"Liberation Day" Countdown: How Will the Implementation of Tariffs on April 2 Affect the Market Outlook?

TechFlow Selected TechFlow Selected

"Liberation Day" Countdown: How Will the Implementation of Tariffs on April 2 Affect the Market Outlook?

The final direction of tariff policy will impact the future trajectory of global trade, the U.S. economy, and the cryptocurrency market.

Author: Luke, Mars Finance

Today is March 26, 2025, less than a week away from the highly anticipated "April 2 tariff implementation day." Dubbed "Liberation Day" by the Trump administration, this date carries grand ambitions to reshape America's trade landscape. Yet, as media speculation mounts, the script of this policy drama appears less radical than initially expected. Meanwhile, the crypto market—a sector acutely sensitive to macroeconomic tremors—is stirring under the shadow of looming tariffs.

A "Moderate Turn" on Tariff Day?

The latest reports suggest that the April 2 tariff measures may not fully realize the ambitious blueprint previously outlined by Commerce Secretary Lutnick. He had envisioned a "three-tiered stacked" tariff system: reciprocal tariffs as the base, supplemented by targeted hikes on specific industries and countries. However, recent rumors indicate potential retreats on the latter two components. It’s akin to an elaborately planned feast ultimately served as a simplified meal—fewer side dishes, but the main course remains.

Why this shift? The reasoning isn’t hard to discern. The Trump team understands tariffs are a double-edged sword. Since taking office, their trade policies have already triggered severe global market volatility: trillions in U.S. equity value erased, supply chain pressures inflating prices, even eggs becoming "luxury goods." Pushing tariffs to the extreme now could hit the U.S. economy first. Goldman Sachs economists warn that despite apparent calm, this "moderate posture" masks risks of "negative surprises." While market expectations price in around 9% for reciprocal tariffs, Goldman estimates the actual rate could double to 18%. That gap alone is enough to make traders hold their breath until the final announcement.

Meanwhile, the upcoming *Review Report on Unfair Trade Practices*, set for release on April 1, will serve as a critical indicator. This report will reveal U.S. scrutiny toward trade partners and directly influence the pace and intensity of future tariffs. If it highlights clear instances of certain nations "free-riding," Trump may seize the moment to escalate. If the tone is softer, markets might enjoy a brief respite. Either way, the report will act as a preview to the "Liberation Day" narrative.

Trump’s Calculus—Fairness, Fairness, Goddamn Fairness?

To understand the logic behind tariff implementation, consider recent statements from key members of Trump’s inner circle. In a recent appearance on the All-in Podcast, Treasury Secretary Bessent and Commerce Secretary Lutnick laid bare their thinking. Lutnick recalled history: between 1880 and 1913, the U.S. relied entirely on tariffs for federal revenue, with no income tax. After WWII, the U.S. voluntarily lowered tariffs to aid global reconstruction, while other nations maintained high barriers—making America the “most open” and, in his words, the biggest loser. For instance, American cars face 20% tariffs entering certain countries, while their vehicles enter the U.S. at just 5%. This asymmetry has infuriated Trump, who declared: “Fairness, fairness, and goddamn fairness!”

Trump’s goals are clear: protect domestic industries to bring manufacturing home, and generate fiscal revenue to plug a $2 trillion deficit hole. Lutnick proposed a “three-pronged strategy”: tariff revenue, sovereign fund investments, and the so-called “immigration gold card” program—reportedly selling 1,000 cards per day, with Trump optimistically projecting 1 million buyers. The other half of the deficit reduction would come from the “Department of Government Efficiency,” aiming to slash $1 trillion in wasteful spending by cutting 25% of the annual $6.5 trillion budget. Ambitious, yes—but execution promises peril at every step.

Treasury Secretary Bessent offered a broader macroeconomic diagnosis, identifying three core U.S. problems: soaring debt, runaway inflation, and manufacturing decline. His remedies include spending cuts, trade system overhaul, and middle-class revitalization. Unlike Lutnick’s aggressive stance, Bessent emphasizes “gradualism” to avoid triggering recession. White House economic advisor Stephen Miran added in a Bloomberg interview that as the world’s largest consumer market, the U.S. holds strong negotiating leverage to force concessions. This confidence stems from strength—but whether it translates into victory depends on how rivals respond.

Tariff outcomes could follow two paths:

First, opponents concede, lower their tariffs on U.S. goods, America wins, and U.S. stocks rally;

Second, retaliation ensues, forcing Trump to escalate—short-term mutual losses, pressure on U.S. equities. In the near term, the latter scenario seems more likely, as few players in global博弈 willingly back down first. But long-term, leveraging its consumer market clout, the U.S. may gradually correct trade imbalances.

The Fed’s Delayed Reaction and the Unfinished Bottom in U.S. Stocks

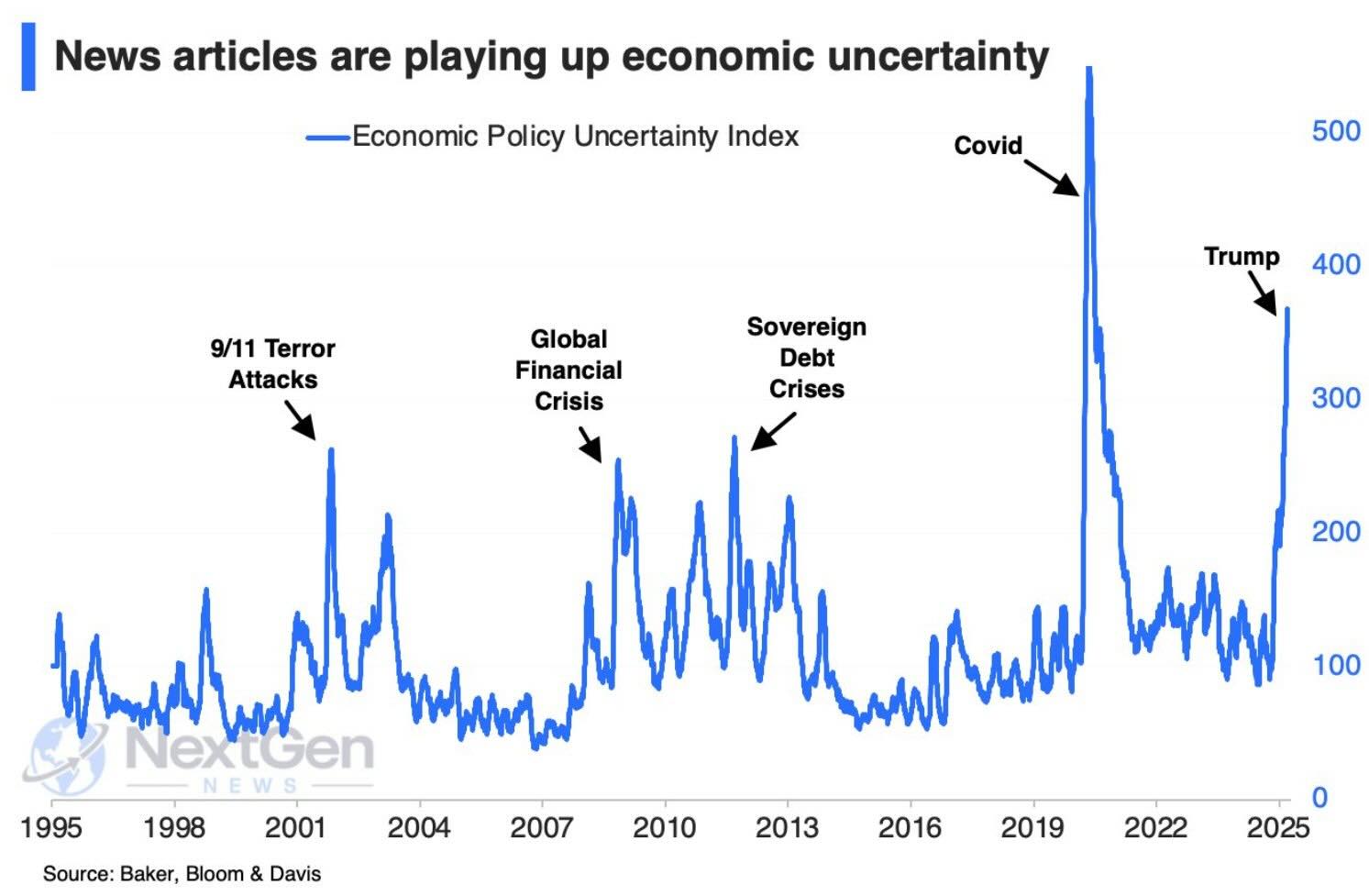

Tariff uncertainty doesn't just reshape trade—it transmits through inflation and monetary policy into capital markets. Recall 2020: pandemic-driven inflation caught the Federal Reserve off guard. Initially convinced inflation was “transitory,” by late 2021 Chair Powell had to admit error before Congress, dropping the “transitory” label and launching a steep rate-hiking cycle. According to Bloomberg data (see Chart 1), the U.S. Economic Policy Uncertainty Index spiked above 500 during the early pandemic—its highest level ever. Though it later dipped, events like the 2022 Russia-Ukraine conflict and the 2024 Trump tariff agenda pushed uncertainty back up. The index now hovers around 200, far exceeding the 1995–2019 average.

The Fed’s response to tariff impacts has also been sluggish. Over recent years, tariff-driven supply chain strain and price increases have significantly lifted inflation expectations, yet the Fed has leaned toward dovish messaging to soothe markets. But such reassurance only fuels short-lived equity rebounds—not sustained reversals. The root cause? The biggest market uncertainty—the direction and magnitude of tariff policy—remains unresolved. As shown in Chart 1, past spikes in economic policy uncertainty during events like 9/11, the Global Financial Crisis, and the Sovereign Debt Crisis all coincided with sharp U.S. equity drawdowns. Today’s elevated uncertainty suggests the stock market bottom may not yet be in. Markets may need either clarity on tariffs or a sharper macro shock to trigger full repricing.

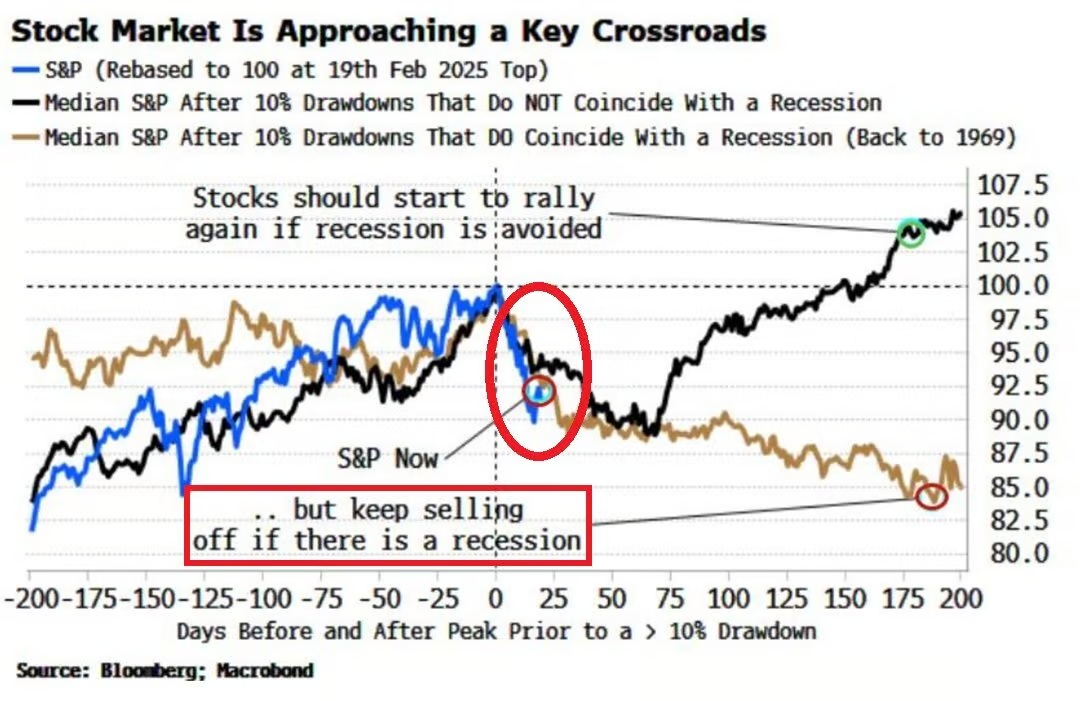

The S&P 500’s recent performance underscores these concerns. Per Bloomberg and MacroBond data, the S&P 500 has fallen 7.8% from its February peak, briefly dipping over 10% last week. Historical patterns show that if the index averages at least another 5% decline over the next five months, a U.S. recession becomes highly probable (yellow line, Chart 2). Conversely, if the S&P 500 recovers within the next 4–5 months, a downturn may be avoided (black line, Chart 2). Still, these are averages. Should a real recession hit, stocks could fall at least 20%. Notably, market sentiment can amplify moves: in 2022, the S&P 500 dropped over 20% without an official recession, as “expected recession” fears dominated market psychology in the second half.

Currently, the S&P 500 stands at a pivotal crossroads. Chart 2 suggests a quick rebound if recession is avoided; continued selling pressure if recession risks grow. Opaque tariff policy only heightens this uncertainty. If April 2 brings stronger-than-expected measures, market panic could push equities even lower.

Crypto Markets on Edge

When tariffs loom, crypto markets feel it first. Bitcoin recently climbed to $88,786, showing signs of recovery—but industry experts sound repeated alarms. CoinPanel trading expert Krytov calls this rally a “bull trap”: shrinking volume, retail hesitation, negative funding rates, and even “smart money” staying sidelined. The market is fragile—like thin ice, ready to crack at the slightest tremor. Aave’s stablecoin borrowing rates falling to 4% further confirm spreading risk-off sentiment.

More worrying is the “hold-to-sell-higher” mindset among long-term Bitcoin holders. These “veterans” await higher exit prices, unknowingly acting as latent sell-side deadweight. Krytov argues that only after these holders finally sell—and the market clears—can major players re-enter. Yet, signs of such a purge remain absent, casting doubt on the rally’s sustainability.

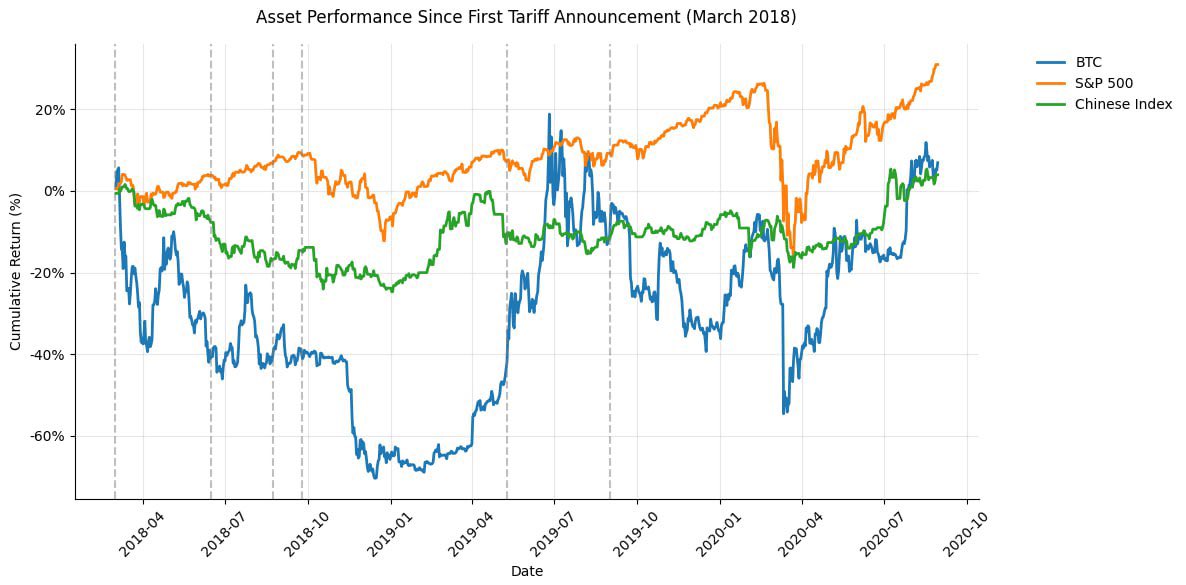

Historical data raises red flags. When Trump first launched his tariff war in 2018, global markets convulsed. As Chart 3 shows, from the March 2018 tariff announcement onward, the S&P 500 fell 12%, while Bitcoin plunged 65%—far outpacing traditional assets. Crypto’s “high risk, high return” nature reveals its flipside: steeper downside vulnerability. In contrast, Chinese indices remained relatively stable, declining less than 20%, highlighting differing sensitivities across markets to tariff shocks.

CoinDesk analysis deepens concern: Bitcoin has formed a “double top” pattern near $87,000. A break below the $86,000 “neckline” could signal a bearish reversal, potentially driving prices down to $75,000 in the short term. Altcoins would fare worse. SignalPlus partner Augustus Fan predicts a soft rebound may persist through month-end, but the April 2 tariff announcement will be the turning point. If policy is mild, Bitcoin could ride dovish Fed sentiment toward $90,000. If tariffs surprise to the upside, tightening liquidity may trigger a broad selloff.

Final Scenarios

How will April 2 unfold? Based on current signals, Trump may opt for a “moderate opening”: reciprocal tariffs set at 10–12%, with sector- and country-specific hikes postponed—preserving pressure options while avoiding economic hard landing. If the April 1 report supports escalation, a second wave could come mid-year. Short-term, markets may wobble from expectation gaps; long-term, if trade wars reshape economic structures, crypto could eventually benefit from recovery tailwinds.

For crypto investors, tariff day is more than a policy milestone—it’s a magnifying glass for market sentiment. Moderate measures might spark a short-term rally; harsher ones will test resilience. Regardless of outcome, this episode reminds us: the entanglement between macro policy and crypto grows ever tighter. Amid turbulence, only those who grasp the tides can truly sail forward.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News