Traditional Institutions Enter Bitcoin: How Much Position Is Appropriate?

TechFlow Selected TechFlow Selected

Traditional Institutions Enter Bitcoin: How Much Position Is Appropriate?

Best strategy: Allocate 3% to 5% of total investment to Bitcoin.

Author: Crypto Research

Translation: Luffy, Foresight News

In the fast-evolving world of investing, diversification has long been a key strategy for reducing risk and enhancing returns. With the emergence of cryptocurrencies—particularly Bitcoin—investors have gained access to a new asset class they can add to their portfolios. This article delves into the impact of incorporating Bitcoin into a traditional 60/40 stock-and-bond portfolio.

Through detailed analysis of various quantitative metrics, we explore how different levels of Bitcoin allocation affect a portfolio’s overall performance, risk, and return profile. From gradually increasing exposure to substantial allocations, we uncover the nuanced relationship between risk and reward in the context of Bitcoin investment.

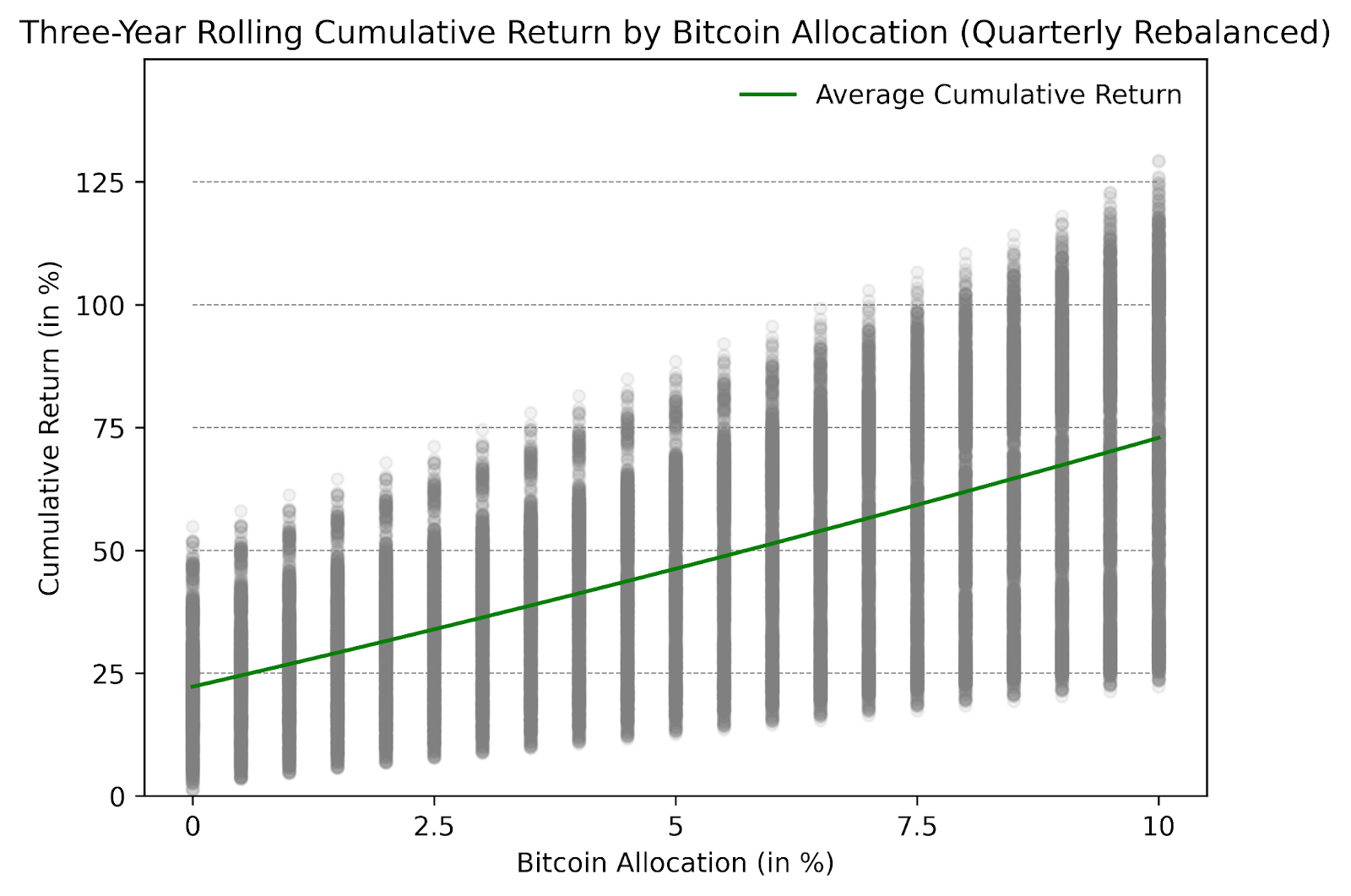

In the charts below, the first column on the left represents a portfolio with no Bitcoin allocation, while subsequent columns show what happens as Bitcoin holdings are gradually increased—up to 10%. These lines do not represent changes over time, but rather indicate the level of Bitcoin exposure held. Notably, historical data shows that the more Bitcoin you allocate, the higher your cumulative returns tend to be.

Figure 1: Three-year rolling cumulative returns of Bitcoin allocations (quarterly rebalanced), Source: Cointelegraph Research

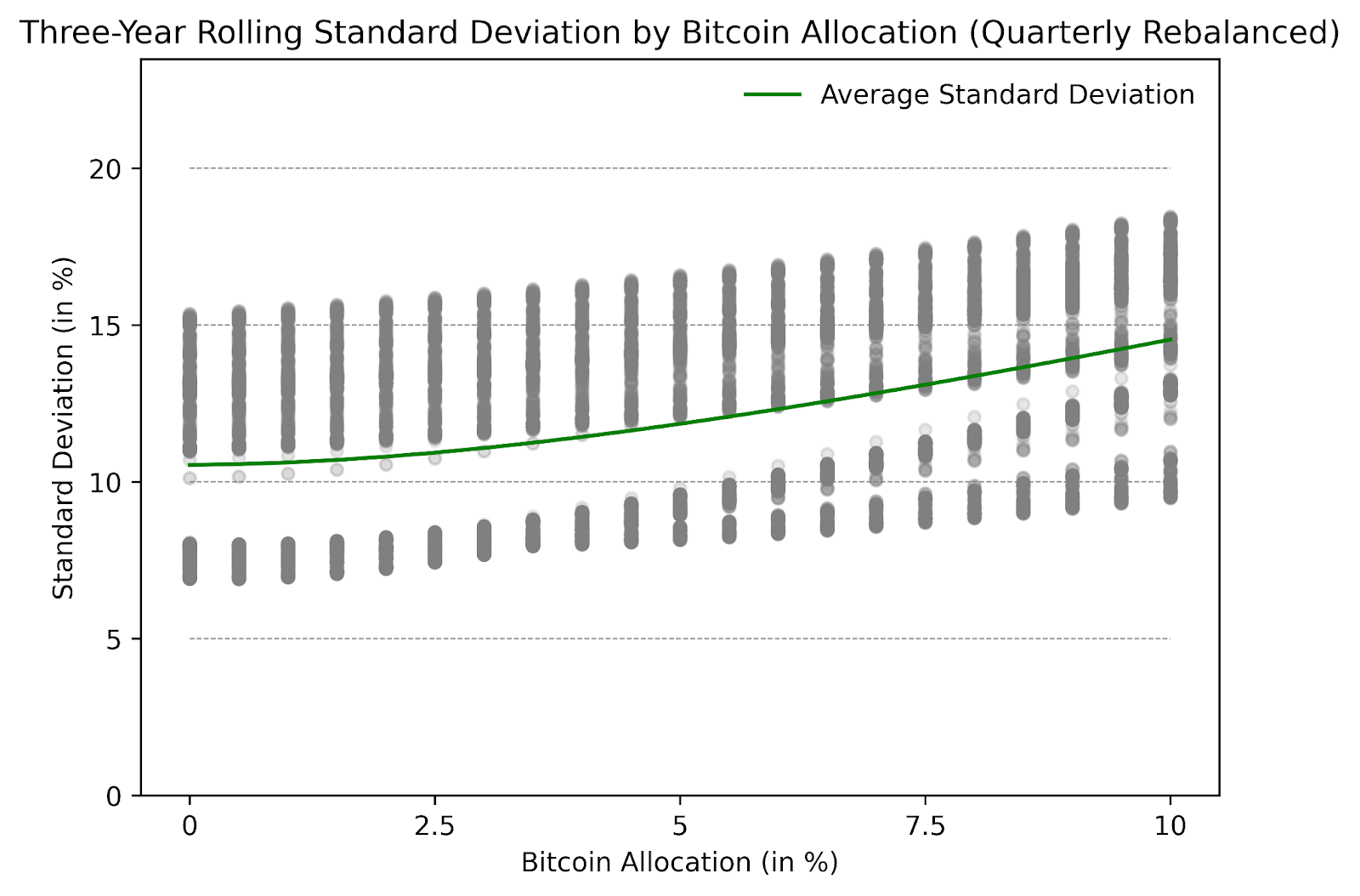

While adding Bitcoin to a 60/40 stock-and-bond portfolio increases cumulative returns, there is a caveat: it may also increase uncertainty and risk. Figure 2 illustrates how volatility changes with Bitcoin allocation. Although risk increases, it does not rise linearly. Instead, the curve shows that adding a small amount of Bitcoin—say, between 0.5% and 2%—does not significantly increase portfolio risk. However, as more Bitcoin is added, risk escalates rapidly and becomes increasingly unpredictable.

Figure 2: Three-year rolling standard deviation of Bitcoin allocations (quarterly rebalanced), Source: Cointelegraph Research

In Figure 3, we combine the information from Figure 1 to examine the portfolio’s Sharpe ratio. The shape of this chart is particularly interesting: it rises sharply at first, then plateaus as more Bitcoin is added. This indicates that adding a modest amount of Bitcoin typically results in higher returns relative to the additional risk taken. But there’s no free lunch: once allocations exceed approximately 5% of total portfolio value, the increase in risk begins to outweigh the benefits. Thus, while a small Bitcoin allocation can be beneficial, beyond a certain point the cost—in terms of significantly increased risk—becomes too high. Based on historical returns and mean-variance optimization, the optimal Bitcoin allocation lies between 3% and 5%.

Figure 3: Three-year rolling Sharpe ratio of Bitcoin allocations (quarterly rebalanced), Source: Cointelegraph Research

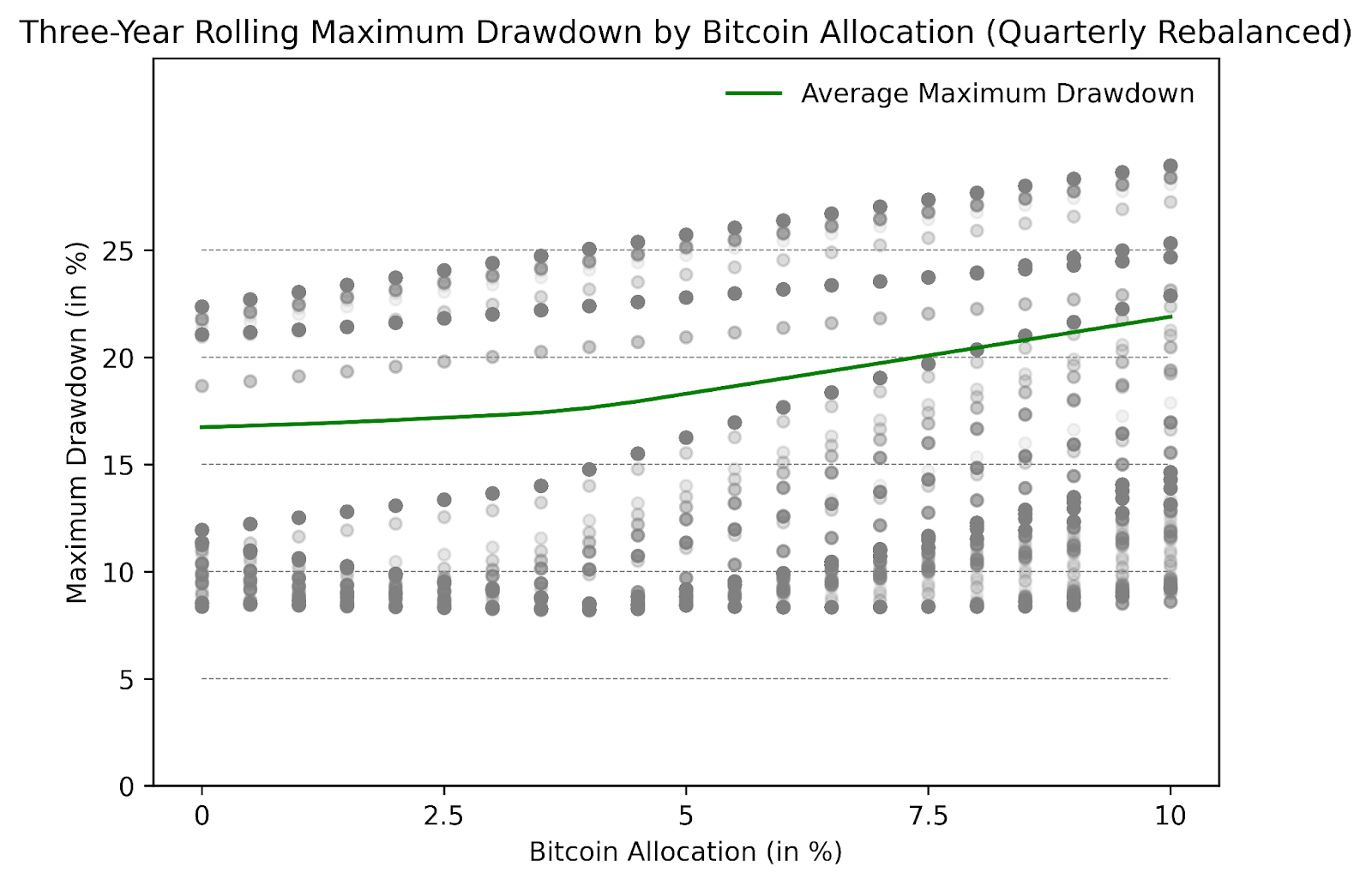

Figure 4 shows how varying amounts of Bitcoin affect the portfolio’s “maximum drawdown.” Similar to the Sharpe ratio, the green line indicates that allocating a small amount of Bitcoin (e.g., 0.5% to 4.5%) to a 60/40 portfolio has little impact on three-year maximum drawdown. However, once allocations surpass 5%, the effect on drawdown increases significantly. For institutional investors with lower risk tolerance, maintaining Bitcoin exposure at or below 5% of total portfolio value may be optimal from both a risk-adjusted and maximum drawdown perspective.

Figure 4: Three-year rolling maximum drawdown of Bitcoin allocations (quarterly rebalanced), Source: Cointelegraph Research

In conclusion, exploring Bitcoin as part of a diversified investment portfolio reveals a delicate balance between risk and return. The data presented highlights the potential for enhanced cumulative returns through strategic Bitcoin allocation, accompanied by increased volatility. Based on historical performance and mean-variance optimization, the optimal approach is to allocate 3% to 5% of total investment capital to Bitcoin.

Beyond this threshold, the risk-return trade-off turns unfavorable, underscoring the importance of careful, informed decision-making when integrating Bitcoin into an investment strategy.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News