Recap of 2024 Crypto Funding Landscape & Outlook on Promising Sectors

TechFlow Selected TechFlow Selected

Recap of 2024 Crypto Funding Landscape & Outlook on Promising Sectors

This article will examine the overall funding landscape of 2024, followed by an analysis of investment trends in specific sectors by prominent VCs.

Background

The crypto market hit rock bottom in 2022, began recovering in Q4 2023, and in 2024 saw Bitcoin surpass the previous bull market high of $69,000. As the market warms up, we believe that beyond price movements, overall fundraising trends within the crypto sector are equally critical.

The level of fundraising activity reflects the momentum driving industry development, reflected in:

-

Driving technological innovation: Fundraising is a key driver of technological advancement. Financial support enables research and application of new technologies, promoting broader industry progress.

-

Market sentiment indicator: Venture capital investment reflects investor expectations for the crypto market’s future. A decline in both the volume and amount of fundraising signals increasingly conservative or even bearish sentiment among external investors.

The positive flywheel effect generated by fundraising is particularly evident:

-

Increased funding rounds: Influx of capital attracts more investors and venture funds, leading to more fundraising deals.

-

Attracting startups: As funding opportunities grow, more entrepreneurial teams and companies enter the crypto space to develop new technologies and applications.

-

Improved ecosystem: The emergence of new technologies and applications enhances the market ecosystem, increasing diversity and innovation.

-

Increased investor interest: A healthier ecosystem and continuous technological innovation attract more investor attention, further strengthening market confidence.

In this report, WOO X Research will examine overall fundraising trends in 2024, analyze investment patterns of prominent VCs across sub-sectors, and use funding data to predict future high-potential areas.

Overall Fundraising Landscape in 2024

-

Funding Amount and Frequency: The overall fundraising market began recovering from November 2023. In 2024, monthly deal counts have consistently remained above 120 (as of mid-July), with monthly funding amounts ranging between $7–10 billion—showing significant growth in both volume and value compared to 2023.

-

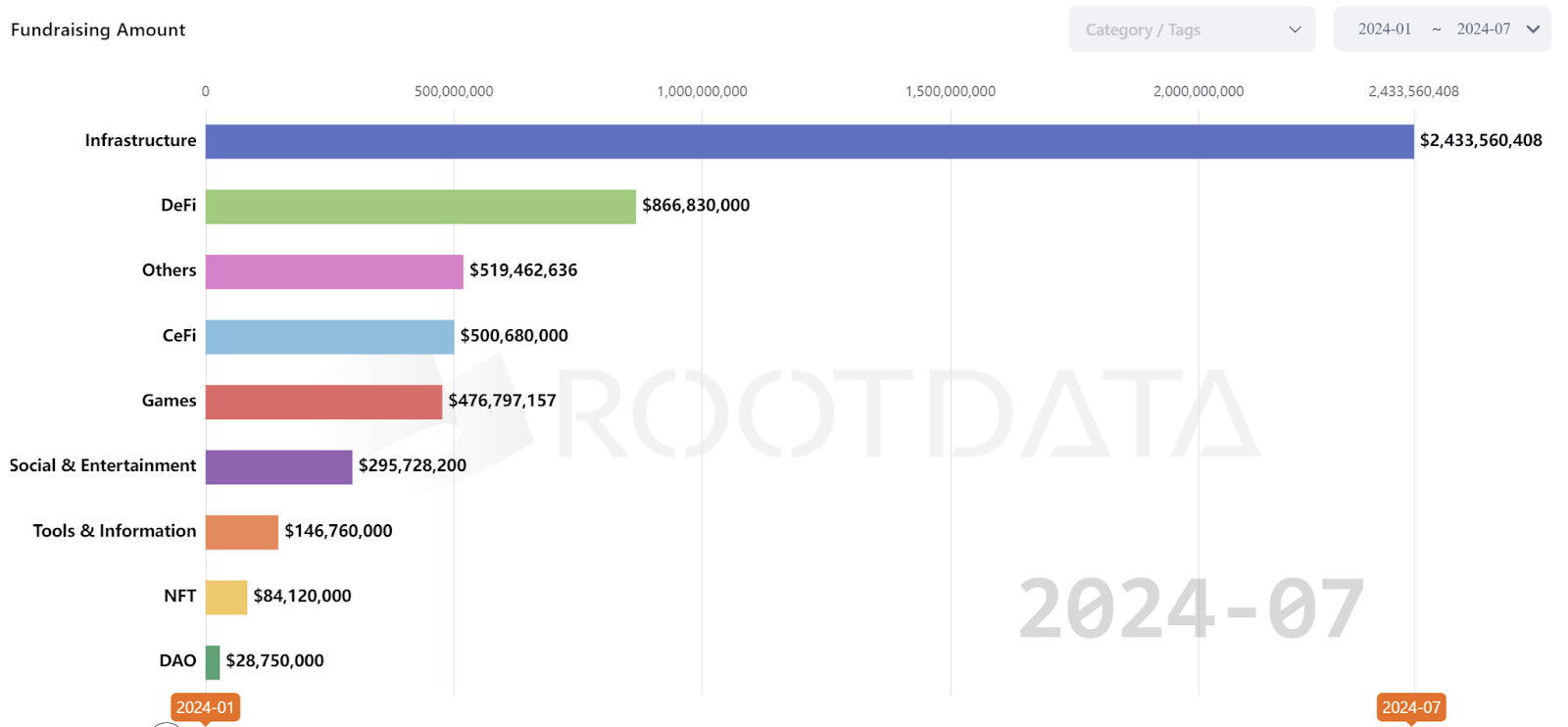

Sector Performance: Infrastructure attracted the most investment, raising $2.4 billion—far exceeding DeFi, which ranked second with $860 million. VC interest in DAOs and NFTs remains weak, ranking last in total funding raised.

-

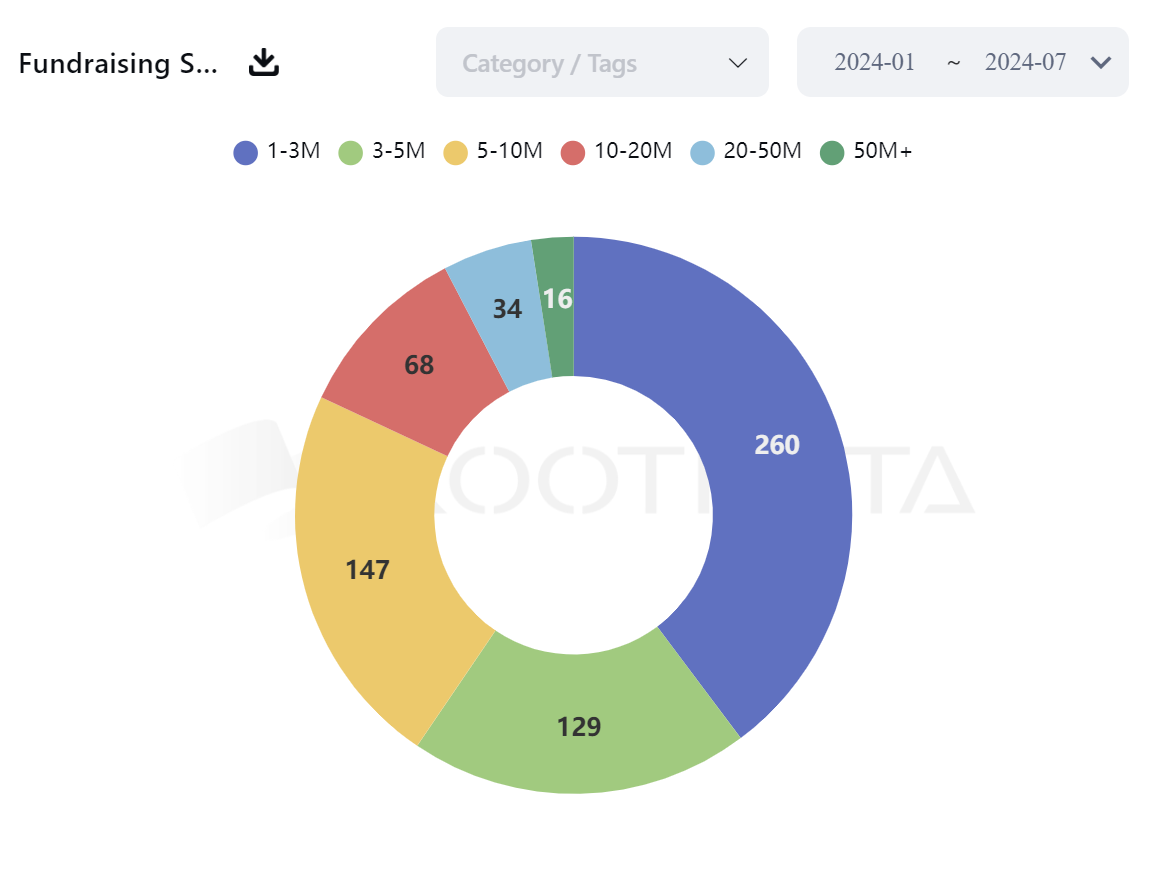

Deal Size Distribution: The $1–3 million range accounted for 40% of deals—the largest share—followed by $5–10 million at 22%. The $3–5 million range declined compared to 2023, with reductions redistributed into the $1–3 million and $5–10 million brackets, indicating a polarization in funding sizes in 2024, with fewer mid-sized raises.

Top VC Investment Trends

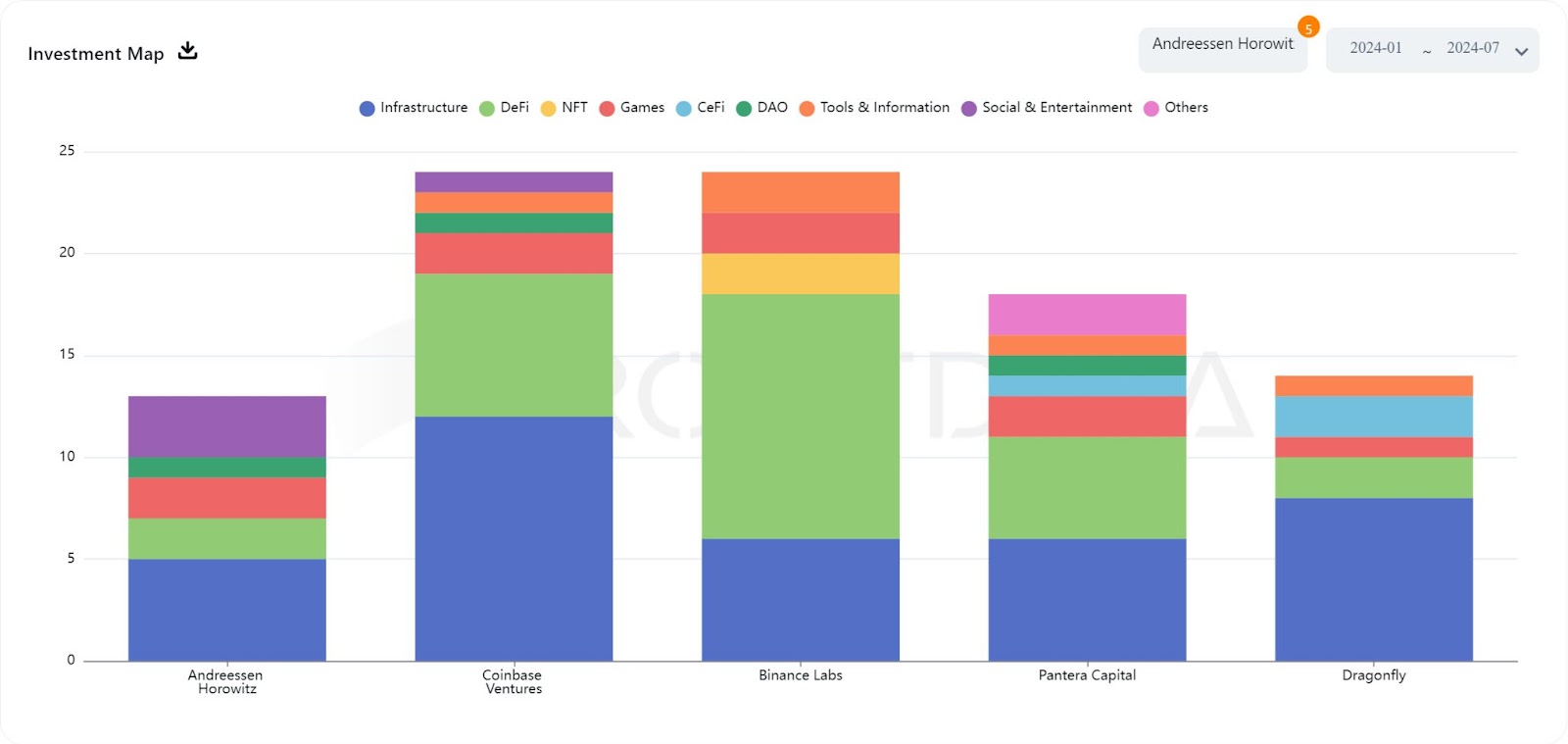

This report focuses on five leading VCs: A16Z, Coinbase Ventures, Binance Labs, Pantera Capital, and Dragonfly.

Key insights from the data above include:

-

A16Z (Andreessen Horowitz): Primarily invests in infrastructure, DeFi, and gaming, with some investments in NFTs and social entertainment.

-

Coinbase Ventures: Diversified investments, with strong focus on DeFi and infrastructure, while also participating in tools & information, social entertainment, and DAOs.

-

Binance Labs: Majority of investments in DeFi and infrastructure, followed by social entertainment and gaming.

-

Pantera Capital: Focuses on DeFi and infrastructure, with partial allocations to NFTs and other sectors.

-

Dragonfly: Broad investment scope, with major allocations to infrastructure, DeFi, NFTs, and tools & information.

Consistent with our earlier observation of 2024’s overall fundraising landscape, these top five VCs continue to prioritize infrastructure and DeFi. Below is a review of their portfolio investments:

-

A16Z: Made 13 public investments, including three lead investments (Friends With Benefits, EigenLayer, Espresso System).

The highest-funded project in its portfolio is Farcaster, a Web3 social app that raised $150 million in Series A at a $1 billion valuation.

Notably, although A16Z did not lead Farcaster’s Series A round, it was involved during the seed round in 2022.

-

Coinbase Ventures: Conducted 24 investments, including two lead investments (El Dorado, WITNESS).

The highest-funded project in its portfolio is Conduit, an infrastructure platform that raised $37 million in Series A to provide developer toolkits.

-

Binance Labs: Completed 24 investments. Prefers direct, solo investments and rarely discloses funding amounts or co-investment details.

Among disclosed investments, Ethena raised the most—$14 million in an extended seed round.

Other independently funded projects include: Catizen, Zircuit, Infrared, Rango, Aevo, Movement, BounceBit, StakeStone, Cellula, Derivio, Babylon, RENZO, NFPrompt, Puffer Finance, Shogun, BracketX Protocol, Memeland—representing the majority. Over 80% of these projects have not yet launched tokens, but if they do, there is potential for listing on Binance.

-

Pantera Capital: Made 18 investments, with 9 led (50% lead rate in 2024). The highest-funded project in its portfolio is Sentient, an open-source AI model that raised $85 million in seed funding to directly compete with OpenAI.

-

Dragonfly: Made 14 investments, leading 11 (79% lead rate in 2024)—the highest among the five firms. The highest-funded project in its portfolio is Polymarket, a prediction market praised by Vitalik Buterin, which raised $45 million in Series B.

Among all projects invested in by these five VCs, only three received backing from two institutions:

Neynar: Development platform for Farcaster

-

Investors: A16Z, Coinbase Ventures

-

Round: Series A

-

Amount: $11 million

-

Date: May 30

Nexus: Modular zkVM project

-

Investors: Dragonfly, Pantera Capital

-

Round: Series A

-

Amount: $25 million

-

Date: June 10

Morph: L2 combining optimistic and ZK technologies

-

Investors: Dragonfly, Pantera Capital

-

Round: Seed

-

Amount: $20 million

-

Date: March 20

Notably, Binance Labs did not co-invest with any of the other four VCs on shared projects.

High-Potential Sectors: Intent-Centric Architectures, Modular Blockchains, Parallel EVM

The global cryptocurrency market cap stands at approximately $2.5 trillion—a relatively small share compared to companies like NVIDIA—highlighting substantial room for growth. As repeatedly noted, infrastructure and decentralized finance (DeFi) remain preferred investment areas for VCs because they form the foundational layer of crypto market development.

Infrastructure supports the entire ecosystem and typically offers longer lifecycles and stable returns; DeFi forms the liquidity backbone of the market—high liquidity attracts more liquidity, creating a positive flywheel effect.

Currently, token prices in infrastructure and DeFi significantly underperform meme coins. This can be attributed to the ongoing absence of rate cuts and limited liquidity inflow. The rise of meme coins also reflects voter backlash against poor-quality VC-backed tokens. However, truly exceptional projects will endure, and short-term price stagnation does not equate to lack of value.

Within infrastructure, we identify three promising areas: intent-centric architectures, modular blockchains, and parallel EVMs. These share a common goal—addressing existing blockchain limitations: intent-centric systems improve user experience, modular blockchains aim to overcome the blockchain trilemma, and parallel EVMs break through traditional EVM processing speed constraints.

Let us tune out short-term noise and grow alongside the long-term evolution of the crypto market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News