BTC Halving and the New Equilibrium: A Sharp Drop in Mining Revenue, Shutdown Price Reaches $55K, and Rapid Growth of Large Holders

TechFlow Selected TechFlow Selected

BTC Halving and the New Equilibrium: A Sharp Drop in Mining Revenue, Shutdown Price Reaches $55K, and Rapid Growth of Large Holders

Essentially, each halving represents another dynamic equilibrium of market supply and demand.

By Carol, PANews

Bitcoin successfully completed its fourth halving on April 20. Following this event, the block reward has been reduced to 3.125 BTC. The halving first impacts the mining industry, causing miners' income to drop sharply in the short term. Additionally, it affects Bitcoin's inflation rate, with market expectations that increased scarcity will drive prices higher. However, in reality, since the halving, Bitcoin has remained range-bound at high levels, with a slight price decline of 3.87%, putting direct pressure on miners and leaving many short-term investors facing losses.

At its core, each halving represents another round of dynamic equilibrium in market supply and demand. During this rebalancing process, what capital movements are worth watching? How severe is the pressure facing the mining sector? What is the current state of Bitcoin’s demand side? PAData, the data column of PANews, analyzed current market data, mining data, and other demand-side metrics, finding the following:

-

Since March, the proportion of unprofitable Bitcoin holdings has steadily risen from 1.28% to 15.18%. The average SOPR index for short-term holders post-halving was 0.99972, suggesting many short-term investors incurred losses due to halving-related expectations.

-

After the halving, on-chain token circulation velocity dropped by 23%, indicating more coins are being accumulated. In terms of holding periods, since the beginning of the year, there has been significant growth in holdings with durations of 1–3 months, 3–6 months, and 3–5 years. Specifically, holdings with 1–3 month durations increased by 7.14 percentage points this year, including a 2.44-point rise after the halving, reflecting a trend toward medium- to long-term accumulation. From the perspective of wallet balances, addresses holding between 100 BTC and 1,000 BTC, and especially those holding 1,000–10,000 BTC, saw increases of over 1.3% in number.

-

Post-halving, miners face significant revenue pressure. Based on current prices and high electricity costs, the shutdown price has reached $55,000—sharply up from the previous low of $14,300 in August last year.

-

Current daily mining revenue stands at approximately $26.49 million, down 51.63% from the pre-halving average of $54.76 million. Daily transaction fees are now around $2.28 million, a 34% decrease from pre-halving levels.

-

Assuming transaction fee income remains constant (at current average fee per transaction and transaction volume), reaching pre-halving daily revenue levels would require the Bitcoin price to reach $94,489.82—51.63% higher than current levels.

-

Assuming the Bitcoin price remains unchanged, achieving pre-halving daily revenue would require daily transactions to reach 1.6737 million—a 202.49% increase from post-halving averages—or an average fee per transaction of 0.00080317 BTC, up 206.08% from current levels.

-

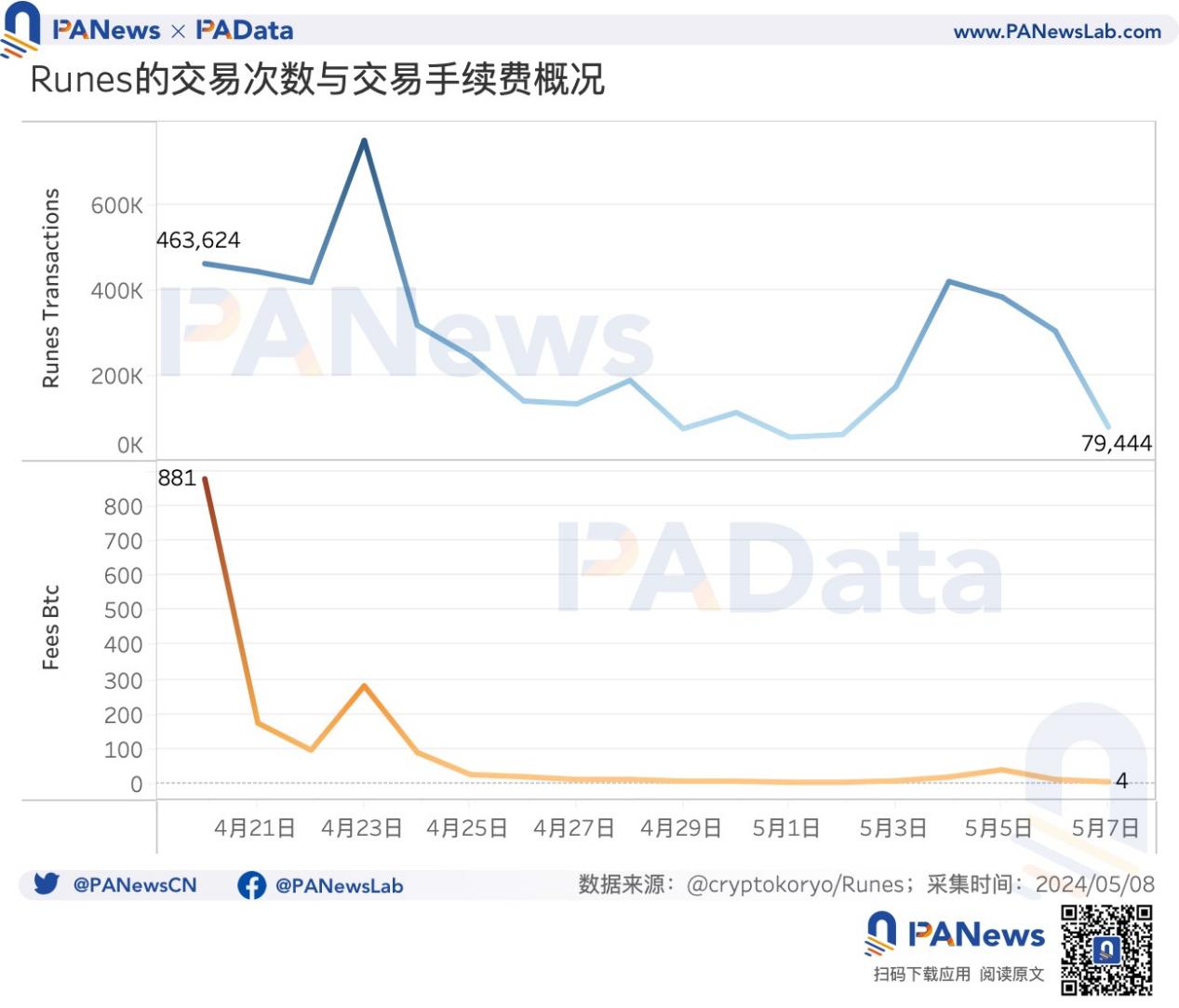

The strong initial demand from Runes brought substantial earnings for miners, contributing 881 BTC in fees on its launch day.

01. Post-Halving Unprofitable Holdings Rise to 15%; Large Holders (100+ BTC) Increase Significantly

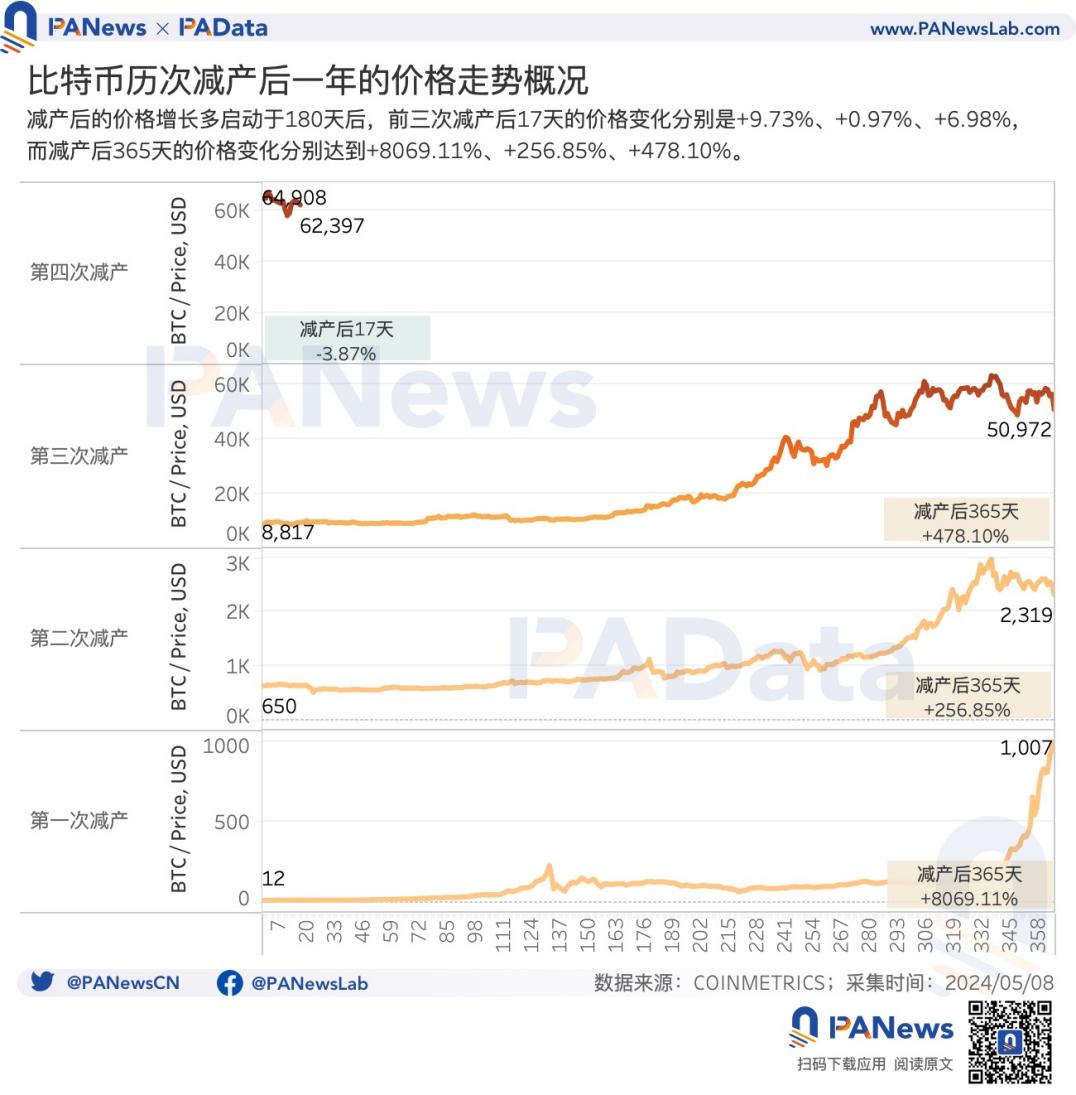

A common market expectation is that Bitcoin prices will surge significantly after a halving. Historical data supports this: in the year (365 days) following each of the past three halvings, Bitcoin prices rose by 8,069.11%, 256.85%, and 478.10%, respectively.

However, in the short term, the impact of halving on price is gradual. In the immediate 17-day period following the previous three halvings, price changes were +9.73%, +0.97%, and +6.98%. This time, however, Bitcoin has remained range-bound since the halving, currently hovering around $62,400—down approximately 3.87%.

Lower-than-expected prices have led to a noticeable rise in unprofitable holdings. Since the halving, Bitcoin has traded between $64,900 and $62,400, while the share of unprofitable coins climbed from 10.95% to 15.18%. In fact, this trend began before the halving. Since March, as prices consolidated above $62,500, the proportion of loss-making holdings has steadily increased from 1.28%, suggesting many short-term investors who bought in anticipation of a post-halving rally have already incurred losses.

The Short-Term Holder SOPR (Spent Output Profit Ratio) further supports this. An SOPR below 1 indicates that holders who owned Bitcoin for more than one hour but less than 155 days are selling at a net loss. According to CryptoQuant, the current SOPR is 1.0022—very close to 1—and the post-halving average is 0.99972, confirming that short-term investors are currently in a net-loss position overall.

Amid weak prices, on-chain coin turnover has also slowed dramatically. According to Glassnode, the current 7-day rolling average circulation velocity is 0.01044—down nearly 23% from 0.01356 on halving day and nearly 33% from the start of the year—indicating a sharp decline.

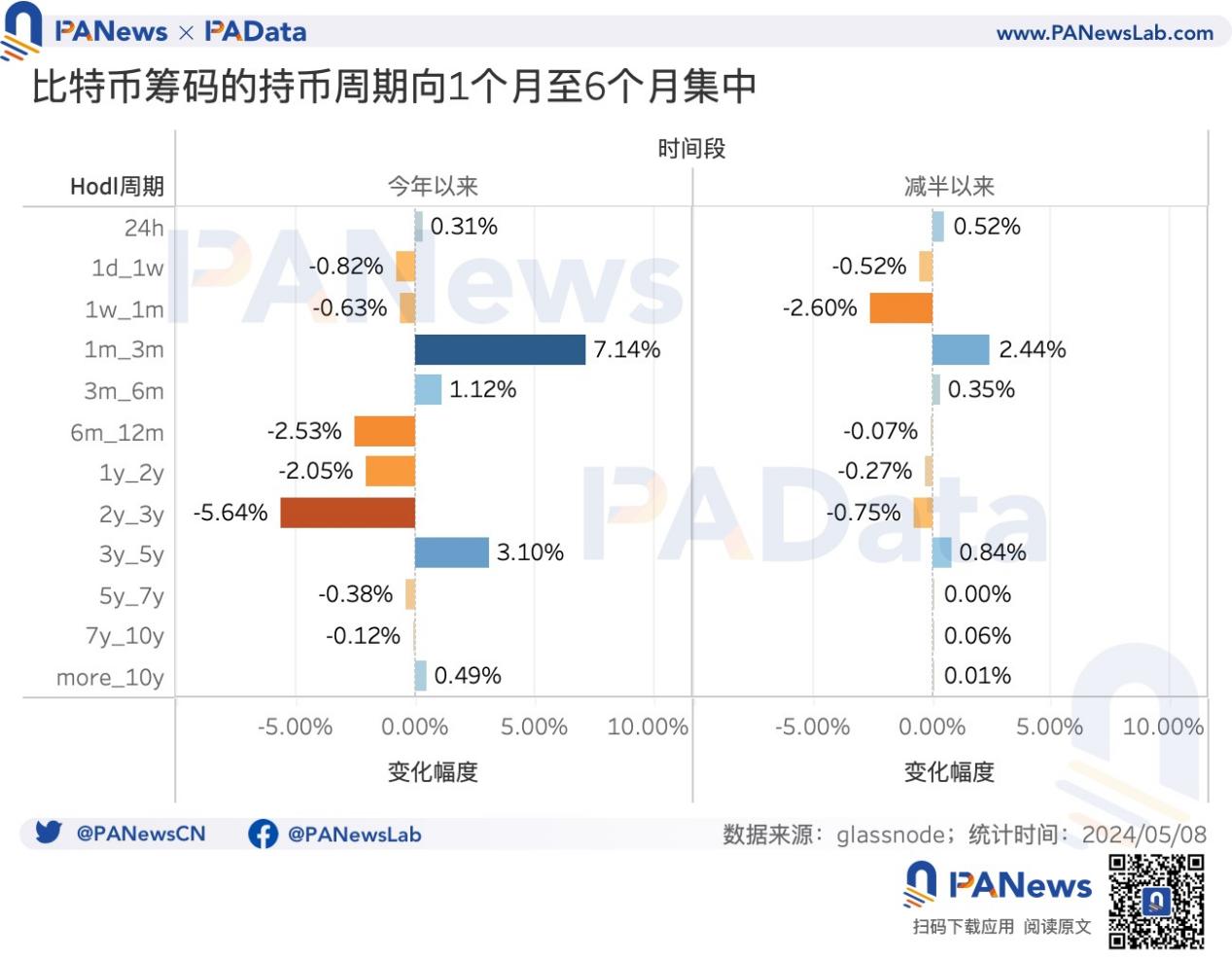

This rapid drop in circulation velocity suggests more coins are entering accumulation phases. By holding duration, since the beginning of the year, there has been clear growth in coins held for 1–3 months, 3–6 months, and 3–5 years. Notably, the share of coins held 1–3 months has increased by 7.14 percentage points this year—including 2.44 points since the halving—reflecting a shift from short-term to medium- and long-term holding patterns.

Looking at wallet balances, since the beginning of the year, among addresses categorized as "Entities" (clusters controlled by single network entities such as exchanges, foundations, whales, or miners), those holding 100–1,000 BTC and 1,000–10,000 BTC have grown significantly—by 1.35% and 1.39%, respectively—with this trend continuing after the halving. Across all addresses, the number of wallets holding 1,000–10,000 BTC increased by 1.07%. These figures indicate growing concentration among large holders and ongoing coin consolidation.

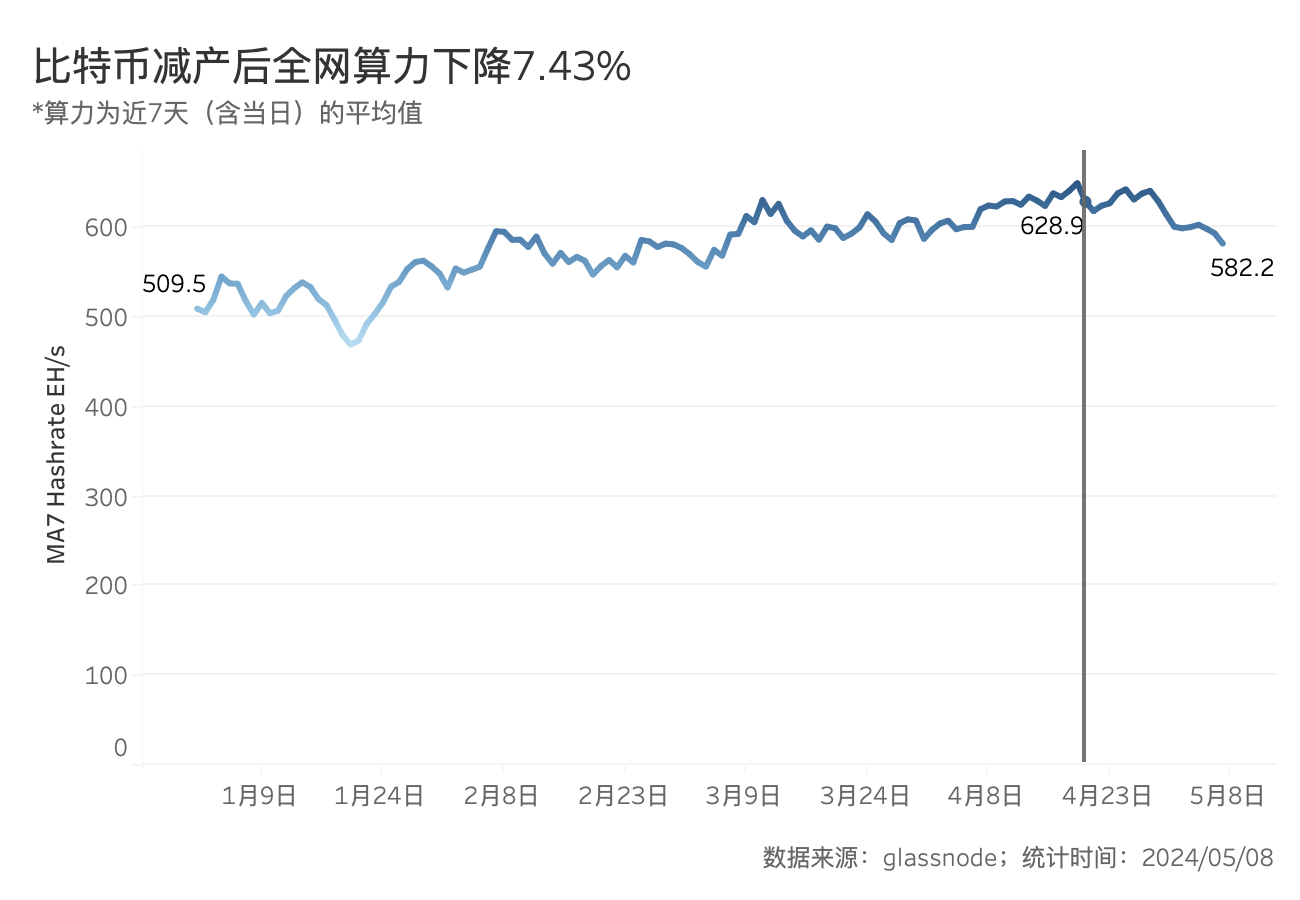

02. Post-Halving Hashrate Drops Over 7%; Daily Mining Revenue Falls to $26.49 Million

Following the Bitcoin halving, network hashrate (7-day average) declined noticeably. According to Glassnode, current hashrate is 582.2 EH/s—down 7.43% from halving day. The hashrate drop exceeds the price decline, suggesting miners have shut down some equipment to maintain profitability.

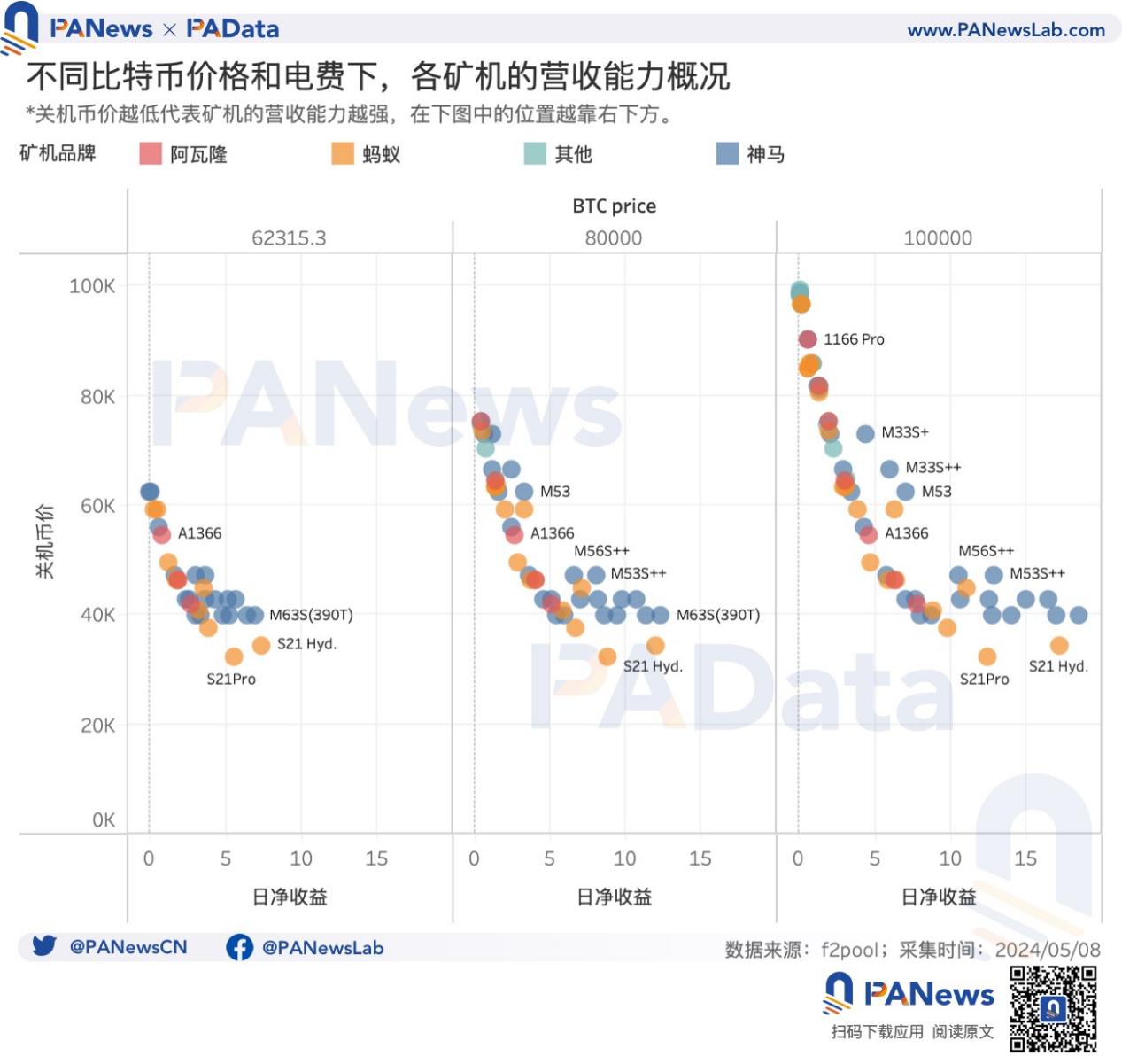

According to f2pool data, miners now face significant revenue pressure based on current shutdown prices. Using the collection-day price of $62,315.29, if miners operate in low-cost electricity regions (assumed at $0.07/kWh), only 31 miner models remain profitable. Among them, the Antminer S21Pro has the lowest breakeven price at $32,200, with a daily net revenue of $5.52. According to BTC.com, the lowest breakeven price was just $14,300 in August last year.

If operating in high-cost electricity areas ($0.12/kWh), only three models remain profitable: the Antminer S21Pro, S21 Hyd, and S21—all requiring Bitcoin prices above $55,200 to avoid shutdowns.

If current market conditions do not improve, electricity cost becomes a decisive factor for miner survival. But how much improvement is needed to ease pressure?

Assuming low electricity costs persist, when Bitcoin reaches $80,000, 45 miner models become profitable. The Antminer S21Pro still has the lowest break-even point, while the WhatsMiner M63S (390T) achieves the highest daily net profit of $12.30. At $100,000, 66 models would be profitable, with the M63S earning up to $18.41 daily. Higher prices greatly expand viable mining options and allow for diversified hardware deployment.

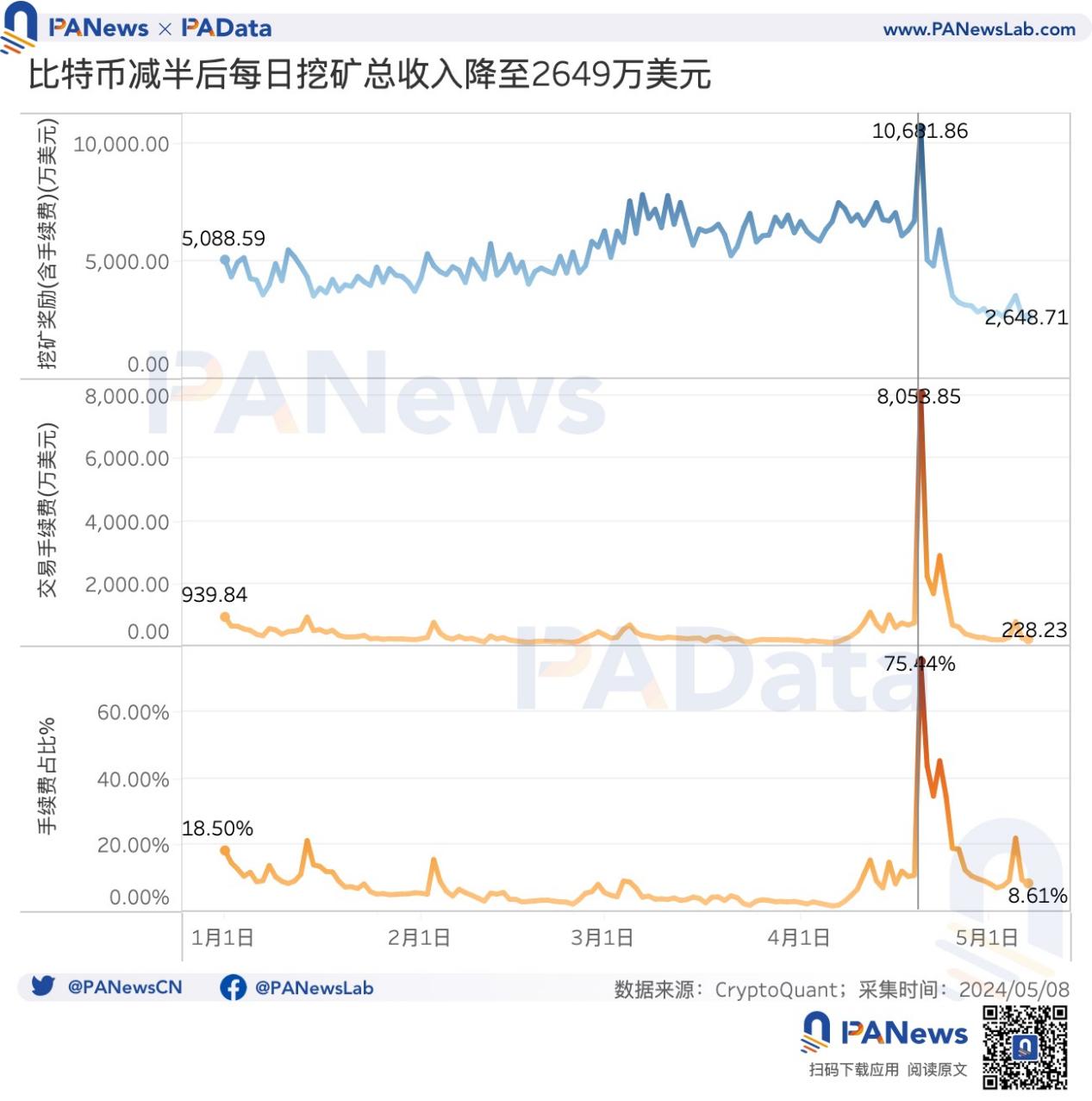

Post-halving, mining revenues have plummeted. According to CryptoQuant, current daily mining revenue is approximately $26.49 million—down 51.63% from the pre-halving average of $54.76 million. Notably, on halving day, Runes protocol launched, pushing daily mining revenue to about $107 million—95.06% higher than the pre-halving average.

Strong on-chain demand can offset halving-related losses through transaction fees. On Runes’ launch day, fees reached $80.58 million—75% of total mining revenue. However, as Runes hype cooled and transaction volumes fell, daily fees have dropped to about $2.28 million—34% lower than pre-halving levels.

Miner revenue (in USD) = (block reward + transaction fees) × price. Thus, post-halving revenue declines can be compensated in two ways: either the price rises significantly (assuming stable fees), or fees increase substantially and sustainably (assuming stable price). Of course, this is a simplified static analysis intended to illustrate the potential effects of halving on price and transaction activity.

Using CryptoQuant data: pre-halving daily mining revenue averaged $54.76 million; post-halving, average daily blocks are 139, meaning average block rewards are 434.23 BTC; average fee per transaction is 0.0002624 BTC; average daily transactions are 553,328.19.

If transaction fee income remains constant (same average fee and transaction count), reaching pre-halving revenue levels requires a Bitcoin price of $94,489.82—51.63% above current levels.

If price remains unchanged and fees stay constant, reaching pre-halving revenue requires daily transactions to reach 1.6737 million—202.49% higher than post-halving averages.

If price and transaction volume remain unchanged, reaching pre-halving revenue requires average fees to rise to 0.00080317 BTC per transaction—206.08% higher than current levels.

03. Bitcoin Demand Remains Weak; TVL and Runes Metrics Decline

Understanding the scale of halving's impact on mining is crucial, as unprofitable miners threaten the blockchain’s foundational security. Beyond price, transaction fees and volume directly reflect demand. So, what is the current state of Bitcoin demand?

Regarding Runes, according to @cryptokoryo’s Dune Analytics dashboard, related transaction counts have dropped from an initial 463,600 to 79,400 currently, with fees falling from 881 BTC to just 4 BTC. As seen in daily mining revenue charts, the strong initial demand from Runes could bring massive gains to miners. The challenge now is maintaining sustained demand for Runes and other Bitcoin-based projects.

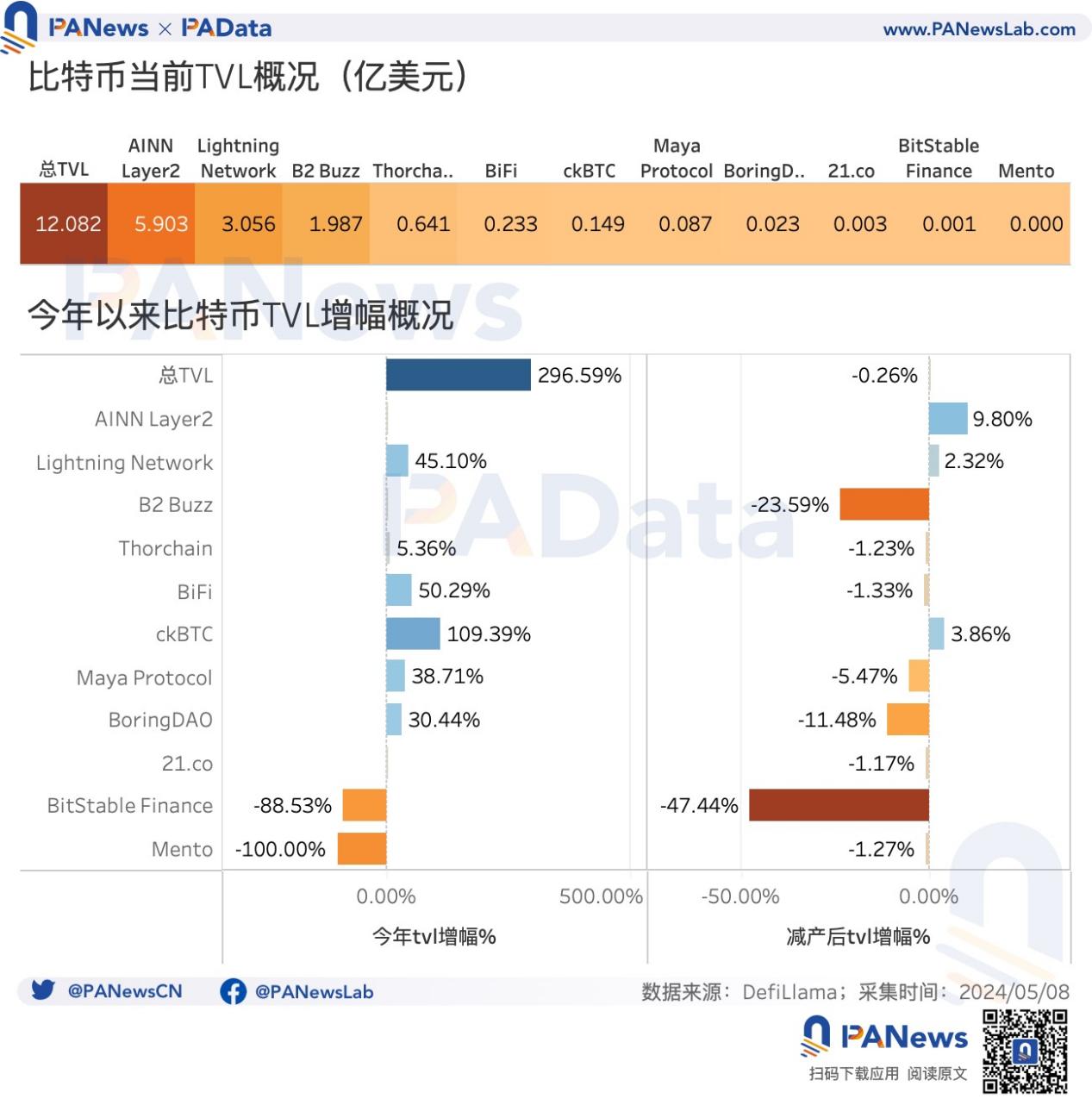

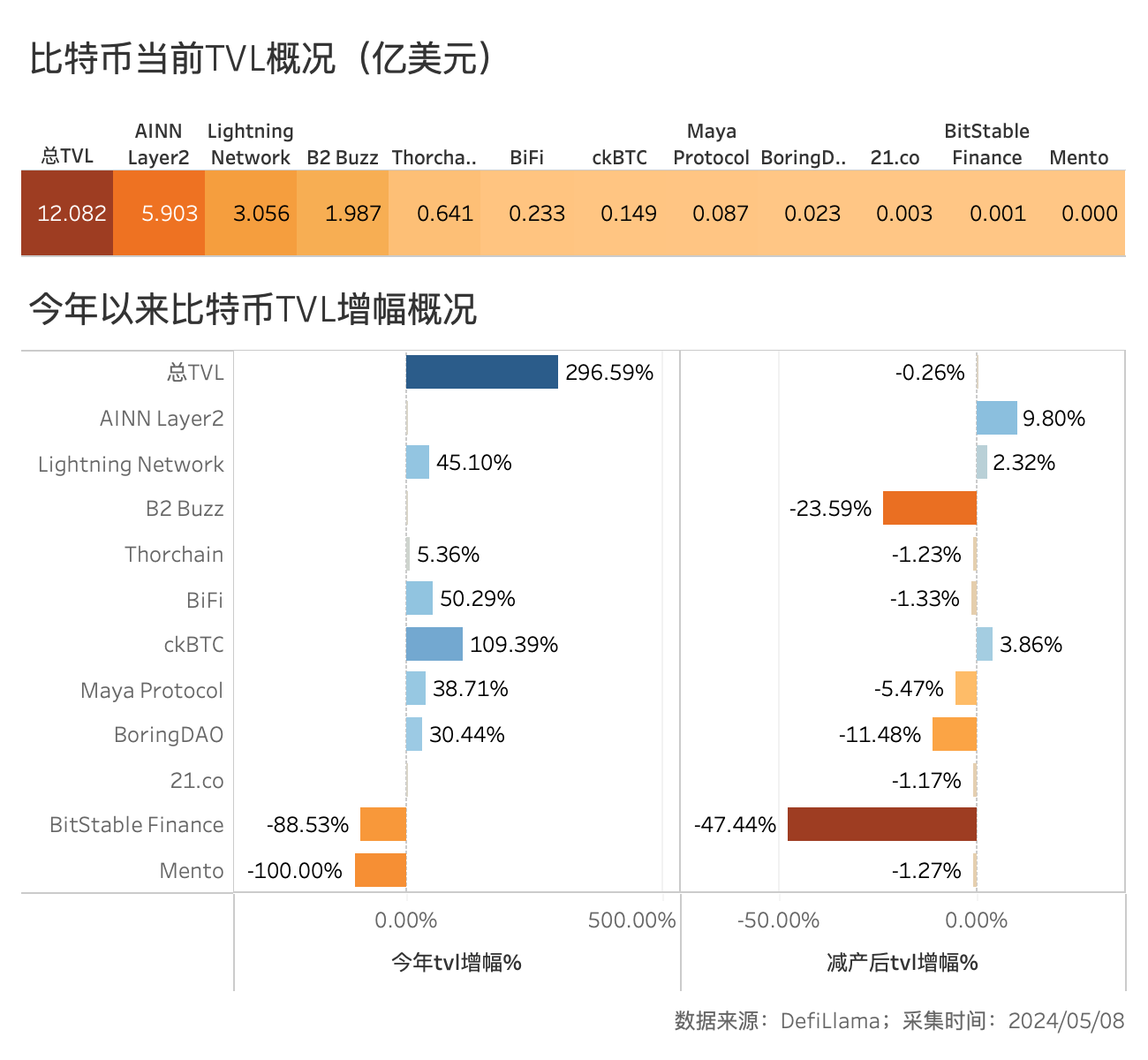

Beyond Runes, Layer2 solutions and DeFi innovations on Bitcoin may unlock new usage demand. Currently, according to DefiLlama, Bitcoin’s on-chain TVL has reached $1.208 billion—up 296% since the start of the year and largely stable post-halving. Besides the Lightning Network, the newly launched AINN Layer2 has performed well, with TVL reaching $590 million, making it a major application in the Bitcoin ecosystem. Additionally, BiFi, Maya Protocol, and BoringDAO have also seen rapid TVL growth this year.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News