IRS 1099-DA Preview: Who Will File, and What Regulatory Message Does It Send?

TechFlow Selected TechFlow Selected

IRS 1099-DA Preview: Who Will File, and What Regulatory Message Does It Send?

This is a new tax form that cryptocurrency brokers will begin using next year to report digital asset transactions.

Author: Jason Bramwell

Translation: TaxDAO

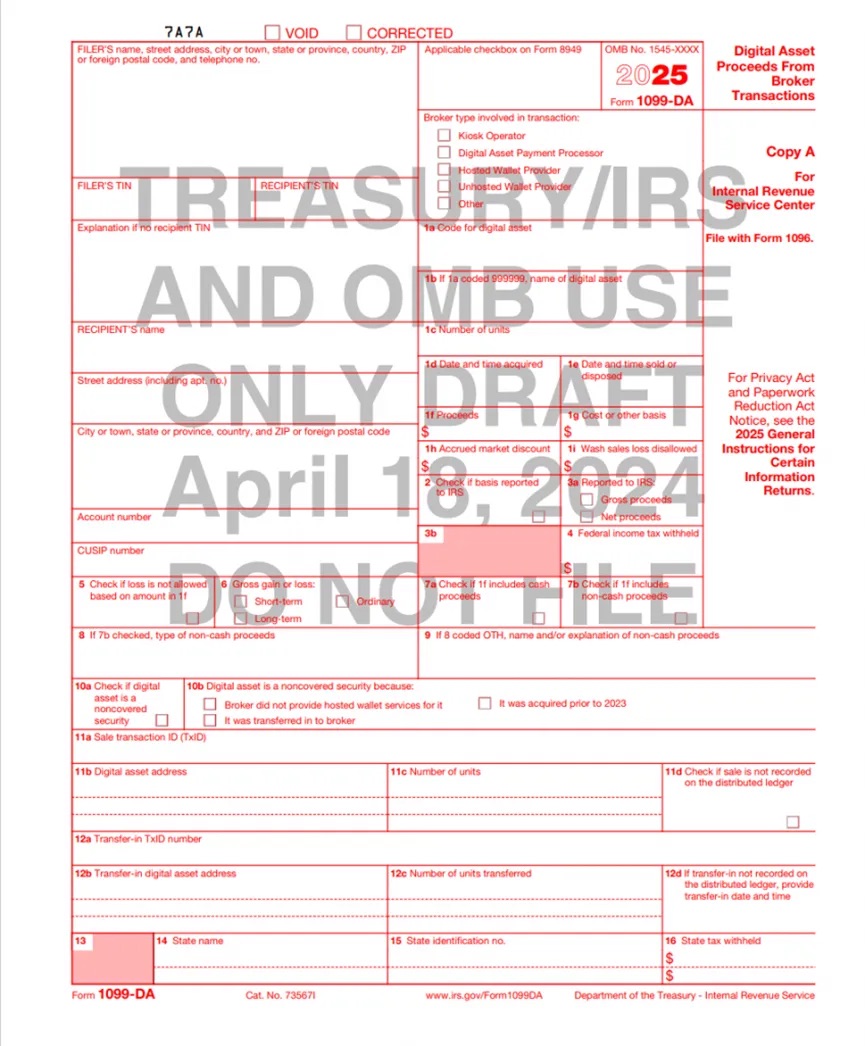

The Internal Revenue Service (IRS) released the long-awaited draft of Form 1099-DA on its website in April—a new tax form that cryptocurrency brokers will begin using next year to report digital asset transactions.

Last August, the tax agency issued proposed regulations requiring brokers to report customers’ sales and trades of digital assets, previewing the upcoming tax form.

“These proposed regulations aim to end confusion in the digital asset space and provide clarity and reporting certainty for taxpayers, tax professionals, and others,” IRS Commissioner Danny Werfel said in a statement on August 25, 2023. “A key part of this effort aligns with the IRS’s greater compliance focus on high-income taxpayers. We need to ensure digital assets aren’t being used to hide taxable income, and the proposed regulations are designed to bring greater clarity to the activities of high-income individuals as well as others using digital assets. We want to make sure everyone pays what they owe under the tax law, and our research and experience show that third-party reporting increases compliance.”

Brokers—defined by the IRS as “digital asset trading platforms, digital asset payment processors, and certain digital asset custodial wallets”—will be required to generate a Form 1099-DA for each sale transaction starting January 1, 2025, and submit the information to both the IRS and their customers.

For digital asset sales or exchanges occurring on or after January 1, 2025, the proposed regulations will require brokers to report gross proceeds on Form 1099-DA and provide customers with statements for tax filing purposes. The IRS stated last August, “In certain cases, brokers will also need to include gain or loss and basis information for sales occurring on or after January 1, 2026, in these information returns so customers have the necessary data for tax reporting.”

Shehan Chandrasekera, CPA and head of tax strategy at CoinTracker, said the draft Form 1099-DA captures some unsurprising data points—such as acquisition date, disposal date, proceeds, and cost basis of disposed crypto assets—which are essential and helpful for taxpayers completing crypto tax filings.

The IRS has also included “non-custodial wallet providers” as an option on the form, further indicating its intent—despite widespread concerns in the crypto industry—to include non-custodial wallets within the definition of brokers.

“What does this mean for you? Going forward, you may be required to provide KYC (Know Your Customer) information before creating a non-custodial wallet and/or when interacting with platforms through such a wallet,” Chandrasekera wrote on X. “This could drastically change how users interact with crypto platforms. It will change decentralized finance as we know it today.”

Jessalyn Dean, vice president of tax information reporting at Ledgible, shared her initial impressions of the draft Form 1099-DA on LinkedIn after reviewing it:

-

They’ve packed a lot of options into this form.

-

As expected, it closely resembles Form 1099-B, which reports sales of traditional financial products like stocks.

-

Most options align with expectations and match the required information listed in the proposed regulations from August 2023.

-

Box 1i includes “wash sale loss disallowed,” but this does not mean cryptocurrencies are subject to wash sale rules. It’s included because these digital assets may also be stocks or securities already subject to wash sale rules (e.g., certain tokenized stocks).

-

Box 11d is intended to indicate sales not recorded on a distributed ledger. This is necessary because transactions occur within internal recordkeeping systems and thus typically lack digital asset addresses or transaction IDs.

-

Box 5 allows brokers to note that losses due to a “reportable change in control or capital structure” are not deductible, referencing instructions for Form 8949 and Schedule D. However, no guidance is provided on which events in crypto and digital assets might qualify. Brokers are left to figure it out on their own, with the added instruction: “The broker should inform you of any such losses in a separate statement.”

The IRS noted that this early draft of the form may be revised based on public comments received regarding the proposed regulations issued last August. The public can submit feedback on the draft or final forms, instructions, or publications to the IRS via IRS.gov/FormsComments. The agency requests that commenters include “NTF” followed by the form or publication number (e.g., “NTF1099-DA”) in the body of the email to ensure proper handling.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News