Will the Bank of Japan take a more "hawkish" step with rate hikes and balance sheet contraction?

TechFlow Selected TechFlow Selected

Will the Bank of Japan take a more "hawkish" step with rate hikes and balance sheet contraction?

Higher-than-expected rate hike, smaller-than-expected balance sheet reduction.

Author: Zhao Ying, Wall Street Insights

The Bank of Japan (BOJ) took a "hawkish" turn, simultaneously announcing a rate hike and balance sheet reduction, demonstrating its determination toward policy normalization.

On Wednesday, July 31, the BOJ announced its latest interest rate decision, raising rates by 15 basis points to a policy rate range of 0.15%-0.25%. The decision passed with a 7-2 vote, exceeding market expectations which had anticipated no change.

At the same time, the BOJ unveiled its plan to shrink its balance sheet—reducing government bond purchases by 400 billion yen per quarter and shifting from specifying purchase ranges to setting fixed amounts. The BOJ unanimously voted to reduce bond buying, though the pace fell short of earlier expectations for a monthly reduction of 1 trillion yen.

The new monetary operations guidelines will take effect starting August 1, 2024. Analysts note:

The BOJ highlighted upside inflation risks over this year and next, which may have motivated its action. If this outlook proves accurate, further rate hikes could follow.

Following the announcement, the yen sharply fluctuated against the dollar, currently falling below 153 after briefly surging past 152 earlier. The Nikkei 225 index continued to decline post-decision, while Japanese 10-year government bond futures narrowed intraday losses after the rate hike announcement.

Rate Hike “Above Expectations,” Balance Sheet Contraction “Below Expectations”

The BOJ’s rate hike was “above expectations”—markets had priced in only about a 40% chance of a July increase—while the balance sheet reduction disappointed, as many expected monthly purchases to drop to 5 trillion yen next month. BOJ Governor Kazuo Ueda had previously emphasized that the reduction would be “substantial.”

Specifically:

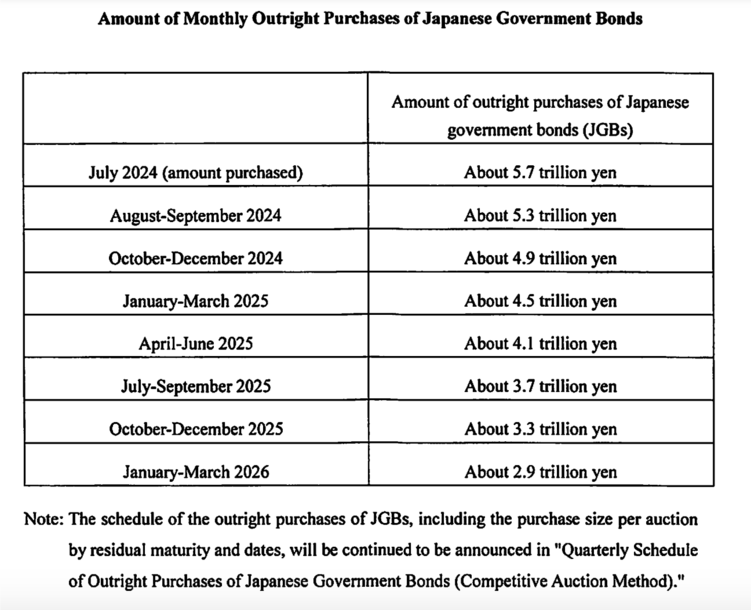

Current monthly bond purchases are around 6 trillion yen; July's were approximately 5.7 trillion yen; from August–September, they will be about 5.3 trillion yen; October–December, around 4.9 trillion yen...

By Q1 2026, monthly purchases are expected to reach about 3 trillion yen, with total Japanese government bond holdings projected to decline roughly 7–8% by mid-2024.

The BOJ added that a 0.25% interest rate will apply to current account balances held by financial institutions at the central bank. It will reduce bond purchases in a predictable manner, announcing purchase amounts each quarter, adjusting plans as needed, conducting a mid-term review of bond buying in June 2025, and evaluating the program during policy meetings if necessary.

Notably, prior to the official announcement, Japanese media appeared to leak details: NHK, Nikkei, and Jiji Press all reported on the potential rate hike, and the 8–9 month bond purchase schedule was released as expected, with reduced purchase amounts compared to prior levels.

Upside Price Risks Loom, Further Hikes Possible

The BOJ stated:

With substantial changes in the economic outlook, it will adjust its accommodative policy stance, given that real interest rates remain clearly low.

If inflation forecasts materialize, it will continue raising rates. Wage growth is notably stronger than last year, and price risks for fiscal years 2024 and 2025 are skewed to the upside.

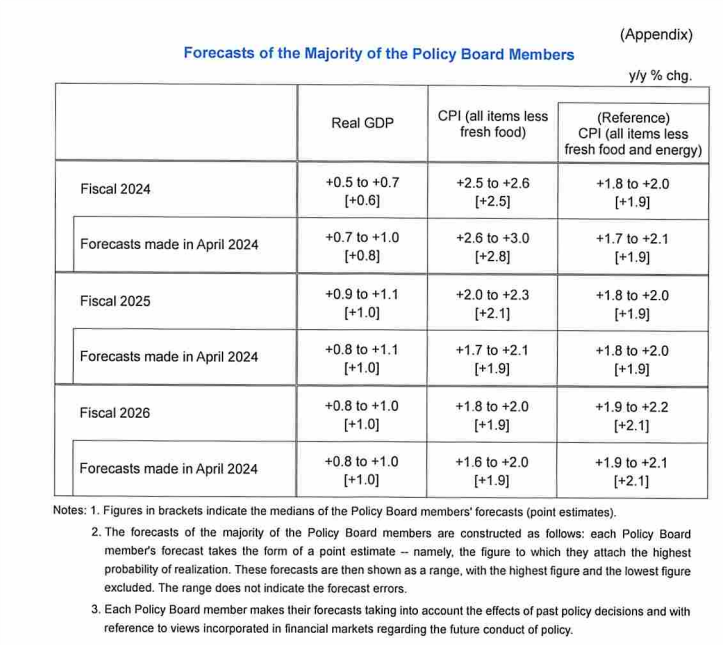

Regarding inflation projections, the BOJ slightly revised down its core CPI forecast for FY2024/25, while keeping excluding-energy core CPI unchanged:

FY2024 core CPI: 2.5%, previously 2.8%; FY2025 core CPI: 2.1%, previously 1.9%; FY2026 core CPI: 1.9%, unchanged from previous.

FY2024 excluding energy core CPI: 1.9%, unchanged; FY2025 excluding energy core CPI: 1.9%, unchanged; FY2026 excluding energy core CPI: 2.1%, unchanged.

Additionally, the BOJ noted:

The yen exchange rate is more likely than before to influence prices, with import prices rising again, requiring vigilance against inflation overshooting.

Despite price pressures, private consumption remains resilient, and corporate behavior is increasingly shifting toward raising both wages and prices.

Loose monetary conditions will continue supporting the economy, with real interest rates expected to remain significantly negative.

Will the BOJ Turn Even More Hawkish?

Analysts believe this rate decision was not dovish. The BOJ formally committed in writing that if favorable trends in economic activity and inflation persist, it will raise rates further—an unprecedented move and the first sign of hawkishness under Governor Kazuo Ueda’s leadership. Regarding bond purchases, Nick Twidale, analyst at ATFX Global Markets, said the BOJ’s pace of balance sheet reduction was far below expectations, weighing heavily on the yen.

However, analysts Toru Fujioka and Sumio Ito believe the yen’s weakness may have reached a turning point:

The BOJ raised its policy rate and indicated it aims to bring monthly bond purchases down to about 3 trillion yen by Q1 2026. While taking these steps, Governor Ueda signaled the central bank’s ongoing commitment to normalization. Wednesday’s move could fuel speculation of another rate hike this year. Coming hours before the Fed’s meeting, the BOJ’s hawkish tilt might mark a turning point for the struggling yen, as traders anticipate a narrowing U.S.-Japan interest rate differential. Any Fed hints at a possible September rate cut would reinforce this view.

Izuru Kato, chief economist at OTAN Research, said:

The rate hike decision was likely aimed at correcting excessively loose monetary policy, reflecting how deeply negative real policy rates have become. Although the BOJ has long maintained that its policy isn’t targeted at exchange rates, the damage caused by yen weakness to small and medium-sized enterprises in rural Japan is surely a key factor behind today’s decision. The size of the hike is small and largely symbolic. There’s no need to fear an accelerated hiking cycle—the BOJ’s moves in March and July merely match what a typical central bank might do in a single hike. This doesn’t mean the BOJ has suddenly turned hawkish. Looking ahead, the BOJ will remain cautious, avoiding overly rapid tightening.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News