Mt. Gox's Repayment Plan Worth up to $9 Billion Could Trigger Market Downturn, But Selling Pressure Might Be Overestimated

TechFlow Selected TechFlow Selected

Mt. Gox's Repayment Plan Worth up to $9 Billion Could Trigger Market Downturn, But Selling Pressure Might Be Overestimated

Although Mt. Gox may exert certain pressure on the market, its selling pressure could be overestimated by the market.

By Nancy, PANews

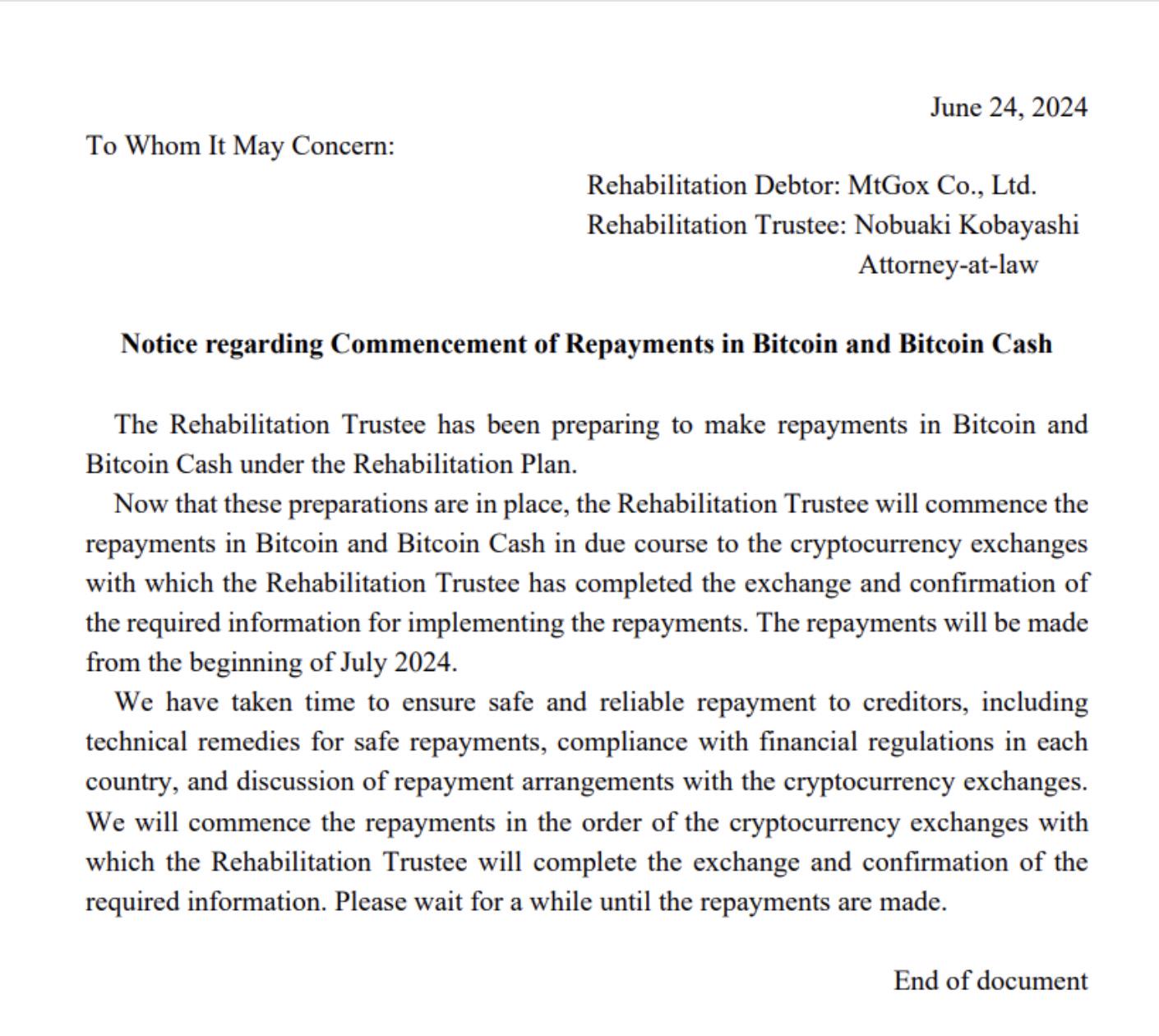

Mt.Gox drags down the market again. On June 24, the Mt.Gox trustee announced that BTC and BCH repayments would begin in July this year, involving crypto assets worth as high as $9 billion. Affected by this news, the cryptocurrency market plunged, with Bitcoin briefly falling below the $60,000 mark.

BTC and BCH Repayments to Start in July; Trustee Determines Payout Order

Official documents indicate that the Mt.Gox trustee has completed preparations and will initiate repayment procedures to cryptocurrency exchanges—including Kraken, Bitstamp, and BitGo—per the rehabilitation plan. The trustee has already confirmed and exchanged necessary information with these exchanges to ensure security and compliance. Mt.Gox has a total of 127,000 creditors (less than 1% from Japan) and must repay 142,000 BTC (currently valued at approximately $8.58 billion) and 143,000 BCH (worth about $53.31 million).

At the end of last month, Mt.Gox began preparing for repayments ahead of the October 31 creditor deadline. Its wallet saw its first movement in five years, redistributing its Bitcoin holdings equally across three new addresses—each containing 47,230 BTC.

However, Mt.Gox will not repay all assets at once. As previously reported by PANews, the repayment scheme includes both base compensation and proportional compensation. The base payment allows each creditor to claim up to 200,000 JPY in Japanese yen. For amounts exceeding this threshold, creditors have two flexible options: an “early lump-sum repayment” or “interim and final repayments.” Under the early lump-sum option, creditors receive only partial compensation, with the excess over 200,000 JPY payable either in a mix of BTC, BCH, and JPY or entirely in fiat currency. Mt.Gox has set the deadline for base, early lump-sum, and interim payments as October 31, 2024. However, creditors seeking higher recovery rates may still need to wait five to nine more years.

By the end of 2023, several Mt.Gox creditors had already received initial compensation in Japanese yen. This upcoming payout marks the first time Mt.Gox will repay in BTC and BCH.

It should be noted that actual disbursements will follow the order in which individual exchanges complete information verification and exchange procedures. This means creditors will receive payouts at different times. According to prior disclosures, BitGo may require up to 20 days for payment processing, while Kraken and Bitstamp could take up to 90 days.

Approximately 95,000 Bitcoins Expected to Be Paid Early; Large Creditors Optimistic About Market Outlook

For an already liquidity-constrained crypto market, the imminent Mt.Gox repayment plan is undoubtedly a major blow. As Bloomberg senior ETF analyst Eric Balchunas commented, if all Mt.Gox bitcoins were dumped into the market, it would offset more than half of the inflows seen in Bitcoin ETFs.

Amid growing fears of massive selling pressure, Bitcoin’s price briefly dropped below $60,000, hitting its lowest level since May. Data from CoinGlass shows that liquidations across the market reached $357 million in the past 24 hours, including $175 million in Bitcoin positions. However, according to multiple institutions and large creditors, the actual selling pressure from Mt.Gox may be less severe than anticipated.

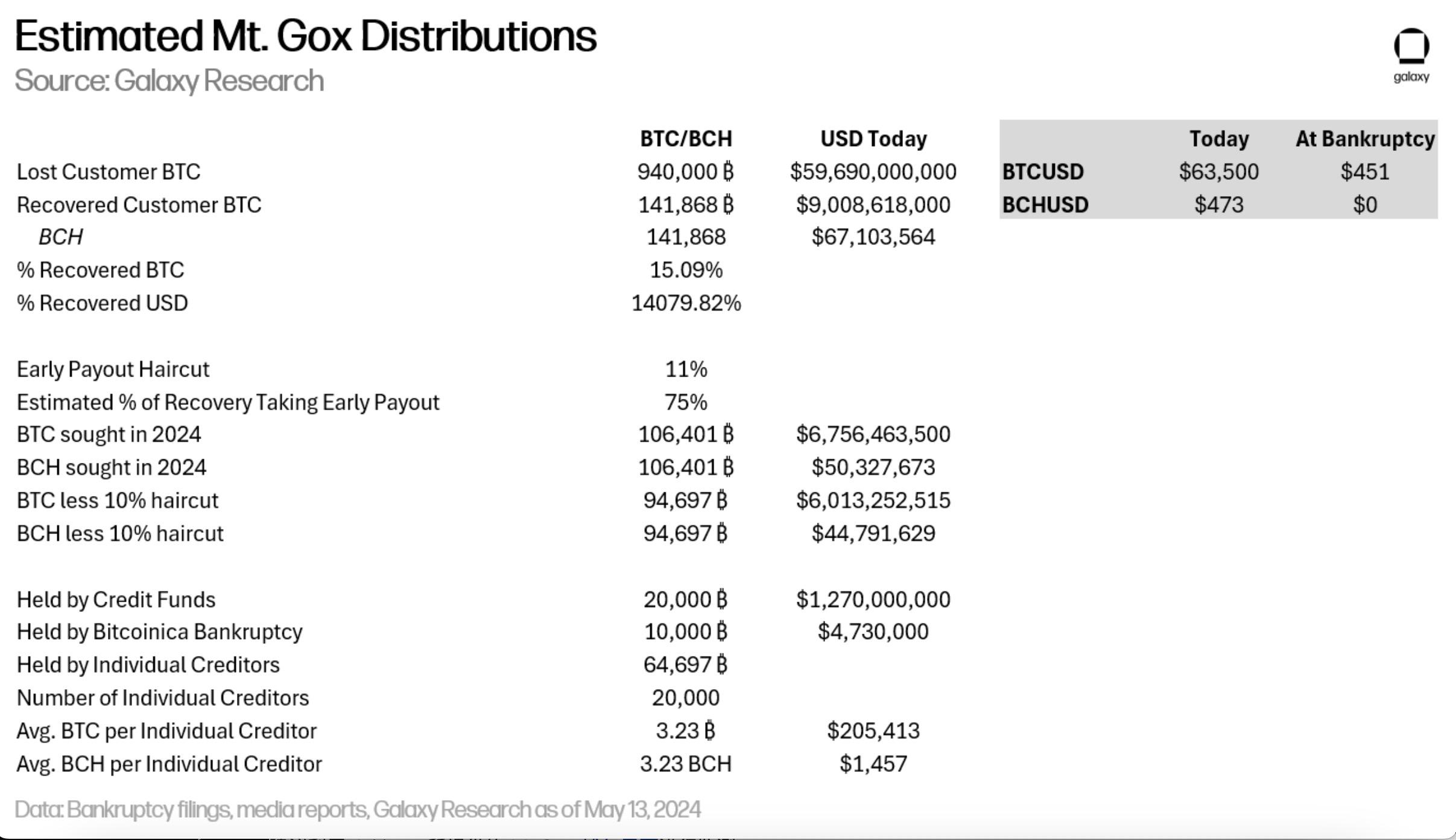

For example, Alex Thorn, head of research at Galaxy Digital, stated on X today that the number of tokens distributed by Mt.Gox is expected to be lower than market expectations. Specifically, Mt.Gox lost around 940,000 BTC but successfully recovered 141,868 BTC (then worth about $63.9 million), now valued at $9 billion. Although the recovery rate was only 15%, this represents a 140x increase in dollar value for creditors. To qualify for early payment, creditors must accept around a 10% reduction. It's estimated that approximately 95,000 BTC will be used for early payouts: about 20,000 BTC belong to claims funds, 10,000 BTC to the Bitcoinica bankruptcy case, and the remaining 65,000 BTC go to individual creditors—a figure significantly lower than the often-cited 141,868 BTC.

In fact, based on creditor claim data compiled earlier by Nobuaki Kobayashi, the Mt.Gox bankruptcy trustee, 226 claimants collectively hold over 50% of total claims and are set to receive 84,650 BTC.

“The potential sell-off pressure from Mt.Gox on Bitcoin may be overstated. Creditors who urgently needed cash had ten years to sell their claims. Those who still hold them now clearly aren’t in a rush to dump their Bitcoin,” said Alistair Milne, CIO of Altana Digital Currency Fund. According to Bloomberg, large creditors and long-term market participants do not believe Bitcoin prices will suffer lasting damage. Many plan either to hold onto the tokens or gradually sell them, betting that prices will continue rising.

For instance, Adam Back, CEO of Blockstream Corp., said selling Bitcoin at the start of a bull market would be an odd timing decision, indicating his intention to retain any allocated Bitcoin. Brian Dixon, CEO of Off the Chain Capital, a major investor who has acquired Mt.Gox claims over many years, said he would consider selling only if better investment opportunities arise. “The Bitcoin market has matured significantly. Creditors must ask themselves whether they need the money for immediate use or whether holding Bitcoin as long-term value storage makes more sense—especially given that Bitcoin has been the top-performing asset over the past 15 years. So I don't expect long-term price damage, though there might be some short-term volatility.”

Alex Thorn also believes the selling pressure on Bitcoin will be limited because individual creditors are predominantly long-term holders and technically savvy early adopters. “They’ve resisted attractive offers from claims funds for years, showing they prefer recovering their Bitcoin rather than accepting dollar settlements. Considering capital gains implications, even a 15% physical recovery delivers substantial returns for claimants since the bankruptcy. Still, if just 10% of the 65,000 BTC held by individuals are sold, that’s 6,500 BTC entering the market—which will likely happen through normal trading activity. Creditors will receive these coins and probably deposit them directly into accounts on Kraken, Bitstamp, or Bitgo, most likely choosing trading accounts. As for claims funds, conversations with some reveal they’re primarily composed of high-net-worth Bitcoin investors seeking discounted BTC exposure, not arbitrage-focused credit funds. While some LPs may choose to sell, overall these funds aren’t dominated by traders looking to flip positions.”

In contrast, BCH may face greater price pressure and underperform during the upcoming distribution. Alex Thorn notes that first, no creditors originally bought BCH; second, BCH liquidity is far lower than BTC, especially on Kraken and Bitstamp—the two exchanges where creditors will receive the tokens. Therefore, once distributed, BCH is likely to underperform relative to BTC, as creditors are more inclined to sell BCH in a less liquid market. For example, Thomas Braziel, partner at 507 Capital, which has been acquiring Mt.Gox bankruptcy claims since 2015, said he might sell his BCH but plans to keep his Bitcoin, hoping for further appreciation—and expects most other creditors to do the same.

Considering the staggered payout methods, distribution patterns of repaid Bitcoin, and statements from major creditors, while Mt.Gox may exert some pressure on the market, its actual impact may be exaggerated by market sentiment.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News