With 189,150 BTC accumulated, will MicroStrategy's strategy blow up?

TechFlow Selected TechFlow Selected

With 189,150 BTC accumulated, will MicroStrategy's strategy blow up?

As long as BTC continues to outperform the traditional world, MicroStrategy is unlikely to face a blowup.

Author: Liu Jiaolian

Recently, Michael Saylor, founder of MicroStrategy, tweeted that the company has once again increased its Bitcoin holdings—purchasing an additional 14,620 BTC at an average price of approximately $42,110. As of December 26, 2023, MicroStrategy has accumulated a total of 189,150 BTC at an aggregate cost of about $5.9 billion, with an average acquisition cost of roughly $31,168 per BTC.

Simple calculations show that, based on Bitcoin's current spot price of around $43,000, MicroStrategy’s position is sitting on an unrealized gain of (43,000 - 31,168) / 31,168 = 38%, translating to a gross profit of over $2.2 billion.

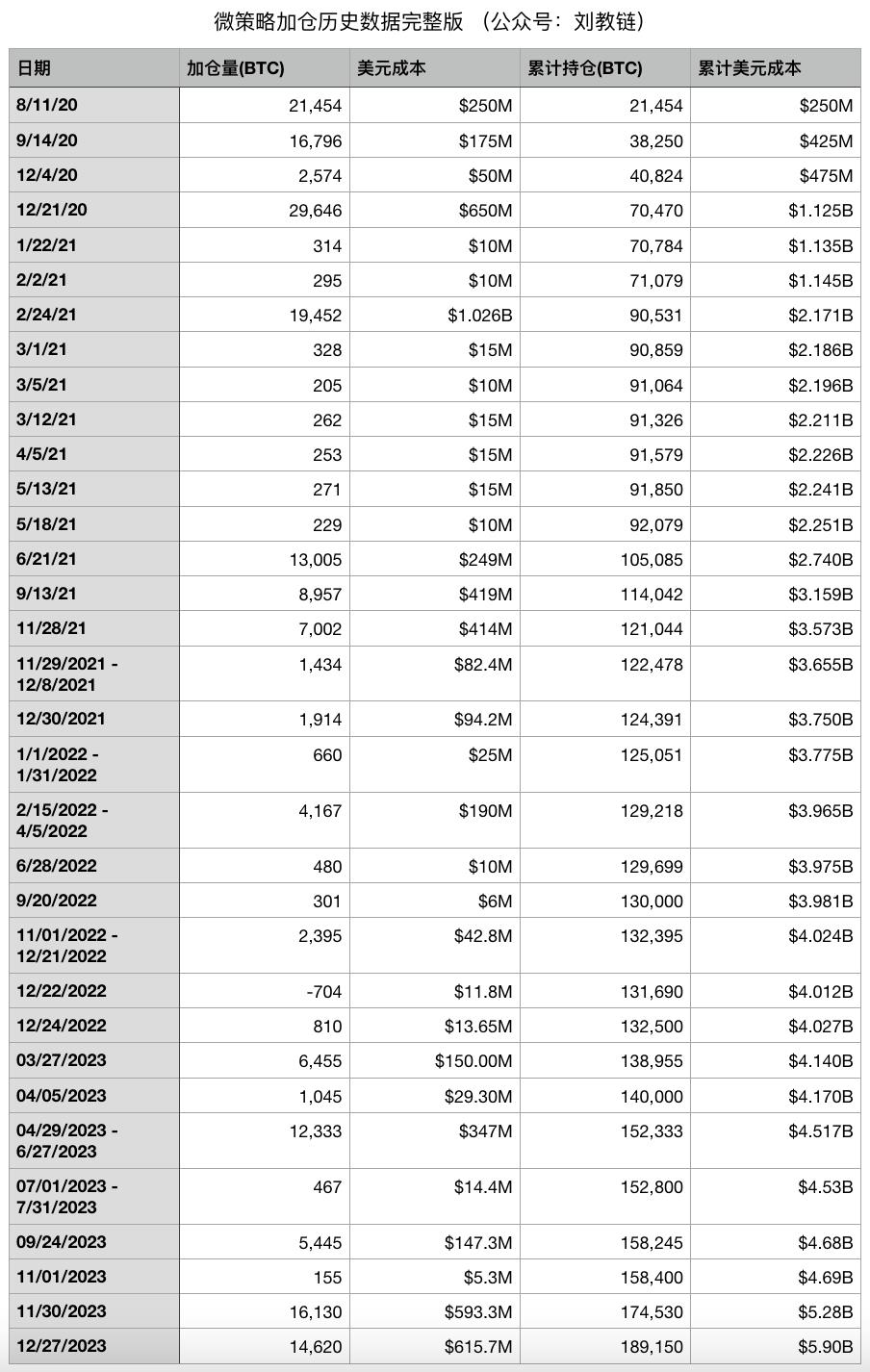

Jiaolian has compiled MicroStrategy’s complete history of Bitcoin purchases from early August 2020 to the end of December 2023 as follows:

Since buying its first batch of BTC at the end of 2020, MicroStrategy has consistently added to its position through bull and bear markets—accumulating during the peak of the 2021 bull market and continuing through the depths of the 2022 bear market, climbing over snow-covered mountains and walking across grasslands, enduring hardships, and finally achieving initial success.

From a long-term perspective, the only effect of a bull market is to raise the average cost basis for accumulation. So for long-term accumulators who continuously buy, which kind of journey is better—a broad plateau-like bull market (like in 2021), or a sharp mountain-like bull market (like in 2017)?

Interestingly, MicroStrategy’s strategy of steadily accumulating BTC regardless of market conditions is also the only approach truly suitable for the vast majority of retail investors.

However, upon closer inspection, MicroStrategy actually engages in several "more professional" moves beyond what ordinary retail investors can do.

First, lending out holdings.

Michael Saylor has stated multiple times that MicroStrategy will hold onto their BTC forever and never sell.

Yet, he also disclosed in late 2021 that MicroStrategy lends its BTC to hedge funds.

That means while MicroStrategy itself never sells, the hedge funds borrowing the BTC certainly do trade it—buying and selling repeatedly to perform arbitrage.

This is similar to how the U.S. Treasury or Federal Reserve does not sell its gold reserves but may lend them to investment banks like JP Morgan to act as market makers in the gold market.

Here lies an additional risk: if a hedge fund mismanages the borrowed BTC and incurs losses, becomes unable to repay, and goes bankrupt, MicroStrategy might fail to recover the full amount of BTC lent out, resulting in a net loss of BTC quantity.

In the long run, it's inevitable that some hedge funds will lose the borrowed assets.

Some people may deposit their digital assets on financial platforms to “earn interest,” which is somewhat analogous to what MicroStrategy does. The risk here, of course, is that the platform could suffer losses or even disappear entirely.

Second, off-exchange leverage.

In previous years, MicroStrategy issued certain long-term junk bonds—some even zero-interest—with maturities extending several years into the future, mostly around 2027–2028. Michael Saylor firmly believes that BTC’s price will be significantly higher in a few years, enabling MicroStrategy to repay these debts and cover any required returns upon maturity.

It is reported that MicroStrategy currently holds about $2.2 billion in debt, while the current market value of its BTC holdings stands at approximately $8.1 billion—meaning roughly $27 in debt for every $100 worth of BTC. This calculation excludes other business assets of MicroStrategy. These are off-exchange obligations; unless BTC drops below $11,000 around the maturity date in 2027–2028, its BTC holdings should fully cover the debt.

However, if MicroStrategy were forced to liquidate such a large volume of BTC to repay debt, it could deliver a significant blow to the market.

Many individuals holding mortgages may find themselves in a situation somewhat similar to MicroStrategy’s use of off-exchange leverage. Of course, mortgages require monthly interest payments at relatively high and floating rates (tied to LPR), making them far less favorable than MicroStrategy’s leverage. Nevertheless, a mortgage is nearly the best form of leverage available to the average worker.

Third, fundraising to accumulate.

Earlier this year, MicroStrategy conducted a secondary stock offering (MSTR) in the U.S. equity market, raising capital from public shareholders to purchase more BTC—using money from stock investors to increase their BTC stack.

Thanks to BTC’s strong performance this year, MSTR shares have risen significantly, allowing Michael Saylor to leverage share issuance as a funding mechanism for further accumulation.

Some have questioned whether, if BTC enters a downtrend or if MSTR decouples from BTC’s performance, MicroStrategy might be forced to sell BTC to prop up the stock?

But it’s important to understand the difference between equity financing and debt financing: equity carries no obligation to repay. So even if MSTR stock fell to zero, MicroStrategy could simply ignore it. Unless Michael Saylor has used shares as collateral—if so, then a sharp drop in share price could trigger margin calls and lead brokers to liquidate pledged shares. However, brokers cannot force MicroStrategy or Michael Saylor to sell BTC to meet margin requirements.

Grayscale’s persistent discount in 2022 already demonstrated this principle. Even at its worst, GBTC’s discount reached around -50%, yet Grayscale remained unmoved. At the time, many spread FUD claiming Grayscale would collapse. But Grayscale is a trust structure—legally insulated and impervious to creditor claims.

Grayscale’s trust holds 630,000 BTC—over three times the size of MicroStrategy’s holdings.

From a legal firewall standpoint, Grayscale’s structure is undoubtedly more robust than MicroStrategy’s.

Regardless, even if—as some netizens suggest—Bitcoin spot ETFs take away MSTR’s investor base, causing users to dump MSTR shares, leading to a decline in MSTR stock and potential decoupling from BTC, this does not necessarily mean MicroStrategy will be forced to sell its BTC holdings. If Grayscale doesn’t guarantee GBTC will track BTC perfectly, MicroStrategy certainly won’t promise MSTR will always mirror BTC either.

Here we must caution those investors treating MSTR as a de facto Bitcoin ETF on U.S. markets—they should be aware of the risk of decoupling and negative premium.

This strategy essentially uses rule-based mechanisms to shift risks onto external investors. For example, when GBTC traded at a deep discount, the risk was contained outside the trust firewall, wiping out speculators like Three Arrows Capital who bet on premium arbitrage. Similarly, MSTR could also fall into a discount, and since equity financing severs any guaranteed return, the risk is isolated within the U.S. stock market, leaving public investors to bear the losses.

For ordinary individuals, such non-recourse funding channels to raise capital for BTC accumulation are generally unavailable.

Fourth, off-chain income.

Don’t forget: MicroStrategy itself operates real businesses and generates ongoing business revenue. It has a steady stream of off-chain cash flow supporting its accumulation efforts.

This aspect is actually quite similar to most individual Bitcoin holders. The optimal strategy remains earning income off-chain and using those earnings to accumulate more BTC.

In summary, it’s clear that MicroStrategy leverages certain financial tools—tools inaccessible or far superior to those available to average retail investors—to enhance its BTC accumulation. Therefore, it’s highly probable that MicroStrategy outperforms most individual holders. Their excess returns stem from structural advantages.

Analysis suggests that due to its aggressive leverage strategies, MicroStrategy could potentially lose part of its BTC holdings under extreme black swan scenarios, possibly underperforming pure BTC-denominated holdings. However, as long as BTC continues to outperform the traditional financial world, MicroStrategy is unlikely to face catastrophic failure.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News