Paradigm: All crypto products are extensions of perpetual contracts

TechFlow Selected TechFlow Selected

Paradigm: All crypto products are extensions of perpetual contracts

A world where perpetuals, collateralized assets, and Uniswap LPs interact seamlessly could be incredibly interesting.

Author: Paradigm

Translation: TechFlow

Recently, we’ve been doing a lot of thinking about power perpetuals (power perps). Power perps are perpetual contracts whose underlying asset is the power of an index price—such as squared (2nd power) or cubed (3rd power) prices.

(Editor’s note: This involves a basic mathematical concept—for example, a squared is called the 2nd power, and a cubed is the 3rd power. The idea discussed by Paradigm in this article can be simply understood as follows: most crypto products can be viewed as variations of perpetual contracts raised to the x-th power.)

Digging deeper into this topic reveals that nearly everything relates to power perps.

In this article, we present three surprising insights:

-

Collateralized stablecoins (like DAI or RAI) resemble 0 perps.

-

Margin futures (like dYdX) are 1 perps.

-

Constant product AMMs like Uniswap are replicating portfolios of 0.5 perps, while constant geometric mean AMMs like Balancer are replicating portfolios for any power between 0 and 1.

This discovery uncovers a surprisingly unified design across three major DeFi primitives. Now let’s examine each one—but first, we need to define perps and power perps.

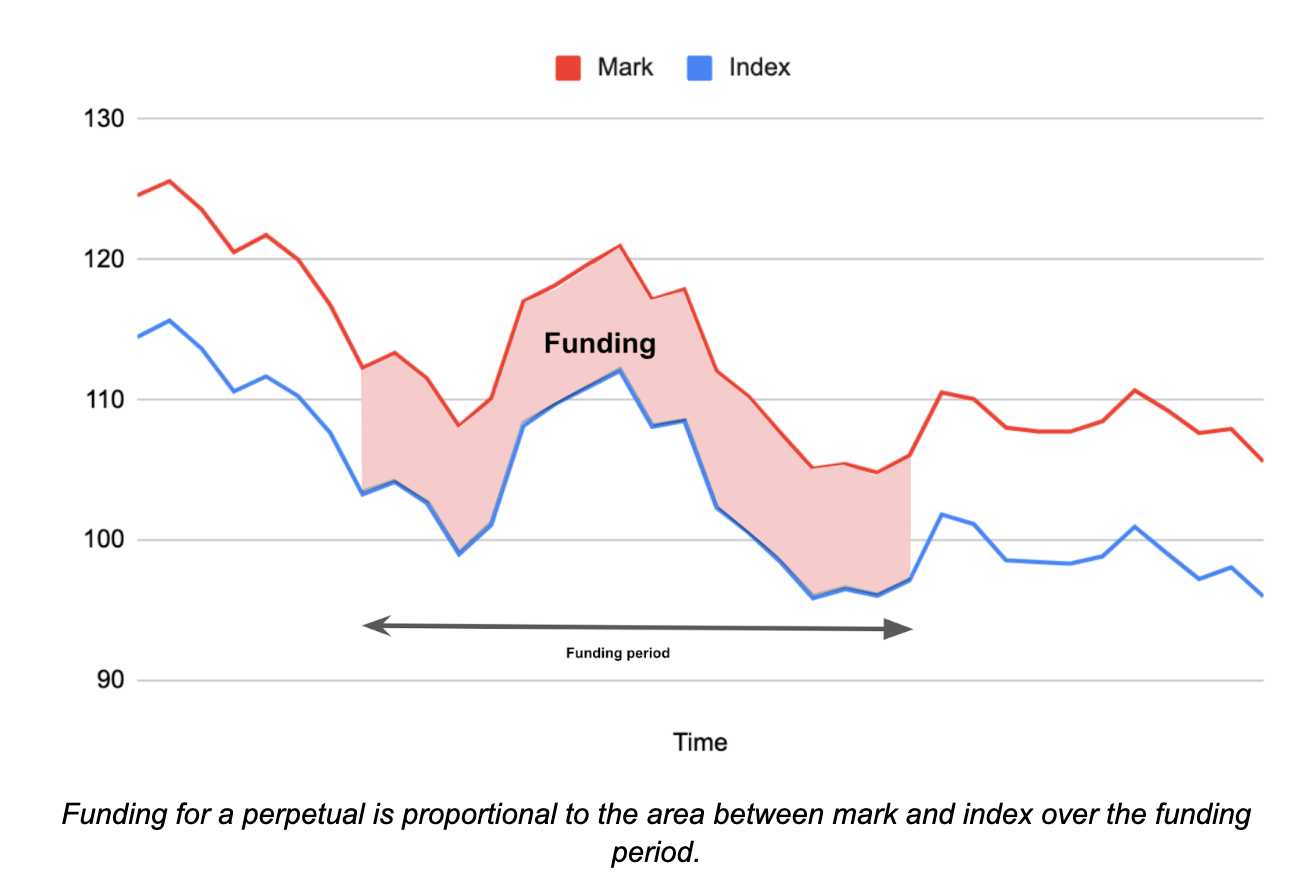

A perpetual contract tracks a first-order index and provides exposure such that the periodic payment increases with the deviation between the trading price (mark price) and the target index price.

Graphically, funding payments scale with the area between the mark price and index price over a funding period (see figure). If the mark price exceeds the index, longs pay shorts. If the mark price is below the index, shorts pay longs.

There are various mechanisms for transferring funding payments (e.g., cash vs. physical settlement, periodic vs. continuous funding, automatic vs. governance-based), and different methods for setting rates based on price deviations (including the proportional mechanism used by Squeeth and the more complex PID controller used by Reflexer). All mechanisms follow the same principle: when the mark price is above the index, longs pay shorts, and vice versa.

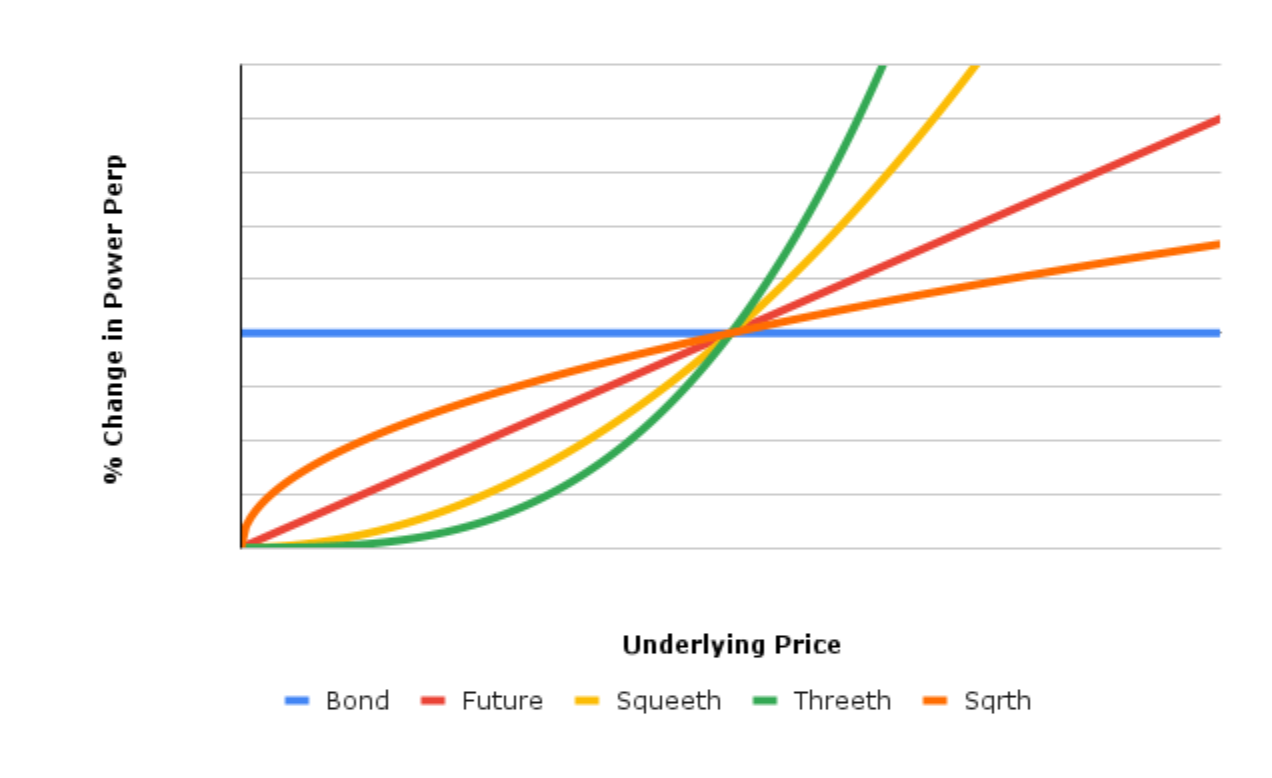

A power perpetual is a perpetual contract where the index price is defined as (index price)^p, where p is some exponent.

To open a short position in a power perp, you lock collateral in a vault and mint (i.e., borrow) some power perps, then sell them to go short. To go long, you buy them from someone who holds them.

The mechanism is driven by a required collateral-to-debt ratio: Collateral Ratio = Equity / Debt = ((Amount of collateral) × (Collateral price)) / ((Number of perps) × (Index asset price)^p )

This ratio must safely stay above 1 to ensure sufficient collateral covers the debt; otherwise, the contract liquidates by buying back enough perps to close the position.

Design of Power Perpetuals

The design of a power perp involves choosing p, a minimum collateral ratio c > 1, and three assets:

-

Collateral asset: e.g., USD

-

Index asset (the asset whose value is tokenized): e.g., ETH

-

Quoting asset (the unit we use to measure value): usually USD

Now we present our three claims.

Claim 1: Stablecoins are 0-perps

A stablecoin is a loan against reliably priced collateral, secured by minted tokens. The following configuration exemplifies a USD stablecoin:

-

Collateral asset: ETH

-

Index asset: ETH

-

Quoting asset: USD

-

Collateral ratio: 1.5

-

Power: 0

This means we post ETH as collateral and mint stablecoin tokens. The index is ETH raised to the zeroth power: ETH^0 = 1.

If I deposit 1 ETH as collateral, and ETH trades at 3000, I can mint up to 2000 tokens. This gives a 1.5x collateral ratio: Equity / Debt = ((1) × (3000)) / ((2000) × (1)) = 1.5

Funding equals the stablecoin’s current USD trading price (mark price) minus the target index price^0.

Funding = Mark Price – Index = Mark Price – Price^0 = Mark Price – 1

The funding mechanism strongly incentivizes the stablecoin’s price to trade near $1. If it trades significantly above $1, it becomes profitable to sell your holdings, mint more stablecoins, sell them, and collect funding. If it trades below $1, buying stablecoins yields positive funding and potential capital gains later.

Not all stablecoins use this exact (mark price – index) funding mechanism, but all collateralized stablecoins share this core structure: a loan backed by good collateral. Even stablecoins with governance-set interest rates adjust them similarly to (mark price – 1) to maintain their peg to $1.

Claim 2: Margin futures are 1-perps

If we change the power in the previous section from 0 to 1 and switch the collateral to USD, we get a tokenized ETH asset:

-

Collateral asset: USD

-

Index asset: ETH

-

Quoting asset: USD

-

Collateral ratio: 1.5

-

Power: 1

I post $4500 in collateral at an ETH price of $3000 and mint one stable ETH token. The collateral ratio is:

The funding for this perp is the dollar trading price of the perp (mark price) minus the target index price^1.

Funding = Mark Price – Index = Mark Price – Price^1 = Mark Price – ETH/USD price

The funding mechanism strongly incentivizes the perp to trade close to the ETH price. If the perp price runs too high, funding encourages arbitrageurs to buy ETH and short the perp. If it drops too low, they’re encouraged to short ETH and buy the perp. There’s a precise argument (see paper on Everlasting Options) that the mark price should be based on expiring instruments providing ETH price exposure.

I can sell this stable ETH asset to short ETH exposure, backed by USD collateral.

From Tokenized Short Assets to Leveraged Margin Perps

The stable ETH asset we constructed isn’t capital efficient. We put in $4500 of collateral to short only $3000 worth (1 ETH) of ETH exposure. We can improve capital efficiency by selling the dollar-denominated stablecoin and using the proceeds as collateral to mint more perps.

With a minimum collateral ratio of 1.5 and ETH at $3000, we get the following sequence:

-

Deposit $4500 and mint 1 stablecoin

-

Sell stablecoin for $3000, deposit proceeds, mint 1/1.5 = 0.666 more

-

Sell stable ETH for $2000, deposit proceeds, mint (1/1.5)^2 = 0.444 more

-

Sell stable ETH for $1333.33, deposit proceeds, mint (1/1.5)^3 = 0.296 more

Summing the trades, we end up minting and selling 3 stable ETH tokens—a $9000 short ETH exposure on $4500 of collateral. This position is equivalent to opening a 2x leveraged short ETH/USD perpetual contract.

If we can use flash swaps or flash loans, this process simplifies: we could flash-swap 3 stable ETH for USD and use the proceeds as collateral to mint stable ETH to repay the flash loan.

With a 110% collateral requirement, we could build a 10x position.

Going Long Instead of Short

To go long, buy stable ETH for USD. For leveraged long exposure, use stable ETH as collateral to borrow more USD, use that to buy more stable ETH, repeat—up to 2x ETH. With flash swaps or flash loans, this can be done in a single transaction.

All this implies that fully collateralized (over-collateralized) perpetuals can be transformed into undercollateralized perps—just like those traded on dYdX.

Claim 3: Uniswap and Other Constant Product CFMMs Are Nearly 0.5-perps

The value of a liquidity position in a Uniswap pool scales proportionally to the square root of the relative price of two assets. For a full-range LP in an ETH/USD pool, the LP’s value is:

V = 2 * (k * (ETH price))^0.5

where k is the product of the two token quantities. The pool earns trading fees every period.

Now consider a perp with:

-

Collateral asset: USD

-

Index asset: ETH

-

Quoting asset: USD

-

Collateral ratio: 1.2

-

Power: 0.5

This perp would track price^0.5, mirroring AMM returns.

A portfolio shorting 2*k^0.5 units of the perp and holding the LP position captures the difference between perp funding and AMM fees. Since this trade offsets price risk, the 0.5 perp’s funding rate should equal the expected Uniswap fee income:

Expected Uniswap Fee = Index – Mark Price

This leads to a powerful result: equilibrium Uniswap fees should equal the 0.5 perp’s funding rate. In the simplified zero-interest case, this gives: Equilibrium Uniswap return = σ²/8

where σ² is the variance of the price return of one pool asset relative to the other. We derive this result from the Uniswap side. We also detail it from the power perp perspective here.

(Editor’s note: “Synthetic Uniswap” refers to a derivative financial product or strategy designed to mimic the behavior of the Uniswap trading platform.)

Thus, stablecoins (and collateralized lending more broadly), margin perpetual futures, and AMMs are all forms of power perpetuals.

Finally

Higher-order power perps—starting with quadratic (squared) power perps. Squeeth was the first quadratic power perp, offering pure exposure to the quadratic component of price risk. By combining higher-power perps with 1-perps (futures) and 0-perps (collateral), we can approximate many payoff functions.

For greater precision, we can approximate any function—sin(x), e^x, log(x), etc.—using a combination of power perps with integer exponents weighted via Taylor series.

A world where power perps, collateral assets, and Uniswap LP positions interact seamlessly could be incredibly powerful.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News