Comprehensive Overview of Singapore's Payment Services Regulatory Framework and Virtual Asset DPT License Requirements

TechFlow Selected TechFlow Selected

Comprehensive Overview of Singapore's Payment Services Regulatory Framework and Virtual Asset DPT License Requirements

In Singapore, regulation of the payment industry is crucial to ensure compliance and prevent illegal activities.

Author: Aiying Aiying

In Singapore, regulation of the payments industry is crucial to ensure compliance and prevent illegal activities. The key regulatory bodies include:

The Monetary Authority of Singapore (MAS) is the primary regulator—equivalent to China’s "One Bank and Three Commissions"—responsible for overseeing financial institutions and companies holding Financial Services Licenses, as well as quasi-financial entities such as those involved in wealth management and credit rating. In addition to MAS, the Singapore Clearing House Association (SCHA) and the Association of Banks in Singapore (ABS) also participate in regulating the payments industry.

I. Evolution of the Payment Regulatory Framework

1. Early Regulatory Framework

Prior to 2006, regulations governing Singapore’s payment system were scattered across the Banking Act, Bills of Exchange Act, and various informal documents.

2. Money-changing and Remittance Business Act (MCRBA)

Enacted in 1979, the MCRBA established licensing and other regulatory requirements for businesses engaged in remittance services.

3. Payment Systems (Oversight) Act (PS(O)A)

In 2006, MAS introduced the PS(O)A, which provided a unified legal foundation for payment system oversight.

4. Legal Consolidation and Update – The Payment Services Act 2019

With innovations in payment technologies, the existing legal framework gradually became inadequate for emerging payment tools and business models. As a result, Singapore undertook a legal overhaul: it repealed the PS(O)A and MCRBA and enacted the new Payment Services Act 2019 (PSA), effective in 2020. This consolidated prior legislation and, after revisions in early 2020, incorporated new digital payment services. Of particular relevance to virtual assets are the regulations concerning e-money and Digital Payment Tokens (DPTs).

II. Regulatory Framework Under the New Act

1. Classification of Payment Services

Under the new legal framework, payment services are divided into two main categories:

-

Payment Service Providers

Providers offering services such as merchant acquiring, remittances, and account issuance are the focus of our discussion below.

-

Payment Systems

Payment systems, analogous to China’s clearing infrastructure (e.g., UnionPay, NetUnion), serve as foundational financial infrastructure enabling fund transfers among participants.

2. Key Regulatory Focus: Payment Service Providers

Given that payment systems primarily involve financial infrastructure and have limited direct interaction with consumers and merchants, the following discussion will focus on the regulation of payment service providers.

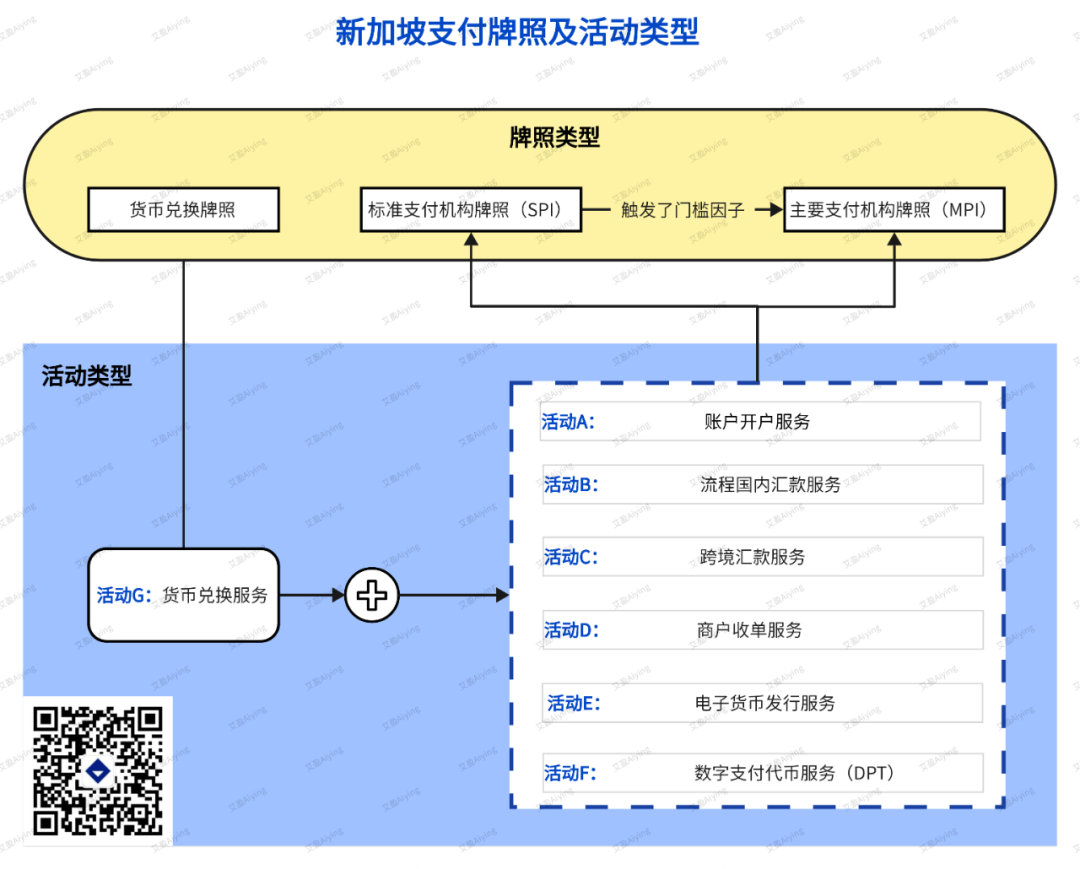

There are three types of licenses applicable to payment service providers:

-

Money-Changing Licence

-

Standard Payment Institution Licence (SPI)

-

Major Payment Institution Licence (MPI)

Singapore further breaks down these three license types into seven distinct activities, as illustrated below:

(Detailed activity descriptions)

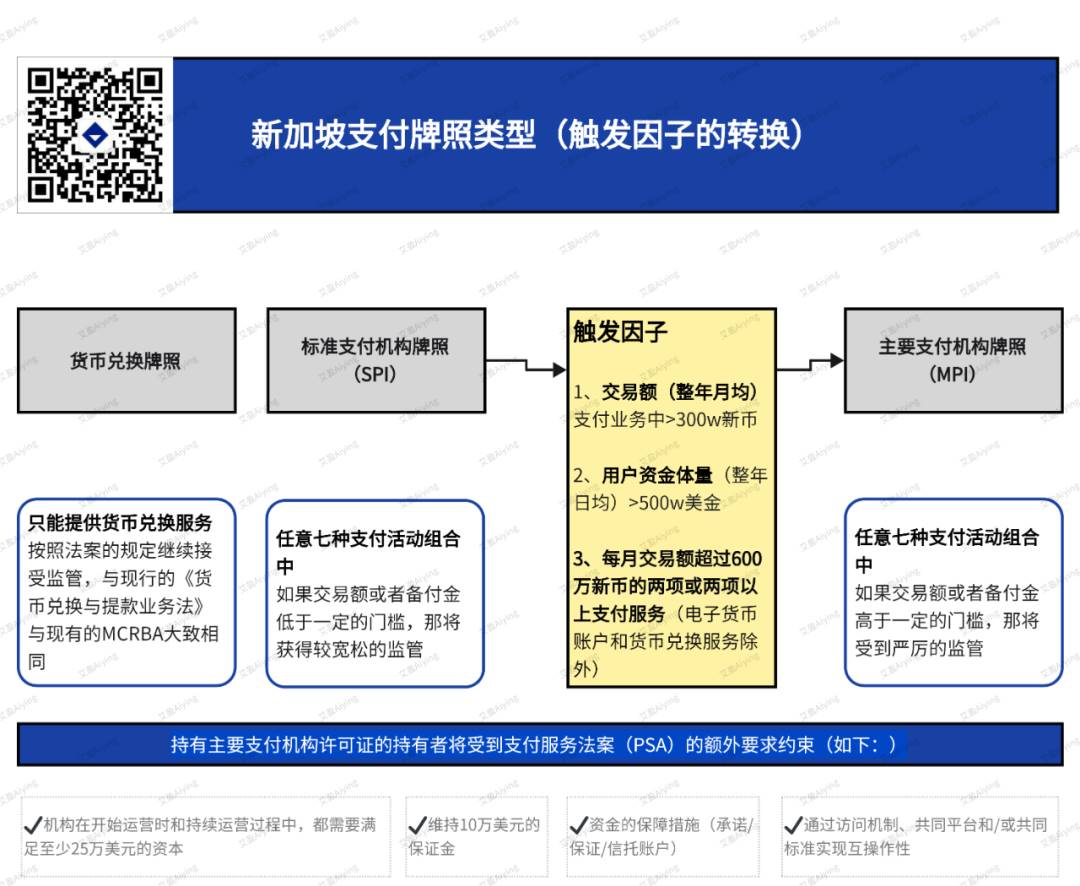

For example, if you apply for an SPI or MPI license, you may declare multiple activities during the application—i.e., the specific services you intend to offer, such as merchant acquiring, wallet services, money changing, or cryptocurrency operations. You can apply for all relevant activities, but regulators will only approve those deemed reasonable, necessary, and for which you meet eligibility criteria. The chart below outlines MAS’s thresholds for determining license type:

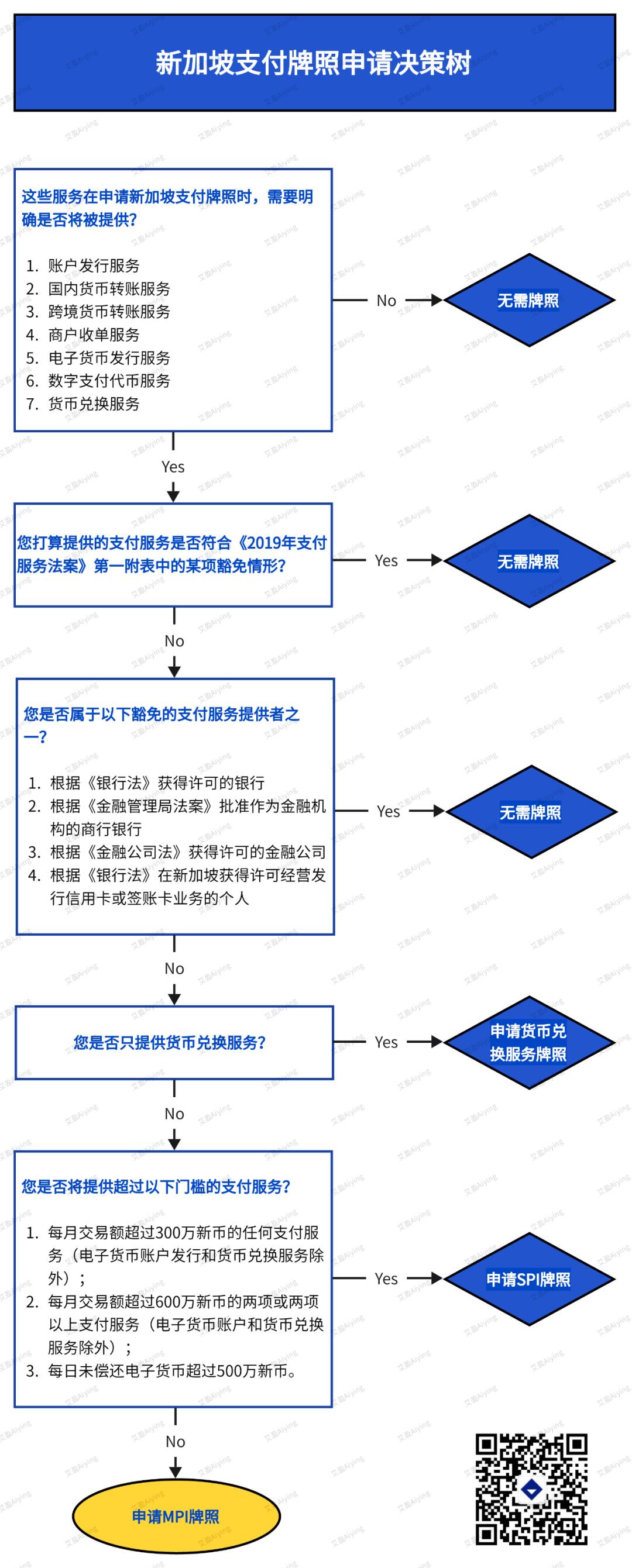

When deciding which license type to apply for based on your intended payment services, you may refer to the decision tree below:

3. DPT – Digital Payment Token Services

Among the seven activities, we now focus specifically on Activity F: Digital Payment Token Services

(1) Definition of DPT Services

(2) E-Money vs. Digital Payment Tokens (DPT)

For virtual assets with payment functionality, the first step is to determine whether they qualify as e-money or DPTs, which then determines the applicable regulatory regime.

The PSA clearly distinguishes between e-money and DPTs:

E-money: Electronically stored monetary value with the following characteristics:

-

Denominated in or pegged to fiat currency;

-

Prepaid for use in transaction payments;

-

Accepted by parties other than the issuer;

-

Represents a claim against the issuer.

Digital Payment Token (DPT): A digital representation of value, characterized by:

-

Expressed in units;

-

Not denominated in or pegged to fiat currency;

-

Recognized by the public as a medium of exchange;

-

Used as consideration for goods or services or for debt settlement;

-

Capable of electronic transfer, storage, or trading.

(3) Differences Between E-Money and DPT

MAS highlights the key differences between e-money and DPTs as follows:

-

Whether denominated in or pegged to fiat currency;

-

Whether it represents a claim against the issuer;

-

Whether its value is determined through market mechanisms.

Payment tokens such as Bitcoin and Ether are typically classified as DPTs.

(4) Stablecoins Are Also Classified as DPTs

Due to their pegging to fiat currencies, stablecoins have been subject to debate regarding classification as either e-money or DPTs. However, MAS considers that stablecoins generally do not meet the definition of e-money because:

-

E-money is an electronic form of fiat currency, whereas stablecoin exchange rates are not fixed;

-

There may be no direct contractual relationship between stablecoin holders and issuers.

Stablecoins such as USDC and Tether are treated as DPTs based on their characteristics.

MAS determines the applicable regulatory framework based on the specific features of each stablecoin. In 2022, MAS proposed draft regulatory policies for stablecoins. For instance, Paxos has received in-principle approval from MAS to issue a new U.S. dollar-pegged stablecoin through its Singapore subsidiary.

(5) Exemption for Non-Monetary Tokens

The PSA provides exemptions for certain non-monetary tokens (e.g., customer loyalty points, in-game assets), provided that they meet the following conditions:

-

Cannot be redeemed with the issuer, transferred, or sold for money;

-

Can only be used to redeem goods or services from the issuer or designated merchants;

-

Are solely for virtual items or services within online games.

III. License Application

Payment License Application Checklist and Requirements:

1. Corporate Entity and Management Requirements

Company Registration: Applicants must be either a company registered in Singapore or a local branch of a foreign company.

Management Structure:

-

At least one executive director must be a Singapore citizen or permanent resident.

-

Alternatively, at least one executive director must hold a Singapore employment pass, and at least one non-executive director must be a Singapore citizen or permanent resident.

2. Fit-and-Proper Criteria

Applicants, along with their directors, CEOs, shareholders, and employees, must meet the "Fit and Proper" criteria.

The applicant company or group must have no record of financial crimes or adverse reputation.

3. Industry Experience and Qualifications

Executive directors and CEOs must possess operational experience in the payment services or financial services industries.

Educational background and professional certifications of key personnel are important evaluation factors.

4. Local Permanent Business Office

Applicants must have a fixed business location or registered office under long-term lease.

The office must ensure privacy, secure storage of business records, and have dedicated staff available for customer inquiries.

5. Capital and Guarantee Requirements

Minimum Capital Requirements:

-

Standard Payment Institution Licence: SGD 100,000.

-

Major Payment Institution Licence: SGD 250,000.

Guarantee Amount:

-

Average monthly transaction volume less than SGD 6 million: SGD 100,000.

-

All other cases: SGD 200,000.

6. Compliance and Risk Control

Establish an independent compliance function or obtain external compliance support; implement AML/CFT policies and conduct risk assessments.

Conduct comprehensive technical testing for online financial services, including penetration testing and independent verification.

7. Audit Arrangements

Implement internal audit arrangements commensurate with the scale of operations.

Undertake annual external audits to ensure regulatory compliance.

8. Letter of Assurance / Undertaking

MAS will evaluate the applicant's financial standing, compliance risks, and public interest considerations.

9. Safeguarding Arrangements

Provide detailed safeguarding arrangements, including the name of the safeguarding institution, draft contracts, and scope of coverage.

If using insurance or bank guarantees, provide a legal opinion confirming compliance with requirements.

10. Proof of Documentation

After approval, submit proof of implemented safeguarding arrangements.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News