Written in a Time of Market Downturn: Don't Stay Stagnant

TechFlow Selected TechFlow Selected

Written in a Time of Market Downturn: Don't Stay Stagnant

In an ever-evolving market, stagnation is death.

Author: Joel John and Siddharth

Translation: TechFlow

Hello!

A few days ago, I noticed a problem with how we write. Most of the time, our articles are technical topics written for founders and investors. That's fine. We skip drama, politics, and fraud, happily being nerds who spend weeks researching topics that can be read in minutes. But we're not in academia—we’re in the free market, investing and building alongside founders. So it’s crucial to stay close to what’s happening around us.

If I were to tell a therapist about my past six months in crypto, I’d summarize it like this:

A 13-year-old launched a meme coin and then dumped it. Scottie Pippen of the Chicago Bulls somehow predicted Bitcoin’s price after having a dream about Satoshi Nakamoto. Speaking of which, Jack Dorsey might be Satoshi. A Frenchman made $28 million betting on Trump winning. By the way, Trump launched a meme coin just days before taking office. Two weeks ago, Argentina’s president tried something similar, wiping out $4 billion in value. Now his opponents are trying to oust him. People lost money on Su Zhu’s exchange. Oh, and the Hawk Tuah girl launched a token—it was a rug. Dave Portnoy also launched a token—also “rugged.” CZ mentioned his dog Broccoli, and it looks like that one hasn’t been “rugged” yet—at least not yet.

Meme coins now have the power to topple presidents—an impressively far-reaching social effect.

It’s not like nothing good is happening in our industry. In October, the UAE clarified it won’t tax crypto. In the U.S., banks can now custody Bitcoin. Someone scammed an agent into transferring $25,000. Oh, and Marc Andreessen sent $50,000 to an agent, causing a token’s market cap to surge to $1 billion. There are rumors the U.S. government is building a strategic crypto reserve. OpenSea might finally launch a token to bail out NFT traders devastated in 2022. FalconX acquired Arbelos. Coinbase clarified the SEC has dropped all lawsuits against it. Last week, Bybit survived the largest hack in human history.

The point is, we’re a resilient bunch. But most of our collective psyche is tangled in bad news—price-driven, mixed with fraud and loads of embarrassment. You can’t help but wonder, “Am I really aligned with these clowns? Am I in a circus? Am I the monkey in this game?” It’s exhausting. Especially when you consider the human brain processes only 10 bytes per second while thinking.

How do I process everything amid this 4K ultra-HD live stream of fraud?

If you don’t consciously set boundaries, working in crypto is like throwing your brain cells into a vortex of headlines spinning at light speed until the sun’s heat vaporizes every cherished memory you’ve ever had.

A gradual descent into madness marked by liquidations and an endless, often meaningless, newsfeed. Like circling through Dante’s Inferno, jumping from one sin to another.

This is why, as a current affairs publication, we tend to keep distance from daily drama.

But given the state of the market and feedback we hear from founders, I think it’s time for a “vibe check” on the current cultural mood. Call it a response to the brief “vibecession” we’re experiencing.

“Memesis” Era

David Perell’s essay on Peter Thiel’s investment philosophy was one of the defining awakenings of my career.

One theme is “mimesis.” The concept, defined by René Girard, centers on humans’ tendency to imitate and compete with each other.

Think about the career choices you made at 17: you looked at what the smartest peers were doing or observed adults living lifestyles you admired, then followed their path. As humans, we naturally gravitate toward imitation and competition because forging new paths demands high cognitive load. We prefer the safety of crowds.

This applies to startups too.

Put enough smart people in a room, and you’ll see them imitating and competing with each other. Label an accelerator or venture fund (like Sequoia or YCombinator) as “elite,” and suddenly you’ll see a flock of bright minds rushing to join—not just for unlocked financial resources, but for the status it confers.

YC understands this well, hence claiming its acceptance rate is lower than Harvard’s. Status isn’t priced outright, but it’s deeply embedded. That’s why young, driven, ambitious twenty-somethings pack up and move to San Francisco, paying sky-high rents, hoping to climb the status ladder.

"Mimesis" drives us to strive to be the best in our field to satisfy our hunger for status

Image from Luke Burgis’s blog

At 15, I often wondered why so many Indian VCs shaped their worldview based solely on A16z partners’ tweets.

After ten years in venture capital, I realized they were simply mimicking the “big money.” If you can “copy” the best, why innovate? Is it an advantage? Not necessarily. But it makes money. That’s why we get waves of “me-too” products. Many mimic and iterate on a concept.

Facebook wasn’t the first social media platform. Instagram wasn’t the first media-sharing platform. Spotify certainly wasn’t the first service allowing users to stream music.

Repetition and iteration benefit consumers. Initially, markets become crowded, but over time, the market decides who survives. So you need multiple founders and VCs solving a problem, usually with similar solutions.

Keith Gill is the Soros of meme stocks. Murad is the Soros of meme coins. I’m trying to be the Soros of newsletters.

In liquid markets, this happens all the time. George Soros became famous for shorting the British pound and breaking the Bank of England. Keith Gill—aka “Roaring Kitty”—gained fame for igniting the GameStop frenzy. Both excelled at pulling most market participants into trades they were already in. Soros convinced traders to short the pound, pressuring the Bank of England. GameStop investors drove the stock price up until Robinhood stepped in to restrict short-selling.

What Roaring Kitty did is just a modern version of Soros’s “reflexivity theory”—both designed self-reinforcing loops. A big trade grabs attention, people follow, prices rise, more jump in, assets suddenly hit new highs.

In Soros’s time, there was no Twitter to endlessly hype things. In fact, he once left the market to study philosophy and write books. Today, you just post a meme coin leaderboard and pull people into the trade. What Soros called reflexivity is what we now call meme coin mania.

People often argue financial nihilism explains why ordinary people invest in meme coins. The idea is that this generation finds itself at 30 without stable careers, partners, or homes, so they bet on random code on Twitter, hoping to crack the financial system that bankrupted them (and keeps them bankrupt). But I think this argument doesn’t hold.

The real reason is “mimesis”—imitation.

Yes, the same force that determines your career choice, which startup YC funds, and how Keith Gill makes money, is also why you lose big on a pile of nonsense tokens named things like TrumpShibuInuWallDoesnotExistcoin.

Image from Murad’s tweet

Let me explain what happens when the internet breaks down barriers to entry into financial markets and information asymmetry.

Here’s how it typically unfolds:

You see a 17-year-old on TikTok or Instagram telling you about the “path to wealth” while sharing a meme coin they traded yesterday. A social media marketing manager at an office shows off a $150,000 NFT on LinkedIn. You watch your bills pile up and feel you’ve found another way out. A friend shares a ticker in a WhatsApp group. An exchange lists a new coin with a logo of a dog wearing a hat. You think, this is it. You put in $100, watch it grow to $117. You think, what if I put in $1,000? Or $10,000? Before you know it, your credit card is maxed out, and you’re deep in.

Note: Mentioning Murad here is out of respect for his massive influence on the meme coin market, not mockery. He defined today’s meme coin category, just as Keith Gill once defined meme stocks.

Pump It

Bitcoin’s emergence in 2009 completely transformed how capital operates online.

You could provide “labor” via Proof-of-Work (PoW—the thing securing the network) and earn Bitcoin as a reward. Since asset value would rise in the future due to demand and deflationary pressure, the future value of current labor increased.

This incentivized people to contribute computing power and hold Bitcoin. But with the rise of ICOs, token issuance became decoupled from proof of work—you could mint tokens without labor.

From March 2017 to 2018, ICOs raised about $28 billion.

Venture capitalists claimed this was the future of “finance,” enabling individuals to coordinate capital and resources to launch new networks. It sounded plausible—until you realized VCs often invested at low valuations (e.g., $10M) and then raised funds months later at much higher valuations (e.g., $100M).

This kind of madness happened in traditional VC during the dot-com bubble nearly two decades earlier. Crypto simply replayed it.

Between 2018 and 2023, the token issuance market matured. We no longer had ICO mania, but VCs still loved investing at low valuations and aiming for high IPO valuations. This is arbitrage.

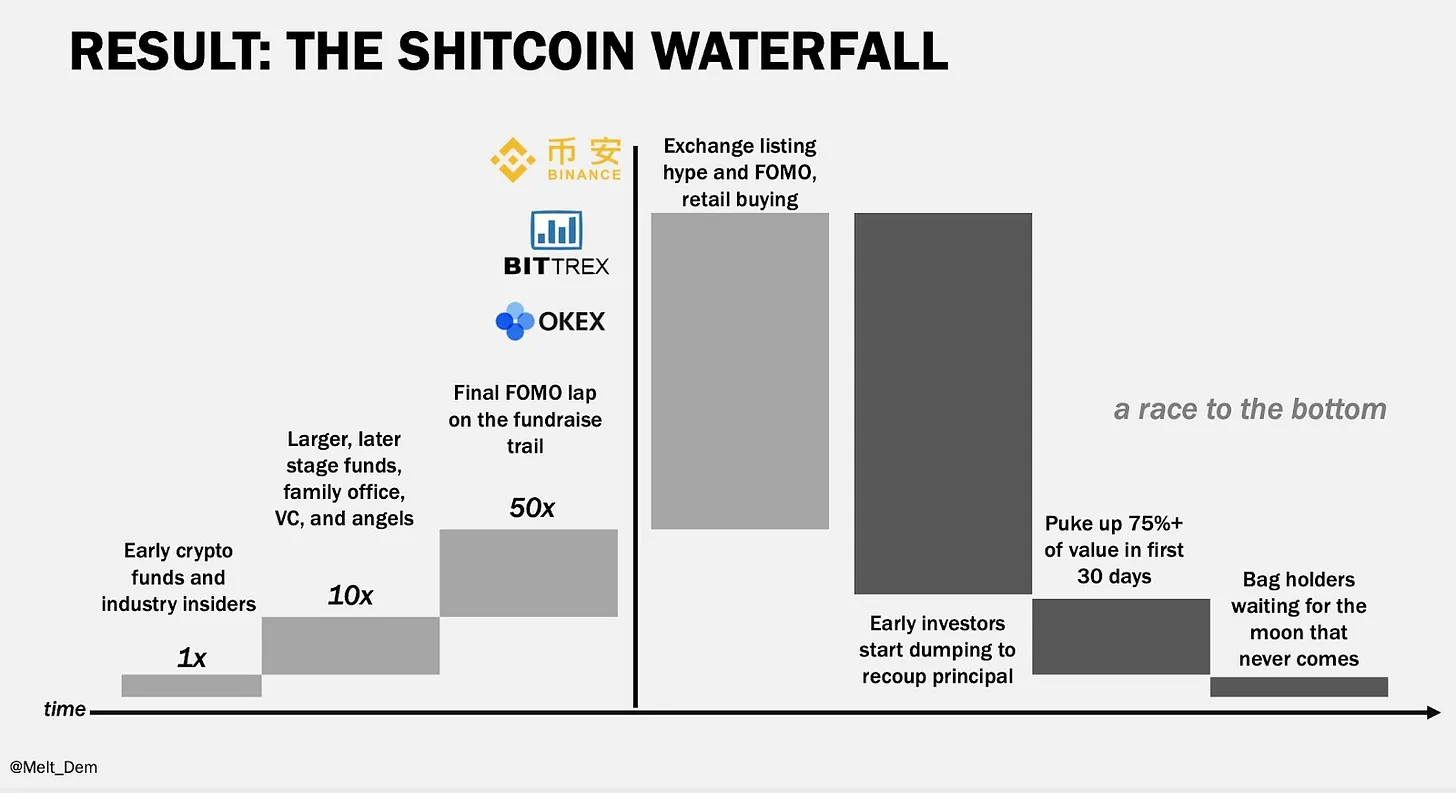

Image: Meltem Demirors’s video perfectly illustrates how capital allocation in crypto begins a free fall the moment a token launches

Investing at low valuations isn’t inherently wrong, but selling at a huge markup to retail investors without substantial progress is predatory. Chamath used a similar strategy during the 2020 COVID market with SPACs (Special Purpose Acquisition Companies). His SPACs have since averaged a 42% decline.

Now, anyone can use PumpFun to instantly become their own Chamath or VC fund. PumpFun is either one of the most innovative financial products of the century or the most predatory platform. The truth likely lies somewhere in between. Meme coins are to markets what pornography is to media. Just as porn won’t disappear, meme assets will persist as long as greed and speculation exist. And many memes will drive meaningful innovation, just as porn pushed technological progress.

While discussing morality is beyond this newsletter’s scope, I want to share two interesting numbers:

-

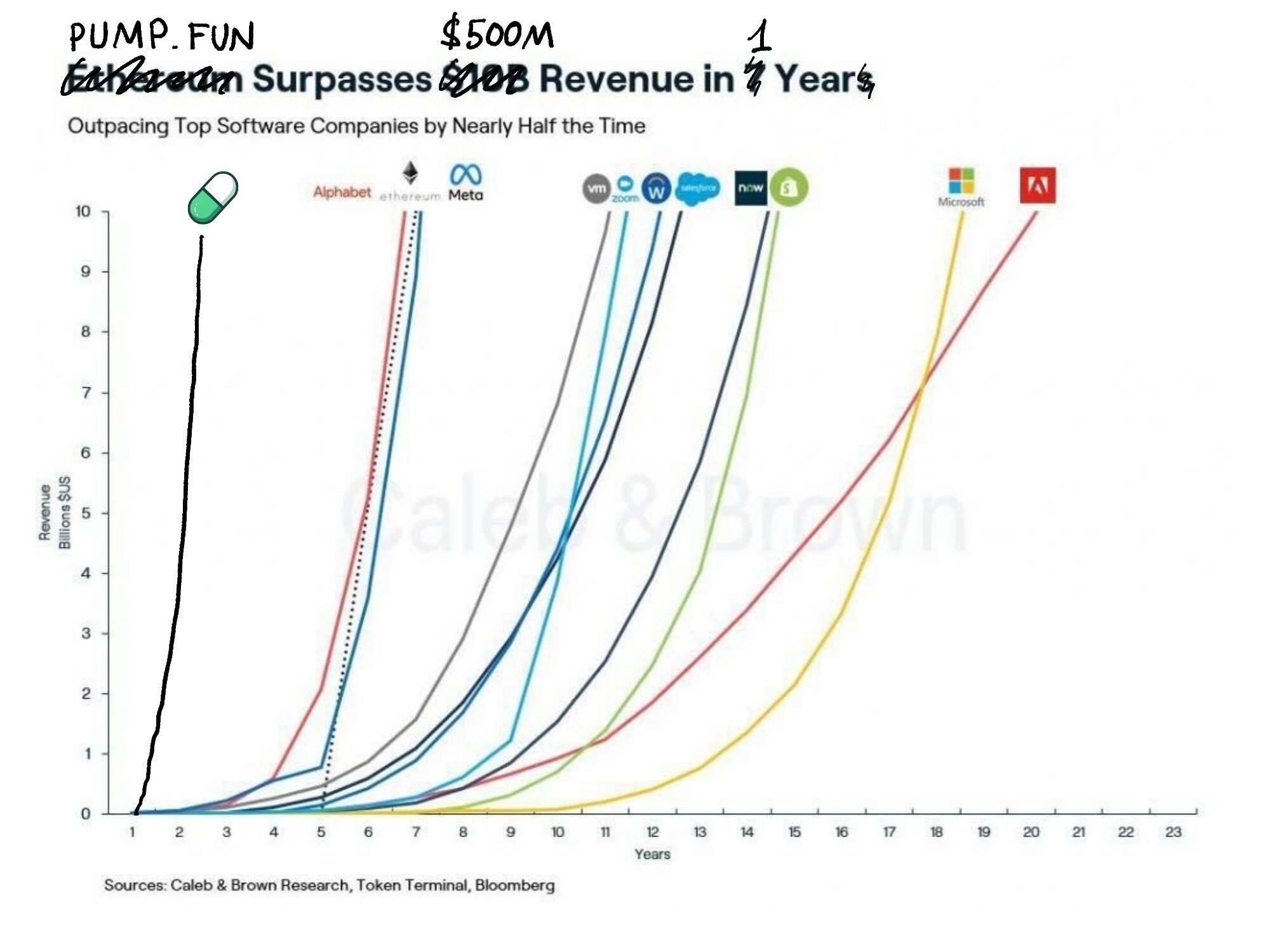

PumpFun’s cumulative revenue chart. They earned $500 million last year.

-

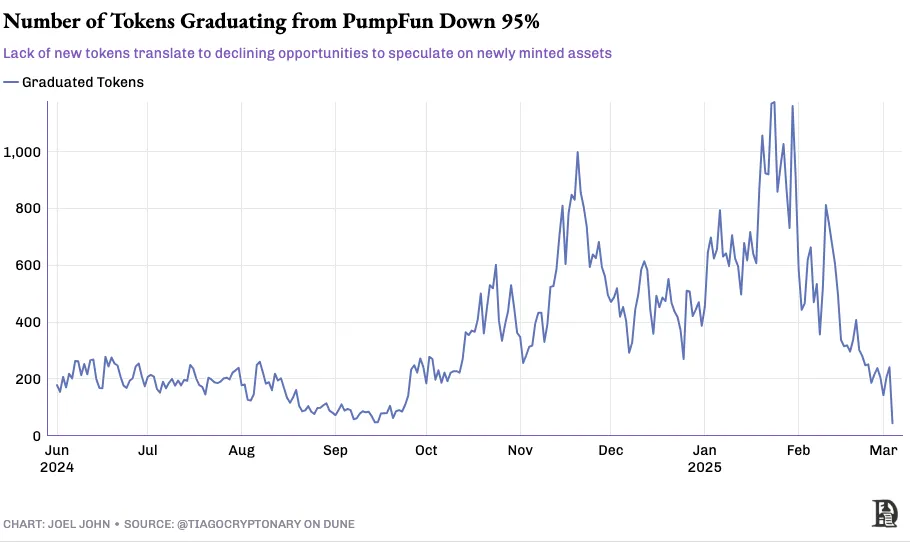

Another chart showing the number of new assets launched on Pump over recent months.

The second chart bears a striking resemblance to previous hype cycles.

I could overlay it with charts of ICO or NFT issuance—they look identical. I’m grappling with (or adjusting to) two parallel realities: one where PumpFun might be among the most profitable startups ever; the other where it starkly reveals crypto’s rawest mechanics. Dave Portnoy once tweeted, wondering aloud what a “rug” even means.

When we say blockchains can coordinate capital, we rarely clarify who that capital serves. It could fund cancer research or urban planning, but internet fringe dwellers often couldn’t care less. Everyone cares about profit and avoiding loss. We’re adults with bills to pay and dreams to chase. So everyone in the market bets on the most speculative plays, diverting capital and attention from truly important things. This is the market’s current state.

PumpFun’s real impact is turning crypto from a niche into a mass tool. When influencers, presidents, and nations issue tokens and watch prices crash, we’re not creating wealth through crypto as we did with Bitcoin in 2009—we’re destroying it. But just as individual expression on the internet can’t be defined by its creators, market outcomes can’t be dictated by tools. The creators of TCP/IP couldn’t decide what I write in this newsletter today.

This frenzy is the price of releasing the “genie from the bottle.”

Image: This chart is a joke inspired by a conversation with CK of ThirdPrime. I assure you, I have 0.0042 ETH in my cold wallet. I’m an “Ethereum guy.”

Without preparing to be offended, there’s no true free speech. Without providing tools for free markets, you can’t avoid most tools fueling greed and speculation. Especially in an era where regulators are “napping,” consequences for launching “rug pull” assets are minimal. Free speech works because saying the wrong thing has consequences. How does a consequence-free free market function? That’s the big question crypto is trying to answer. But as with most things, the market will eventually find its own solution.

The meme market resembles blogs and personal expression online in many ways.

Early on, blogging was niche. You could start one, but not everyone would read it. I love seeing old WordPress blogs online—they remind me of an era when people wrote to express themselves, not to influence. A few years ago, meme assets were like that. Doge was special precisely because its creators didn’t launch it to be a “meme.” As meme asset tools evolved, everyone could launch a meme coin, just as everyone could create a Facebook page.

In social networks, attention eventually concentrates on a few creators.

In meme assets, capital will also eventually concentrate on a few key names. The challenge is that people lose money along the way.

Image: Wassielawyer’s tweet captures what many of us feel inside

So where do we go from here?

Are we, as Zoomers say, “screwed”? Is there light at the end of the tunnel? Do I need to switch industries? What should we do!?

If I didn’t admit I’ve mulled over these questions multiple times in the past two quarters, I’d be lying. Not because I’ve lost faith in crypto’s potential and future—but because of how attention is allocated. The only antidote I’ve found is grounding my reality in human interactions, not the noise on Twitter.

Whenever my feed fills with the latest scam, I talk to a founder in our portfolio—a mental massage to restore confidence. Perhaps this is the greatest privilege of working at Decentralised.co—we gain perspectives beyond the feed from founders.

So if I were to zoom out and ask what excites me, what will define the next decade, here’s how I’d lay it out: treat this as a blueprint.

Respect the Pump

You just heard ten minutes of me complaining about fraud and lack of substance in crypto. If you’re still here, buckle up—here comes a shot of optimism with logic behind it.

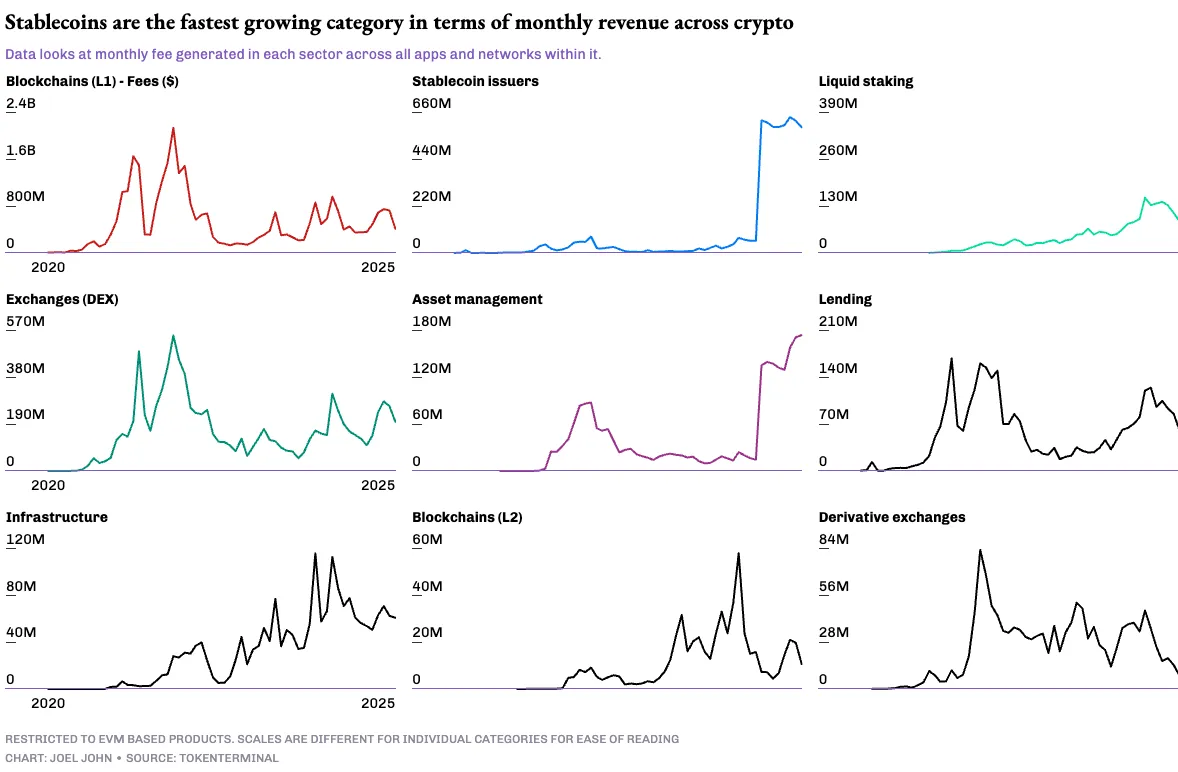

First, let’s look at applications that actually generate revenue, because that gives us direction on whether they’re worth our time. TokenTerminal doesn’t track all the apps we’d like to see—it leans slightly toward EVM (Ethereum Virtual Machine)—but it has the best data on price, revenue, and profitability. So I started my analysis by looking at the top ten revenue-generating categories.

The revenue figures below show monthly income each year over the past decade. The data is granular because we want to play skeptics. We want to see growth—because hey, what’s the point of staying in a stagnant industry? We want “hockey stick” growth.

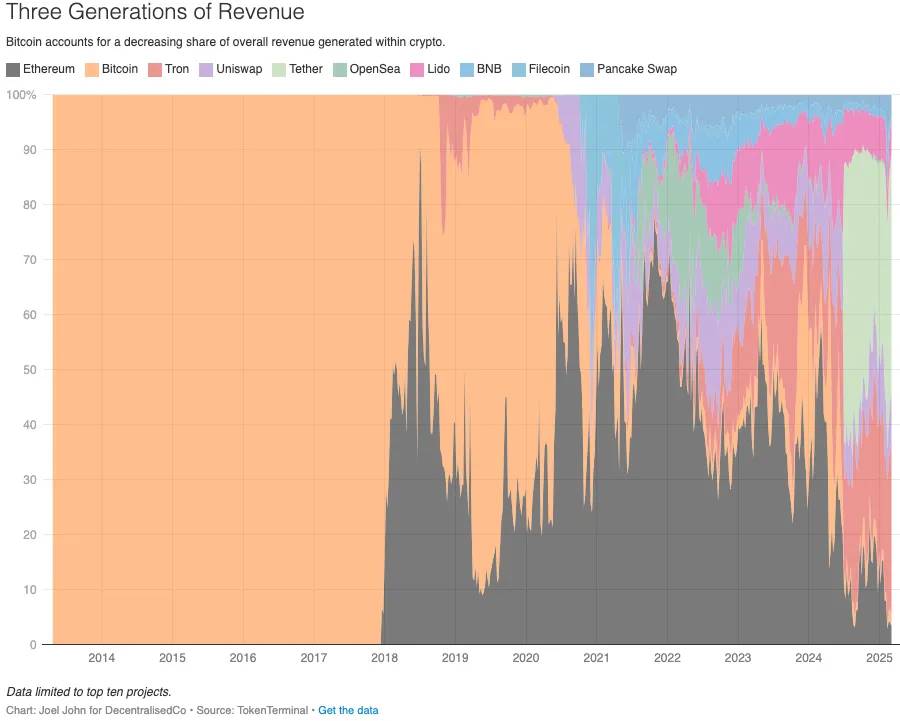

Looking at revenue, you’ll notice three phases of industry growth.

-

Phase one, which I call the “Dark Ages.”

Before Ethereum smart contracts took off. Before 2018, blockchain transaction fees were the industry’s primary economic output. Sure, you could count miner revenue and related businesses (like CoinDesk), but that didn’t apply to edge users. Developers didn’t directly benefit.

-

Then from 2018 to 2022, applications and use cases exploded.

Revenue was no longer limited to transaction fees but expanded to on-chain businesses. You can see “Blockchain Layer-1” fees gradually declining, making way for exchanges and lending. I call this crypto’s “Enlightenment Era”—a magical period when people questioned blockchain limits, defied Satoshi’s dogma, and created alternative business models.

It was during this “Enlightenment Era” that Play-to-Earn (Axie Infinity) and yield farming took off. Of course, some chapters ended in failure, like medieval European political alliances. But it paved the way for people to question possibilities and explore new paths.

-

After 2022, a new category rose at astonishing speed.

Guess what I call it? The “Industrial Era” of crypto. Just as humanity discovered the convenience of machine manufacturing and transportation, crypto practitioners discovered the possibility of scalable, automated revenue.

The “alchemy” of this era is stablecoins.

Everyone wants yield and fast capital movement. Fintech companies still rely on banks, and banks depend on governments to dictate capital flow rules. Stablecoins abstract away the regulations fintech firms historically faced, spawning a new generation of businesses. Tether and Circle earned over $5 billion in a year.

According to The Economist, stablecoin value transfers reached $2.76 trillion last year, about 2/5 of all blockchain transaction value (up from 1/5 in 2020). The same article noted that in March 2024, stablecoin transactions accounted for 4% of Turkey’s GDP. I won’t dive deeper here since this piece isn’t about stablecoins.

Now that we’ve established the industry can generate revenue at multi-billion dollar scales, the question becomes: how “sticky” is this revenue? Crypto revenue may be seasonal, but in scale, it can change lives. Think of OpenSea, PumpFun, or Play-to-Earn booms. Of course, some argue NFTs and meme assets created massive “bubbles” that ruined lives.

Whether the market is zero-sum is beyond this article’s scope (and I don’t want to plunge you into deeper existential crisis). But one way to think about it: revenue in these cycles is high enough to let companies earn what they’d normally make in a lifetime.

A useful mental model for blockchain-native apps is varying product maturity.

Depending on market cycles, speculative premiums increase. Take stablecoins—they’ve evolved to the point where large enterprises use them for remittances. That’s why Stripe made a $1 billion acquisition in this space last year.

On-chain analytics tools sold to governments (like Chainalysis) and smart contract auditing firms (like Quantstamp) have also reached mature revenue scales. These businesses have solid cash flows and sufficient margins to attract traditional capital.

Image: For reference only, not absolute. Much of this positioning is subjective.

If you layer these questions, you get a matrix. One axis is centralization vs. decentralization; the other is seasonality. Highly seasonal apps like FriendTech might be centralized but struggle to bring value to the ecosystem because they rarely pass value to edge users. Uniswap, while mostly decentralized, struggles to return value to shareholders. That’s why last year they introduced a fee switch on the frontend. Since then, Uniswap Labs has generated nearly $103 million in fees.

Corporate needs—revenue, margins, control over capital allocation—often conflict with our desires for decentralization and passing value to users.

A few companies have struck a balance—innovating and decentralizing while passing value to users and maintaining growth potential.

My personal favorite is Layer3.

If you haven’t heard of Layer3, think of it as an ad network aggregating one of crypto’s largest user bases. They help new users discover native crypto products and reward early adopters with dollars or crypto. So if you’re a new app or a newsletter like ours, instead of running ads on Google targeting uninterested eyeballs, you go to Layer3 to reach a curated group of crypto-native users. Unlike Google, Layer3 returns most generated value back to users as incentives.

In the past, I wrote about how they aggregate users. On average, about 60,000 users trade on their product daily. Last quarter alone, they returned ~$1.4 million to users. Annually, that totals $5.8 million.

In advertising, $5.8 million is trivial. Kanye West spent more on a Super Bowl ad. But the point is, this $5.8 million is interesting because it’s an early example of a product returning value to users. It’s an open ad network where consumers (early adopters) receive real dollar compensation through a global funding pipeline.

Anu of Working Theorys has a clever framework for zero-sum vs. positive-sum products. She notes some products reduce usage of others. For example, you use either Google Docs or Notion. Companies rarely switch between them because each suite has lock-in effects—you’d need to manually migrate the whole team. But some products are positive-sum—you can use Perplexity, Claude, and ChatGPT on the same day for different use cases. These don’t erode each other’s market share until user preference becomes clear, like Google vs. Bing.

Predatory products are often zero-sum because they leave (average) users worse off. Markets aren’t zero-sum if there’s underlying economic rationale. Someone who bought Tesla stock in 2018 profited from its rise without requiring someone else to lose. You could say stock moves correlate with Tesla’s output. But in meme markets, the game increasingly feels negative-sum.

The reason is simple:

Users need others to deploy capital for the asset to rise. That’s fair—all capital markets work this way. But users also need the “hype” to last long. From the start, you’re counting on the frenzy to continue. That’s okay because the “greater fool theory” gets people to buy assets. But as prices rise, people revalue their “net worth” based on thin liquidity pools. For example, a Congo-related token reaches a $1B FDV (fully diluted valuation) with less than $5M in trading pools. People “revalue” their net worth based on this illusory capital. When the game inevitably ends, they’re usually worse off.

Products like Layer3 are positive-sum because they don’t extract value directly from users. If you use their tools and stick around long enough, you can earn thousands just as an early adopter. As crypto crosses the chasm, we’ll see more products optimized for positive-sum dynamics—that’s how you build critical mass. The more users Layer3 has, the better deals the team can negotiate for them.

Marketers also prefer positive-sum games because they know users from Layer3 are more skilled and experienced—they’ve already used multiple relevant products.

One way to view crypto’s current revenue landscape is through what I call the “marginal adjacent user” lens. In emerging fields, founders are often best suited to solve niche problems. In the 1970s, Jobs and Wozniak built products for computer-literate enthusiasts who wanted portable, affordable home computers—niche, technical, expensive, and narrowly targeted. In contrast, 1990s Jobs obsessed over bringing tech to the masses—less technical, more general, price-sensitive, and extremely user-friendly.

If you built in crypto before 2021, targeting active on-chain users worked because revenue per customer was high. In a curious market, selling novelty works. But as users lost money and interest in subsequent years, expanding the market became essential. A few chains and apps (mainly on Solana) did well, capturing the next wave of on-chain users. The risk is these products may repeat 2019 DeFi—slightly faster, cheaper, better UX, but fundamentally doing the same thing.

According to Mary Meeker’s latest report, there are about 3 billion people online today. At the most optimistic estimate, crypto’s monthly transacting users range between 30–60 million. That’s generous. But consider: multiple products constantly fight for these users. Essentially, it’s “cannibalization”—market growth can’t sustain multiple players.

So teams compete on (i) pricing, (ii) incentives, or (iii) features—until margins collapse and they die—a literal “race to the bottom.”

What’s the alternative? Build things that go mainstream because mainstream markets offer both “moats” and margins. Our crypto “popularity contests” about who has the highest TPS (transactions per second) or who’s more “aligned” are useful for feeds but don’t pay bills. Layer3 appeals to me because they’re not chasing existing users—they’re expanding the market and capturing part of its value.

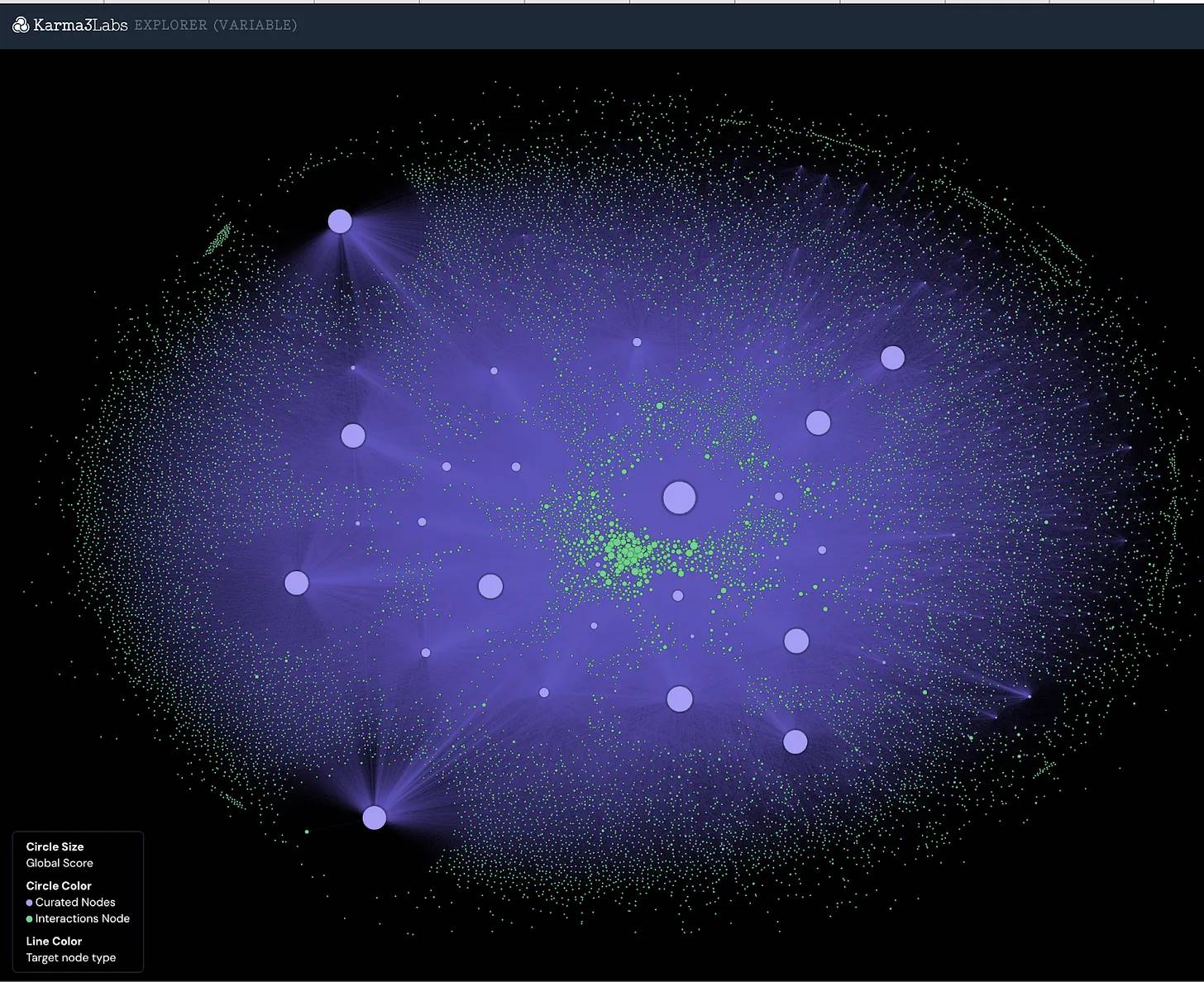

The theme of “expanding the market” isn’t limited to Layer3. OpenRank is a product built on Farcaster. Since Farcaster user activity is usually relayed on open networks (blockchain), it’s easy to assess which users are valuable and which communities are organic. OpenRank helps identify the right users and directly incentivize them with tokens, NFTs, or early access. This means any developer can target specific users on social networks.

Image: Karmalabs mapping Farcaster users in their filter

Layer3 and OpenRank represent two different approaches to advertising in the blockchain era.

One curates protocols, users, and incentives; the other lets the market identify users on open networks and target them directly. While it remains to be seen how Farcaster evolves or which ad model persists, one thing is certain: blockchain is changing how value transfers for content online. Sure, this market is niche now, but it has potential for exponential growth.

A personal example I’ve witnessed is stablecoins. In 2019, stablecoin market cap was around $1 billion—hard to imagine five years later it would reach $204 billion. But today, that’s exactly where it stands.

So the key question: can the market for crypto-related users grow similarly large? Can it reach hundreds of millions in five years? What would it take to build such a world?

We’ve already seen early signs in parts of the industry interacting directly with hardware networks.

For example, Frodobots and Proto use points or tokens (like USDC) to incentivize users to map geospatial data. Frodobots ships physical robots to users who ride them through towns, uploading data to create the world’s largest urban navigation dataset. Proto incentivizes users to map dense city networks using their phones. What attracts me to these models is their ability to capture data trustlessly (via device sensors) from third parties while incentivizing users with global capital networks.

UpRock uses crowds to provide data for website monitoring—a variation.

UpRock’s SaaS platform Prism offers an alternative uptime monitoring system with accuracy comparable to DePIN (Decentralized Physical Infrastructure Networks). Their network consists of nearly 2.7 million devices globally, forming UpRock’s backbone—the core consumer product powering Prism. When developers need insights, they can tap into UpRock’s user base—many earn rewards by collecting data via mobile and desktop apps. Could this work on fiat rails? Sure.

But try making millions of micro-payments daily across 190+ countries and see what happens. UpRock uses blockchain to accelerate payments and maintain a verifiable, public record of past payouts. They tie it together with their core token (UPT). At writing, the team burns UPT when earning external revenue via Prism.

This isn’t to say we’re on the brink of radical innovation that’ll make tokens “fly like Iron Man.”

No, we’re not there yet. The best example is agentic tokens, highlighting the gap between innovation and token performance. Let me start with a set of charts.

After the hype cycle, we can safely ask: is there anything valuable lurking beneath?

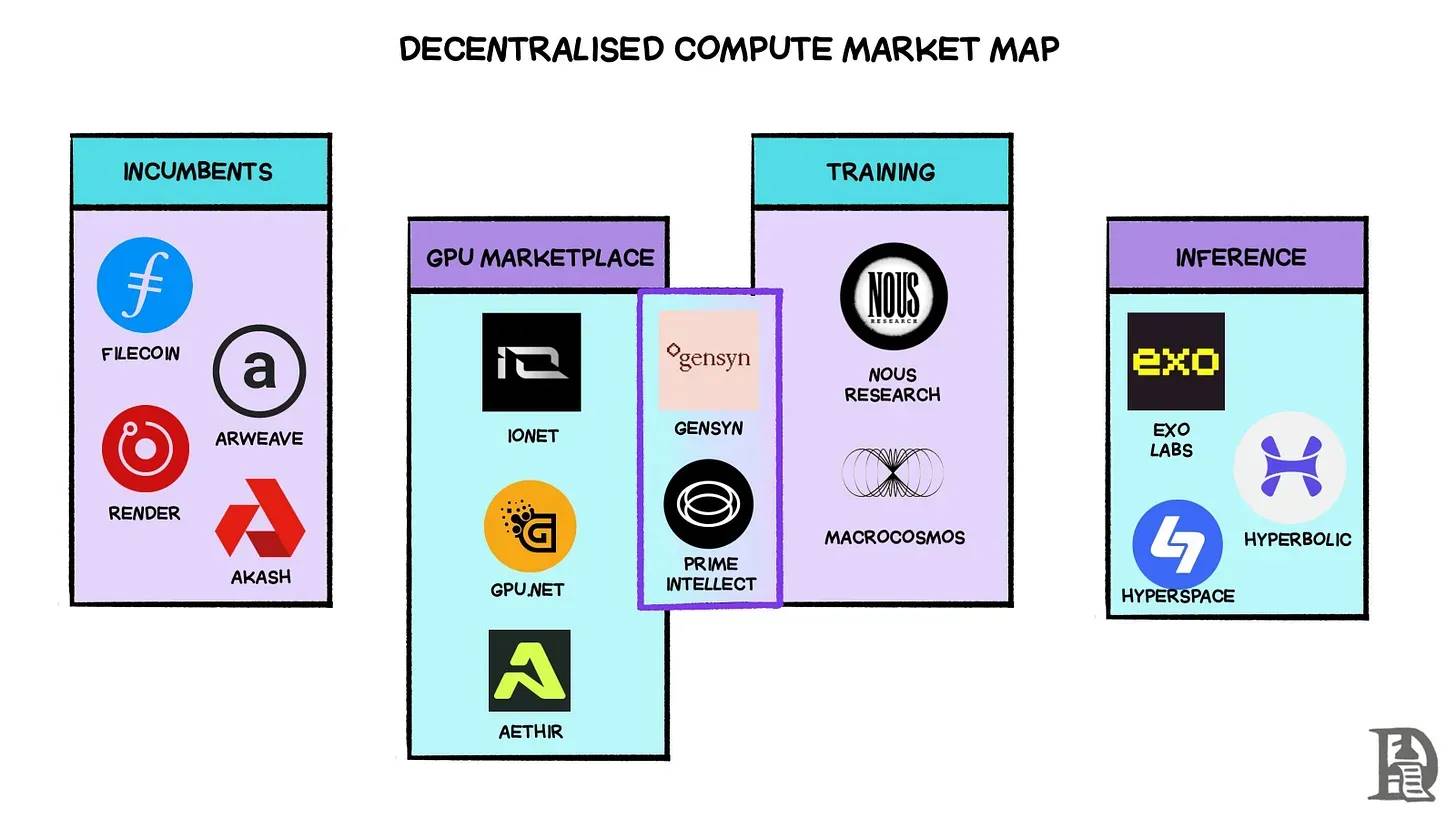

The most compelling intersection of crypto and AI isn’t agents themselves, but decentralized training and compute networks—using tokens to incentivize training and serving AI models across a global network of computers and GPUs.

You can see early iterations of this pattern at Pond’s Model Factory. They’re incentivizing creation of a machine-learning-capable model that simulates how judges rank open-source contributions.

So you can gather data (like UpRrock) or find people to build models (like Pond). But in a world where energy and compute are scarce, where do you run these models? Shlok explained this in a prior piece; I’ll quote him directly:

Who are these new AI-native markets? io.net is one of the early leaders in aggregating enterprise-grade GPU supply, with over 300,000 verified GPUs on its network. They claim 90% cost savings versus centralized incumbents and earn over $25,000 daily ($9M annualized). Similarly, Aethir aggregates over 40,000 GPUs (including 4,000+ H100s) to serve AI and cloud computing use cases. Previously, we discussed how Prime Intellect created a large-scale decentralized training framework. Beyond those efforts, they also offer a GPU marketplace where users can rent H100s on demand. Gensyn is another project heavily betting on decentralized training, adopting a similar training framework and GPU marketplace approach.

In short, crypto has evolved to the point where we can source data, find people to build models, fine-tune them, and mobilize the physical infrastructure needed to run AI models. Meanwhile, the average crypto person is still asking “when moon?”—completely unaware they’re sitting on a pile of “uranium” that could take us much further. Some developers get it. Teams like Gud.Tech and Nomy are building trading agents that accept user input, understand context, and execute transactions.

What does this mean?

Chatbots have existed since at least 2015. Getting information from bots isn’t novel. What draws me to Gud and Nomy is how they abstract the complexity of cross-chain asset purchases. Nomy offers a simple chat box: type “buy 50 po with my eth on base,” and the agent executes the trade automatically, no multiple signatures needed. Similarly, Gud is building a trading product that almost always delivers the best price by optimizing liquidity sources. These products blur the line between consuming information (Twitter, newsletters) and executing transactions—all powered by advances in AI.

Why do I highlight these two teams specifically? Because they embody everything we’ve discussed so far.

-

They target crypto-affiliated users, not fighting over the same small user pool.

-

They’re not zero-sum because their growth depends on sustained user engagement.

-

They package critical infrastructure (like gasless transactions) into a single usable product.

-

They build at the frontier of crypto and AI in ways relatable to average internet users.

I emphasize Gud and Nomy because they’re built by teams who深耕 infrastructure before moving to the application layer. This reveals a simple truth: the application era has arrived. If cash flow, revenue, moats, and user retention truly matter, applications will carry that torch. Infrastructure has matured to the point where arguing over TPS is no longer meaningful. Our refusal to abandon these heuristics is just another sign of stagnation.

To evolve, we need to change the conversation. Maybe even develop a shared language of optimism.

Cathedrals, Not Trenches

In the mid-1940s, as WWII threats faded, aviation faced a new challenge—building aircraft that mimicked birds, specifically pigeons (by the way, this comes from Where Is My Flying Car, a great book). The goal was planes that could land in backyards without long runways. Despite massive improvements in efficiency regarding passenger capacity and fuel economy, we still don’t have retail-owned flying cars.

Does this mean aviation failed? No. In 1961, John F. Kennedy said:

We choose to go to the moon. We choose to go to the moon in this decade and do the other things, not because they are easy, but because they are hard, because that goal will organize and measure the best of our energies and skills, because that challenge is one that we are willing to accept, one we are unwilling to postpone, one we intend to win, and the others, too.

Fueled by this optimism, decades of U.S. investment and effort during the Cold War laid the foundation for today’s Silicon Valley. More intriguingly, in 1903, the media openly argued we wouldn’t have flying machines for another million years. A million years!? Sounds like they expected evolution to help us. But we didn’t wait blindly.

We made it happen. In 1969, we landed on the moon.

But between 1903 and 1969, flight attempts failed repeatedly. Crypto feels much like that—we’re too focused on perfecting the “engine” rather than actually serving “passenger transport.” Kennedy’s political will injected new energy and direction into aviation—mobilizing people, resources, and policy toward a mission. This wasn’t a one-off event, but a pattern.

In David Perell’s essay on Peter Thiel, he highlights how medieval Europe united during destructive, dangerous times to build cathedrals. These structures were symbols of hope, taking centuries and immense resources to build. They required coordination of finance, security, talent, and labor—far beyond everyday efforts.

An ordinary worker building a cathedral might only hope to see its completion in their lifetime. Today, similar acts involve spending 4–5 years scaling a consumer app while most of the industry obsesses over technical details.

Today, through meme coins, we see humans struggling to figure out how to use money when asset issuance and trading move as fast as text messages. We’ve been here before. In the 1400s, we adapted to how interest rates affect capital. In the 1700s, we discovered the power—and chaos—of trading company shares. The South Sea Bubble was so severe that the 1720 “Bubble Act” banned creating joint-stock companies without royal charter.

Bubbles are a feature, even a necessity. Economists view them negatively, but bubbles are how capital markets identify and evolve into new structures. Most bubbles begin with surges of energy, attention, and obsession in emerging fields. This excitement pushes capital into anything investable, inflating prices. Recently, I’ve seen this obsession around agent projects. Without the combination of financial incentives (token prices) and hype, we wouldn’t have so many developers exploring this space.

We call them “bubbles” because they burst. But price declines aren’t the only outcome. Bubbles drive radical innovation. Amazon didn’t become “useless” in 2004—it laid the foundation for AWS, which powers the modern web. Could 1998 investors foresee Jeff Bezos succeeding? Probably not. That’s the second aspect of bubbles—they create enough experimental variants to eventually produce a winner.

But how do we conduct enough experiments to witness a winner?

That’s why we need to focus on building “cathedrals” instead of dancing in “trenches.” My argument is that meme assets themselves aren’t bad. They’re excellent testbeds for financial innovation. But they’re not the long-term, revenue-generating, PMF-seeking game we should play. They’re test tubes, not labs. To build our “cathedrals,” we need a new language.

We’re already seeing early versions of this new language in projects like Kaito and Hype. I don’t hold their tokens, but they’ve become category leaders in their own right. Their token prices have also found stable footing, unlike many VC-backed “star projects” that delivered nothing after 36-month lockups. As people realize crypto’s core meta-game has evolved, more will rally around this new language.

Image: To end stagnation, one must confront the “monster” within

In 2023, when I wrote Has Crypto Failed?, I believed we’d move toward a market where founders and VCs recognize the importance of revenue and PMF. That was my PTSD after FTX, wishing for rational participants. In 2025, I fully realize that’s no longer realistic—hope is no longer a strategy.

Next, highly agentic individuals will create a parallel game, building their own “cathedrals.” They won’t chase fame on crypto Twitter but listen to and build for internet edge users. They’ll earn real product revenue, not depend on exchanges’ “blessings.” The driving force behind this shift is the crisis of faith I mentioned at the start.

People will start asking: “Why am I here?” and then change the game they’re playing.

The split between revenue-generating and non-revenue-generating tools will be crypto’s great divide. Eventually, we won’t talk about “working in crypto,” just as no one says “I work on the internet” or “I work on mobile apps” today. They’ll talk about what the product does. That’s the language we should use more often.

When I started writing this, I tried to pinpoint what truly troubled me. Fraud? Meme assets? Not quite. I think the real pain comes from recognizing the gap between effort and impact in crypto—especially compared to AI. Sure, we have stablecoins, but so many other innovations go unnoticed or unmentioned. That’s what makes me feel stagnant.

In an evolving market, stagnation is death.

If you stagnate, you die. But if you end stagnation, you survive. That’s the irony behind “ending stagnation”—to preserve life, you must be willing to end core internal parts. That’s the price of evolution, the price of staying relevant. Crypto stands at that crossroads. It must choose to end parts of itself so those capable of evolving and dominating can grow beyond infancy.

Respect the cathedral,

This piece was heavily inspired by Boom and the End of Stagnation. If you haven’t read it, I absolutely urge you to.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News