Data Interpretation of Crypto's Reorientation: Growing Pains Amid Global Liquidity Crunch

TechFlow Selected TechFlow Selected

Data Interpretation of Crypto's Reorientation: Growing Pains Amid Global Liquidity Crunch

Data-driven insights into the authentic on-chain world.

Author: Hedy Bi, OKG Research

Globally, there are over 5 billion searches conducted every day, and 491 exabytes (EB) of data enter our lives daily. If all this data were delivered via email, it would equate to one person needing to process 3.6 billion emails per day. As blockchain technology continues to evolve, moving from off-chain to on-chain systems, the world built on on-chain data can no longer be ignored. According to on-chain data calculated by OKLink from OKGroup, the daily trading volume of just one cryptocurrency—USDT—is already equivalent to one-tenth of the New York Stock Exchange’s average daily trading volume.

The world is being digitized. In particular, blockchains publicly and rigorously record every transaction, and the massive volume of data along with complex transaction networks makes it increasingly difficult to comprehensively and clearly analyze our market environment. OKG Research, the research institute of OKGroup, has partnered with PANews to launch a new series that uses data to reveal the true nature of the on-chain world.

This article is jointly produced by OKG Research, the research arm of OKGroup, and PANews: using data to uncover insights into the real on-chain world.

Recently, despite the opening of ETF channels, the anticipated "massive inflow of capital" into the crypto market has not materialized, as liquidity shortages in global financial markets have spilled over into the crypto space. The emergence of new channels also means that the established rules of traditional, complex, and mature markets are now colliding with the culture and investment logic of the crypto market. As a result, the crypto market has transformed from a nearly closed safe haven into a small boat adrift in the open sea. This fundamental shift in market nature brings new challenges.

Bitcoin: No Longer Digital Gold?

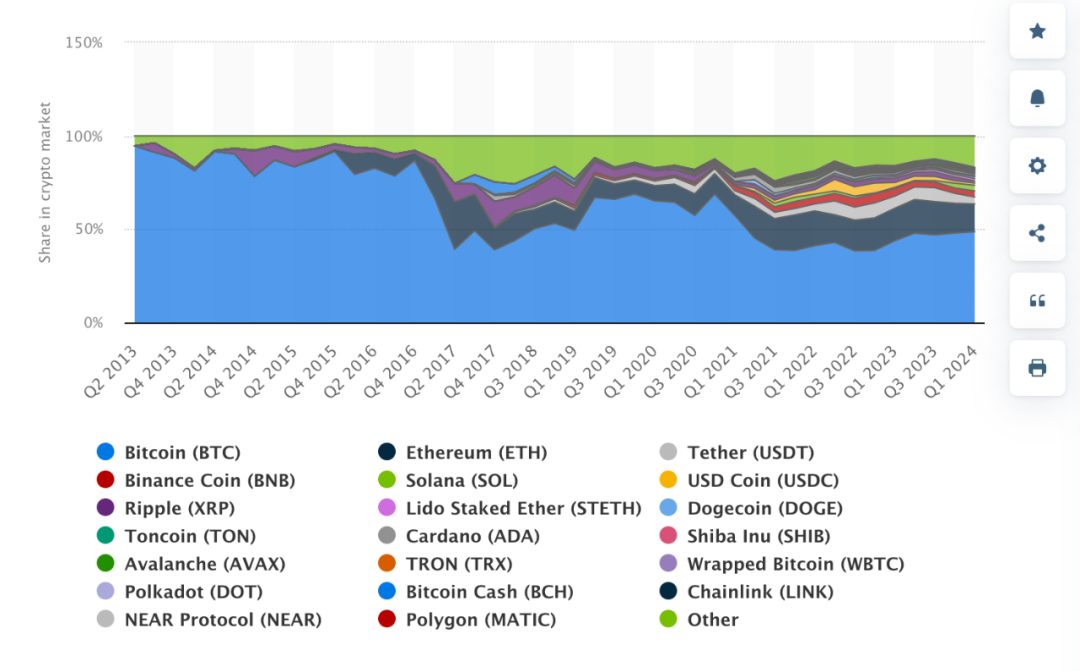

To understand the crypto market, we start with Bitcoin, which accounts for half the market.

Pic: Dominance of Bitcoin and other cryptos in the overall market from 2nd quarter of 2013 to 1st quarter of 2024

Source: statista

Looking back at this year, several key events stand out. For example, in April, heightened tensions between Iran and Israel—and Iran’s retaliatory actions—caused a noticeable drop in Bitcoin prices, even though Asian-Pacific markets showed little reaction in their financial sectors. Additionally, U.S. economic data not only affects domestic financial markets but also influences Bitcoin. For instance, during the first half of the year, when U.S. unemployment figures rose above expectations, markets interpreted this as increasing the likelihood of looser monetary policy by the central bank, which could fuel a rebound in U.S. equities—and in turn, push Bitcoin prices upward.

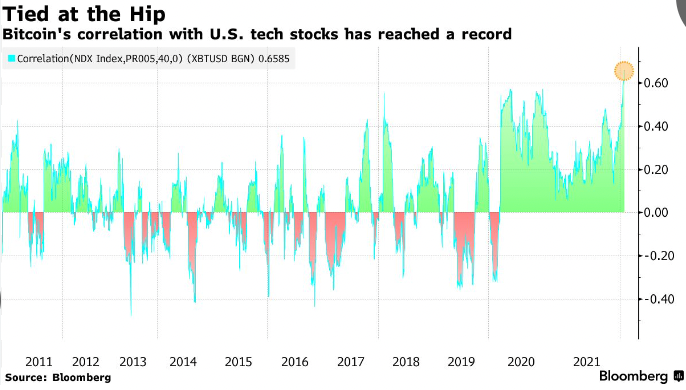

Previously, Bitcoin was seen as “digital gold,” believed to move inversely to the U.S. dollar cycle. But today, Bitcoin appears more like an “amplifier” of the Nasdaq. For institutional investors entering the space, Bitcoin lacks conventional fundamental analysis metrics (such as financial indicators or cash flow analysis). Its value is primarily determined by supply and demand dynamics and investor sentiment, making commodity-like characteristics combined with sentiment indicators key tools for quantitative trading strategies. Coupled with the widespread use of leverage in crypto markets, Bitcoin exhibits higher volatility—a new market trait we must adapt to.

Compared to 2022’s Seven Rate Hikes, Crypto Demand Is Clearly Weaker

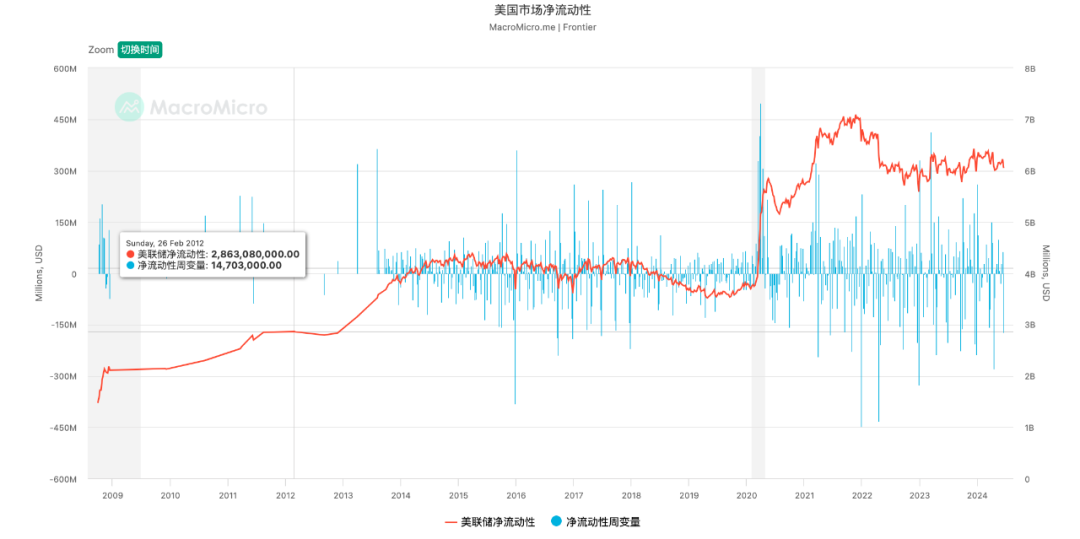

Taking the U.S. market as an example, M2 (broad money supply) has been slowly declining since the first half of 2022. According to Macromicro.me, seven Federal Reserve rate hikes between March and December 2022 caused the U.S. net liquidity index to plummet rapidly—and it has not recovered since. The U.S. interest rate hikes in 2022 had a significant impact on market liquidity, which failed to sustain prior growth trends. Consequently, demand in the crypto market has clearly diminished.

Source: Fred

Source: MacroMicro

We examine stablecoins to gain deeper insight into crypto market demand. Stablecoin issuance mechanisms mean that their issuance directly reflects market demand for crypto. Overall stablecoin market capitalization has increased by approximately $30 billion since the beginning of 2024 (about six months). Compared to the second half of 2021 and first half of 2022, this growth rate is significantly slower—even though those earlier periods coincided with tightening global financial liquidity. This indicates that the crypto market has shifted from being a hedge against risk to becoming just another small vessel in the vast ocean of global finance.

Pic: Stablecoin Total Market Cap

Source: DeFiLlama

Thus, we can roughly conclude that the overall character of the crypto market has shifted—from a nearly closed-off haven for hedging financial risks to a market far more sensitive to macroeconomic conditions. Bitcoin has evolved from “digital gold” into an “amplifier” of U.S. equity markets like the Nasdaq. Economic indicators influence market liquidity and directly affect the crypto market.

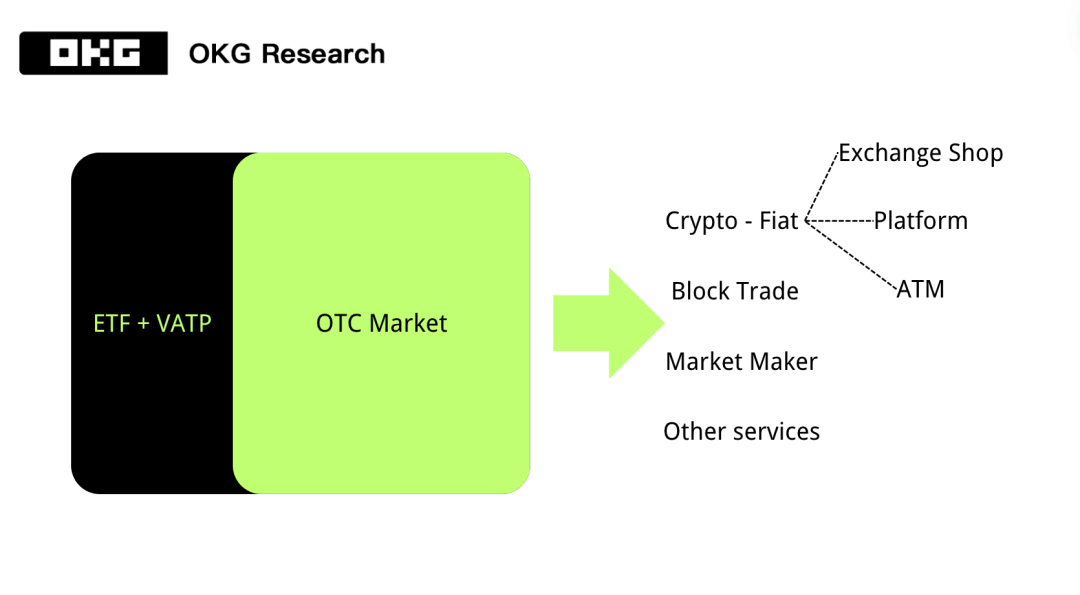

This OTC Is Not That OTC: Injecting Liquidity Into the Market

Under current macroeconomic policies, how do we address liquidity issues in the crypto market? Two general approaches exist: promoting institutional investor participation and improving market infrastructure. Here, we focus on the first approach.

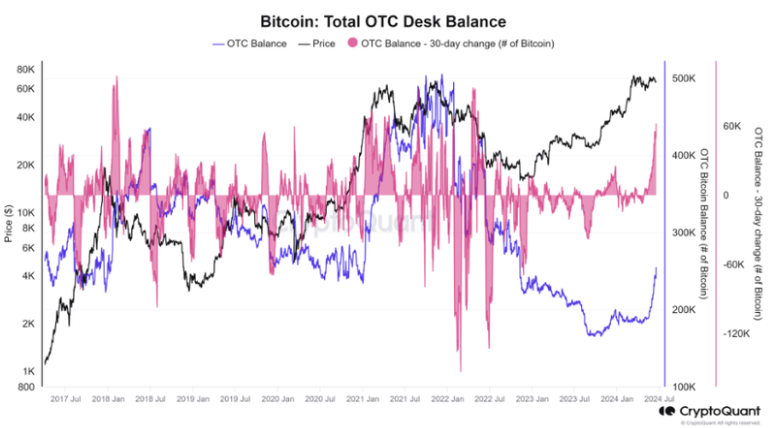

In promoting institutional participation, over-the-counter (OTC) trading is an indispensable—yet often overlooked—channel. Taking Bitcoin as a single asset globally, according to CryptoQuant, OTC desks hold daily balances fluctuating between 100,000 and 500,000 BTC (worth approximately $6.5 billion to $32.5 billion at a BTC price of around $65,000). In contrast, the average daily inflow into Bitcoin ETFs is about $122 million (Farside Invest data, as of July 5, UTC+8), amounting to merely a fraction—tens to hundreds of times smaller—than OTC volumes.

Source: CryptoQuant

However, OTC in the crypto context differs somewhat from what many assume. Commonly, OTC refers to the bridge between fiat and cryptocurrencies—this was especially true before compliant channels like ETFs emerged, making OTC the primary access point for retail users. Yet, from a broader financial market perspective, OTC serves two other critical functions—facilitating large-scale trades and providing liquidity and market stability—that remain underdeveloped in crypto.

Source: OKG Research

On the institutional front, RWA (Real-World Assets) is another frequently discussed solution. However, the author believes that RWA can only improve liquidity if it genuinely adopts crypto assets as the accounting unit and is issued on public blockchains, rather than remaining confined to consortium or private chains. Currently, most RWA initiatives are limited to enterprise consortium chains or inter-institutional financial networks. For example, Hedera’s collaboration with BlackRock in April to tokenize money market funds (MMFs) used a partially decentralized blockchain solution.

As the Web3 landscape continues to evolve, we witness internal transformation. The crypto market is shifting from a niche避险 market to one highly responsive to economic dynamics. Bitcoin has transitioned from “digital gold” to an “amplifier” of U.S. equity markets like the Nasdaq. To address recent liquidity challenges in the crypto market, a multi-pronged strategy is essential—not only adapting to macroeconomic cycles but also recognizing and developing previously overlooked areas to inject fresh vitality and enhance market stability and maturity.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News