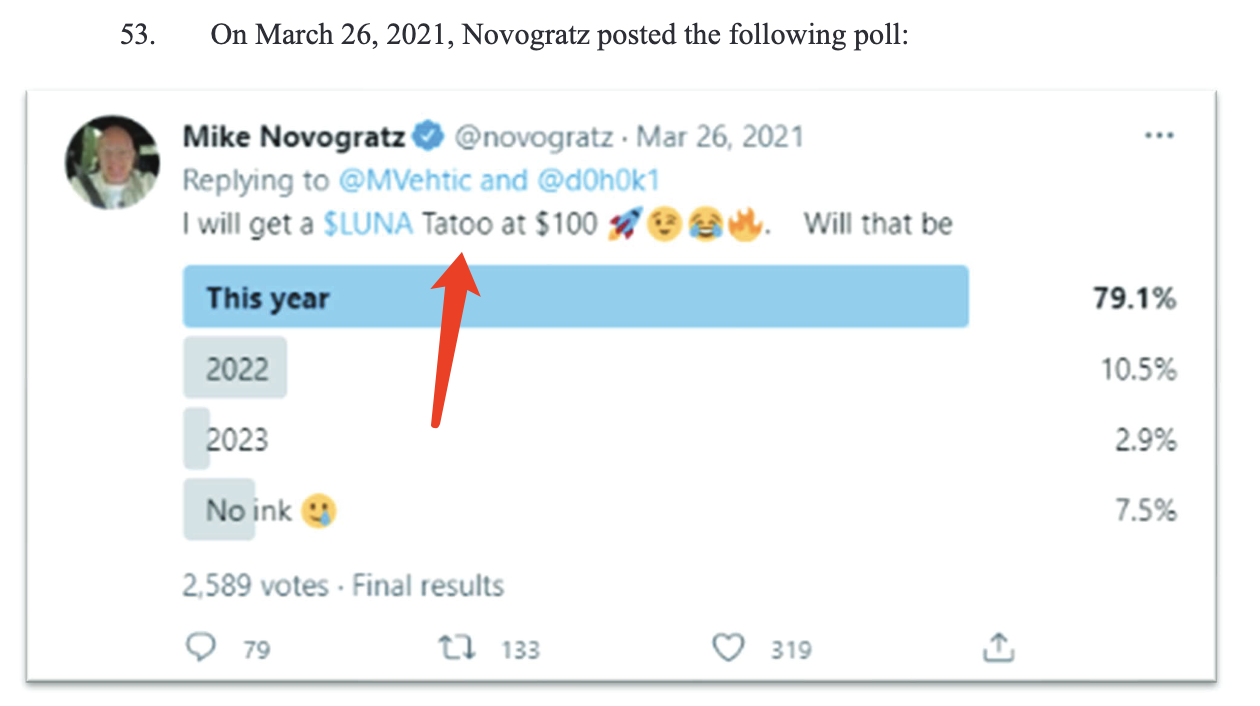

On March 26, 2021, Novogratz tweeted that if Luna reached $100, he would get a Luna tattoo (see image below).

On December 24, 2021, Novogratz tweeted again, claiming Luna had hit $100 and that he would commemorate the moment with a cool tattoo. He added he was still looking for design inspiration (see image below).

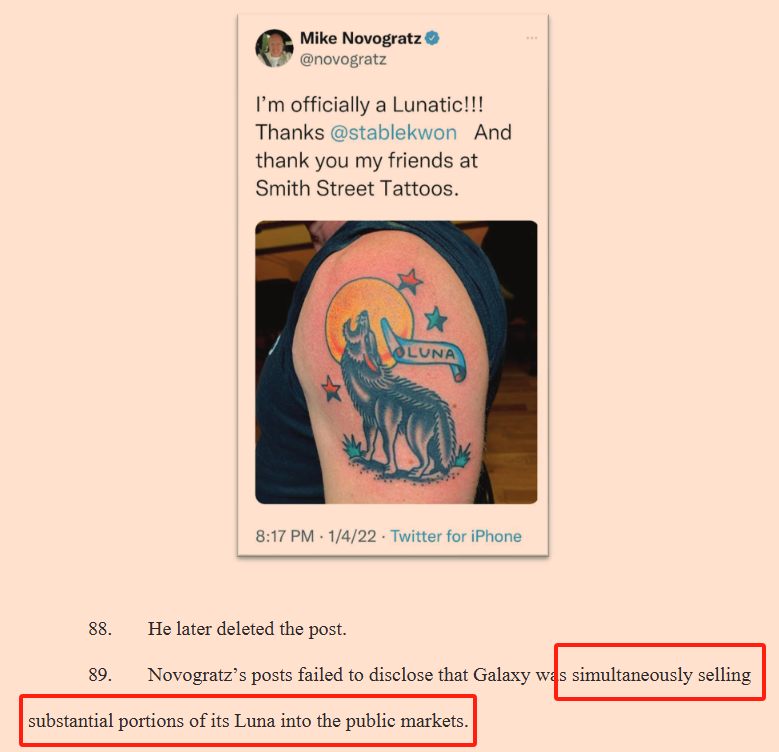

Shockingly, on January 4, 2022—on the very same day he sold 165,000 Luna tokens at an average price of $86—he posted the now-infamous tattoo image that sparked a frenzy (see image below).

Yet in his post, he said absolutely nothing about selling Luna.

What do you think? Isn't that shocking?!

To act so hypocritically is rare indeed—truly going to any lengths for profit. And there are even more egregious tactics we’ll explore later.

But today, we must first address a major question.

Is Galaxy really innocent? Did Novogratz actually deceive anyone?

You might find this question strange—and so do I—but given how many KOLs are passionately defending Novogratz, why are they doing so?

1. KOLs Rally to Defend Galaxy

Galaxy Digital’s decision to pay $200 million to halt the investigation exploded like a bomb within the crypto community, triggering strong backlash from numerous prominent KOLs. Many expressed emotional support for Novogratz on Twitter and podcasts, with some even calling the case a carefully orchestrated “judicial kidnapping.”

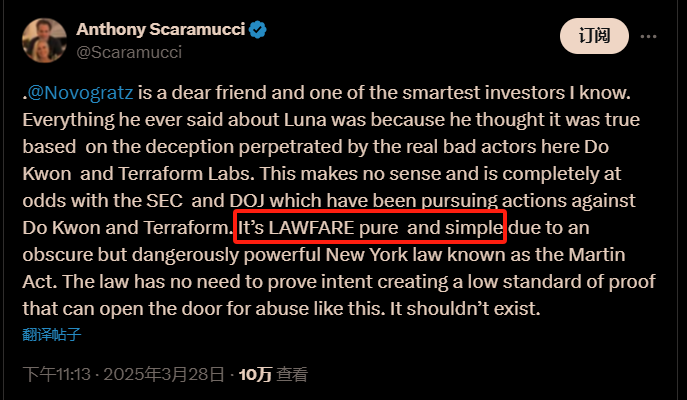

The most influential defense came from Anthony Scaramucci, founder of SkyBridge Capital.

Scaramucci is known for his blunt rhetoric. His defense even drew coverage from blockchain media outlets—the headline from Cointelegraph read: *“NAYG Lawsuit Against Galaxy Was ‘Lawfare, Pure and Simple’ — Scaramucci.”*

On March 28, he tweeted directly that the lawsuit was pure “LAWFARE,” naked judicial bullying!

He argued that New York State was using an overly broad law—the Martin Act—that allows companies to be forced into settlements without the prosecution needing to prove fraudulent intent. Sharp words, straight to the point. That single tweet gained thousands of likes and retweets overnight, rapidly spreading across the crypto community.

Evidently, all criticism centers on one thing: the Martin Act—a law that grants the Attorney General special powers to pursue cases without proving fraud intent, leading Galaxy to pay $200 million in what some call “extortion money.”

So, what exactly is the “Martin Act” that Scaramucci refers to?

2. The Martin Act

To understand why Galaxy Digital willingly paid $200 million in “settlement fees,” we must first examine the origins and nature of this so-called tool of “judicial overreach”—the Martin Act—as described by Scaramucci.

Enacted in 1921 and often called “Wall Street’s harshest weapon,” this law is now stirring controversy in the cryptocurrency world.

2.1 Why Is the Martin Act So Harsh?

The Martin Act, formally known as Article 23-A of the New York General Business Law, was among the first state laws in U.S. history specifically targeting fraud in securities and commodities markets. It grants the New York Attorney General (NYAG) broad investigative and prosecutorial authority over fraudulent activities related to securities or commodity transactions conducted in or from New York State.

It’s considered “harsh” due to two key differences from standard securities laws:

No Need to Prove Fraudulent Intent (Scienter)

In typical securities fraud cases, prosecutors must demonstrate that the defendant intentionally deceived investors. But under the Martin Act, the NYAG only needs to show that the defendant’s actions could mislead investors—even unintentional conduct can constitute a violation.

No Requirement to Prove Actual Financial Loss

In conventional fraud cases, victims must clearly prove they suffered tangible financial harm. Under the Martin Act, however, the NYAG can intervene immediately if there is potential for public misinformation—even if no actual economic damage has yet occurred.

In short, the Martin Act is highly preventive, giving regulators near-total initiative.

2.2 Why Was the Martin Act Created?

In the early 20th century, U.S. financial markets expanded rapidly, and securities fraud became rampant. Around 1920, states began passing so-called “Blue Sky Laws” to regulate securities offerings, and New York followed suit. After witnessing widespread investor losses due to false securities promotions, State Senator Louis Martin proposed the bill in 1921.

The legislative context was starkly practical: countless investors lost fortunes due to misleading claims, but proving intentional fraud was extremely difficult. Thus, the Martin Act lowered evidentiary thresholds, enabling the Attorney General to swiftly protect investors.

Initially aimed at obvious scams, it eventually evolved far beyond its original scope, becoming New York’s most powerful instrument for financial market oversight.

2.3 What Makes the Martin Act Special?

The strength of the Martin Act lies in three critical aspects:

Concentration of Enforcement Power in the Attorney General

The Martin Act does not grant private individuals the right to sue. Enforcement power rests solely with the New York Attorney General’s Office. Any investor seeking redress must file a complaint with the AG, who then decides whether to initiate investigations or lawsuits. This extreme concentration of power makes the law uniquely formidable.

Broad and Confidential Investigative Authority

The Attorney General may launch investigations proactively, without needing to establish reasonable suspicion. Investigations are strictly confidential; subpoenas can be issued to any party, and leaking investigation details can result in criminal charges.

Severe Penalties

Violators face massive fines, injunctions, and even criminal prosecution. Recent examples include Galaxy Digital’s $200 million penalty and the Trump Organization’s $450 million fine—both demonstrating the law’s formidable punitive reach.

Despite its power, the Martin Act lay dormant for decades until Eliot Spitzer became New York Attorney General in 2002, reviving this long-sleeping legal weapon.

3. The Martin Act Strikes Back

If laws have personalities, the Martin Act is undoubtedly aggressive and action-oriented. Though born a century ago, it wasn’t until the early 2000s that it truly flexed its muscle, shaking Wall Street with high-profile cases including Merrill Lynch, the Global Settlement with Ten Major Investment Banks, and the Trump Organization case.

3.1 The Merrill Lynch Case: The Fall of Wall Street’s “Big Short”

The case that first brought the Martin Act into the spotlight was the 2002 Merrill Lynch scandal—led by none other than newly appointed Attorney General Eliot Spitzer.

In early 2002, amid the aftermath of the dot-com crash, Spitzer targeted Merrill Lynch. He uncovered serious conflicts of interest involving analyst Henry Blodget, who publicly recommended tech stocks while privately labeling them “junk” and “worthless” in internal emails.

For example, Merrill publicly advised clients to buy Infospace stock, while Blodget privately wrote it was “garbage, absolutely untouchable.” Such contradictions were widespread, causing massive losses for retail investors.

Leveraging the Martin Act’s low burden of proof, Spitzer didn’t need to prove Blodget’s malicious intent—only that the statements misled the public. Unable to defend itself, Merrill Lynch settled by paying $100 million, pledged to decouple analyst compensation from investment banking revenue, and saw its reputation collapse. The case marked the moment Wall Street began fearing the Martin Act.

3.2 The Global Settlement with Wall Street’s Top Ten Investment Banks: A Trial That Shook Global Finance

Spitzer’s ambitions didn’t stop there. He next set his sights on Wall Street’s core: ten global financial giants including Goldman Sachs, Morgan Stanley, and Citigroup.

In 2003, Spitzer discovered systemic conflicts of interest across these banks’ research divisions. Analysts routinely inflated stock recommendations to win underwriting business—even promoting stocks they knew were fundamentally weak.

For instance, Morgan Stanley analyst Mary Meeker heavily promoted shares of Drugstore.com, prompting widespread retail buying. Yet internally, she admitted the company had poor prospects and was “not worth investing in.” When Spitzer’s team exposed this, public outrage erupted.

Using the Martin Act, Spitzer launched relentless investigations. Ultimately, the ten banks collectively settled in 2003 for a total of $1.4 billion.

Fines included $110 million from Goldman Sachs, another $200 million from Merrill Lynch, and $125 million from Morgan Stanley. Beyond penalties, banks agreed to enforce strict firewalls between research and investment banking to prevent future conflicts.

This case became known as “the largest and most impactful settlement in Wall Street history”—the peak demonstration of the Martin Act’s power. From then on, the separation between analyst incentives and banking interests became an inviolable line, leaving lasting trauma across the industry.

3.3 The Trump Organization Case: Even a Former President Can’t Escape the Martin Act

If the Merrill Lynch and Big Ten Bank cases showed the Martin Act’s power in finance, the Trump Organization case proved it could reach even the most politically sensitive figures.

In February 2024, New York Attorney General Letitia James invoked the Martin Act against former President Donald Trump’s business empire, accusing the Trump Organization of systematically inflating asset values for years to secure better loan terms and insurance rates.

Investigations revealed gross exaggerations—e.g., Trump Tower in Manhattan, realistically valued at around $500 million, was claimed to be worth over $2 billion when applying for loans. Dozens of such incidents misled banks and financial institutions.

Thanks to the Martin Act’s lack of requirement to prove subjective intent, the court quickly ruled the Trump Organization guilty of fraud, imposing a record $450 million fine. Trump and his family businesses also faced restrictions on conducting business in New York State.

Despite Trump’s vehement denials, the clear provisions and low evidentiary bar of the Martin Act left him no choice but to accept the judgment—an event that severely damaged his business empire and demonstrated the law’s cold, cutting edge to both political and business elites.

3.4 Summary: Side Effects and Controversies of the Martin Act

Through the Merrill Lynch, Big Ten Banks, and Trump Organization cases, it’s clear the Martin Act has become the New York Attorney General’s master key for maintaining financial order. Any improper conduct in securities or financial products occurring in or from New York risks falling under its reach.

However, such expansive power invites criticism. Financial professionals argue the Martin Act’s low threshold enables regulatory abuse, stifles innovation, and turns minor missteps into costly penalties.

Yet I believe: for the crypto market, the Martin Act is nothing short of a divine sword sent from heaven.

4. Why Is the Martin Act a Divine Sword?

Many may wonder: isn’t this sharp “legal blade” slashing at financial firms constantly, hindering innovation and harming markets? Some in the crypto space even view it as a tyrannical axe, ready to strike innocents at any moment.

But let me say this: for today’s crypto market, the existence of the Martin Act is precisely the long-overdue opportunity for normalization.

Why?

Simple: harsh laws for turbulent times.

4.1 Just How Chaotic Is the Crypto Market?

Even the most optimistic believers must admit the crypto market is absurdly chaotic. In just a few years, it has become a global epicenter of financial fraud, spawning countless shocking scams that seem to grow more brazen by the day.

Consider some data:

According to a March 2025 FTC report titled *New FTC Data Show a Big Jump in Reported Losses to Fraud to $12.5 Billion in 2024*, reported crypto scam losses reached $1.4 billion in 2024, with investment scams accounting for $5.7 billion—total fraud losses hitting $12.5 billion, showing an upward trend. Globally, Chainalysis’ *2024 Global Crypto Crime Report* estimates total crypto fraud reached $19 billion last year—an increase of 55% year-on-year.

Fraud techniques are diverse and ever-evolving:

First: Classic Rug Pulls

In early 2022, projects like Squid Game Token leveraged popular IPs to hype prices tens of thousands of times in days, drawing in vast sums from retail investors. Then, at peak value, developers instantly drained liquidity pools, fleeing with over $3.3 million. Investors watched helplessly as their holdings dropped to zero—in mere minutes.

Second: Market manipulation via Pump & Dump schemes.

Galaxy Digital’s involvement with Luna is a textbook case. Novogratz aggressively hyped Luna on social media as the “next king of stablecoins,” while quietly dumping his holdings—leaving retail investors holding the bag during a brutal crash. This tactic is widely used; CoinGecko data from 2023 shows over 60% of new cryptocurrencies crash within 90 days of launch, many showing clear signs of manipulation.

Third: Tech-wrapped Ponzi schemes.

The collapses of Terra/Luna and FTX stand out. Terra founder Do Kwon promised Anchor Protocol users 20% annual returns, attracting over $60 billion in a year. But those returns were classic Ponzi dynamics—new investors funding old ones. Once inflows slowed, the entire ecosystem collapsed, wiping out millions. FTX was even more surreal: Sam Bankman-Fried posed as a philanthropic prodigy while secretly funneling customer funds to Alameda Research for speculative bets—erasing $32 billion in market cap overnight.

Beyond these headline-grabbing collapses, retail investors constantly face phishing attacks, hacks, and insider trading. According to PeckShield’s Q1 2025 report *Crypto Hacks Top $1.6B in Q1 2025*, losses from platform breaches totaled $1.63 billion—up 131% from $706 million in Q1 2024—across more than 60 incidents.

Attack methods vary: private key theft, fake smart contracts, even self-theft by project teams (“exit scams”). The level of chaos is staggering.

While such hacking events fall outside the jurisdiction of the Martin Act and the NY Attorney General, we should recognize that these threats deter many from engaging with decentralized finance. Cyberattacks are unquestionably crimes—often organized, sometimes even state-sponsored. We’ll cover that separately another time.

4.2 Why Is the Crypto Market So Chaotic?

The disorder in crypto doesn’t arise in a vacuum—it stems from a complex interplay of institutional, technological, and cultural factors.

First: Regulatory Vacuum.

Over the past decade, the crypto market raced ahead faster than regulators could respond, creating fertile ground for scammers, speculators, and opportunists. For example, the SEC and CFTC have long debated how to classify Bitcoin, Ethereum, and altcoins, leaving the market in legal limbo. In late 2022, after FTX collapsed, Congressman Patrick McHenry lamented: our delayed regulatory response allowed scams like FTX to flourish.

Second: High technical barriers and severe information asymmetry.

Blockchain technology is inherently complex, making it hard for average users to distinguish truth from fiction. Meanwhile, projects and exchanges control nearly all critical data, operating with little transparency. In the Terra case, Anchor Protocol offered 20% APY, but its mechanics remained opaque. Retailers relied on celebrity endorsements and blindly followed the crowd—becoming the final bagholders. Right before FTX imploded, SBF still claimed “platform funds are ample,” yet users had no access to real reserve proofs. This “black box” model made fraud easy to execute.

Third: Massive moral hazard driven by profit motives.

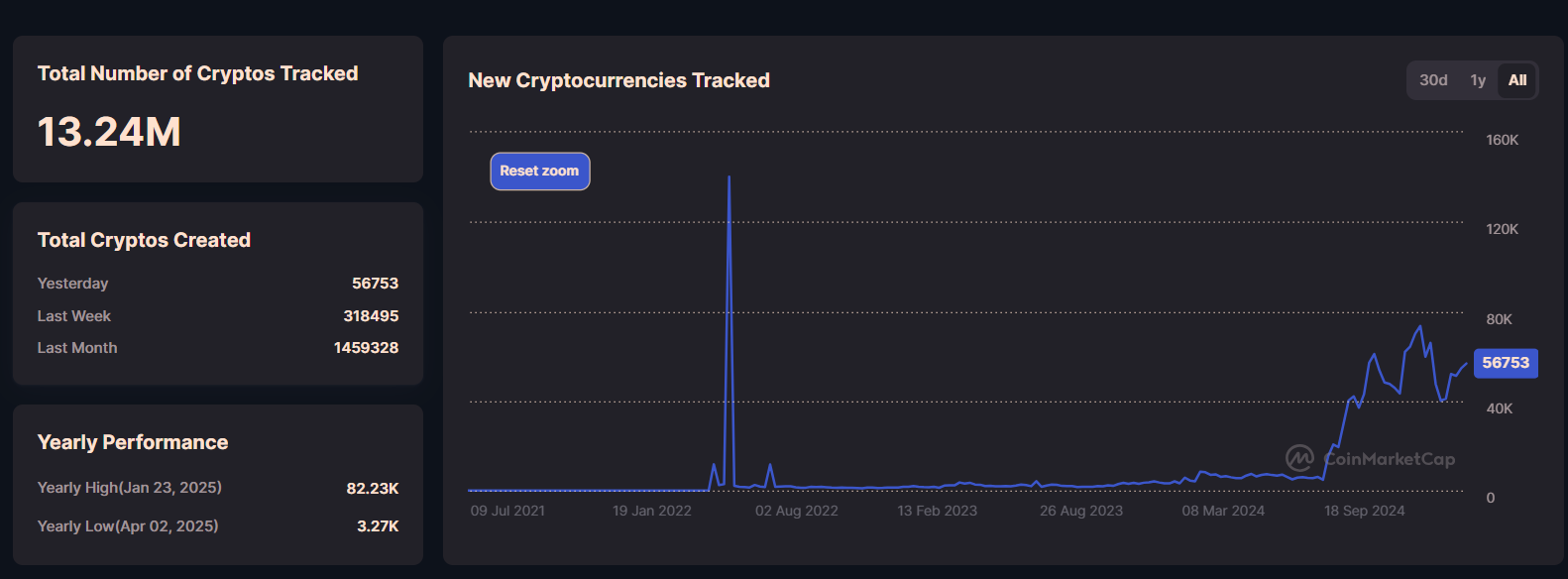

Liquidity in crypto is immense. Anyone can launch a token, list it on exchanges, and raise money instantly. As of April 2025, CoinMarketCap lists over 13 million cryptocurrencies—but fewer than 100 have real-world utility. The rest are essentially “air coins” or “trash coins.” Driven by wealth effects, projects, exchanges, and capital players often collude to manipulate markets.

Fourth: Amplification by media.

Mainstream and especially social media frequently promote new projects irresponsibly for clicks. Twitter, Reddit, Telegram groups overflow with paid shills and KOLs pumping assets—many openly manipulating markets. CoinDesk reported that in 2023 alone, false promotional content on social media caused over $1 billion in direct investor losses. Most ordinary users lack the tools to verify authenticity and easily become victims.

Fifth: Misuse of Decentralization Ideology.

Crypto’s anti-authoritarian ethos promotes decentralization to create fairer finance—but is often exploited by bad actors to evade regulation and accountability. DeFi platforms frequently hide behind “decentralization,” refusing to disclose team info or audits. When user funds are stolen, they often refuse compensation, claiming “users bear their own risk in a decentralized system.” This abuse worsens market chaos.

Sixth: Lack of self-regulation and internal oversight.

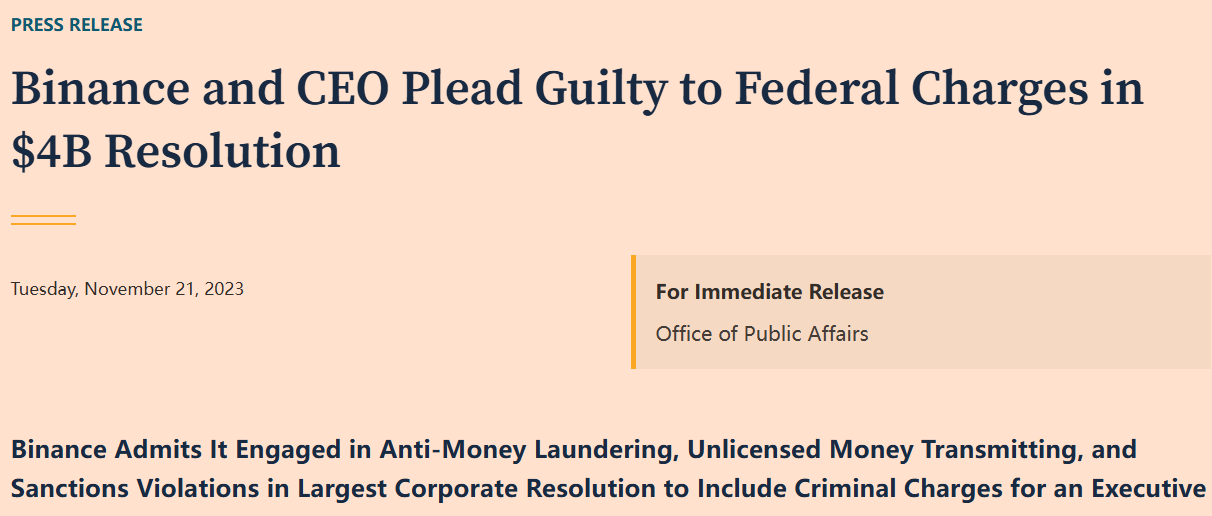

Traditional finance developed strict compliance cultures over decades. Crypto, in contrast, lacks such norms. Even top-tier exchanges like Binance and Coinbase have repeatedly been caught violating rules or engaging in insider trading. In November 2023, Binance and its CEO Changpeng Zhao admitted to anti-money laundering and sanctions violations, paying over $4 billion in fines (per DOJ announcement).

In summary, the root causes of crypto chaos are deeply intertwined: lagging regulation, information asymmetry, moral hazard, media amplification, ideological misuse, and lack of self-governance. These structural flaws have turned the market into a “Wild West,” offering perfect conditions for fraudsters and speculators.

And precisely in this context, the value of the Martin Act becomes evident.

4.3 Why Is the Martin Act a Powerful Sword?

They say, “History doesn’t repeat itself, but it rhymes.” Today’s crypto market mirrors the chaos of early 20th-century stock markets—this saying couldn’t be more fitting.

Turn back the clock to the early 1900s, when U.S. stock markets were in a “Wild West” era—just like today’s crypto space: full of opportunity, but inseparable from scams.

Back then, there was no SEC, no modern securities framework. Wall Street was a paradise for fraudsters. Market manipulation, insider trading, and false advertising were rampant. One notorious figure was “stock king” Jesse Livermore. In the 1920s, he used massive capital to spread rumors and collude with brokers to inflate stock prices before dumping at the peak. During the 1929 crash, he personally profited over $100 million (equivalent to tens of billions today), while tens of thousands of retail investors lost everything overnight.

At the time, like today’s crypto world, securities markets operated in a regulatory void. Companies issued stocks freely, without disclosing financials, audits, or accountability. Brokers manipulated markets freely; retail investors were lambs to the slaughter.

A famous example: in the early 20th century, Charles Ponzi ran the infamous Ponzi scheme, promising 50% monthly returns through international stamp arbitrage. In reality, he paid old investors with money from new ones. Within a year, he collected over $20 million (hundreds of millions today), then vanished—leaving investors ruined and markets in disarray.

Amid such chaos, states began enacting early securities regulations—“Blue Sky Laws.” The Martin Act was a landmark example, born in 1921 during New York’s most fraudulent period, designed to protect ordinary investors from securities scams.

The Martin Act’s severity quickly showed results. By strictly regulating issuers and brokers and punishing misleading statements, it helped New York curb rampant fraud in the 1920s–30s. Swift, harsh responses to emblematic cases—like fake oil companies and real estate scams—reduced fraud and restored market order.

In 1934, the federal government established the SEC and passed the Securities Exchange Act of 1934, incorporating lessons from Blue Sky Laws like the Martin Act to strengthen national oversight. Only under such strong regulation did U.S. securities markets evolve into the world’s most liquid, trustworthy financial system.

Today, crypto is undergoing a similarly wild growth phase: 56,000 new cryptocurrencies emerge daily, totaling 13.24 million. It brims with innovation, yet teems with risks and scams. Like Wall Street of old, today’s crypto market desperately needs a “harsh regulatory storm” to end its lawless expansion and transition toward healthy development.

Yes, the Martin Act may feel excessively harsh—with its low burden of proof and heavy penalties making many uncomfortable. But history teaches us: fair markets require strong legal deterrence. Only through strict punishment can order be restored and investor confidence rebuilt.

The current chaos in crypto mirrors the early days of stock markets. Learning from history, we should cherish this century-old sword—the Martin Act. Its role in shaping crypto outweighs temporary discomfort.

Conclusion

History never repeats, but it always rhymes. A century ago, the Martin Act emerged from a chaotic Wall Street. A century later, it is being summoned once again—to rescue today’s flood of crypto debris.

Some say, “Regulation kills innovation.” But history shows: “Innovation without regulation ultimately becomes a carnival for scammers.” Wall Street thrives not despite freedom, but because a sharp legal sword stands behind it.

In finance, without reverence, there is no safety; without regulation, there is no future. The Martin Act’s blade is sharp—but it cuts down fraud and greed, not innovation. Law never blocks true innovation; it only clears away the frauds disguised as innovation.

A truly free market fears no legal sword.

The Martin Act isn’t perfect—but in an uncontrolled crypto world, it remains a vital weapon to protect ordinary investors. Imperfect? Yes. But essential to hold tightly.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News