Value Investing in the Crypto World: Betting on Products That Generate Stable Profits

TechFlow Selected TechFlow Selected

Value Investing in the Crypto World: Betting on Products That Generate Stable Profits

The only sustainable way to make profits is to own a real product that generates revenue.

Author: Octoshi

Translation: TechFlow

What is Value Investing?

As the name suggests, value investing is an investment strategy focused on acquiring undervalued assets whose intrinsic value exceeds their current market price.

Value investing is often combined with fundamental analysis and typically focuses on the following characteristics:

-

Price below book value: Stocks trading at low prices relative to their book value of assets.

-

Significant margin of safety: The difference between intrinsic value and market price, providing protection against misvaluation.

-

Low Price-to-Earnings (P/E) ratio: A P/E ratio lower than industry or overall market levels.

-

Financial strength: Companies with strong balance sheets, low debt, and stable cash flows.

-

Competitive advantage: Companies with sustainable competitive advantages that allow them to maintain dominance in their industry and achieve high returns on capital.

In fact, Benjamin Graham is considered the father of value investing, and Warren Buffett—the world's most famous and successful investor—was his student.

Can Value Investing Be Applied to Cryptocurrencies?

This is a great question. In fact, why not take a few minutes to think about it and draw your own conclusion?

Although in the crypto space we see memecoins multiplying 100x, cryptocurrencies without real value or with high fully diluted valuations (FDV) rising, and all sorts of strange phenomena, I believe we can apply value investing in crypto, but we need to account for certain differences. Traditional stock market value investing strategies may lead to losses when applied directly to cryptocurrency.

One of the biggest differences lies in fundamentals and their weighting. In such a fast-changing emerging industry, growth metrics like revenue and active users carry less weight because they can change rapidly—and may even be manipulated or influenced by temporary incentives. These incentives eventually end, turning what seemed like a fundamentally sound investment months ago into a poor choice today.

Which Cryptocurrencies Might Be Suitable for Value Investing?

Now that we understand the concept of value investing and know it can be applied to crypto investments, the next question is: which cryptocurrencies might qualify as value investments?

To find answers, let’s revisit the characteristics of value investing and try applying them to cryptocurrencies:

Risk-Free Value (RFV):

The first characteristic—"price below book value"—in crypto is known as Risk-Free Value (RFV).

RFV investing involves buying tokens where treasury value exceeds market cap (MC), then waiting for this mispricing to correct. This correction can happen in various ways—for example, through organic growth as more people notice the discrepancy and buy the token to reach fair valuation; via governance proposals to use part of the treasury or earnings to repurchase undervalued tokens; or through protocol shutdowns that allow investors to redeem their tokens for a proportional share of the treasury.

This sounds like free money—but it comes with risks. Often, such discounts exist for good reasons, most commonly due to distrust in the team, who might execute a "Rug Pull" or slowly drain the treasury through salaries, budgets, or other bad practices while ignoring the community. There’s also opportunity cost, as extended waiting periods may cause us to miss other opportunities.

These scenarios have happened many times in crypto. Some cases I recall include ROOK, Tribe DAO, NonusDAO, Nexus Mutual, Aragon, and FLOOR and NFTX. Additionally, the Patagon v. Spartacus case set a solid legal precedent showing that despite the industry’s youth, DAOs are not immune to legal accountability.

Concave is another noteworthy case. It traded below book value for a long time, used its treasury to participate in multiple seed rounds, acquired Fjord for $1.5 million, and successfully launched it with a $250 million fully diluted valuation (FDV), returning all value to holders. For instance, throughout the bear market, you could buy CNV for under $4, and each token entitled you to $9 in USDC from Fjord fees, $15 in locked FJO tokens, plus allocations from other seed rounds like Tapioca and Berachain still pending (potentially another $15 per token).

Arbitrage also falls into this category, typically occurring when assets lose their peg—for example, stablecoins or liquid staking/re-staking tokens trading below a 1:1 ratio. Cases I remember include crETH2, USDC, stETH, and ezETH. Each case must be analyzed individually—we all know what happened with UST.

At the time of writing, there are some RFV opportunities—for example, GNO buybacks via a specific wallet. We’ve also identified cases like JPGD and HEGIC, both tokens significantly discounted relative to their treasuries—almost 100% ETH—so I view them as long-term ETH holding vehicles. The latest opportunity is USDR, a stablecoin trading at $0.61 backed by real estate undergoing liquidation.

Interestingly, Warren Buffett started his career using this very strategy. Berkshire Hathaway was originally a textile company; Warren bought it to restructure and profitably sell off, but management resisted, so he took control—and the rest is history.

Margin of Safety

The above RFV examples can also be seen as margin of safety, but a treasury larger than market cap (MC) isn’t strictly necessary. For example, if a protocol’s treasury represents 70% of its market cap, that means in the worst-case scenario, we’d only lose 30% of our investment. Several protocols have decent treasuries—you can check them on DefiLlama. Many even put their treasuries to work in DeFi, such as TempleDAO and ParagonsDAO.

Low Price-to-Earnings Ratio

While not numerous, there are indeed some profitable protocols (where income exceeds expenses). Although most will have high P/E ratios, exceptions do exist. However, as previously mentioned, this metric can be manipulated or fluctuate significantly due to the dynamic nature of crypto markets.

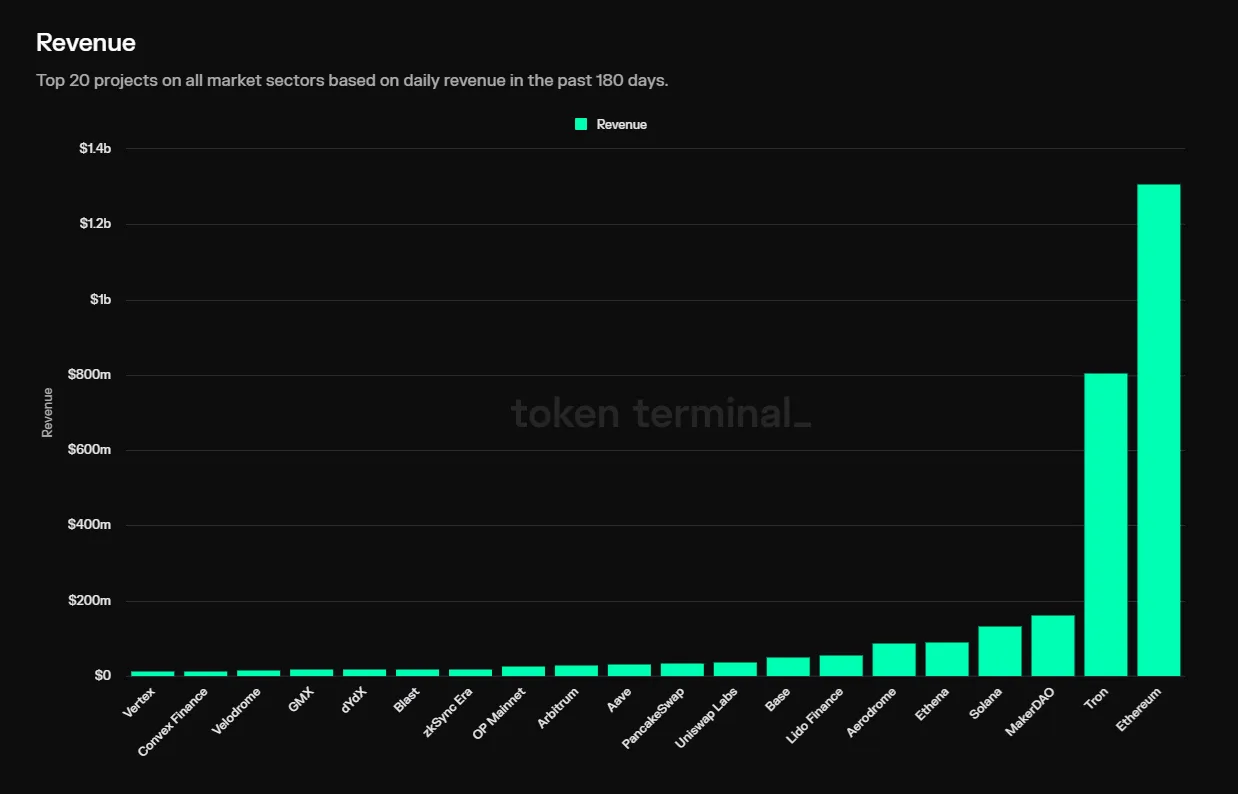

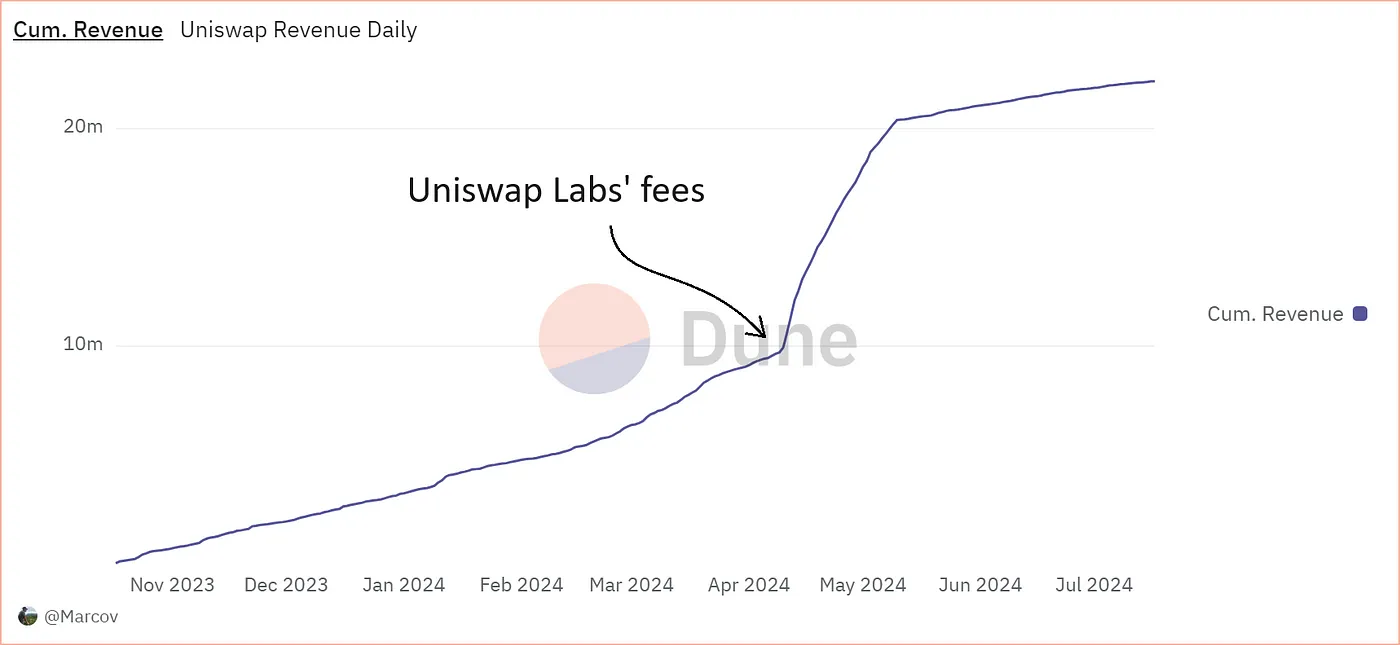

Token Terminal is a great tool to start exploring this data. We can begin with the fees dashboard to see which protocols generate the most fees, but these fees don’t necessarily go to the protocol—for example, Uniswap, one of the top fee generators, directs 100% of fees to liquidity providers (currently). That’s why we have the revenue dashboard, which shows the portion of fees going to the protocol. But even that isn’t enough, since protocols may spend heavily on incentives (expenses) to generate those fees—which is why we have the earnings dashboard, showing revenue minus incentives.

Another excellent tool for viewing all this data is Defillama’s fees dashboard. If you want to go further, consider the protocol’s spending on salaries, marketing, development, etc. A great resource for this is Defillama’s expenses dashboard (again, thanks to the llamas).

With these data points in mind, we currently see most L1s/L2s with negative P/E ratios. The largest dapps—AAVE, MKR, and LDO—are beginning to turn profitable, with Price-to-Sales (P/S) ratios around 20–30.

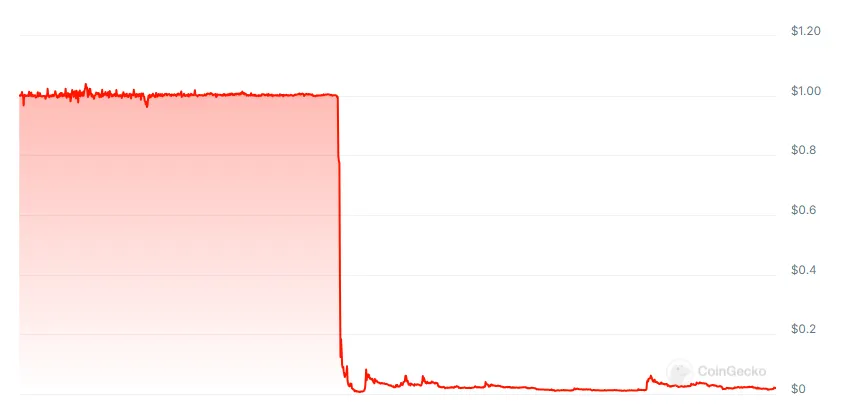

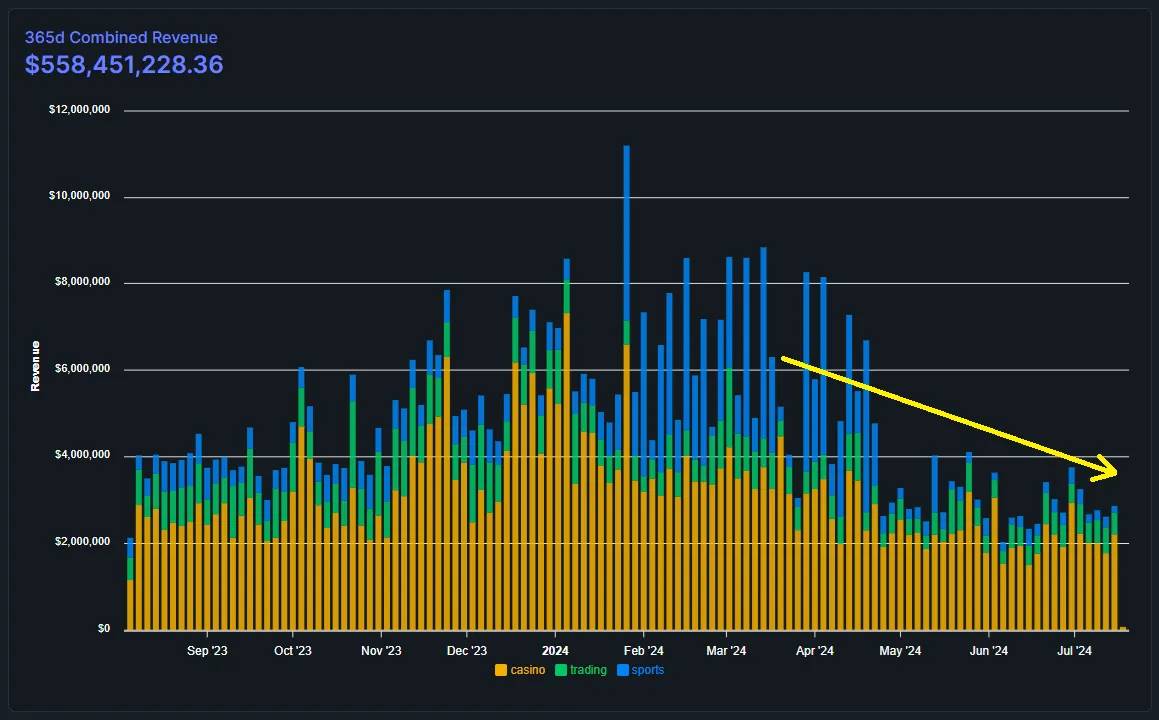

But if we’re talking about low P/E, one business that comes to mind is Rollbit, a crypto casino with a $232 million fully diluted valuation (FDV). Annualizing its revenue over the past 30 days gives us $342 million per year, resulting in a mere P/S ratio of 0.68! To calculate the P/E ratio, we’d need to subtract expenses, but Rollbit lacks transparency here. Perhaps this lack of transparency, along with some controversies and unclear team focus, explains the discount. Personally, such situations often create good buying opportunities—but do your own research (DYOR), especially since revenue appears to be gradually declining:

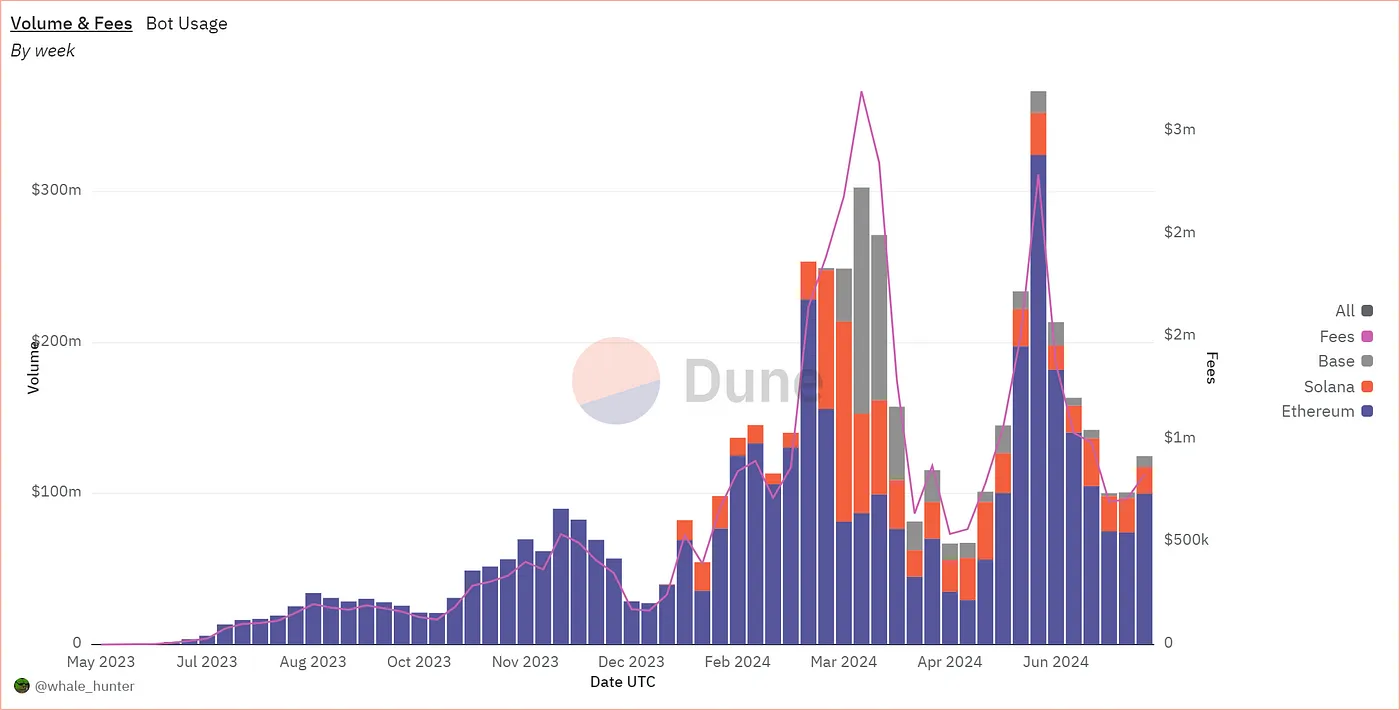

Another one to watch is Banana Gun, a popular trading bot on Telegram. Despite a sharp price increase after announcing a Binance listing, it still has a P/S ratio of 12, real revenue, ongoing product development, and organic growth. DYOR is still recommended.

Strong Financials and Competitive Advantage

Let’s now examine the last two characteristics of value investing. Strong financials include being debt-free (rare in crypto, though there have been cases post-exploit), steadily increasing and relatively stable profitability, organic growth, and a productive treasury. Competitive advantages include strong branding, intellectual property (e.g., Uniswap V3 protecting its code), network effects, and liquidity—features that enable a protocol to maintain dominance.

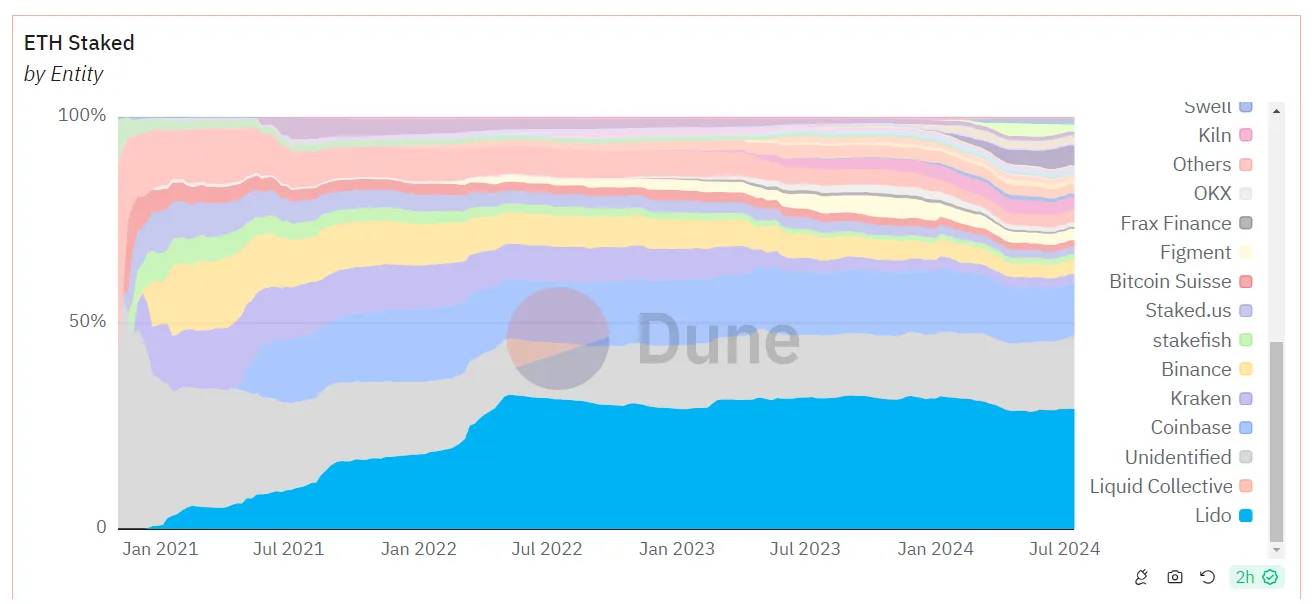

Lido is a prime example. It’s the protocol with the highest total value locked (TVL)—$33 billion versus $15 billion for second place—and holds a 29% market share in stETH (compared to Coinbase’s 12.7%, EtherFi’s 4.8%, and Binance’s 3.5%). Moreover, stETH is considered the safest liquid staking token (LST), with the highest liquidity and DeFi integration. We saw user preference for stETH during Eigenlayer or Simbiotic launches, where stETH filled orders far faster than other LSTs. This is undoubtedly one of the best examples of competitive advantage in DeFi—an organically formed monopoly!

Aave and Uniswap also fall into this category. Aave holds a 37% market share, Uniswap 28%. Additionally, Uniswap accounts for 52% of total volume among decentralized exchanges (DEXs). Both are mature protocols with strong brands, making users feel secure when lending or providing liquidity. As competitive advantages grow, these protocols can improve their margins—for example, Uniswap charges a 0.25% fee on its interface, though currently this goes to Uniswap Labs. This could change in the future.

Maker is another strong protocol, possibly with the strongest financials, though I’m skeptical about its long-term competitive advantage—other stablecoins like USDC and USDe appear to be gaining market share.

Though it’s a stock, Coinbase ($COIN) is also a solid value investment with clear competitive advantages. For example, its LST $cbETH charges a 20% fee—the highest in the market, compared to 10% for Lido and Binance. Coinbase offers a wide range of products including its CEX, futures, staking services, its own L2, wallet, Circle stake, and more.

Solana can also be included here. Though its finances are weak—its inflation far exceeds fee-generated revenue—this may be a strategy to gain market share (and it’s working so far). It also has its own ecosystem, organic growth, real users, low entry barriers, and excellent user experience.

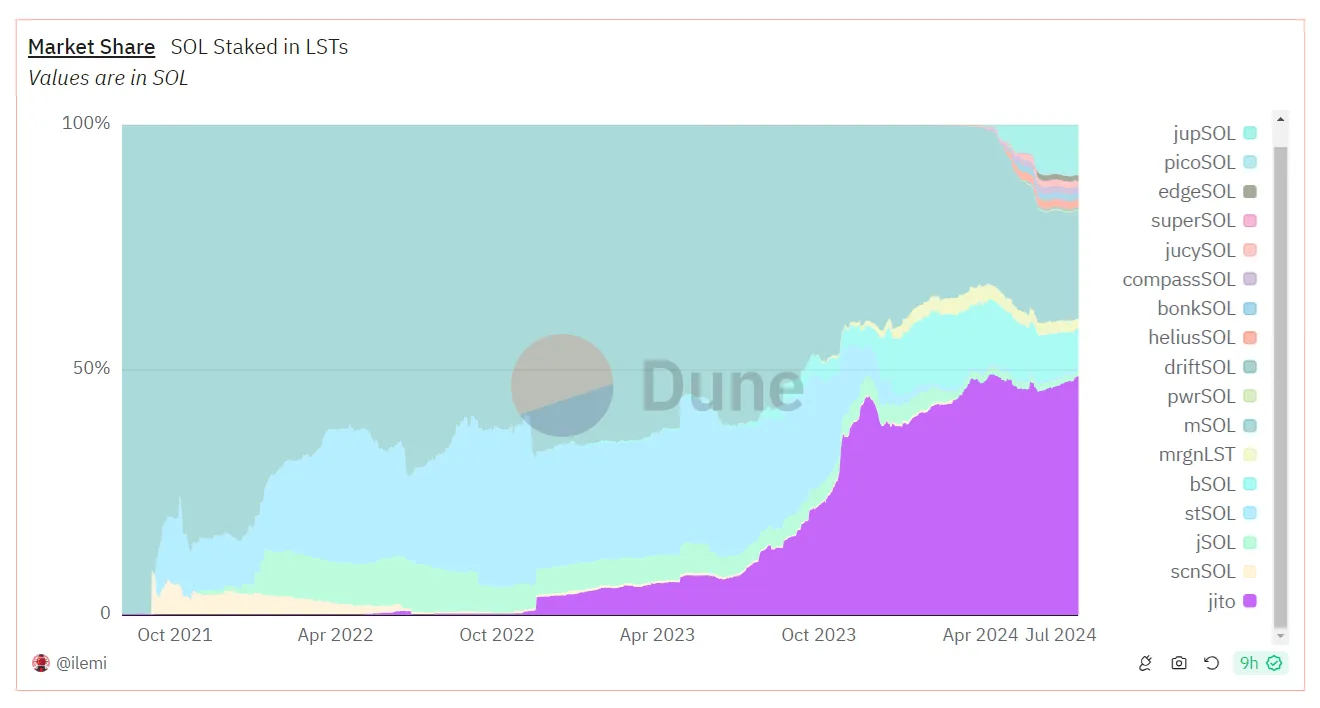

A dominant protocol within Solana is Jito. It’s the dapp with the highest TVL at $2 billion. While JitoSOL holds only a 3% market share (since most SOL is natively staked), it commands 48% of the LST market share (using the same methodology, Lido holds 71%). Jito’s revenue appears solid and growing, though its current valuation is quite high ($2.7 billion vs Lido’s $1.9 billion)—everything depends on Solana’s future.

Another Solana project I really like is Phantom, the default wallet with an outstanding interface (10/10). I believe most people will use wallets on mobile phones rather than PCs in the future, giving Phantom and its mobile app a significant edge. Its competitive advantage could allow it to charge fees on swaps (similar to Metamask, Rabby, and Uniswap Wallet). Although Phantom has no token, I rank it as a high-priority project.

Phantom ranks #1 among Finance Apps on Google Play

To clarify, although I haven’t discussed tokenomics, it’s another crucial area for research. I believe tokenomics aligned with value investing should be simple, with most tokens already in circulation and delivering value to holders in various ways. Good ponzinomics may help launch a project and gain liquidity, but won’t be profitable long-term. The only way to achieve lasting profitability is by building a real product that generates profits.

I hope you found this article useful and interesting. If so, please share it with others. I write purely out of passion, with no financial incentive. If I see enough support, it will motivate me to write more!

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News