Why Does the Web3 Market Need Brokers? Analyzing Broker Positioning and Future Beyond the ETF Era

TechFlow Selected TechFlow Selected

Why Does the Web3 Market Need Brokers? Analyzing Broker Positioning and Future Beyond the ETF Era

Non-compliant centralized exchanges will not forever "act as both referee and player."

Author: Beihai, Co-founder of PicWe

The approval of Bitcoin spot ETFs by the U.S. SEC has opened a new door for the digital asset market. Regulations are continuously pushing the industry toward an orderly and secure direction, making compliance one of the focal points in 2024. Only those who can achieve compliance early will gain a competitive edge as institutions rapidly enter the market.

Whether it's compliant exchanges or independent brokers, their era is just beginning.

White Lu Salon recommends reading today: Beihai, co-founder of PicWe—a platform specializing in Web3 brokerage services—shares insights on compliant exchanges and the development of Web3 brokers. Understand existing issues within the Web3 industry, recognize the importance of compliant exchanges and Web3 brokers, and explore the positioning and future of Web3 brokers in the post-ETF era.

Below is the original article.

One drama, "Blossoms Shanghai," mirrors half the history of brokerage firms.

People in Web3 resonate deeply with this series. Many instinctively substitute "stocks" with "tokens" while watching. The Chinese stock market in the 1990s closely resembles today’s cryptocurrency market. People frequently get rich overnight through leveraged trading or go bankrupt suddenly; everyone hopes friends profit but fears them showing off luxury cars like Land Rovers. Missed opportunities that could have led to financial freedom happen every month. Now that ETFs have been approved, Web3 is transitioning from its “Old Eight Stocks” era into a period of great prosperity.

In "Blossoms Shanghai," “No. 101 Xikang Road” refers to where Uncle Gu instructs A Bao to buy stocks. It's the nickname for the Jing'an Securities Trading Department of the Industrial and Commercial Bank of China, Shanghai Trust Investment Company. "A giant tree starts from a tiny sprout." This location marked the beginning of China’s brokerage firms during the reform and opening-up period.

So we must ask: Where is Web3’s “No. 101 Xikang Road”?

I. Why Does the Web3 Market Need Brokers?

In traditional securities markets, ordinary traders cannot access exchanges directly. They place orders through brokerage firm branches, which act as intermediaries executing actual trades on their behalf. In the Web2 era, users no longer need physical branches—they can place remote orders via electronic terminals. However, individual traders still cannot trade directly on exchanges and continue to rely on brokers to execute transactions. This is the most fundamental function of brokers: “buying agency services.”

In contrast, Web3 exchanges (Exchanges) impose no restrictions—any user can trade directly on decentralized platforms. So does Web3 need brokers?

Many traditional exchanges operate under a membership system and are non-profit organizations. Members self-govern, regulate each other, and participate directly in stock trading and settlement.

(1) Compliance Transformation of Web3 Exchanges

Web3 exchanges fall into two categories: centralized exchanges (CEX) and decentralized exchanges (DEX). DEX profits come from two sources: transaction fees and appreciation of the platform’s native token. CEXes generate additional revenue from a third source: user losses (referred to as “client loss”). Client loss refers to the amount users lose due to trading activities on the exchange. When users place orders, the exchange must match corresponding token trades—this defines the core trading function. Other operations such as Launchpad offerings will gradually cease being primary business lines as compliance transformation progresses.

Imagine if, in "Blossoms Shanghai," stock prices at the exchange could fluctuate based solely on Qiang Zong’s word without real capital movement—then even ten Qi Lin Hui groups couldn’t save Bao Zong.

In current practice, exchanges often engage in order matching and synthetic/virtual trading. Order matching improves efficiency and is acceptable. But virtual trading poses significant risks. Financial derivatives like perpetual contracts were originally designed for peer-to-peer betting. Perpetual contract prices don’t need to align with spot prices, and different exchanges may quote different prices for the same token. However, when bets and positions are transparent to the exchange, many exchanges actively intervene, manipulating virtual prices to consistently win against users. This explains frequent cases of users getting liquidated due to price manipulation (“pinning”). For example, Sun’s HT incident last year targeting large holders.

Some CEXes offer trading volume despite insufficient underlying token reserves. While most users merely speculate, some occasionally withdraw funds. Smaller exchanges may block withdrawals entirely, allowing only numerical trading. Larger ones might temporarily suspend withdrawals to acquire sufficient tokens on-chain or from other exchanges. Yet price volatility during this window exposes exchanges to potential losses. Thus, the quantity of spot tokens held becomes a key competitive advantage for CEXes. But hoarding tokens further exacerbates liquidity shortages in Web3.

These problems hinder the path to compliance—but they will ultimately be resolved.

(2) Insufficient Overall Liquidity in Cryptocurrencies

The overall scale of the cryptocurrency market remains small. Traditional financial markets still dominate, dwarfing crypto markets in size. For instance, global equity markets have a total market cap of about $110 trillion, with the U.S. accounting for approximately $45.5 trillion (around 42.1%). Even after the sharp rise from November last year to now, the total market cap of cryptocurrencies has only recently recovered to $1.59 trillion. This total barely exceeds Australia—the 16th largest equity market globally—and still lags behind South Korea, ranked 15th.

Crypto assets cannot be freely exchanged across types. Tokens, NFTs, inscriptions, etc., use different protocols such as ERC-20, ERC-721, BRC-20. Assets using different protocols cannot convert directly. Some require third-party tools for swaps, while others depend on auctions settled in tokens.

Each public chain fragments liquidity. Tokens on separate chains can only move via cross-chain bridges, which are slow and insecure. As a result, most capital stays confined within individual chains. Every new public chain launched divides an already scarce liquidity pool, especially when external inflows are limited.

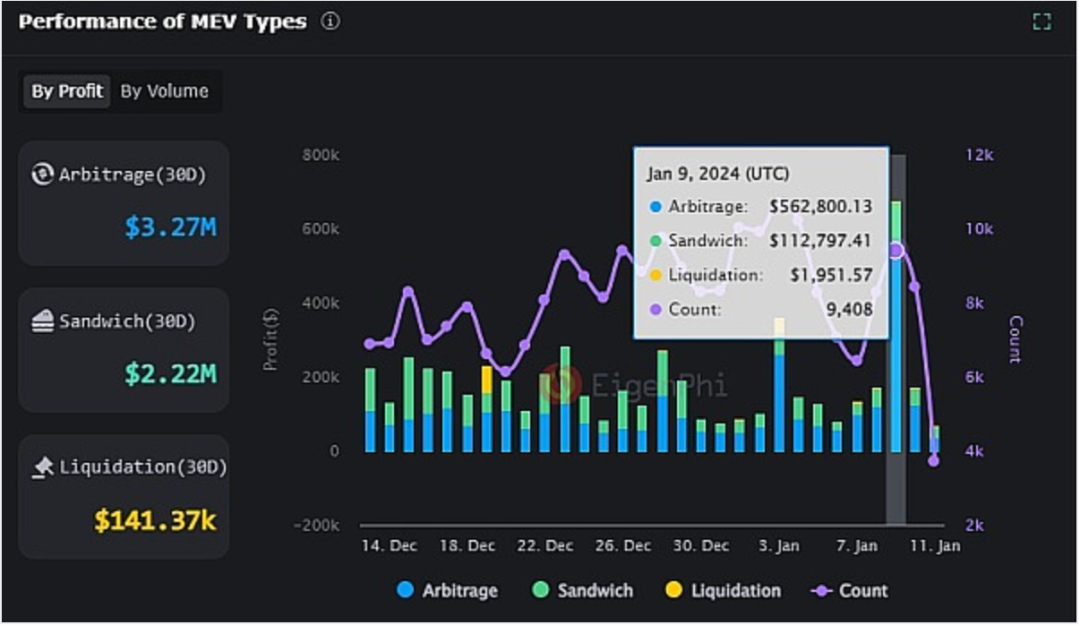

Dex developments fail to meet growing user demands. Dexes are limited to single chains or specific ecosystems. Compared to CEXes, they involve more complex operations and higher learning curves for average users. On-chain trading also carries risks such as arbitrage exploitation or “sandwich attacks,” leading to significant losses from minor mistakes.

▲ MEV data categorized by type, December 14, 2023 – January 11, 2024

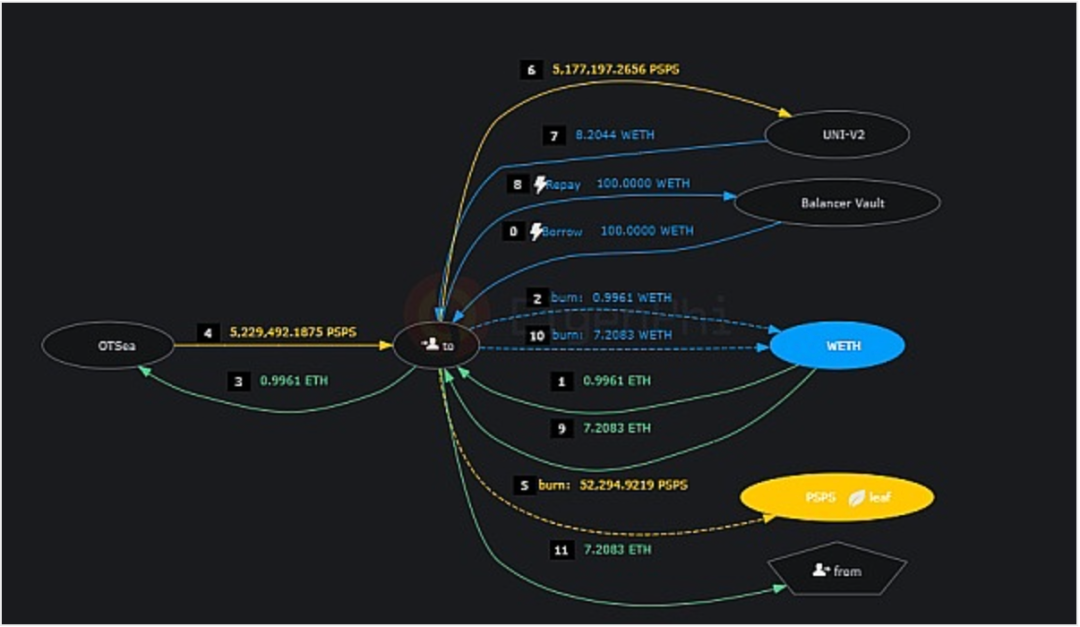

▲ Arbitrage case on January 10, 2024: Profited $17,000 using $25 via flash loans.

(3) User Trading Experience Needs Improvement

No one-click purchase for any token. Many have experienced spotting a promising investment opportunity but not knowing where to buy the token—or worse, purchasing counterfeit tokens. Many tokens are available only on certain exchanges or exclusively on-chain. To date, no product in Web3 allows users to buy any arbitrary token seamlessly. Even with on-chain tools, purchases are restricted to specific ecosystems—for example, 1inch is useless outside EVM-compatible chains.

On-chain trading has a high learning curve. Even seasoned insiders often struggle with questions like “Where do I buy?” or “How do I buy?” Each ecosystem and protocol varies greatly. Chains intentionally create barriers to retain liquidity and minimize TVL outflows. Heterogeneous chains support only their own wallets, and each builds its own DeFi ecosystem. This prevents users from completing all token transactions with a universal wallet and dApp.

II. Role of Web3 Brokers in the Post-ETF Era

(1) Positioning of Exchanges After the ETF Era

With ETF approval, the Web3 industry will become increasingly regulated. CEXes will gradually revert to their true nature as exchanges (Exchange), unlikely to continue acting as both referee and player. Future compliant CEX revenues will stem from four sources: trading commissions; broker membership fees; consulting service fees; and holding/withdrawal fees for tokens. The first three align with traditional exchanges, while the fourth is unique to Web3.

Holding and withdrawal fees will become important revenue streams for Web3 exchanges. Securities and tokens differ significantly in attributes and functions. Tokens carry broader financial rights and wider use cases than securities. Unlike securities, where investors rarely request physical delivery, Web3 users frequently want to withdraw tokens. Holding large amounts of crypto incurs substantial funding costs. In the future, brokers may not hold tokens themselves—exchanges will custody them instead. Withdrawals will be initiated by brokers and fulfilled by exchanges. Exchanges will charge brokers custody fees and users withdrawal service fees.

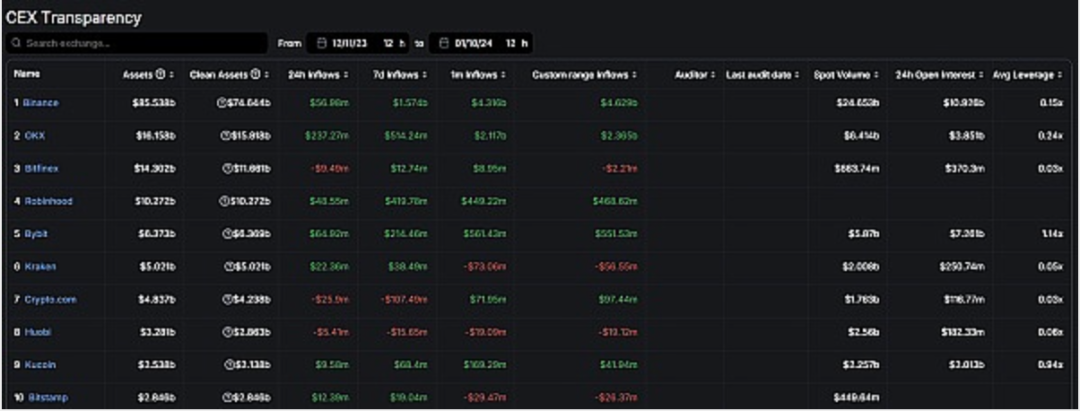

▲ Asset holdings of CEXes

(2) Positioning of Web3 Brokers

Web3 brokers provide five key services:

First: Agency buying services. Brokers leverage Web3 infrastructure to integrate CEX and DEX, enabling one-click purchases of any token and facilitating seamless token transactions. Like securities, users care less about who supplies the stock and more about ease of trading.

Second: Advisory services. One aspect involves education—brokers must explain basic Web3 concepts and promote blockchain technology to newcomers. They also assist with account setup, deposits, withdrawals, and compliance per local regulations. The other aspect is investment advice—providing guidance to help users identify investment targets and make informed trading decisions.

Third: Leverage financing and derivative services. As exchanges become compliant, perpetual contracts and margin trading will shift from exchanges to brokers, effectively preventing conflicts of interest where “referees play the game.” When projects or users need funding, broker-held capital and credit lines for token withdrawals at exchanges will become preferred solutions. Additionally, copy trading, on-chain monitoring, and similar services will consolidate under broker offerings.

Fourth: Asset management. Beyond traditional wealth management and fund products, Web3 brokers can offer unique on-chain products such as yield farming and stablecoin staking/lending, helping users achieve periodic, stable asset growth.

Fifth: Underwriting, distribution, and OTC services. Although Web3 fundraising can occur directly via IDO or ICO, having a broker’s endorsement enhances credibility in underwriting and distribution. Moreover, with numerous token unlocks occurring monthly within the ecosystem, OTC services help avoid market price fluctuations. Trusted brokers facilitate these OTC trades more efficiently through established relationships.

III. Web3 Brokers Will Become a Niche Sector in the Trading Landscape

In both traditional finance and cryptocurrency markets, whenever a bull market begins, the trading sector explodes first. “Buy brokers during bull markets” is a shared consensus.

Currently, Web3 brokers remain an emerging niche, yet several projects are already emerging. Based on service types, they can be categorized as follows:

First: Buy-agent tools. Web3 lacks an equivalent to East Money or Tonghuashun apps in traditional securities—platforms allowing users to buy any stock with one click. In the future, a series of buy-agent tools will emerge, enabling users to purchase any token effortlessly—without needing to learn on-chain operations or register on exchanges.

Currently, PicWe is the platform offering this service. Built on AA wallets, aggregated trading systems, and SIS technology (state validation service based on Lightning Network), PicWe connects liquidity across CEX and DEX. Users don’t need to provide exchange APIs or register on exchanges—PicWe’s agency-buying service enables “one-click purchase of any token.” All user assets are securely locked on-chain. The platform’s DApp and Telegram bot are live and undergoing beta testing.

Second: Information platforms. When ETF approval news broke, ETH surged nearly 10%, while L2 sectors and ETH-related concepts (e.g., ETC) spiked close to 20%. Accessing information faster means boarding earlier—with lower cost, reduced risk, and higher returns.

The fastest off-chain data intelligence system in Web3 is BubbleAI. Combining proprietary AI large-model analysis engines, BubbleAI creates an “All-in-One” AIFi ecosystem, empowering global users by delivering the most complex data in the simplest, fastest way. The BubbleAI terminal beta is already live. Core features include real-time signal aggregation, AI sentiment analysis, AI agent copy-trading, AI trending sector tracking, and AI strategy bots. Currently, BubbleAI is running a whitelist application campaign with over 20,000 applicants.

Third: Financial derivatives. Derivatives come in many forms, but the closest to brokerage services are copy-trading platforms. Copy-trading includes three main types: DeFi yield farming, copy-trading (further divided into CEX copying and tracking on-chain Smart Money), and quantitative trading. Among these, yield farming focuses on “yield stacking” or stablecoins and leans more toward traditional finance. Copy-trading has larger volumes and will likely become a major component of Web3 broker services.

One notable player in broker-led copy-trading is Logearn—the world’s first decentralized auto-investment/copy-trading middleware and a聚合-type decentralized copy-trading platform. It offers decentralized copy-trading SaaS solutions, fully integrating copy-data and processes across CEX, DEX, wallets, and communities, aggregating all industry copy-trading liquidity. This makes it easier for users to enter Web3 for investing or trading.

Fourth: Asset management tools. Crypto markets have historically offered high yields, keeping Web3 asset management projects highly popular. Platforms vary by holder control rights into centralized, decentralized, and semi-centralized models, differing in product design and technical approaches. Overall, Web3 asset management projects vary widely—short-term high-yield tools often perform poorly or incur losses over long cycles. Only those surviving full market cycles prove truly robust.

Enzyme launched in 2017, allowing managers to build custom portfolios and investors to choose specific fund managers. After launching V2, it supports nearly 200 assets, hosts over 1,300 portfolios, and manages around $1.7 billion in on-chain assets. However, since users in this space favor short-term high returns, Enzyme—despite being the leader in decentralized asset management—remains relatively small. This bull run might bring forth high-quality semi-centralized on-chain asset management projects.

Fifth: Underwriting, distribution, and OTC platforms. Platforms like Amber provide channels for non-crypto users to buy digital assets. However, there is currently no smart-contract-based OTC platform helping project teams complete token trades outside secondary markets.

January 11, 2024, marks a new epoch for Web3. In the future, compliant Web3 exchanges and brokers will work together to build more convenient trading infrastructure, attract massive external adoption of crypto assets, deliver warmer, more personalized trading experiences, aggregate liquidity across the entire cryptocurrency market, strengthen global blockchain consensus, and jointly welcome Web3’s blossoming era.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News