How will modularity and rollups affect Ethereum?

TechFlow Selected TechFlow Selected

How will modularity and rollups affect Ethereum?

How will modularity, rollups, account abstraction, and restaking impact Ethereum?

Author: Christine Kim, Vice President of Research at Galaxy

Translated by: Chief Villager of Elephant Mountain, Carbon Value

Executive Summary

The upcoming Ethereum Cancun/Deneb upgrade is expected to significantly reduce fees that rollup operators pay for block space, which will negatively impact revenue for Ethereum-based fee-generating protocols in the short term. ETH may underperform as a result, especially if Ethereum-based rollups increasingly interoperate with alternative settlement and data availability (DA) chains that offer superior performance and lower costs. In the long run, if modular blockchain theory proves correct, primary network fee drivers on layer-1 blockchains like Ethereum and Celestia will be layer-2 rollup service providers—not end users. Consequently, combined with the growing adoption of account abstraction on L2s, the main individuals holding ETH to pay for block space are likely to be rollup operators rather than end users.

Introduction

A longstanding challenge in the crypto industry is how to scale public blockchains while maximizing—or at least preserving—their decentralization and security properties. The recent launch of Celestia represents a maturation of new solutions to the blockchain scalability trilemma. Celestia is the first highly optimized public blockchain designed specifically to provide data availability (DA) for rollups. As a DA layer, Celestia lacks native transaction execution capabilities. Instead, it provides block space for rollups to temporarily publish batches of user transaction data. Using techniques such as data availability sampling (DAS), Celestia reduces the cost of block space dedicated to execution layers—such as smart contract rollups posting data on behalf of on-chain users.

Ethereum is also working to reduce the cost of block space used for DA purposes, albeit at the expense of higher node requirements. Proto-Danksharding is the primary code change included in Ethereum’s next network upgrade, known as Cancun/Deneb, which is expected to increase temporary data storage capacity per Ethereum node by 768kB. This additional block space for rollup transactions is estimated to reduce Ethereum’s DA costs by at least an order of magnitude.

At the core of modular blockchain theory is the idea that public blockchains should not perform all essential functions of general-purpose computation within a single network (i.e., the monolithic or integrated blockchain model). Instead, responsibilities such as execution or data availability should be outsourced to specialized infrastructure providers to enhance functionality and performance.

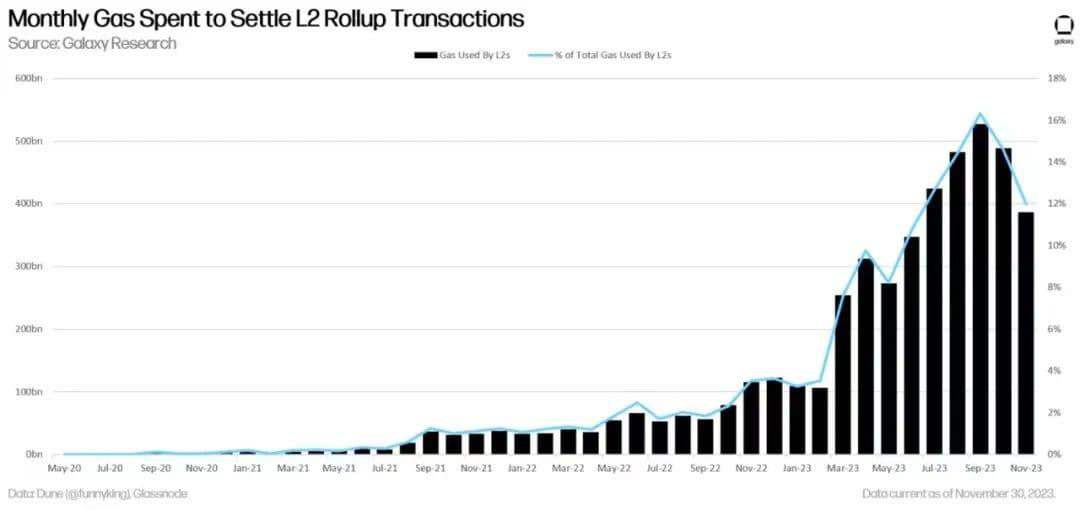

As Ethereum upgrades its network to better support Layer 2 rollups, protocol revenue from rollup sequencers—the entities responsible for publishing user data from end users to the DA layer—could eventually surpass that from direct L1 end users. Currently, rollups account for 12% of gas paid on Ethereum, up from 3% at the beginning of the year.

Monthly Gas Spent on Settling L2 Rollup Transactions

This report explores both the short- and long-term prospects of value accrual from L2 rollups to L1 public blockchains, factoring in the impacts of re-staking and account abstraction. The activation of near-term upgrades like Cancun/Deneb, coupled with increasing flexibility for L2s to migrate away from using Ethereum as their settlement and DA layer, could negatively affect Ethereum's value proposition in the short term. However, in the long term, as rollup technology matures and Ethereum enhances its DA capabilities, Ethereum is poised to outperform.

This report extends our previous research paper on modular blockchain theory titled "The Significance of Blockchain Modularity," which introduces many terms and concepts related to modularity and offers deeper insights into fee generation and revenue drivers in layered blockchain architectures—we recommend reading that paper as a primer before engaging with this one.

L2 Adoption in 2023

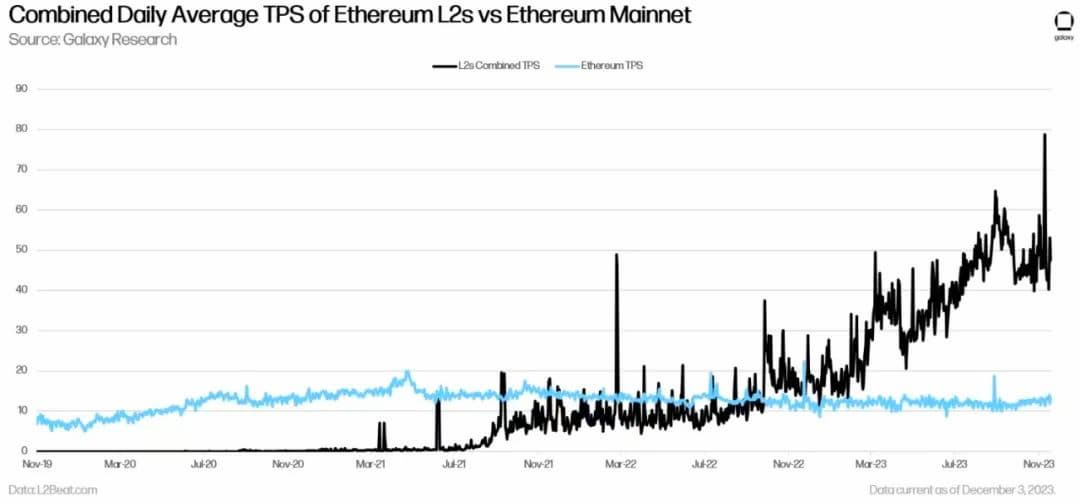

Since January, transaction activity on Ethereum L2s has more than tripled. In 2023, both nominal and percentage growth in daily transaction volume on L2s reached their highest levels to date.

Daily TPS Sum of Ethereum L2s vs. Ethereum Mainnet

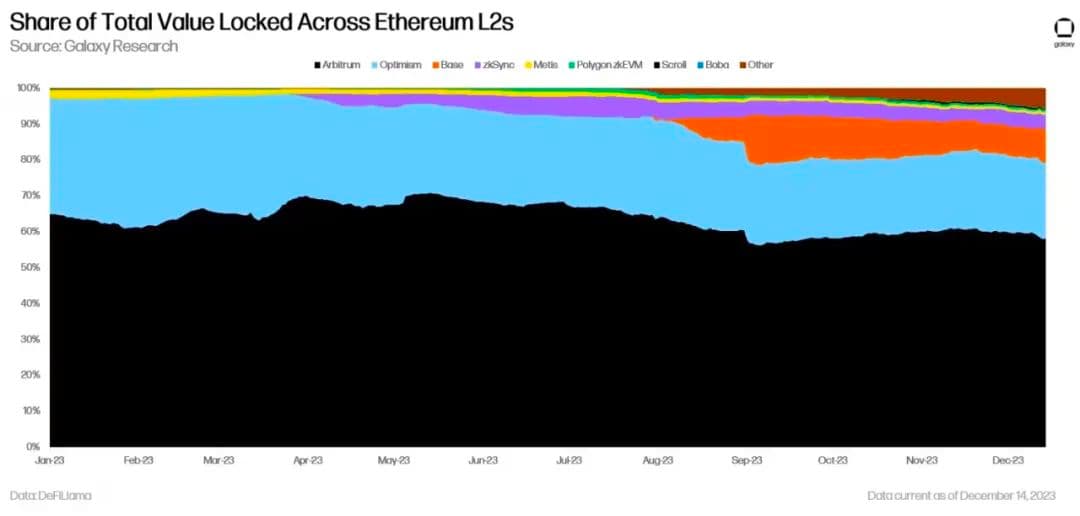

Among L2s, Optimism and Arbitrum saw the largest declines in total value locked (TVL) share on Ethereum L2s in 2023, dropping 11% and 7%, respectively. Base and zkSync Era experienced the greatest gains, with TVL shares increasing by 9% and 4%. (Note: TVL metrics are based on token dollar values and do not necessarily reflect changes in the nominal number of tokens deposited into protocols.)

Share of Total Value Locked in Ethereum L2 Ecosystem

Notably, Base, a rollup launched this year by cryptocurrency exchange Coinbase, has rapidly gained adoption and popularity among L2 users. As of December 12, Base ranks third in TVL among Ethereum L2s. In terms of transaction volume, Base occasionally exceeds daily transaction counts of Arbitrum and Optimism—the two most widely used L2s by TVL.

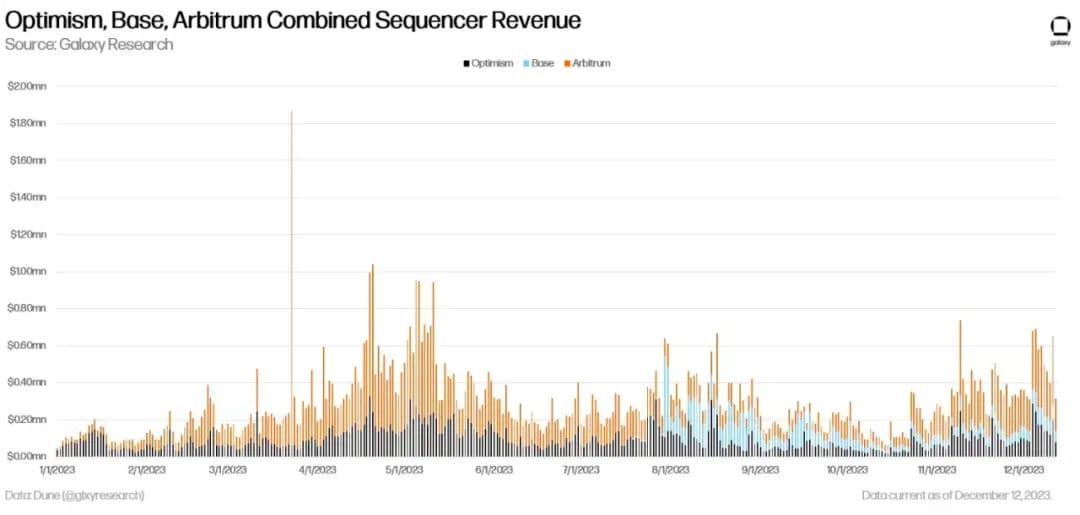

Among the top three Ethereum L2s by TVL, the Base sequencer generates approximately 20% of total revenue by ordering user transactions and batching them into blocks. To date, sequencers on Optimism, Base, and Arbitrum have collectively earned $140 million in user fee revenue.

Combined Sequencer Revenue of Optimism, Base, and Arbitrum

Looking ahead to 2024, the activation of the Cancun/Deneb upgrade will drastically reduce the cost of batching and settling user transactions on Ethereum, thereby increasing rollup sequencer profit margins while decreasing Ethereum’s fee income.

Cancun/Deneb Upgrade

The key code change in the Cancun/Deneb upgrade is Ethereum Improvement Proposal (EIP) 4844, also known as Proto-Danksharding. Native Proto-Danksharding creates dedicated block space for rollup transactions. These transactions, known as “blobs,” will be priced according to a separate fee market distinct from regular user transactions and will only be stored temporarily on-chain for about three weeks. With EIP-4844 activated, each block will include an additional 768KB of data space for rollup use.

The Cancun/Deneb upgrade could reduce Ethereum’s fee revenue in the short term, as EIP-4844 is expected to cut rollup operators’ block space costs on Ethereum by more than tenfold. Additionally, due to ongoing technical challenges around scalability, decentralization, and interoperability in rollup technology, much of Ethereum’s fee revenue may continue to come from end users transacting directly on L1 rather than from L2s. Until rollup technology matures, Ethereum is unlikely to see significant revenue benefits from EIP-4844.

Short-Term Technical Challenges

Below are three key development areas prioritized by rollup operators in 2023 and expected to remain focal points in 2024:

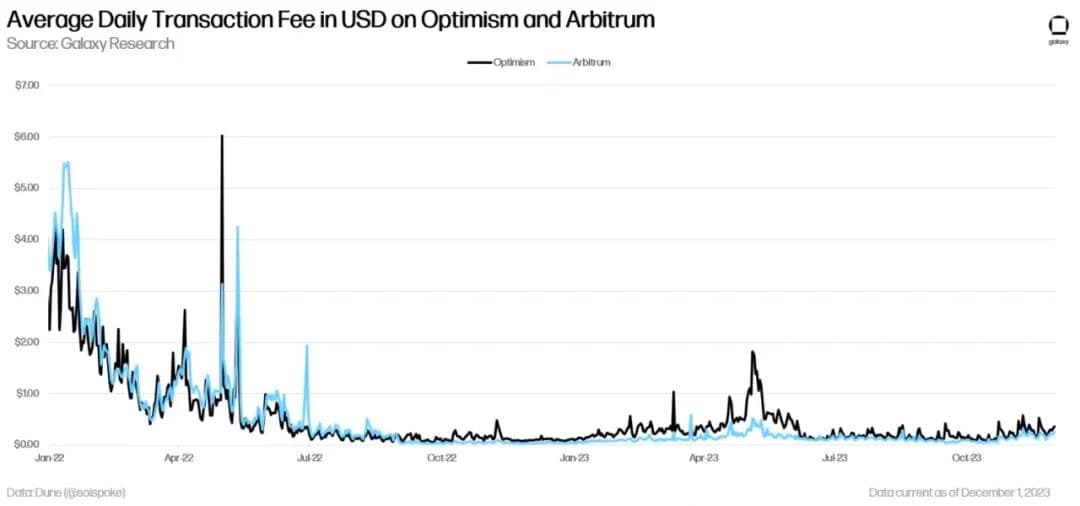

Scalability: Rollups are not immune to fee volatility. As highlighted in our earlier report on blockchain modularity, in June 2022, when Project Galxe’s Arbitrum Odyssey marketing campaign triggered massive on-chain activity, transaction fees on Arbitrum—the L2 with the highest TVL on Ethereum—briefly exceeded those on Ethereum itself. Since then, Arbitrum fees have declined significantly, particularly after the Nitro upgrade in August 2022.

Optimism’s Bedrock upgrade, completed in June 2023, was similarly aimed at improving network scalability and reducing gas fees. Scalability remains an active area of developer focus and innovation for rollups.

Daily Average Transaction Fees on Optimism and Arbitrum (USD)

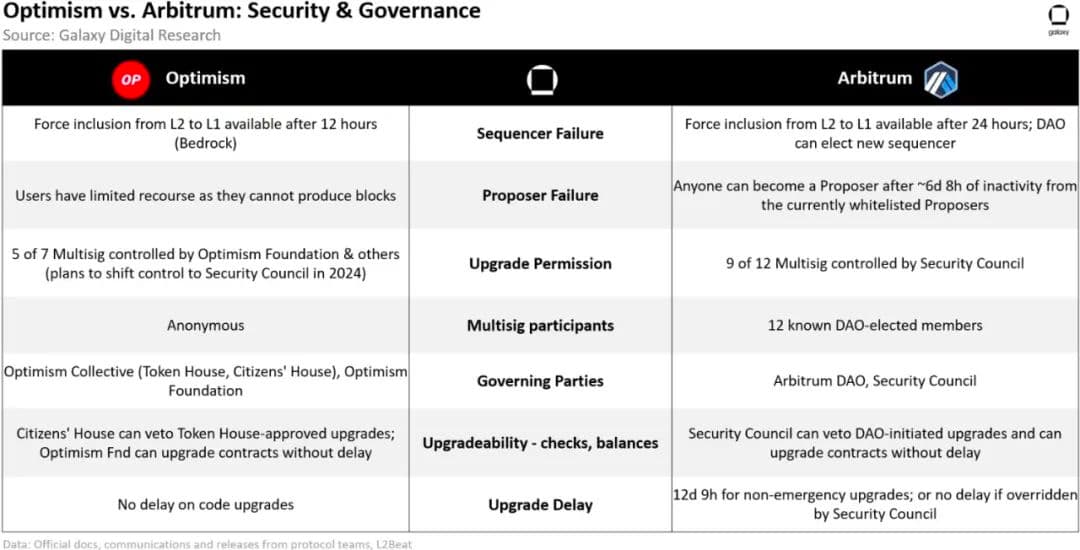

Decentralization and Security: Another major focus area for rollup development is decentralization. All cryptocurrencies on Ethereum remain vulnerable to centralization risks because they currently rely on a single node operator to order transactions and produce blocks. Key efforts to improve decentralization and security include: (i) implementing validity/fraud proofs, (ii) expanding the set of validators and sequencers, and (iii) removing admin keys and distributing rollup control through governance.

Optimism & Arbitrum: Security and Governance

Interoperability: One of the main reasons Ethereum dominates the general-purpose blockchain market is its strong network effects. As more users join Ethereum, liquidity for assets interacting on Ethereum increases, reinforcing the network’s value in a positive feedback loop. This fragmentation of liquidity presents a barrier to rollup adoption. Decentralized finance (DeFi) ecosystems benefit from concentrated liquidity and composability of dApps on a single protocol. Therefore, enabling seamless asset migration from L1 to L2—and across different L2 ecosystems—is a critical development area that will help drive user migration from Ethereum to L2s.

Advantages of Alternative DA Solutions

In the short term, Ethereum’s revenue will still primarily come from transactions initiated directly by end users on L1. As cost savings from L2 scalability upgrades grow and rollup decentralization and interoperability improve, user adoption of L2s will increase. Moreover, crypto companies choosing alternative decentralized DA layers like Celestia can achieve higher profitability simply by passing on part of their cost savings to users. Beyond Ethereum and Celestia, other L1 blockchains such as NEAR have announced plans to better serve rollups as DA layers.

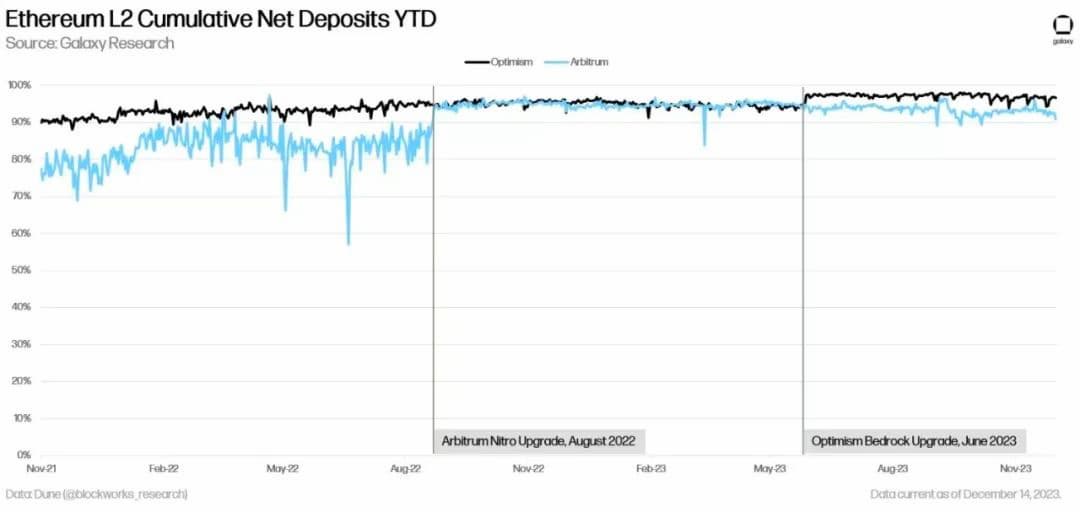

As shown below, users on L2s can spend over 90% less on transaction fees compared to users on Ethereum:

Cumulative Net Deposits on Ethereum L2s Year-to-Date

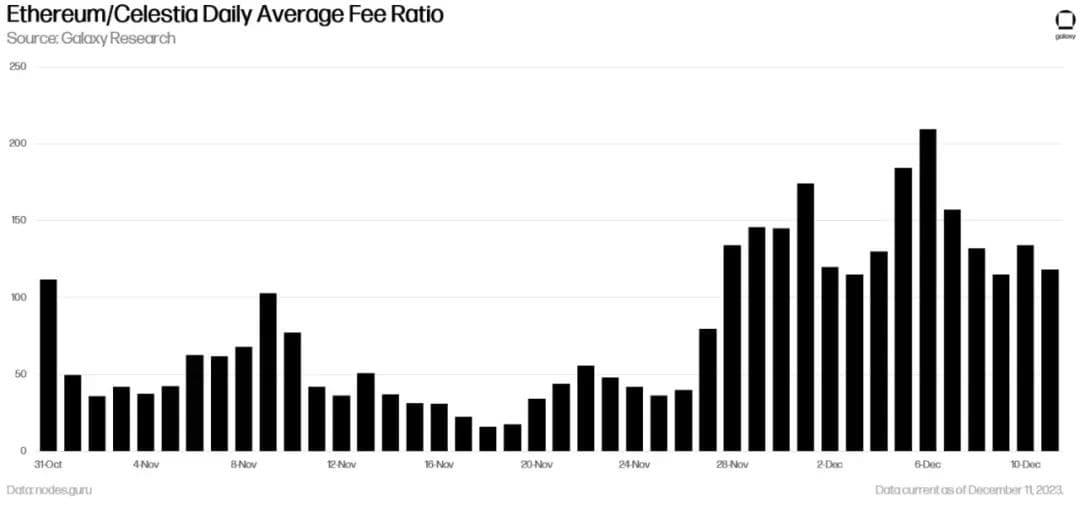

By publishing user transaction data from rollups onto Celestia instead of Ethereum, rollup operators can enjoy higher profit margins due to lower transaction fees on Celestia. On average, fees on Celestia are multiple times cheaper than on Ethereum, though this is partly due to Celestia being a relatively new chain, having launched on mainnet on October 31, 2023. The chart below shows the fee ratio between Celestia and Ethereum based on daily average transaction fees (in USD). Celestia’s daily transaction fees are, on average, 80 times cheaper than Ethereum’s. (Note: The following data reflects all types of user transaction fees on Celestia and Ethereum, not just fees paid by rollup sequencers.)

Average Daily Fee Ratio: Ethereum vs. Celestia

As a nascent blockchain live for less than two months, Celestia has not yet been widely adopted by L2s for DA. Most of Celestia’s current transaction activity consists not of blob confirmations but of staking and delegation activities involving Celestia’s native asset. As blob transaction volume increases on Celestia, fees may fluctuate and trend upward. However, given Celestia’s optimization for DA—a feature currently absent on Ethereum—rollup costs on Celestia are unlikely to exceed those on Ethereum under comparable conditions.

In summary, we expect Ethereum’s network revenue to decline—or at least remain below what it would have been without the upgrade—following the 2024 activation of the Cancun/Deneb upgrade due to reduced block space costs. Furthermore, due to persistent scalability, decentralization, and interoperability challenges facing rollups, a majority of Ethereum’s network revenue is expected to continue coming from end users rather than L2s. Lastly, if sequencers retain some of the cost savings instead of fully passing them to users—or opt for alternative rollup solutions like Celestia—rollup profit margins are expected to rise in the short term.

Long-Term Outlook

Over a five-year or longer horizon, as blockchain applications and services achieve mass adoption, Ethereum’s revenue could rise substantially, with rollup usage for transaction execution potentially exceeding Ethereum’s by 10x or more. Lower L2 fees could unlock new use cases for blockchain applications across gaming, social media, entertainment, sports, and beyond. These new use cases, expected to drive broader adoption of blockchain-based applications (also known as decentralized applications or dApps), will likely increase overall demand for Ethereum block space, thereby boosting Ethereum’s total revenue. In this scenario, Ethereum’s primary revenue source would be rollup services leveraging it as a settlement and DA layer. Additionally, as competition intensifies among end users, rollup sequencers’ profit margins are expected to compress.

In the coming years, the emergence of multiple highly optimized DA layers may accelerate the shift of Ethereum L2s from exclusively publishing data to Ethereum toward cheaper alternative DA layers. These new DA layers could eventually challenge Ethereum more directly, potentially weakening Ethereum’s current status as the dominant foundational layer for rollups. However, as discussed earlier, network effects matter. Rollup developers are actively improving interoperability and composability between dApps deployed across different rollup protocols. Projects like Caldera, Hyperlane, and Polymer are building tools to enable rollups to operate seamlessly across multiple DA layers without compromising user experience. So long as shared settlement and DA layers like Ethereum continue to offer advantages in user experience—particularly in facilitating asset transfers across different rollups and their hosted dApps—Ethereum is likely to maintain its dominance as the most valuable DA layer.

Ethereum’s Competitive Advantages

Although Ethereum dominated the 2023 market as the settlement and DA blockchain with the highest security, value, decentralization, and network effects, competition from Celestia and other blockchains designed from inception to support rollup activity is intensifying. While Celestia currently lags behind in scale and maturity compared to Ethereum, over time there is a risk—albeit small—that Ethereum’s dominance as the leading DA blockchain for rollups could erode. To counter this, Ethereum core developers are pushing forward with the Cancun/Deneb upgrade to strengthen Ethereum’s DA capabilities. However, when assessing the long-term impact of L2 rollups on Ethereum’s revenue, one must consider the possibility that rollups may never deliver the same level of decentralization, security, and interoperability as the base layer.

Despite their lower fees, the fragmentation of application-layer liquidity across L2 rollups may anchor most user transaction activity on Ethereum in both the short and long term. In such a case, even if Celestia performs better as a DA layer, Ethereum’s competitive advantage as the world’s most decentralized general-purpose blockchain may prevail and continue attracting new users. Under this scenario, Ethereum’s revenue would remain highly volatile and dependent on the number of users interacting with applications directly on its base layer. Some users may choose to transact on Ethereum despite cheaper L2s and alternative L1s, valuing its unmatched decentralization and security as a general-purpose blockchain.

As previously noted, in the short term, if most end-user activity remains on Ethereum rather than migrating to L2s, high fees and a temporary spike in network revenue could occur. However, without scalability, Ethereum’s revenue will remain constrained by limited transaction throughput and unpredictable due to insufficient block space to meet new demand. Short-term revenue gains driven by user payments will ultimately be hampered by the network’s inability to support larger-scale user activity, negatively impacting Ethereum’s long-term value as a general-purpose blockchain.

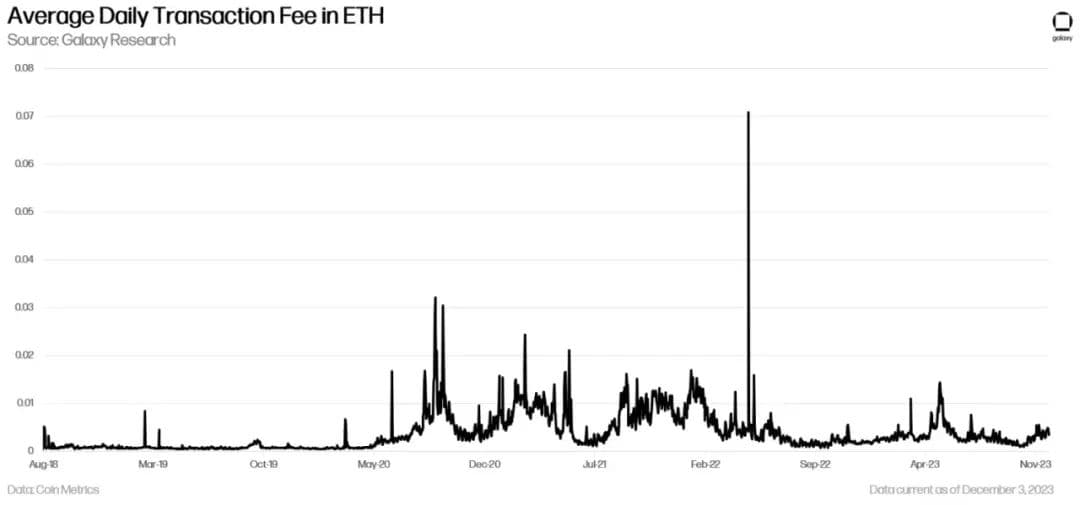

The chart below illustrates fluctuations in Ethereum’s daily average transaction fees denominated in ETH:

Daily Average Transaction Fees in ETH

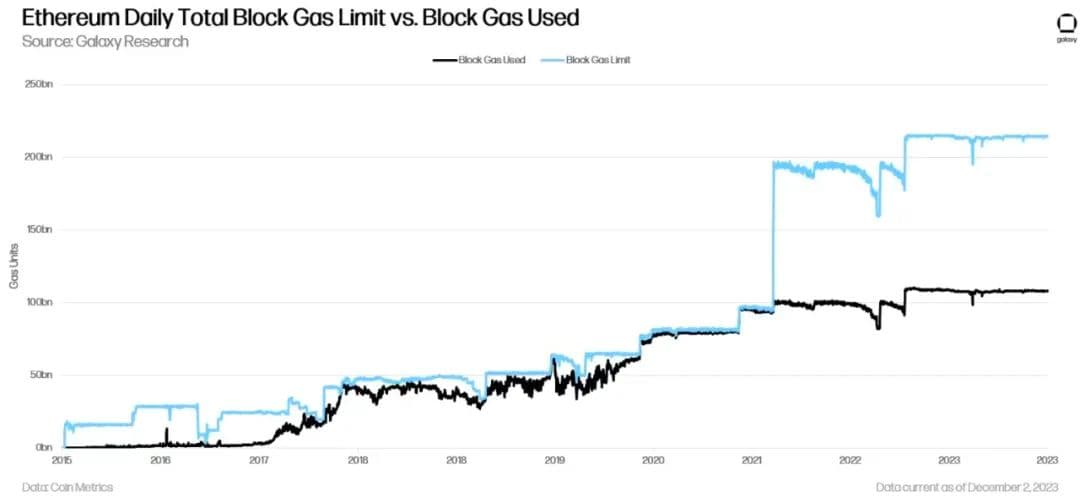

During the first six years of Ethereum’s existence, miners collectively voted to increase the block gas limit, effectively raising the number of transactions per block by at least 12x. In August 2021, Ethereum core developers executed a hard fork—an incompatible network-wide upgrade—that doubled the maximum block gas limit from 15 million to 30 million and restructured the fee market to reduce fee volatility.

The chart below illustrates how Ethereum’s block gas limit has increased since its inception due to overwhelming user demand for block space:

Ethereum Daily Total Block Space Limit vs. Used Block Space

Despite these historical adjustments to Ethereum’s block gas limit, fee volatility and limited network scalability remain persistent issues. If rollups fail to effectively inherit the bulk of end-user activity over the long term, a sustainable solution will be required.

Additional Considerations

Two additional factors worth discussing regarding long-term value accrual from L2s to L1s are the trend of native account abstraction on L2s and restaking solutions on Ethereum.

Account Abstraction

If L2 rollup sequencers become the intermediary service through which end users interact with blockchain-based applications—rather than interacting directly with Ethereum—then in the future, users may no longer need to hold ETH directly. Instead, they could pay transaction fees in stablecoins or even fiat currency, depending on the sequencer and rollup design, with the rollup sequencer converting these payments into ETH on behalf of users to cover Ethereum transaction fees.

Increased flexibility and programmability in how fees are paid on L2s is primarily enabled by a technology called “account abstraction,” which has not yet been implemented on Ethereum and is unlikely to be prioritized in the near future. While Ethereum core developers recognize its benefits, coordination is lacking, and implementation has not been prioritized over other urgent upgrades such as increasing validator maximum effective balance, Verkle trees, Ethereum Virtual Machine Object Format (EOF), and proposer-builder separation (PBS).

Although proposals exist to implement account abstraction without modifying the core Ethereum protocol (e.g., ERC-4337), widespread adoption is unlikely, as it requires dApp developers to update their smart contracts and users to adopt alternative mempools. In contrast, as an emerging technology, rollups serve as ideal testbeds for natively implementing account abstraction at the protocol level. Currently, rollups like zkSync and Starkware have already done so, meaning user accounts created on these protocols automatically gain enhanced programmability and usability.

Native account abstraction on rollups transforms the user experience when interacting with dApps, unlocking new functionalities for user transactions, including but not limited to:

Improved experience for recurring or frequent transactions: For certain on-chain games and DeFi applications, users often submit multiple transactions. Accounts can be programmed to automatically authorize interactions with specific dApps, eliminating the need for repeated private key approvals for the same smart contract.

Ability to halt fund outflows during hacks: Embedded logic can pause withdrawals if a user’s account exceeds a predefined threshold.

Support for social recovery of private keys: User accounts can be designed to rely on a combination of private keys and social recovery mechanisms to transfer funds. If a user loses their private key, the account can be programmed to regenerate a new key using a threshold (e.g., 2-of-3 or 3-of-5) of other recovery devices.

Restaking

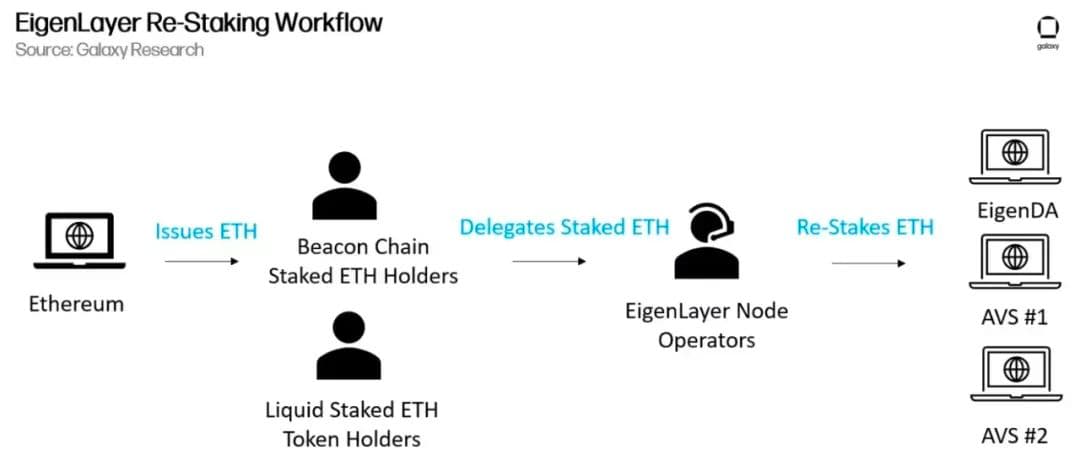

Another factor relevant to Ethereum’s rollup value accrual over the next five years is the maturation of restaking protocols like EigenLayer. As explained in Galaxy Perspectives’ article on restaking, EigenLayer enables users to reuse their staked ETH to secure other protocols and dApps, thereby earning higher yields. As of December 2023, EigenLayer developers are testing the restaking workflow for EigenDA—a supplementary DA layer secured by staked ETH—allowing rollup operators to post data to EigenDA instead of directly to Ethereum. Validator node operators who choose to restake via EigenLayer will face additional slashing conditions when validating transactions on both Ethereum and EigenDA, but in return, they earn staking rewards from two protocols instead of one. The EigenLayer team expects to launch EigenDA on mainnet in the first half of 2024. Subsequently, new protocols will be added, allowing validator node operators to restake across multiple AVSs beyond EigenDA.

EigenLayer Restaking Workflow Diagram

Restaking protocols like EigenLayer may take several years to mature and achieve broad adoption on Ethereum. The first active validation services (AVS) on EigenLayer will initially be curated and rigorously tested. EigenLayer developers are intentionally limiting the amount of ETH and liquid staking tokens that can be deposited into the protocol. Currently, the EigenLayer team has set an initial cap of 117,000 ETH for liquidity restaking into the EigenDA AVS. By December 18, 2023, this cap will increase to approximately 200,000 ETH. Additionally, on December 18, EigenLayer will begin accepting deposits from six new liquid staking tokens: osETH, swETH, oETH, EthX, WEBETH, and AnkrETH.

As of December 14, 2023, the total amount of staked ETH—including liquid staking tokens like rETH, stETH, and cbETH, as well as native ETH—deposited into EigenLayer represents less than 1% of the total ETH staked on Ethereum. Over time, the EigenLayer team will gradually increase deposit capacity for EigenDA and other AVSs to ensure economic security for both Ethereum and associated AVSs is not compromised before the protocol is thoroughly tested. Full development of EigenLayer’s roadmap may take years and could encounter unforeseen bugs, especially as AVS pools expand.

To the extent that restaking becomes a reliable and scalable activity on Ethereum—similar to how liquid staking via protocols like Lido has become commonplace—reusing staked ETH to provide additional security for operations such as sequencing is expected to benefit rollups. Moreover, even as issuance to validator node operators declines over time, Ethereum’s staking yield is expected to rise, potentially increasing demand for ETH not only from rollup operators but also from DeFi applications and foundations. Even if ETH’s utility for executing transactions on Ethereum diminishes as rollup applications grow, restaking activities could still generate attractive yields, encouraging individuals and entities beyond rollup operators to buy and stake ETH.

Conclusion

Ethereum’s revenue will benefit from sustaining larger-scale transaction activity via L2s, although in the short term, the network may face declining revenue due to limited rollup adoption and upgrades that subsidize rollup costs. Because the imminent upgrade is expected to reduce rather than increase fee payments, ETH may underperform in the short term—at least from the perspective of investors valuing Ethereum based on its fee-generating protocol revenue.

Rollup technology remains nascent, facing technical challenges and adoption barriers in the short term. Over time, as rollups improve in scalability, decentralization, security, and interoperability, the majority of end-user activity may migrate from Ethereum to L2s. When this occurs, competition among L2s for users will intensify, and rollup operators’ profit margins may shrink.

In the long run, technologies like native account abstraction on L2s will further reduce the need for end users to directly hold ETH. More likely, with the presence of liquidity solutions and the maturation of restaking platforms like EigenLayer, end users and DeFi protocols will hold tokenized representations of ETH and their accrued yields. The primary holders of native ETH may become rollup operators, who use the token to purchase block space on Ethereum on behalf of end users. Further research areas related to L1 value accrual from L2s include the impact of maximum extractable value (MEV) on modular blockchain ecosystems and the evolution of zero-knowledge proofs in shaping rollup design, bridges, and economics.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News