Centralized USDT has no future—what lies ahead for stablecoins?

TechFlow Selected TechFlow Selected

Centralized USDT has no future—what lies ahead for stablecoins?

Can stablecoins, an important Web3 application, become even more Web3-native?

Author: Liu Honglin

Blockchain, as an umbrella term originating from Bitcoin, inherently carries strong financial attributes and a spirit of libertarianism. Yet, due to regulatory pressures, most Web3 projects strive to prove that their tokens are utility tokens rather than security tokens—to avoid scrutiny from mainstream regulators.

But not all projects face the same struggles. In the world of Web3, there exists another type of token that desperately wants users to treat it like money: stablecoins. As mediums of payment, their biggest challenge is stability (Russia's ruble raises its hand…)

The narrative behind stablecoins is simple: for every dollar held in a bank account, one issues a corresponding coin on the blockchain. The focus is purely on emotional and price stability. In many ways, stablecoins bridge the stability of traditional currencies with the decentralized advantages of blockchain technology, serving as a vital link between the real world and the on-chain economy—and becoming among the first mass-scale applications bringing blockchain to everyday people.

Yet as USDT and other centralized stablecoins have come to dominate the market, we've suddenly realized: the dragon slayer has become the dragon.

Tether, issuer of USDT and a central hub in global Web3 infrastructure, controls over 65% of the global stablecoin market. It earns tens of millions of dollars annually from its stablecoin operations. Yet, paradoxically, it operates as one of the most traditional, centralized Web2-style companies.

USDT’s issuance and freezing mechanisms rely entirely on a single centralized entity. Its transparency is low, profits are largely disconnected from users, and governance power is highly concentrated. These traits might be acceptable in a conventional internet company—but for a cornerstone firm in the Web3 ecosystem, they’re deeply problematic. Because this isn’t Web3 at all!

Recall that core tenets of Web3 include openness, transparency, trustlessness, and value sharing. These principles seem entirely absent in Tether, a centralized stablecoin operator.

So here arises a critical question: Can we make stablecoins—this pivotal Web3 application—more aligned with Web3 ideals? Perhaps this alignment will define the next generation of stablecoin innovation.

In this article, Attorney Honglin shares insights into a project he’s recently studied, exploring how decentralization can be meaningfully integrated with stablecoin design. As always, this piece is for educational purposes only and does not constitute investment advice.

Project Overview: Usual

Usual is a decentralized fiat-backed stablecoin issuance platform aiming to break down barriers between traditional finance (TradFi) and decentralized finance (DeFi), bridging the two ecosystems.

Usual centers around three core products:

-

Common Stablecoin: Designed for payments, trading, and collateral use.

-

Usual LST (Liquid Staking Token): A yield-generating product.

-

Usual Governance Token: Grants holders decision-making rights within the protocol.

Usual aggregates tokenized real-world assets (RWA) from reputable institutions such as BlackRock, Ondo, Mountain Protocol, M0, and Hashnote. It transforms these into permissionless, on-chain verifiable, composable stablecoins—enhancing liquidity for traditionally illiquid assets and making them more accessible to a broader range of investors.

More importantly, through the $USUAL token, ownership and governance rights are redistributed, enabling community members to become owners of the platform’s infrastructure, funds, and governance. This drives deeper integration between Web3 and the real world. With Usual’s architecture, stablecoin issuance becomes not just digitization of assets, but a reimagining of the traditional financial system itself.

Usual was founded by Pierre Person, born January 22, 1989. He previously served as a member of France’s National Assembly (6th constituency) and was a long-time election advisor and political ally of President Emmanuel Macron. Pierre Person’s political background combined with his understanding of blockchain technology allows him to lead the Usual team with a unique perspective, fostering convergence between Web3 and traditional finance. As a member of the French Socialist Party, he contributed to key legislative initiatives including LGBT healthcare access and cannabis legalization—demonstrating cross-domain thinking and innovation.

In terms of funding, Usual has attracted attention and capital from multiple prominent investors. In April 2024, Usual raised $7 million in a round led by IOSG Ventures, with participation from GSR, Mantle, and Starkware. In November, it secured an additional $1.5 million, backed by Comfy Capital and early crypto investor echo. In December, Usual announced a $10 million Series A round co-led by BinanceLabs

and KrakenVentures. These investments bring not only essential capital but also valuable industry resources and strategic guidance to accelerate project development.

Key Features of the Usual Stablecoin

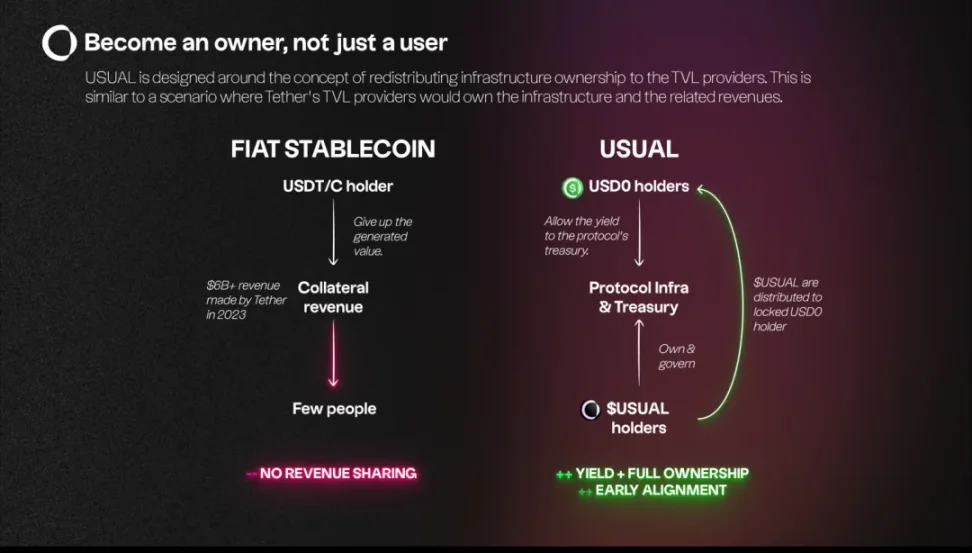

Unlike traditional centralized stablecoins, USD0, the stablecoin issued by Usual, demonstrates distinct advantages in stability, transparency, yield distribution, and decentralized governance.

Collateral Selection and Transparency

While traditional stablecoins are typically backed by cash or short-term commercial paper, USD0 uses ultra-short-dated real-world assets (RWA) as collateral—such as U.S. Treasury bills and overnight reverse repurchase agreements. Holders can convert USD0 into USD0++ to earn yield, which comes in the form of either risk-free USD0 or $USUAL tokens. Crucially, USD0’s underlying collateral is fully transparent and verifiable on-chain, allowing users to inspect and validate the assets backing USD0 at any time. This significantly enhances transparency and builds user trust in the protocol.

Innovative Yield Distribution Mechanism

With traditional stablecoins, nearly all generated yield flows directly to the issuer, leaving users with no direct benefit. USD0 takes a different approach—one rooted in fairness and transparency. All yield generated by USD0 is directed into the protocol treasury, and 90% of $USUAL token emissions are allocated to the community. This includes users, liquidity providers, and contributors. Through this mechanism, USD0 ensures participants share in the protocol’s growth, rather than concentrating profits solely within a central entity.

Even more interestingly, USD0 holders can upgrade their holdings to USD0++ to earn additional yield. This boosts user engagement and ensures that users benefit directly as the protocol grows—truly embodying the principles of decentralization and shared value creation.

In contrast, traditional stablecoins like USDT, despite holding vast amounts of U.S. Treasuries, retain nearly all profits within Tether Ltd. There is virtually no mechanism for ordinary users to participate in profit-sharing. For example, in the first half of 2024 alone, Tether reported a net profit of $5.2 billion—almost all of which went to the company, with no portion distributed to users.

Decentralized Governance and Transparent Management

Decentralized governance is one of USD0’s standout features. Within the Usual protocol, community members are not merely users—they can stake $USUAL tokens to participate in governance. They gain voting rights over treasury funds and key protocol decisions. This means the issuance and management of USD0 are not controlled by a single centralized authority, but collectively governed by the community.

The benefits of decentralized governance are clear: decisions are insulated from manipulation by any single interest group and better serve the collective interest. In contrast, traditional stablecoins like USDT are almost entirely controlled by Tether, offering minimal avenues for user governance participation.

Risk Management Advantages

As mentioned, USD0 uses highly liquid and secure government bonds as collateral. Compared to reserves held in commercial banks, this reduces exposure to systemic banking risks. The use of short-duration assets helps prevent forced fire sales during large-scale redemptions. Long-duration assets may need to be sold at a discount under redemption pressure, but short-term maturities mitigate this risk.

Additionally, all assets are tokenized and recorded on-chain, allowing users to verify their liquidity and safety in real time. This transparency greatly strengthens user confidence. Smart contracts automate the issuance and management of USD0, while arbitrage mechanisms help maintain price stability. When the market price of USD0 deviates from its peg, arbitrageurs can act to restore equilibrium. Together, these measures minimize price volatility and reduce the likelihood of systemic failure during mass redemptions.

Conclusion

As the Web3 sector continues to evolve, decentralized finance (DeFi) and cross-border payments have emerged as some of blockchain’s most promising use cases. Stablecoins, as critical bridges connecting traditional finance with on-chain assets, must embrace decentralization, transparency, and fair yield distribution to remain relevant and sustainable.

One of Web3’s core philosophies is decentralization and shared value creation. The Usual project embodies this principle by innovatively merging the strengths of traditional finance with the decentralized ethos of Web3. Through a more transparent, equitable, and decentralized framework, it introduces a new model for stablecoins—one that delivers higher yields to users and enables broader community participation in governance and value capture.

This, perhaps, is what the future of Web3.0 stablecoins should look like.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News