Arthur Hayes' latest article: BTC price fluctuates between $60,000 and $70,000 until August

TechFlow Selected TechFlow Selected

Arthur Hayes' latest article: BTC price fluctuates between $60,000 and $70,000 until August

Buy in May and hold cash, waiting.

Author: Arthur Hayes

Translation: GaryMa, Wu Shuo Blockchain

Note: This article is a selected and translated excerpt from the original text, and some details or information may have been omitted. We recommend readers refer to the original text while reading this piece to obtain more comprehensive information.

Since mid-April, as some degens observed the ongoing decline in crypto markets, they’ve been screaming about a “May crisis.”

The price action has played out exactly as I expected. The U.S. tax season, concerns over future Federal Reserve policy, the Bitcoin halving, and slowing growth in assets under management (AUM) for U.S. Bitcoin ETFs collectively created a much-needed market cleanse over the past two weeks. Speculators or short-term traders might choose to temporarily exit the market and wait and see what unfolds next. But us tough guys will continue to hodl—and if possible, accumulate even more of our favorite crypto reserve assets like Bitcoin and Ethereum, along with high-beta altcoins such as Solana, Dog Wif Hat, and I must say, Dogecoin.

This is not a fully comprehensive global macroeconomic, political, and crypto article. Instead, I want to highlight why actions by the U.S. Treasury, the Federal Reserve, and the Republic First Bank rescue now and in the near future provide fiat liquidity or increase pathways for fiat liquidity. I’ll quickly walk through some charts that support my bullish thesis.

Quantitative Tightening (QT) Slowdown = QE

When the average investor equates quantitative easing (QE) with money printing and inflation, it spells trouble for the elite class. Hence, they need to change the terminology and their method of delivering the financial system’s (toxic) monetary heroin dose. Slowing down the pace of balance sheet runoff under the Fed’s Quantitative Tightening (QT) program sounds harmless. But make no mistake—by reducing QT from $95 billion per month to $60 billion, the Fed is effectively adding $35 billion in dollar liquidity each month. When you factor in interest on reserves, reverse repo (RRP) payments, and Treasury interest payments, the slowdown in QT increases the total amount of stimulus flowing into global asset markets every month.

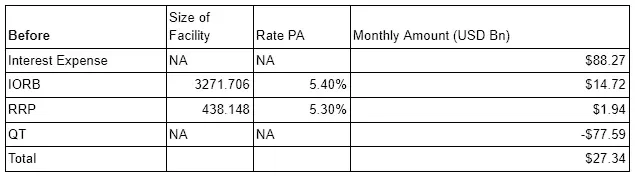

The Fed announced this week that it would reduce QT at its May 2024 meeting. Using a convenient chart, let’s examine dollar liquidity before and after the meeting.

Note that the QT line is based on the Fed’s weekly reported balance sheet and actual monthly average reduction amounts in 2024. As you can see, the Fed failed to meet its $95 billion monthly target. That raises the question: if the new target is $60 billion per month, will the Fed also fall short? Falling short of targets is actually beneficial for dollar liquidity.

“High” interest rates require the Fed and the U.S. Treasury to pay interest to the wealthy, and when combined with slower QT, this becomes even more stimulative.

That’s Powell’s side of the story—what about his good partner, Yellen?

U.S. Treasury Quarterly Refunding Announcement (QRA)

Because the U.S. is in a state of fiscal dominance, Yellen’s statements carry more weight than any other monetary official. Every quarter, the U.S. Treasury issues a QRA to guide the market on the quantity and type of debt that must be issued to fund the government. Ahead of the Q2 2024 QRA, I had several questions:

1. Will Yellen borrow more or less than last quarter, and why?

2. What will the maturity profile of the issued debt look like?

3. What will the target Treasury General Account (TGA) balance be?

Question 1:

For the April–June 2024 quarter, the Treasury expects to borrow $243 billion in net privately held marketable debt, assuming an end-of-June cash balance of $750 billion. This borrowing estimate is $41 billion higher than the one released in January 2024, primarily due to lower cash receipts, partially offset by a higher starting cash balance at the beginning of the quarter.

If you hold Treasuries, this is bad news. Supply will increase, and despite strong U.S. economic and stock market performance, tax revenues remain disappointing. This will accelerate tantrums in the bond market, pushing long-term interest rates significantly higher. In response, Yellen might resort to some form of yield curve control—and that’s when Bitcoin will truly begin its climb toward $1 million.

Question 2:

Based on current fiscal projections, the Treasury expects to increase the size of 4-week, 6-week, and 8-week bill auctions in the coming days to ensure sufficient weekly cash availability around late May. Then, ahead of the non-withholding and corporate tax payment date on June 15, the Treasury anticipates moderately reducing short-term bill auction sizes from early to mid-June. Subsequently, throughout July, the Treasury expects to return short-term bill auction sizes to levels seen in February and March—or close to those highs.

Yellen needs to increase short-term bill issuance because the market cannot withstand her reacting at the long end of the yield curve. Another benefit of increasing bills is that it drains the Reverse Repo (RRP), thereby injecting dollar liquidity into the system.

Question 3:

For the July–September 2024 quarter, the Treasury expects to borrow $847 billion in net privately held marketable debt, assuming an end-of-September cash balance of $850 billion.

The TGA balance target is set at $850 billion. The current balance stands at $941 billion, implying a drawdown of approximately $90 billion over the next three months.

This QRA announcement has a mildly positive impact on dollar liquidity. It’s not as explosive as the November 2023 announcement that sent bonds, stocks, and crypto prices soaring. But it will slowly help our investments appreciate over time.

Republic First Bank

Have you heard of this tiny, rusted-out bank? I hadn’t heard of it before it collapsed. The failure of another non-Too-Big-To-Fail (TBTF) bank isn’t noteworthy in itself. But what matters is understanding how U.S. monetary authorities reacted—and what that reveals about their mindset.

The U.S. government (via the FDIC) insures deposits at any U.S. bank up to $250,000. When a bank fails, uninsured depositors should theoretically get nothing. However, in an election year, that’s politically unacceptable—especially if the ruling party has spent months assuring the public that the banking system is healthy.

Here’s an excerpt from the FDIC:

As of January 31, 2024, Republic Bank had approximately $60 billion in total assets and $40 billion in total deposits. The FDIC estimates the cost to the Deposit Insurance Fund (DIF) related to Republic Bank’s failure will be $667 million. The FDIC determined that Fulton Bank’s acquisition of Republic Bank was the least costly resolution to the DIF compared to alternatives. The DIF is an insurance fund established by Congress in 1933 and managed by the FDIC to protect deposits at banks nationwide.

To understand what really happened, you need to read between the lines.

Fulton agreed to acquire Republic First and guarantee full protection for all depositors—but only if the FDIC provided some cash. The FDIC gave Fulton $667 million so that all Republic First depositors could be made whole. Why use the insurance fund to cover all deposits when some were uninsured?

Because if all deposits weren’t covered, the entire banking system could collapse. Any large depositor would immediately move funds to a TBTF bank, which enjoys an implicit government guarantee on all deposits. Then, thousands of regional banks across the country would fail. In a democratic republic with elections every two years, that’s not a desirable outcome. Once the public realizes that bank failures are entirely due to Fed and Treasury policies, some overpaid fools might actually have to find real jobs.

Rather than face political fallout during an election year, officials have effectively guaranteed all deposits in the U.S. banking system. This implicitly adds $6.7 trillion in liabilities—the amount of unprotected deposits reported by the St. Louis Federal Reserve.

This leads to money printing because the FDIC’s insurance fund doesn’t have $6.7 trillion. Maybe they should ask CZ for advice—after all, funds aren’t safe. Once the fund is depleted, the FDIC will borrow from the Fed, which will print money to repay the loan.

Like the other implicit money-printing policies discussed in this article, there isn’t a massive liquidity injection today. But we can now be absolutely certain that trillions of dollars in potential liabilities have been added to the Fed’s balance sheet—liabilities that will ultimately be financed by printing money.

Buy in May and Hold

Slowly adding billions in liquidity each month will dampen future negative price volatility. While I don’t expect the crypto market to immediately recognize the inflationary nature of recent U.S. monetary policy announcements, I do anticipate prices bottoming out, consolidating, and then beginning a slow upward climb.

As summer arrives in the Northern Hemisphere, some crypto investors will feel the market heating up and may sense they’re already wealthier—prompting them to spend time in trendy spots and enjoy life. I certainly won’t be glued to the Bitcoin charts all day—I might even go dancing. The recent sharp sell-off gave me a perfect opportunity to unlock my USDe and deploy synthetic dollars into high-beta meme coins.

I’m buying Solana and related dog coins for momentum trades. For longer-term altcoin holdings, I’ll increase my allocation to Pendle and hunt for other “discounted” cryptos. I’ll use the rest of May to build my positions. Then it’s time to hold and wait—for the market to finally recognize the inflationary implications of recent U.S. monetary policy moves.

For those seeking predictions, here are the key points:

1. Did Bitcoin hit a local low around $58,600 earlier this week? Yes.

2. What’s your price forecast? A strong rally above $60,000, followed by trading between $60,000 and $70,000 through August.

3. Are the recent Fed and Treasury policy announcements forms of implicit money printing? Yes.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News