Stablecoins, the second-largest buyer of U.S. Treasuries

TechFlow Selected TechFlow Selected

Stablecoins, the second-largest buyer of U.S. Treasuries

The strangest unintended consequence.

Author: Kunle

Translation: TechFlow

Long ago, I was a bond and foreign exchange trader. During U.S. Treasury auctions, I remember we would periodically discuss one question every few months: “What’s China’s bid?” referring to whether the People’s Bank of China (PBOC) would be a buyer in that auction. Looking back, I don’t even recall if this actually impacted any auction I observed, but the takeaway for me was that perhaps one day the PBOC wouldn’t buy at an auction—and when that happened, the U.S. Treasury might be in trouble.

It wasn’t until recently, when I saw the chart below, that I revisited this thought (translator’s note: the red bars represent stablecoins—the amount of stablecoins used to purchase U.S. Treasuries):

Source of the chart can be found here.

You don’t need to squint too hard to see what it suggests. The crypto world may have inadvertently designed a system that could strengthen the dollar’s status as the global reserve currency. Here’s why.

Bitcoin maximalists often argue:

-

The U.S. government (and most governments) borrow excessively and print too much money.

-

This behavior amounts to stealing wealth from the future.

-

Eventually, this will lead to hyperinflation and devalue the dollar.

-

When that happens, the dollar will collapse.

-

Therefore, holding Bitcoin is a hedge against points 1 through 4 above.

Personally, due to the dollar’s reserve currency status and other factors (e.g., few assets match the liquidity of dollar markets, making dollars unavoidable at scale), the dollar behaves oddly compared to other currencies—but I don’t fully understand these dynamics, nor am I deeply versed in them.

Additionally, another macro view I’ve gathered from business news is:

-

The world is becoming increasingly multipolar / less integrated.

-

For this reason (among others), China (and possibly other governments) are less interested in holding U.S. Treasuries (hence buying more gold), which partly explains why spot gold prices are at historic highs while ETF gold holdings decline.

While I lack strong arguments explaining why this macro theme exists, many data points suggest it’s real. However, I believe crypto has caused another interesting phenomenon—an actual balancing force. Fundamentally, demand for dollars among non-U.S. individuals and businesses far exceeds supply. For non-U.S. individuals, the dollar is typically a more stable store of value than their local currency, which is often difficult to access via local banks. For non-U.S. businesses, about 40% of cross-border trade is still settled in dollars. Wealthy individuals in developing countries often move excess savings to the U.S., U.K., or Europe. Cities like London, Vancouver, and New York reflect demand for dollar-denominated assets. Non-wealthy individuals in developing nations struggle to access dollars—a pent-up demand lasting decades. I’ve previously discussed this issue.

Stablecoins in Emerging Markets

The "digital gold" narrative in crypto—that crypto hedges inflation and its permissionless nature protects users from government confiscation—is more accurate for stablecoins (cryptocurrencies pegged to reserve currencies like the dollar) than for Bitcoin. Moreover, given that the largest share of fiat-backed stablecoins are dollar-denominated, stablecoins aren't particularly useful as inflation hedges for U.S. citizens.

In a country with poor monetary management, someone might theoretically hold Bitcoin speculatively at some point. But Bitcoin’s volatility so far makes it unreliable as a store of value—when you actually need to spend it, you can’t predict its purchasing power. In short, in emerging markets, ordinary people lack sufficient surplus savings to withstand Bitcoin’s volatility for emergency needs. This makes Bitcoin a very expensive and inefficient store of value in the short term. By contrast, before crypto, wealthy individuals in poorer nations commonly held foreign currencies (usually dollars, pounds, or euros) as a savings mechanism—a practice that was (and remains) widespread. As a market maker, I’ve long believed that a good heuristic for judging a country’s economic trajectory is “Where do the rich keep their wealth?” Wherever wealth flows upon enrichment (e.g., immediately buying property in New York or London) signals citizen fear of wealth seizure—either explicitly or indirectly via money printing.

Governments hate this, as it creates natural selling pressure on local currencies and moves assets beyond their control. Yet, fiat-backed stablecoins pegged to dollars or euros (actual managed assets) are permissionless and effectively beyond government reach—essentially digital versions of existing use cases. Before stablecoins, you had to buy dollars from a bank and hold them in an account (with its own advantages), but banks could

a) refuse to sell them to you;

b) charge high fees for purchase or holding;

c) be forced by the government to transact at artificial exchange rates or limit how much you could buy or hold.

Even today, if you’re in the U.S., try going to a local American bank or logging into your Chase mobile app to buy euros—you’ll quickly see how poorly supported this is.

Essentially, everyone worldwide wants access to a relatively stable currency to denominate their savings—one with predictable exchange rates relative to daily goods and services. For most people today (2024), the dollar and euro are more stable than local currencies. Dollar-backed (or pound-, euro-backed, take your pick) stablecoins offer a permissionless way to achieve this. The loudest voices in crypto have little incentive to tell you this because USDC won’t make them rich. Ironically, stablecoins actually help address runaway hyperinflation, whereas Bitcoin merely trades domestic currency volatility for crypto volatility. This isn’t to say Bitcoin is useless—only that if you truly need to access your savings unpredictably, Bitcoin is a poor choice.

The Strangest Unintended Consequence

Stablecoins are turning retail investors/citizens/savers around the world into implicit buyers of U.S. Treasuries. Here’s why:

-

Stablecoins allow people outside the U.S. to hold dollars in a permissionless way that their governments cannot control and their banks would never easily provide—and in some cases, earn interest in USD. The poorer you are, the harder it is to access dollars. And this is just beginning—stablecoins are only starting to be used for non-crypto purposes, such as replacing SWIFT transactions and cross-border SME payments (which Bridge does). I can only imagine demand will continue rising as stablecoin use expands offline.

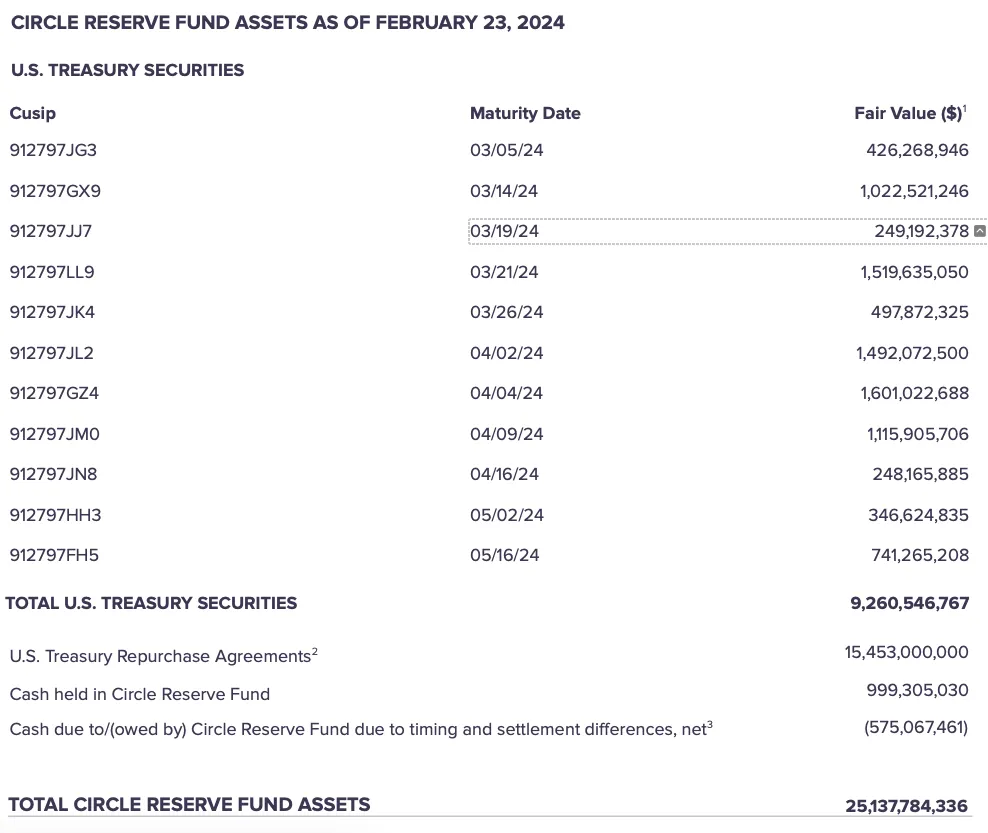

-

Well-managed stablecoins must essentially hold the most stable and liquid securities—primarily U.S. Treasuries. For example, as of February 2024, most USDC holdings consist of U.S. Treasuries, repos, and cash:

-

Thus, demand for Treasuries grows linearly with stablecoin demand itself.

-

This essentially means roughly 90% of stablecoin demand will translate into demand for Treasuries in some form.

From a strange angle, buying a stablecoin backed by Treasuries is almost easier than buying the underlying Treasuries directly. A threefold increase in stablecoins would make them one of the top five holders of U.S. Treasuries. Therefore, it’s not far-fetched that crypto growth could help sustain the dollar’s role as the reserve currency for the next generation.

Implications If These Trends Continue or Accelerate

If these trends persist, several potential implications arise.

First, given that stablecoins are largely backed by Treasuries, there are novel contagion scenarios we haven’t experienced before. For instance, during the kind of hyperinflation event feared by crypto advocates, mass redemption attempts by retail holders could destabilize stablecoins and impact the broader crypto market.

Likewise, we might encounter a “breaking the buck” event—because while stablecoins trade 24/7, underlying Treasuries do not. Stablecoin issuers may not be able to produce real dollars fast enough, potentially leading to de-pegging, where stablecoins trade at a discount during panic (like USDC trading at 85 cents during the SVB crisis). Such events could affect not only crypto markets but also money market funds as a category.

It’s hard to predict how this plays out. As stablecoin usage grows—especially institutional adoption within crypto—the mechanisms for transferring assets will shift. In crises, asset correlations tend to be much higher than in calm periods. At current scale, by the time we realize how it unfolds, it may already have happened.

Second, the broad distribution of Treasuries via stablecoins to retail investors—and the partial monetization of reserves by stablecoin “managers”—makes weaponizing Treasuries far less likely compared to when held by foreign central banks. As stablecoins grow and accumulate more U.S. Treasuries, the likelihood of mass sell-offs during conflicts harming U.S. government financing diminishes. Retail investors/savers worldwide are unlikely to express political preferences by selling stablecoins (even if anti-USD), since their local currencies may be equally volatile. Plus, for stablecoin issuers, earning yield is how they profit (e.g., Tether earned $1 billion in 2023 from Treasury yields), so they lack intrinsic motivation to sell unless redemptions occur.

Put differently, U.S.-China decoupling and related capital flow restructuring are generally seen as detrimental to dollar dominance. Yet, the rise of stablecoins counters this trend and may ultimately reinforce the dollar and Treasury dominance. Driven purely by liquidity and network effects, as fiat-backed stablecoins grow, their liquidity increases (alongside dollar liquidity), and as more individuals hold dollars (or dollar equivalents), the dollar’s position becomes harder to dislodge.

Third, “flight to quality” trades during crises typically favor reserve currencies (mainly the dollar in recent decades). Historically, this shift has been most evident among institutional investors (partly because markets are institution-dominated, partly because retail access to bonds is limited). In a world where global retail can easily access dollars via USDC/USDT, the emergence of retail “flight to quality” isn’t far-fetched—where individuals globally shift from a) crypto and b) local currencies to USDC, because this is the first time they ever could.

Finally, there’s risk for emerging economies as monetary policy/sovereignty is partially ceded to individual savers. Capital controls are tools governments use to combat currency depreciation, but these become harder if citizens can directly buy USD against CAD/AUD (via USDC/USDT). This implies that if fiat-backed stablecoins continue gaining adoption, governments will eventually develop tools to at least track citizen usage—preserving the effectiveness of capital controls.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News