BTC Halving 2024 Outlook: Long-Term Bullish, But Is It Worth Trading Now?

TechFlow Selected TechFlow Selected

BTC Halving 2024 Outlook: Long-Term Bullish, But Is It Worth Trading Now?

From a supply perspective, this is undoubtedly a bullish event.

Author: Rick Maeda

Translation: TechFlow

Executive Summary

-

On the surface, the long-anticipated Bitcoin halving has historically been bullish for the network.

-

However, given the limited number of past halvings and a closer look at BTC’s performance within broader market contexts, it is difficult to make any highly confident assertions based solely on the halving event itself.

-

Overall, the Bitcoin halving may not be a directly tradable event, but structurally, from a supply standpoint, it remains bullish. With favorable macro tailwinds, BTC could rally again after the halving.

Main Text

The consensus around the Bitcoin halving is that it's bullish, and the prevailing belief is that it's a tradable event. But is this really true? In this article, we examine past halving events and analyze supply and macro data leading into the upcoming 2024 halving to gain deeper insight into what this pre-announced event might mean for investors.

What Is the Bitcoin Halving?

The halving is a pre-programmed event in the Bitcoin network that cuts the block reward for miners in half (see below for more on what this means). It is a key mechanism in Bitcoin’s monetary policy, ensuring that only 21 million BTC will ever exist in circulation and preventing inflation by reducing the rate at which new bitcoins are created.

This pre-programmed update occurs every 210,000 blocks—approximately once every four years—with the next one expected around April 20, 2024. When Bitcoin launched in 2009, the mining reward was set at 50 BTC. After three previous halvings (in 2012, 2016, and 2020), the reward will soon drop to 3.125 BTC per block.

Bitcoin uses a proof-of-work (PoW) consensus mechanism to validate and secure transactions on the blockchain. In PoW, miners compete to solve complex mathematical problems, with the first miner to find the correct solution earning the right to add the next block of transactions to the blockchain. As compensation for validating transactions and adding blocks, the winning miner receives newly minted bitcoins as a reward—a reward that gets “halved” during each halving event.

The Reality of Past Halvings

At first glance, halvings have proven highly bullish for BTC.

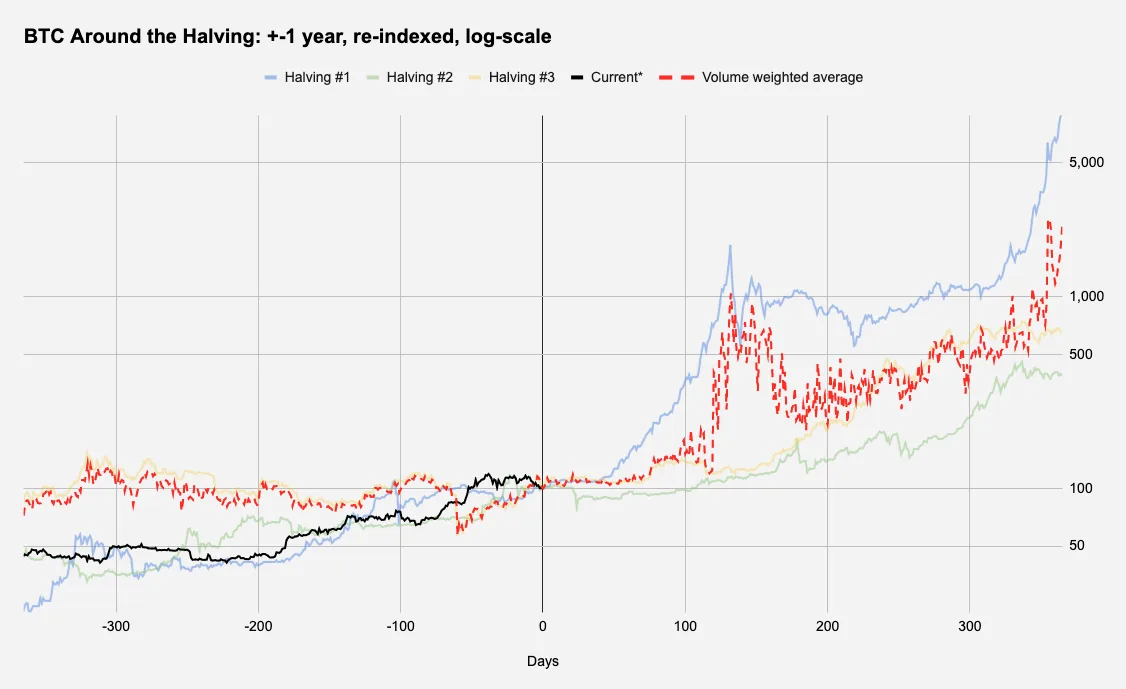

Figure 1 below shows the historical price trajectory of BTC before and after each prior halving event—from one year before to one year after. The red dashed line represents the volume-weighted average of previous halvings, while the black line shows BTC’s current path.

Figure 1: Halvings Are Bullish for BTC

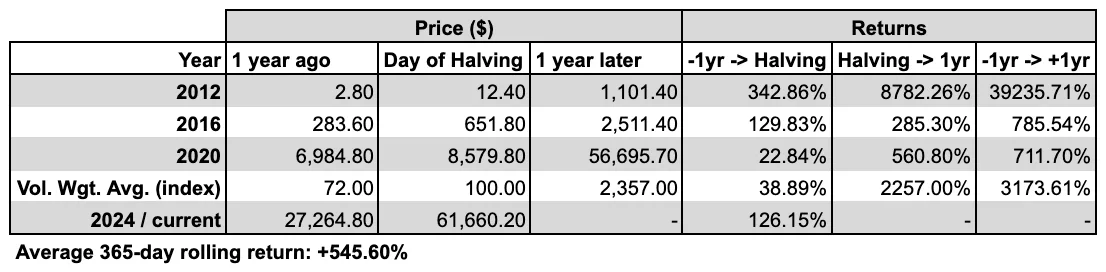

Figure 2 presents Bitcoin’s performance around halvings in tabular form.

Figure 2: Bitcoin Performance Around Halvings

With the upcoming halving scheduled for April 20, 2024, we extrapolate recent price movements using the latest data available as of April 17, 2024.

The logarithmic y-axis in Figure 1 suggests that halvings act as bullish catalysts. However, with only three observations—where the first occurred when BTC was just $12.80 and the third took place in May 2020 amid a broad surge in risk assets driven by pandemic-related quantitative easing policies—any interpretation of the data must be approached with caution. Moreover, when examining BTC’s average one-year returns since mid-2011, returns one year after the halving have not been particularly impressive, except for the first halving in 2012.

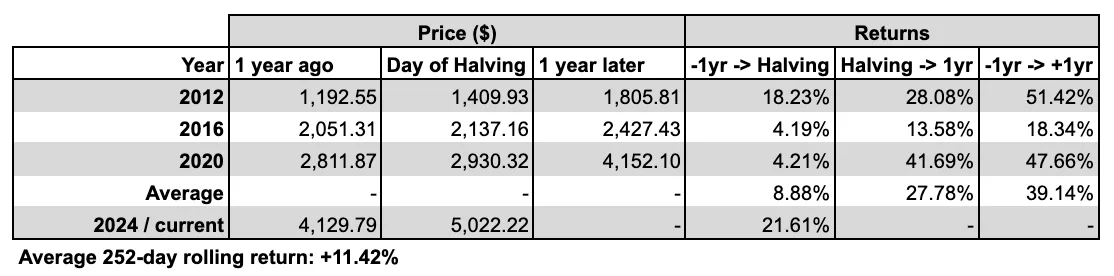

The 2020 halving raises an interesting question about overall market conditions. In Figure 3 below, we replicate Figure 2 using equities, specifically the S&P 500 index, as a benchmark for risk assets:

Figure 3: S&P 500 Performance Around Halvings

The S&P 500 has delivered an average rolling one-year return of +11.42% since mid-July 2011—aligning with the timeframe of available BTC price history—while its average one-year performance following Bitcoin halvings exceeds +27%, more than double the average! This highlights an important reality often overlooked by popular narratives. Just as we wouldn’t conclude that “a protocol update in the Bitcoin network cutting miner rewards is extremely bullish for the S&P 500,” we should be cautious about drawing strong conclusions about BTC based purely on past halving performance. By some metrics—such as outperformance hit rate—one could even argue that Bitcoin halvings have been more beneficial for SPX than for Bitcoin itself!

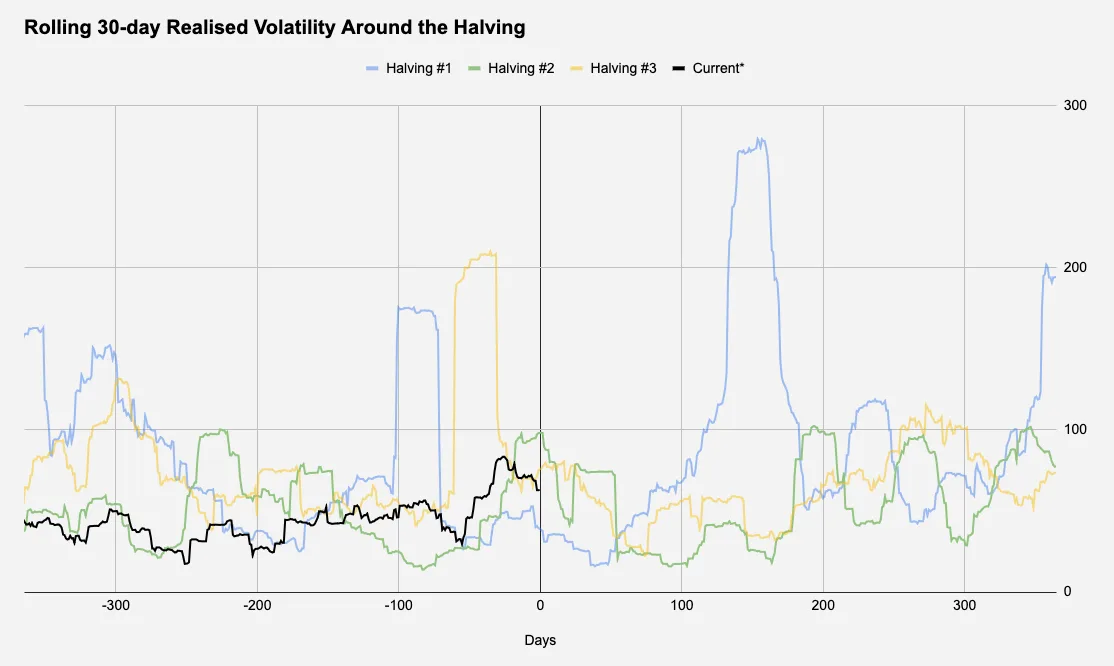

For those interested in volatility, there appears to be no clear relationship with halving dates or periods. Figure 4 examines realized volatility over 30-day windows before and after each halving:

Figure 4: No Pattern in BTC Volatility

Themes for the 2024 Halving

1: Long-Term Holders

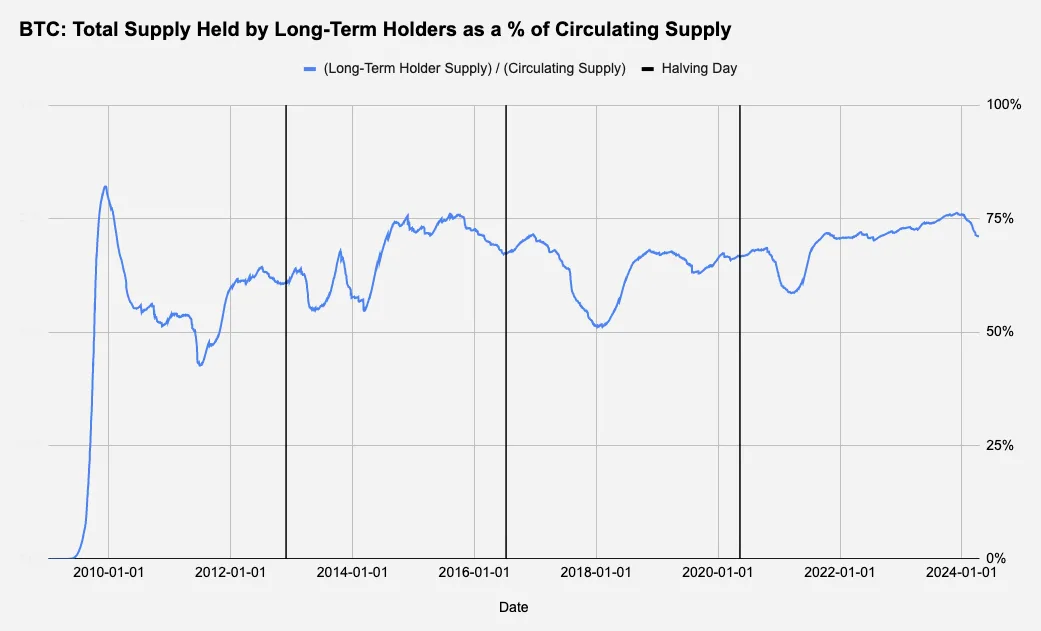

Here, we examine the total amount of BTC held by long-term holders, adjusted for supply. Since BTC’s circulating supply increases until the hard-capped limit of 21 million is reached, we divide the holdings of long-term holders by the circulating supply at the time to view the percentage held:

Figure 5: Bitcoin Held by "Long-Term Holders"

Although less pronounced in 2020, Figure 5 suggests that long-term holders tend to take profits ahead of halvings, with a decline also visible in 2024. This selling dynamic is often attributed to miners; since the halving effectively cuts revenue per block by 50%, miners frequently sell part of their reserves when rewards decrease in order to upgrade hardware for more efficient mining under lower reward conditions. With only days remaining until the 2024 halving, this structural selling pressure may currently be underway.

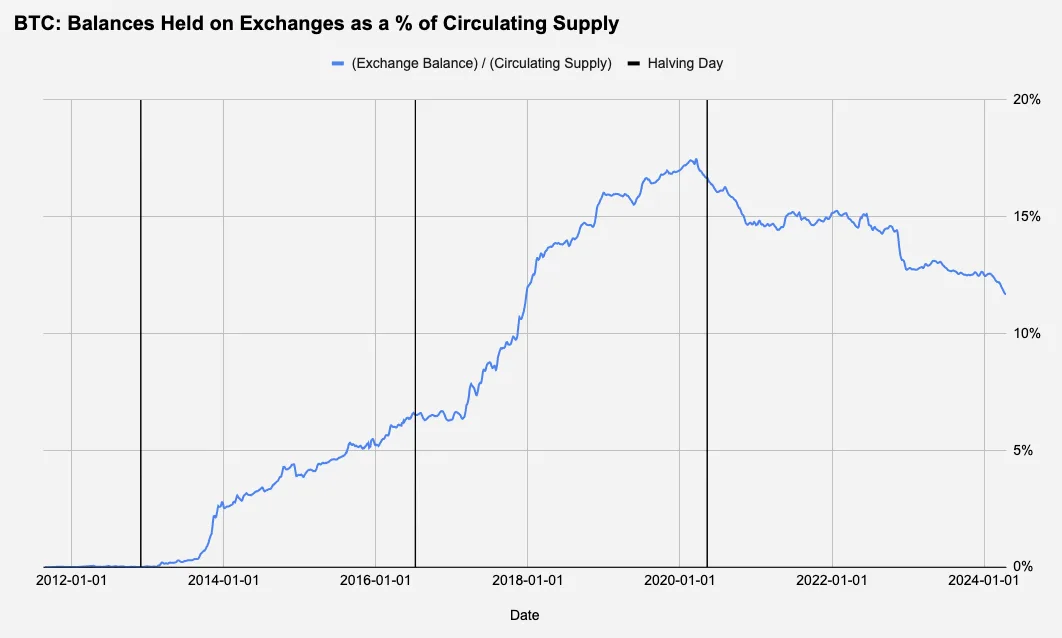

2: Exchange BTC Balances

While exchanges themselves do not make directional bets, we still examine whether exchange reserve holdings (and by extension, possibly their internal market makers) exhibit any patterns around halving dates:

Figure 6: Bitcoin Held by Cryptocurrency Exchanges

Figure 6 reveals nothing particularly noteworthy related to halvings. The only observable trend is a longer-term one: exchange balances underwent roughly six years of accumulation, followed by a steady decline as the previous bull market began.

3: Macro Context

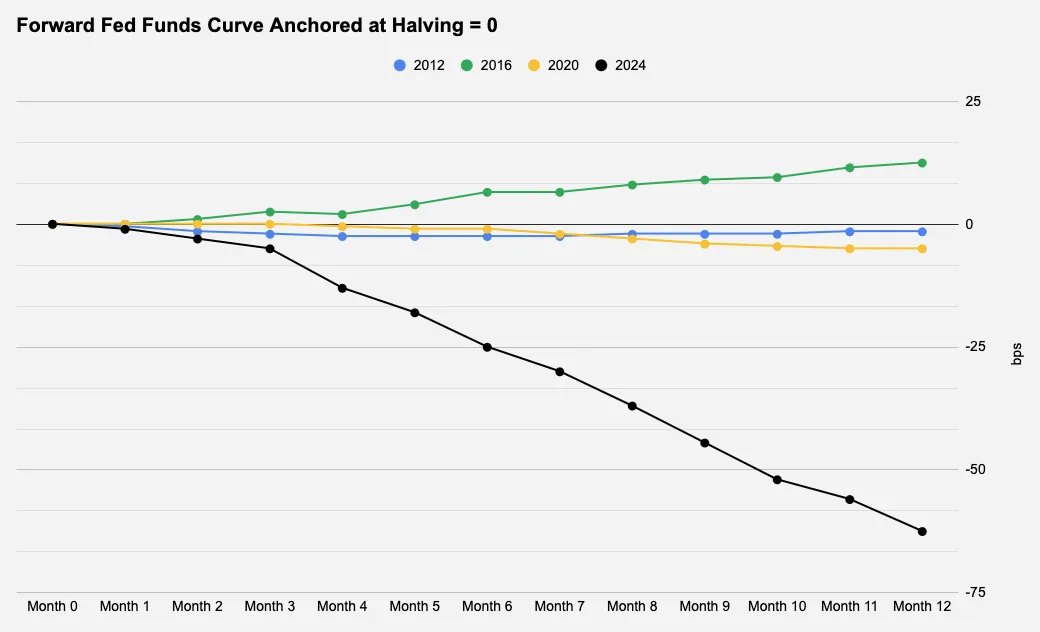

There is frequent debate about the relevance of macro conditions to Bitcoin, but macro cycles—particularly dollar liquidity (as a function of monetary policy, interest rates, risk appetite, etc.)—remain key drivers of asset prices over medium to long horizons. With this in mind, we focus on the market-implied federal funds rate for the 12 months following each halving date.

Figure 7: The Fed at Halving Events

Clearly, the upcoming 2024 halving stands out as an outlier, with nearly three rate cuts priced in.

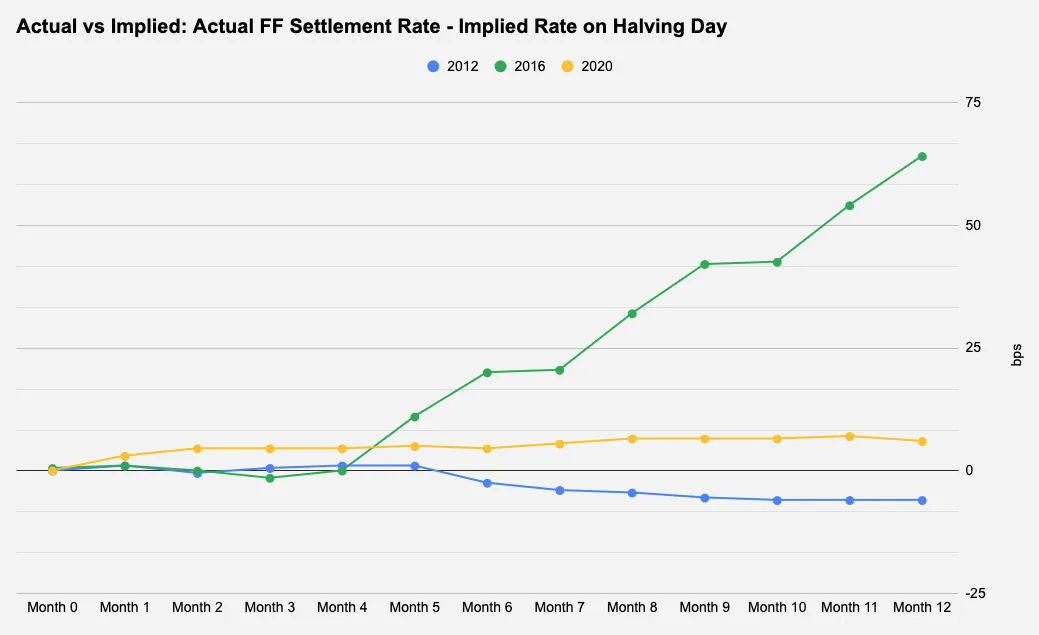

Lower interest rates are typically bullish for risk assets, but for price action, what matters most is not the already-priced-in rate, but deviations from market expectations—whether due to inflation data or statements from the Fed Chair. In Figure 8, we compare the actual settled implied rates on each halving date with prior market expectations to assess how accurate the forward pricing in Figure 7 truly was.

Figure 8: Accuracy of Fed Expectations

Data for 2012 and 2020 were relatively unremarkable, deviating by less than 10 basis points from initial expectations. However, 2016 warrants attention, as the Fed raised rates twice after the second halving—an outcome not priced in at the time. Interestingly, Figures 1 and 2 show that the 12 months following the 2016 halving delivered the weakest BTC performance among the three prior halvings and was the only instance where returns fell below the one-year average. Today, with more than two rate cuts priced in over the next 12 months, a key driver post-halving may instead be persistent U.S. inflation—or any other factor that could prompt the Fed to hold steady rather than cut.

Conclusion

We briefly explored the unique macro backdrop of the upcoming halving, but other factors not covered in this report—particularly the recent launch of spot BTC ETFs—are also significant. Given that BTC has recently captured all the attention, this is undoubtedly the most anticipated halving to date. The growing institutionalization of BTC introduces new participants that could alter supply-demand dynamics and price behavior. Notably, newly launched ETFs now hold over 4.1% of BTC’s circulating supply, while MicroStrategy holds over 1%. With only three prior halvings on record, drawing statistically significant conclusions from past performance to determine whether this is a tradable event remains challenging. Structurally, however, from a supply perspective, the halving is unquestionably bullish.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News