Bitcoin and U.S. markets plunge across the board: Behind Black Monday, yen carry trade unwinds

TechFlow Selected TechFlow Selected

Bitcoin and U.S. markets plunge across the board: Behind Black Monday, yen carry trade unwinds

Respect the market and risk!

By TechFlow

When a butterfly flaps its wings in Brazil, it could trigger a tornado in Texas one month later.

On July 31, the Bank of Japan raised its policy interest rate from 0%–0.1% to around 0.25%, marking the first rate hike since ending its negative interest rate policy in March this year.

Over the past month, the Japanese yen has appreciated approximately 8% against the U.S. dollar. As expectations grow for narrowing U.S.-Japan interest rate differentials, the reversal of carry trades is now triggering a large-scale global "liquidation."

Some global financial markets experienced a Black Monday.

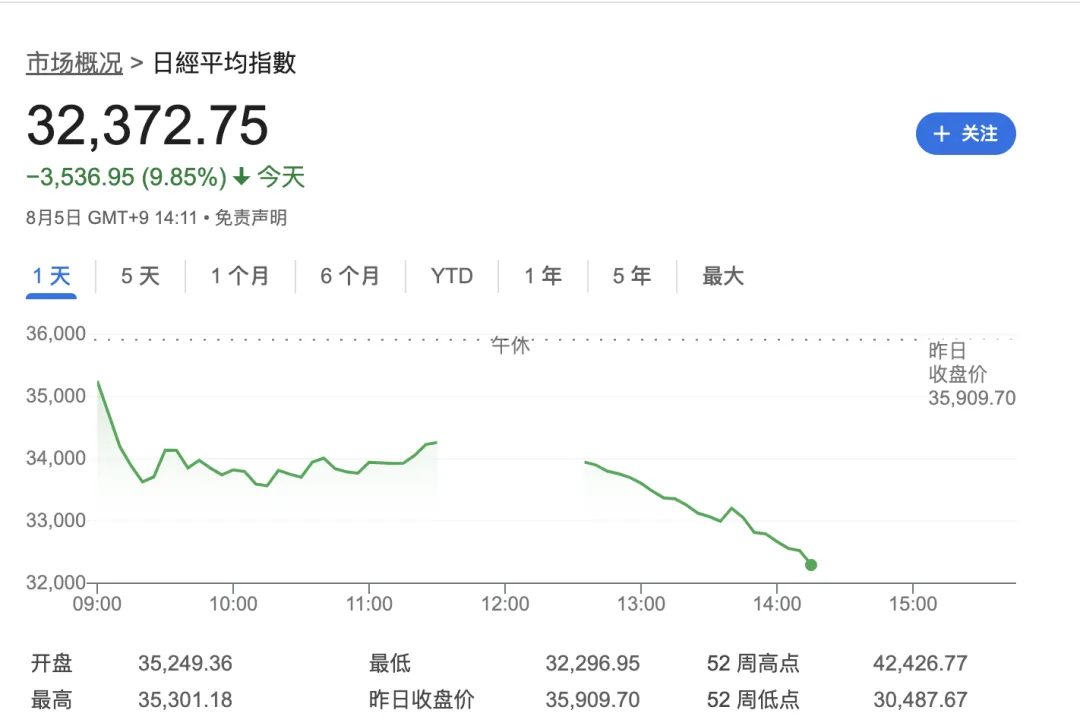

Japan's stock market suffered an epic plunge, with the Nikkei index plummeting 9% and the Tokyo Stock Exchange Index triggering circuit breakers twice—its largest single-day drop in eight years.

South Korea and Taiwan’s stock markets were not spared either.

South Korea's market opened down over 4%, with Samsung’s share price falling as much as 5%—its largest decline since 2020—prompting the Korea Exchange to implement temporary trading halts.

U.S. equity futures continued to slide, with Nasdaq 100 futures dropping more than 2%. Yields on two-year U.S. Treasury notes fell by 9 basis points, reaching their lowest level since May 2023. The U.S. Dollar Index dropped to around 103. Tonight’s U.S. markets are expected to face another stormy session.

However, the hardest hit was arguably the crypto market.

Bitcoin briefly dropped to around $54,000, while Ethereum fell to about $2,100—a nearly 20% daily decline. Over $800 million in long positions were liquidated within 24 hours, and the total market capitalization of the entire cryptocurrency market fell below $2 trillion.

In hindsight, this global sell-off may have been caused by a combination of the reversal in yen carry trades and escalating tensions in the Middle East.

What is a yen carry trade?

Currency carry trades are a form of interest rate arbitrage—borrowing in a low-interest-rate currency and investing in higher-yielding or higher-return assets.

Given Japan’s persistently low interest rates, market participants have long borrowed yen at low cost, converted them into U.S. dollars or other currencies, and invested in higher-yielding assets abroad.

The peak of yen carry trades began in 2004. To stimulate economic recovery, the Bank of Japan maintained a "zero interest rate" policy from March 2001 to July 2006. In contrast, Western economies frequently raised rates during this period, creating attractive yield spreads. Investors borrowed yen cheaply and bought high-yield currencies like the U.S. dollar and euro, investing in equities, real estate, or directly purchasing high-yield denominated assets for profit.

Historically, yen carry trades have supported bull markets globally by channeling cheap capital into other markets.

A classic example is Warren Buffett borrowing in yen last year to buy shares in major Japanese trading companies, fully hedging exchange rate risks, and focusing purely on the stable cash flows of these corporate giants.

Even the U.S. stock market’s prolonged bull run amid rising interest rates has benefited significantly from liquidity provided by yen carry trades.

Bitcoin, too, has benefited from sustained yen depreciation.

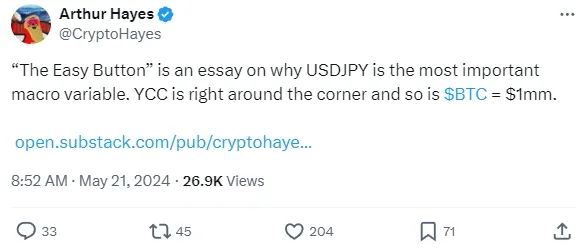

In May, BitMEX founder Arthur Hayes wrote an article bullish on Bitcoin, arguing that a weak yen could push Bitcoin toward $1 million.

Arthur pointed out that the USD/JPY exchange rate is one of the most critical variables in the global economy. The complex interplay between the monetary policies of China, the U.S., and Japan profoundly influences cryptocurrency market trends.

Regarding the expanding U.S.-Japan interest rate differential and the yen hitting new lows, Arthur noted that the Bank of Japan is reluctant to raise rates because it holds the largest amount of Japanese government bonds (JGBs). Rate hikes would cause bond prices to fall, leading to significant losses for the central bank. Yet if the BoJ stays put while the Fed doesn’t cut rates, the yield advantage of the dollar over the yen will persist, prompting investors to keep selling yen, driving further depreciation.

“Faced with global fiat currency depreciation, Bitcoin is the best-performing asset—and they know it. When measures are taken against yen weakness, I will mathematically forecast how capital inflows into the Bitcoin ecosystem could push prices to $1 million, or even higher,” Arthur predicted.

However, events have unfolded contrary to Arthur’s prediction—the yen did not continue depreciating; instead, the Bank of Japan began raising rates.

Historically, each reversal of yen carry trades has potentially triggered crises, as a major side effect has been inflating asset bubbles in recipient countries and markets—particularly emerging economies.

Massive flows of yen-funded capital have spread widely across global stock, foreign exchange, and commodity markets, becoming a pivotal force shaping market dynamics. Their rapid movements have also cast shadows of instability over international financial markets. For this reason, both the International Monetary Fund (IMF) and the Bank for International Settlements (BIS) have repeatedly warned about the dangers of yen carry trades.

The IMF once published a report examining the link between yen carry trades and the subprime mortgage crisis. It concluded that the unwinding of yen carry trades often leads to capital outflows, triggering global declines in asset prices. As financial institutions de-leverage, credit contraction follows.

Specifically, the impact of a reversal in yen carry trades manifests in several key areas:

Asset price volatility: Unwinding carry trades forces capital to exit high-yield risk assets, typically causing asset prices to fall.

Credit market tightening: As financial institutions unwind yen carry positions, they must sell assets and repay debts to reduce leverage, reducing liquidity in credit markets and tightening lending conditions.

Shifts in risk appetite: The VIX, or “fear index,” has a negative correlation with the scale of yen carry trades. When investors expect low risk and high returns, carry trade volumes rise—and vice versa.

Exacerbation of the subprime crisis: As institutions unwound their carry trade positions, prices of subprime-related assets fell further, worsening credit market strains and amplifying financial institution losses.

Recently, the sharp downturn in U.S. equities, led by tech stocks, largely reflects massive reverse unwinding of carry trades.

According to a report by Citigroup analysts Osamu Takashima AC, Daniel Tobon, and Brian Levine, the historical threshold for U.S.-Japan interest rate differentials that triggers a reversal—from rising to falling USD/JPY—is about 4.75%. Currently, the spread stands at approximately 5.25%. Reaching that threshold may require three rate cuts by the Federal Reserve, a process likely taking about six months.

Respect the market and risk!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News