Contract Gambling Guide: How Do Bookmakers Manipulate Prices to Ultimately Reap Retail Traders?

TechFlow Selected TechFlow Selected

Contract Gambling Guide: How Do Bookmakers Manipulate Prices to Ultimately Reap Retail Traders?

Finally figured out how the losses happened.

Author: OwenJin12

This article is not targeting $P**** specifically; I simply picked a project with clearly abnormal secondary market data to make the argument more convenient.

This article discusses a common strategy used to manipulate spot and futures prices—potentially executed by the project team's market cap management group, professional market makers, or large speculative capital. For simplicity, we’ll use the commonly accepted term “whales” throughout this article.

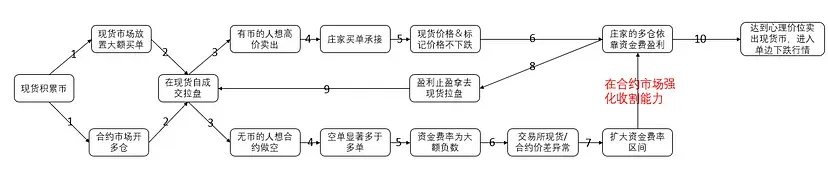

1. Brief Overview First

2. Observations

Have you often seen the following unreasonable situations on exchanges?

Phenomenon 1: Low on-chain and spot trading volume, but high futures volume

Take Gate as an example: futures trading volume is about 60 times that of spot.

Phenomenon 2: Price rises while trading volume gradually declines?

The price keeps rising, yet trading volume decreases, and MACD shows clear bearish divergence.

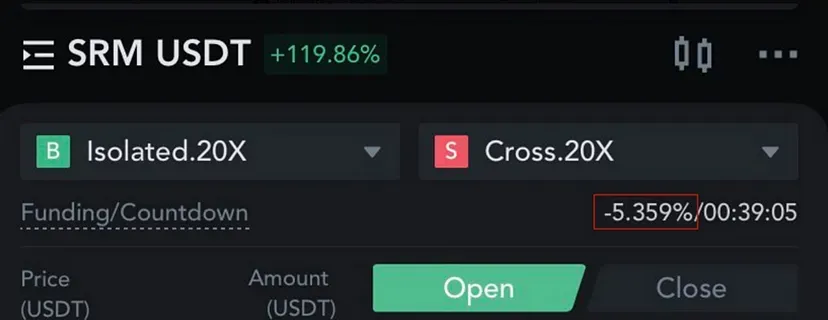

Phenomenon 3: Opposite long/short ratios between spot and futures markets, resulting in negative funding rates

High prices lead users to collectively expect a drop, but they don’t hold the coin—so they can only short via futures. This creates completely opposite market sentiments between spot and futures markets.

This contradiction leads to a funding rate of -0.66%, settled every 8 hours, amounting to -1.98% over 24 hours.

For example, trading derivatives (futures) is like buying/selling real estate. I am a property developer whose properties mainly serve wealthy buyer A, who purchases all units in my development. Pricing power lies solely between me and A—we are the only two parties influencing supply and demand for the property.

B, although not an owner, believes the property is overvalued and bets 1 million that A’s investment will fail. B is unlikely to succeed because the circulating price is controlled by me and A. Transactions between us directly affect the market price. If we agree on a transaction price, B is bound to lose. B’s bet against A resembles derivative trading, which does not impact the spot market price.

Even if B thinks the property is worth only $1/sq ft, this opinion cannot materialize because B isn't engaging in spot trading but in derivatives. Derivatives bet on spot prices, so those controlling spot prices (me and A) largely determine outcomes in derivatives trading.

In this analogy, the developer is the project team, A is the “whale” controlling circulating supply (and potentially spot prices), and B represents futures traders.

This is why naked short selling in derivatives markets is widely considered extremely risky.

3. Essential Futures Knowledge

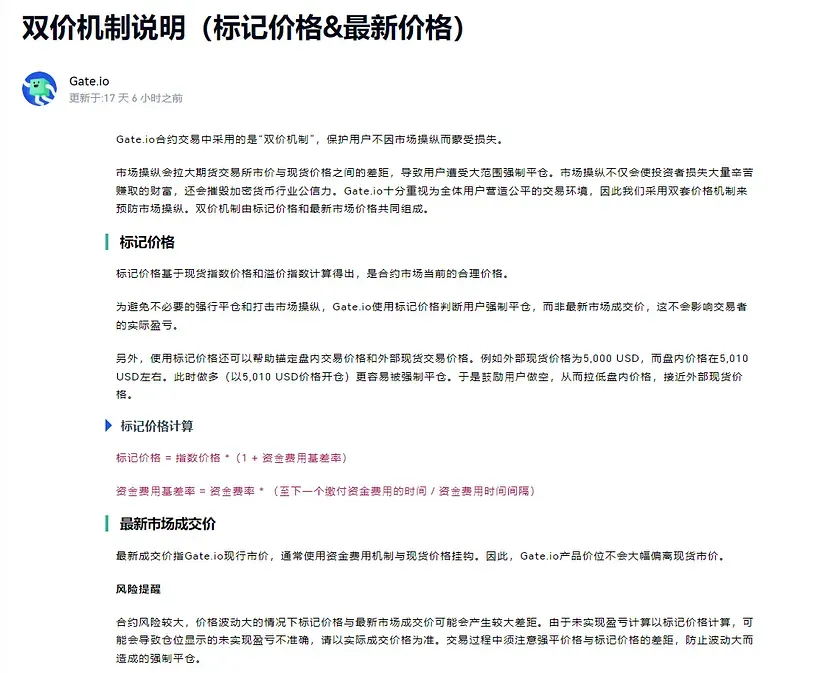

Knowledge Point 1: What are mark price and last traded price in futures?

A futures contract has two prices: last traded price and mark price. Users typically trade based on the last traded price. However, liquidations use the mark price, which is algorithmically calculated using spot prices from external exchanges to objectively reflect fair value.

Gate's explanation of futures mark price:

https://www.gate.io/help/futures/futures_logic/22067/instructions-of-dual-price-mechanism-mark-price-last-price

In other words, whoever controls the spot price controls the mark price, and thus determines whether liquidations occur in the futures market.

Knowledge Point 2: What is funding rate?

To prevent futures prices from drifting too far from spot prices, funding fees are exchanged every 8 hours—from long positions to short positions, or vice versa—narrowing the gap between spot and futures prices.

Knowledge Point 3: What is a project’s circulating market cap?

A project’s economic model depends on its whitepaper. It usually includes allocations for the team, early investors, community airdrops, treasury, etc. The less transparent the whitepaper, the higher the risk of manipulation. For instance, even if the whitepaper grants freedom to the community, it may also give market makers/institutional whales enough leeway to acquire cheap tokens at low prices—tokens that cannot be diluted later due to lack of inflation or linear vesting mechanisms.

4. Process of Controlling Small-Cap Futures

Step 1: Find a low-circulating-market-cap project with futures listed on CEX

Typically choose small projects with circulating caps between $1M–$10M, with futures leverage around 20–30x.

Step 2: Raise capital > circulating market cap

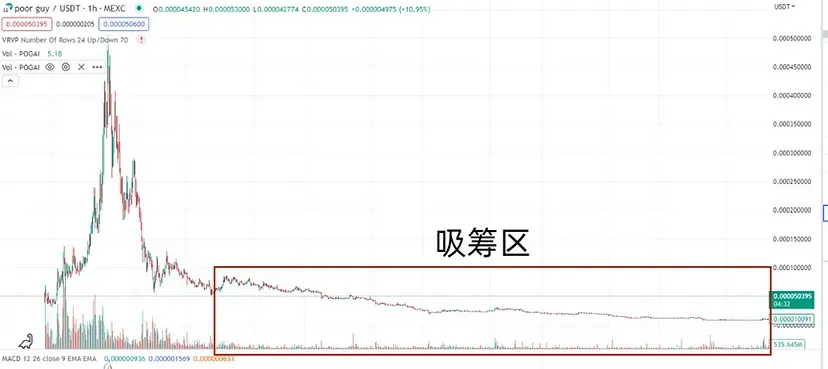

Large-scale speculative players love manipulating small-cap futures. Take $P**** as an example, with a $5M circulating cap. After accumulating 60% of circulating supply during a prolonged downtrend, a whale needs only $2M USDT and 3M coins held idle to fully control both spot and futures prices.

Step 3: Control spot order book price

As long as the 3M coins aren’t sold, the maximum sell orders on spot would be $2M. To maintain the price, the “whale” must prepare $2M USDT as support capital.

Clearly, even if all external $P**** were dumped simultaneously, the price wouldn’t fall.

Step 4: Control futures mark price

As mentioned earlier, futures mark price derives from spot prices across exchanges—meaning the mark price remains fixed once spot is controlled.

Step 5: Open long futures positions

Once mark price is secured, deploy own capital to open leveraged long positions. Conservative? Use lower leverage. Aggressive? Use higher—doesn’t matter, since mark price is locked. The whale’s longs will never get liquidated.

Step 6: Pump with capital or self-trade via sub-accounts

For shallow, low-cap coins, pumping 100% in a day requires minimal capital. If price doesn’t rise organically, create a sell order at +100% via a sub-account. Once filled, the coin will show +100% gain in 24H.

Seeing this, retail traders rush in, generating massive shorting demand.

Step 7: Earn steadily from funding rates

At this point, spot order books have few sell orders, but futures shorts are numerous—causing spot price to exceed futures price, leading to negative funding rates. The wider the gap, the higher the negative rate. Even if mark price stays flat, shorts must pay hefty funding fees to longs every 8 hours.

Under this mechanism, whales profit continuously from funding fees. In extreme cases, holding SRM long could yield 16% daily without moving a finger.

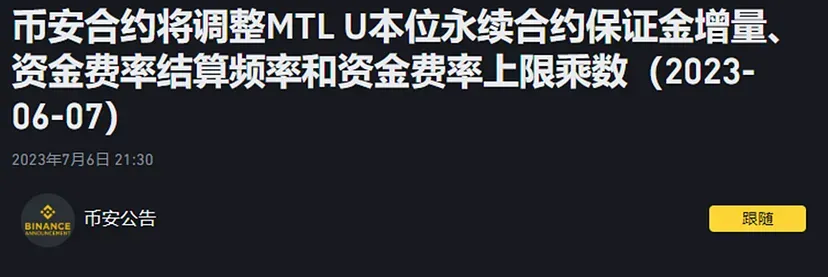

Notably, exchanges frequently adjust funding rate caps trying to narrow spot-futures gaps. But they miss the root cause. Expanding rate ranges doesn’t solve the issue—it actually empowers project teams/market makers/institutional whales to harvest retail via funding fees.

Adjustment of LINA funding rate

Adjustment of MTL funding rate

You may notice LINA and MTL were recent pump-and-dump coins with deeply negative funding rates.

5. How Whales Profit

First profit source: Buy low, sell high on spot.

Remember: Whales aren’t charities. Coins bought aren’t gold or BTC—they must eventually be sold for profit. Every pump exists only to enable a future dump.

Second profit source: Funding rate income.

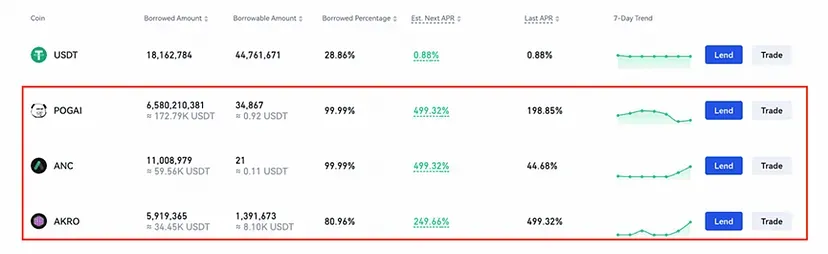

Third profit source: Pledge idle coins into leveraged lending markets. On Gate, for example, users can earn over 499% APY via Margin Savings.

After reviewing the process, one key prerequisite emerges: control over circulating supply. Coins with linear unlock schedules cannot be manipulated long-term, as each unlock changes circulation.

6. Where’s the Problem?

Problem 1: Can futures open interest (OI) exceed spot circulating market cap?

Futures only require USDT to open positions, while spot selling requires actual coins. Creating sell pressure on spot vs. opening shorts on futures differ greatly in difficulty.

Back to Step 3 in Section 3: the whale has already hoarded the coins. Even if users believe the coin is severely overvalued, they can’t create sell pressure on spot. They turn instead to futures shorting. Thus, user sentiment, constrained by low liquidity, cannot express itself in spot markets and spills into futures.

Return to mark price in Section 2: it’s based on spot trades, already controlled by the project team/market makers/institutional whales. Hence, liquidation conditions are also under control.

Therefore, when futures OI > spot circulating market cap, it indicates that coin scarcity prevents true price discovery. Excess OI amplifies spot-futures basis deviation.

Problem 2: When funding rates are abnormal, does expanding their upper/lower limits really promote fairness?

Current exchange solutions involve widening funding rate bands. While this appears to reduce spot-futures price gaps, it actually enhances the ability of project teams/market makers/institutional whales to harvest retail. Most exchanges now cap funding rates at [-2%, +2%]. Further expansion only increases “whale” profits.

Thus, while current funding rate mechanisms anchor derivatives to spot prices, they do not ensure market fairness—and may even exacerbate unfairness.

7. How Retail Traders Can Avoid Risk

Warning 1: Beware of small-cap projects with high-leverage futures—this gives whales an unfair advantage over retail

When users follow by buying spot or going long on futures, they become the buyers enabling whales to offload inventory and harvest retail again.

Warning 2: Projects with high absolute funding rates

Warning 3: Whales don’t do charity—the cost of pumping must be recovered through dumping

Exit early and avoid becoming the whale’s bagholder. When you start thinking, “This is a valuable coin—I’ll hold it until the next bull run,” the whale’s dump is likely imminent. That mindset is exactly what the whale wants to cultivate—to find someone willing to take their bags.

In small-cap futures markets, betting against whales is like playing Texas Hold’em with them seeing your cards—while they’re also the dealer.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News