Coinbase 2024 Crypto Market Outlook: Bitcoin's Dominance Further Strengthens, DePIN and Decentralized Computing Seen as Promising

TechFlow Selected TechFlow Selected

Coinbase 2024 Crypto Market Outlook: Bitcoin's Dominance Further Strengthens, DePIN and Decentralized Computing Seen as Promising

The foundation for a better cryptocurrency user experience is being built, which will help the industry bridge the gap from early adopters to mainstream users.

By Coinbase Research

Translation: TechFlow

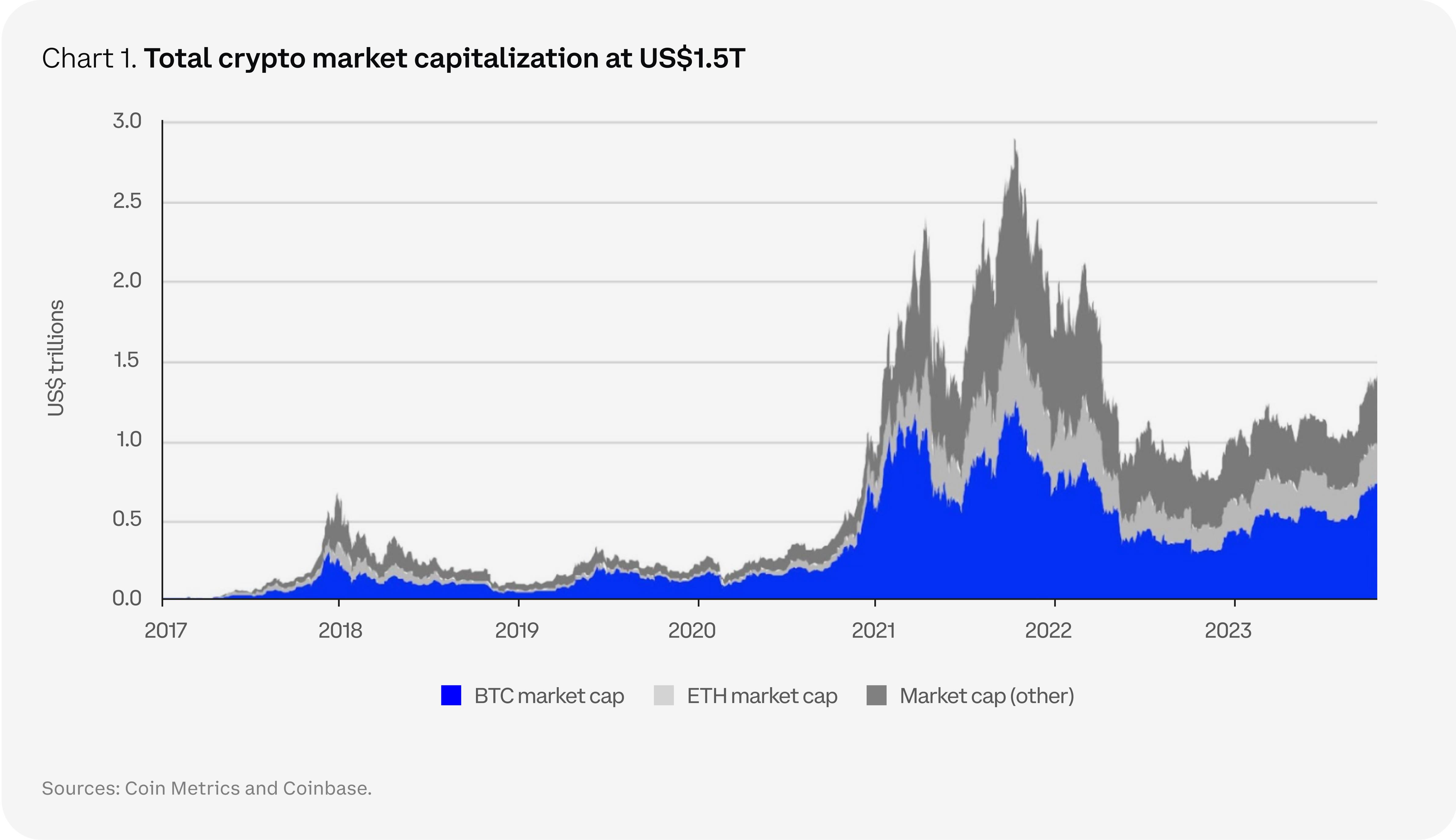

The total market capitalization of the cryptocurrency market doubled in 2023, indicating that crypto has survived the bear market and is now transitioning from bear to bull. Coinbase published a comprehensive report outlining the dominant narratives it expects to lead the crypto space in 2024, along with in-depth discussions on Bitcoin, Ethereum, stablecoins, and more.

Key Takeaways

-

Coinbase believes institutional investment will remain primarily focused on Bitcoin through at least the first half of 2024, driven in part by strong demand from traditional investors entering the market.

-

2024 will provide favorable macro conditions for risk assets, and critically, regulatory progress will continue to drive long-term crypto adoption.

-

Web3 developers will continue building real-world use cases, with foundational technologies already becoming evident.

-

The foundation for better crypto user experiences is being laid, helping the industry bridge the gap from early adopters to mainstream users.

Author's Note

The doubling of the total crypto market cap in 2023 suggests this asset class has emerged from its "harsh winter" and is undergoing transformation. That said, we believe it’s still too early to definitively label this shift—or view improved market sentiment as conclusive proof against crypto skeptics. What is clear, however, is that despite challenges within the crypto space, developments over the past year have exceeded expectations. This demonstrates that crypto is here to stay; the current challenge lies in seizing the moment to build a better future.

The catalysts behind crypto’s 2023 recovery were not innovations tied to its intrinsic value proposition. Instead, events such as the U.S. regional banking crisis and escalating geopolitical tensions reinforced Bitcoin’s status as a secure safe-haven asset. Additionally, spot Bitcoin ETF applications from some of America’s top financial institutions implicitly acknowledged crypto’s disruptive potential—possibly signaling clearer regulation ahead and helping eliminate frictions that previously hindered capital inflows.

Progress rarely follows a straight line. To build a more resilient market, Web3 developers must continue creating real-world use cases that help bridge the gap between early adopters and mainstream users.

The groundwork for these advancements is already visible—ranging from Web2-inspired products like payments, gaming, and social media, to crypto-native innovations such as decentralized identity and decentralized physical infrastructure networks (DePIN). The former are easier for investors to grasp but face fierce competition from established Web2 giants. The latter could reshape the technological landscape but require longer development timelines and broader user adoption remains distant. Nevertheless, blockchain infrastructure has made significant strides over the past two years, creating the necessary conditions for experimentation and innovation—bringing us close to an inflection point.

Asset tokenization is another critical use case currently attracting traditional finance players into the ecosystem. Full-scale rollout may take another 1–2 years, but renewed interest in tokenization reflects economic realities: today’s opportunity cost is higher than during the immediate post-pandemic period, making capital efficiency from instant settlement of repos, bonds, and other capital market instruments increasingly important.

Against this backdrop, we believe the long-term trend of institutional crypto adoption will accelerate. Indeed, rumors suggest Bitcoin’s late-2023 rally has already begun attracting a broader range of institutional clients—from traditional macro funds to ultra-high-net-worth individuals—into the crypto space. We expect the launch of spot Bitcoin ETFs in the U.S. to further accelerate this trend, potentially enabling the creation of more sophisticated derivatives built atop compliant, ETF-based underlying assets. Ultimately, this would improve liquidity and price discovery for all market participants.

We believe the above points represent some of the core themes shaping the crypto market in 2024, which we will explore in detail below.

Theme 1: The Next Cycle

Bitcoin Dominance

Market dynamics in 2023 largely unfolded as anticipated in our 2023 Crypto Market Outlook. A shift toward higher-quality digital assets led Bitcoin’s dominance to rise steadily above 50% for the first time since April 2021. This was largely due to multiple well-known and established financial giants applying for spot Bitcoin ETFs in the U.S., whose participation helped validate and strengthen crypto’s prospects as an emerging asset class. Although some capital may rotate into higher-risk segments of crypto next year, we believe institutional flows will remain firmly anchored in Bitcoin at least through the first half of 2024. Moreover, strong demand from traditional investors entering the market will make Bitcoin’s dominance difficult to shake in the near term.

Bitcoin’s unique narrative helped it outperform traditional assets in the second half of 2023, and we expect this trend to continue into next year. Unless broad risk-off environments trigger liquidity demands, we believe Bitcoin could perform well even under challenging macroeconomic conditions. For example, fiscal strength in the U.S. and elsewhere may limit restrictive monetary policies aimed at curbing capital stagnation. The U.S. commercial real estate sector appears vulnerable and could place renewed stress on regional banks. Both developments should reinforce Bitcoin’s long-term appeal as an alternative to the traditional financial system. All of this may amplify the deflationary narrative tied to Bitcoin’s halving event in April 2024.

A New Trading Regime

The previous crypto bear market (2018–2019) ended with the emergence of decentralized finance (DeFi) and the rise of multiple Layer 1 (L1) networks built ostensibly to meet anticipated demand for on-chain blockspace. Development activity on these platforms brought crypto further into the mainstream before overall activity stalled by the end of 2021. It later became evident that additional blockspace wasn’t necessarily required. In response to subsequent low expectations, developers used the bear market to build—focusing on overcoming technical barriers hindering new blockchain use cases.

The first phase of this progress involved building the infrastructure needed for a web3 future—such as scaling solutions (Layer 2s), security services (re-staking), and hardware (zero-knowledge proofs). These remain key investment opportunities in crypto, but arguably, much of the foundational infrastructure has already been established over the past two years. With this foundation enabling more decentralized applications (dapps), we believe the crypto trading regime will evolve accordingly. Specifically, we expect more market participants to focus on identifying promising web3 applications capable of bridging the chasm between early adoption and mainstream usage.

Many market participants rely on Web2 analogies—such as payments, gaming, and social media—to generate investment ideas within Web3. The industry has also seen the emergence of more uniquely crypto-native use cases, including decentralized identity, decentralized physical infrastructure networks (DePIN), and decentralized computing. We believe the challenge lies not only in identifying industries but also in picking winners. Achieving dominance in any given sector depends not just on first-mover advantage (though helpful), but on realizing and monetizing the right network effects. Before early 2004, at least six other social media platforms—including Friendster and MySpace—had achieved notable success but failed to match Facebook’s scale or recognition. Given the nascent nature of digital assets, we expect many market participants will increasingly rely on proxies and platforms to capture opportunities in the next cycle.

L1 Equilibrium

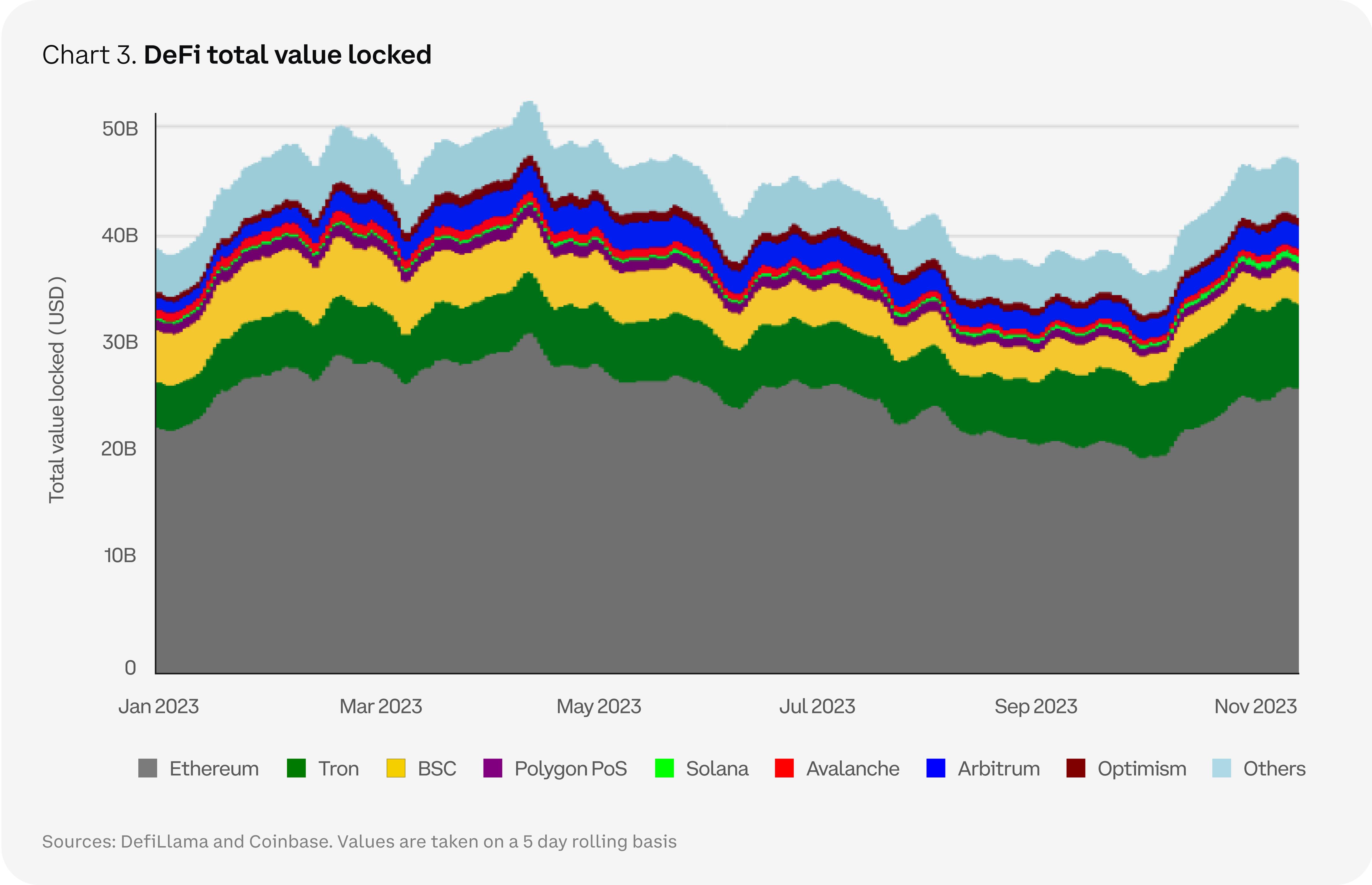

In our view, the moderation of on-chain activity over the past two years has reduced demand for L1s. Ethereum’s dominance among smart contract platforms remains solid, leaving little room for direct competition. Approximately 57% of the value locked across the crypto ecosystem resides on Ethereum, while Ethereum holds second place in overall crypto market capitalization at 18%, behind only BTC. As market participants increasingly focus on applications, we expect alternative L1s to reposition their networks to align better with shifting narratives. For instance, more industry-specific platforms have emerged—some focusing on gaming or NFTs (e.g., Beam, Blast, Immutable X), others on DeFi (e.g., dYdX, Osmosis), or institutional users (e.g., Avalanche’s Evergreen subnet, Kinto).

Meanwhile, the concept of modular blockchains has gained traction within the crypto community, with many L1s stepping in to serve one or more core blockchain components: data availability, consensus, settlement, and execution. Notably, Celestia launched on mainnet in late 2023, reigniting discussion around modular blockchain design by offering a plug-and-play data availability layer. Other networks and rollups can now publish transaction data via Celestia, guaranteed to be available on-chain for anyone to verify. Other EVM-compatible L1s are refocusing on smart contract execution, effectively transforming into Ethereum L2s—for example, Celo.

That said, integrated chains like Solana still hold significant positions within the crypto ecosystem, meaning the debate between modularity and integration will likely persist. We believe the trend toward increasing differentiation among chains—by industry or function—will continue into 2024. However, the ultimate value of these blockchains will still depend on which projects are being built atop them and how much usage they attract.

Evolution of L2s

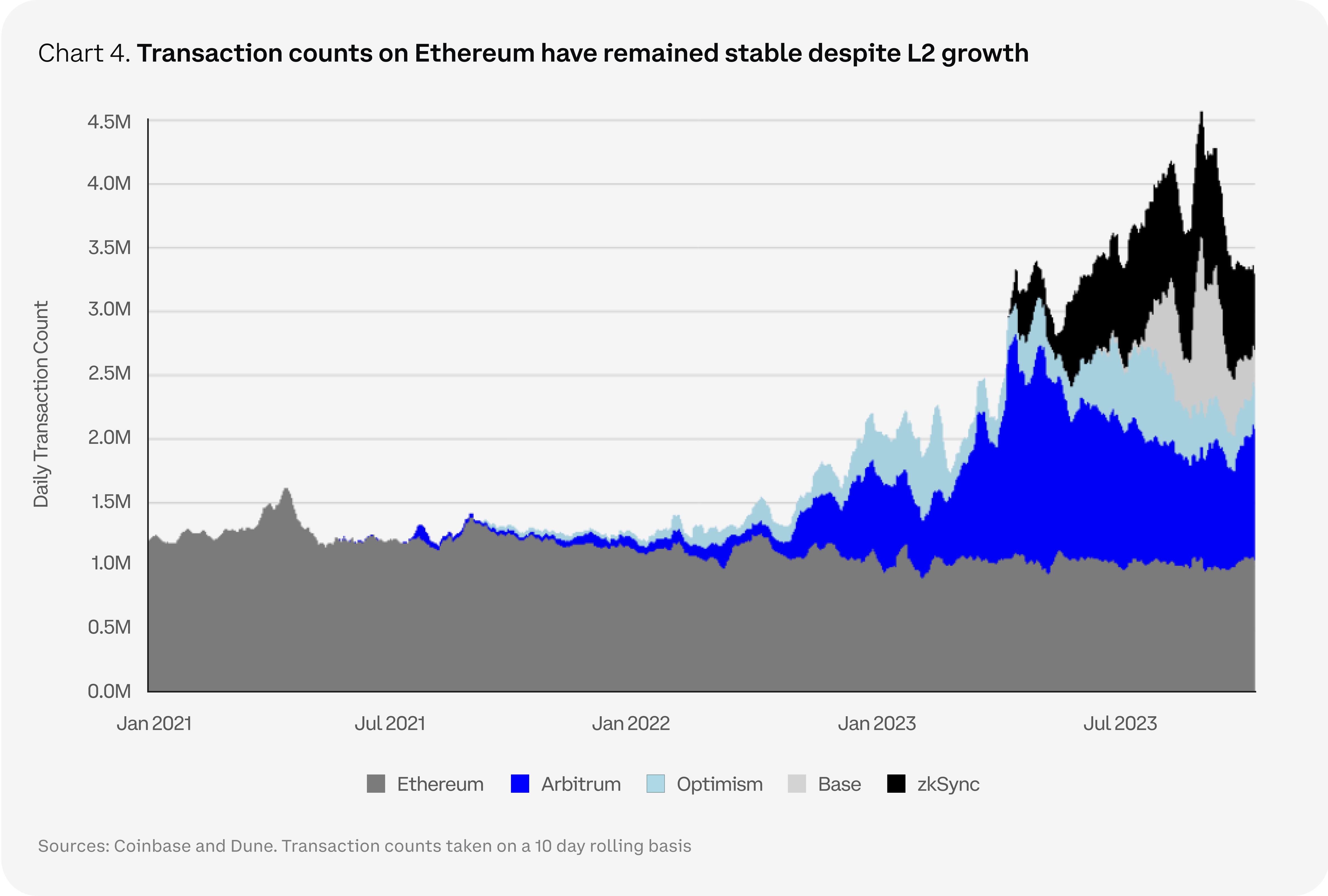

The rapid growth of Layer 2 scaling solutions has been fueled by new rollup stacks (like OP Stack, Polygon CDK, and Arbitrum Orbit) and the abstraction of functions into specialized layers. As a result, developers can now more easily build and customize their own rollups. However, despite the growing number of L2s, they have diverted almost no activity away from Ethereum’s mainnet—in fact, they’ve absorbed activity that might otherwise have occurred on competing L1s.

For example, comparing bridges connecting Ethereum L2s versus alternative L1s shows that the share of ETH locked in rollup bridges has grown from 25% of all bridged ETH in early 2022 to 85% by the end of November 2023. Meanwhile, although rollup usage has increased, the number of transactions on Ethereum remains relatively stable, averaging around one million per day. In contrast, the combined activity on Arbitrum, Base, Optimism, and zkSync currently averages over two million transactions daily.

Moreover, modular theory is manifesting uniquely in the L2 space. Eclipse attracted significant attention in 2023 for challenging existing conventions—it is a “general-purpose” scaling solution relying on a modular architecture. Notably, Eclipse leverages:

-

(1) Solana Virtual Machine (SVM) for transaction execution

-

(2) Celestia for data availability

-

(3) Ethereum for settlement (security)

-

(4) RISC Zero for zero-knowledge fraud proofs.

This is just one example of how we’re beginning to experiment with different (non-EVM) virtual machines at the execution layer—though the full impact on the ecosystem remains to be seen. With the upcoming Dencun fork expected in Q1 2024, we may also see a reduction in L2 transaction fees settled on Ethereum.

Theme 2: Resetting the Macro Framework

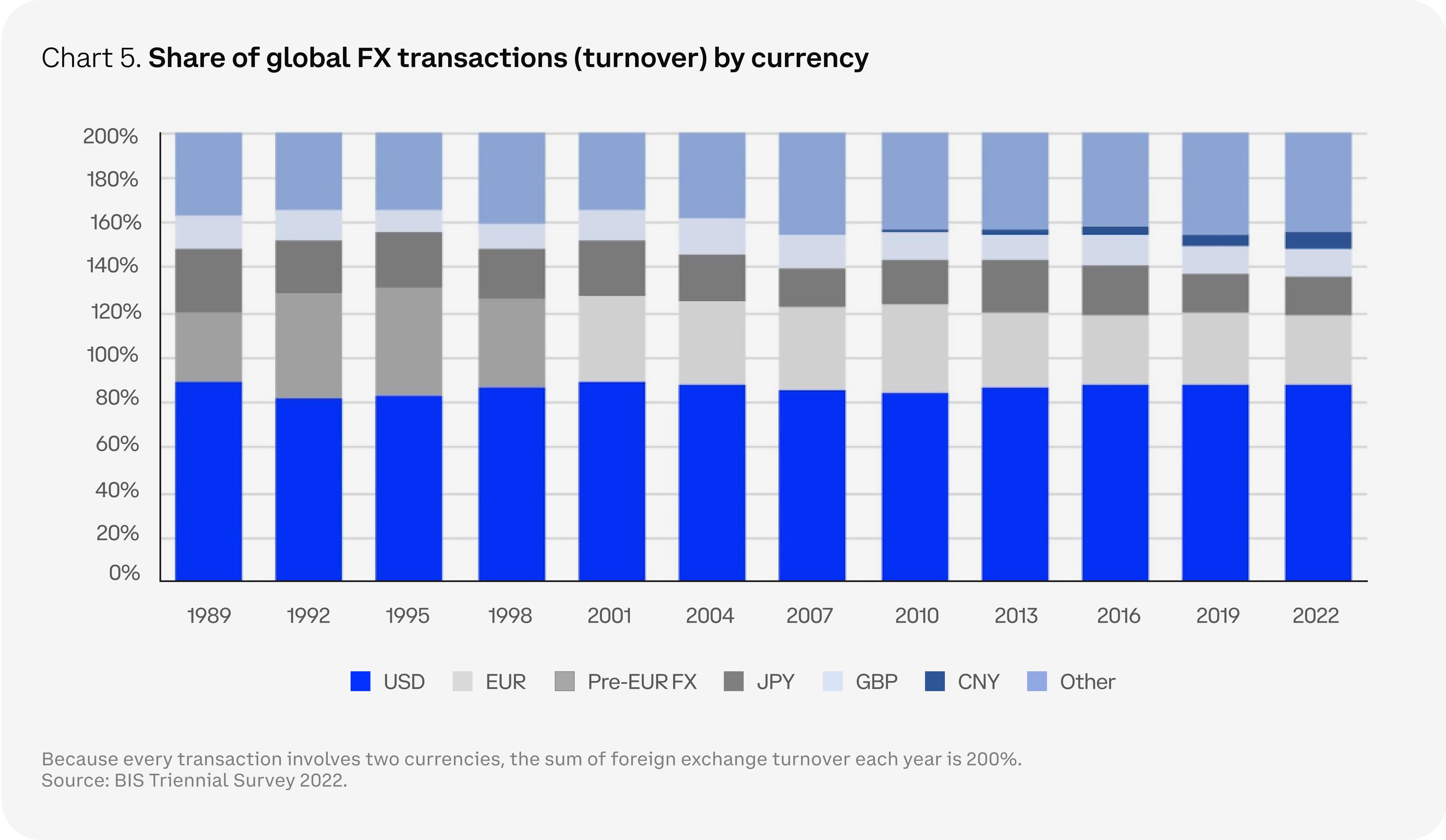

The Long Road to De-Dollarization

De-dollarization may remain a long-term theme in 2024, especially during an election year. However, the reality is that the dollar faces no immediate threat to its global dominance. Clearly, the dollar is at an inflection point. While full de-dollarization may take generations to unfold, the global monetary system has already begun moving away from dollar hegemony. U.S. macroeconomic imbalances continue to grow—Congressional Budget Office (CBO) projections indicate servicing the national debt will cost $1 trillion by 2028, or 3.1% of GDP. The CBO forecasts federal deficits will expand from an average of 3.5% of GDP over the next decade to 6.1%.

On the other hand, de-dollarization has been discussed since the early 1980s—and yet, the dollar remains the world’s reserve currency. In fact, the dollar’s oversized role in global finance and trade means it has consistently accounted for roughly 85–90% of international transactions over the past four decades. What has changed is that increasing U.S. sanctions—particularly those imposed on Russia following the Ukraine war—have weaponized global finance. This has accelerated interest in developing new cross-border payment solutions, as more countries enter bilateral agreements to reduce reliance on the dollar. For example, France and Brazil (among others) have started settling commodity trades in Chinese yuan. Additionally, central bank digital currency (CBDC) trials are expanding to bypass the cumbersome correspondent banking system.

Crypto advocates argue that Bitcoin and other digital stores of value play a crucial role in this emerging shift from a unipolar to multipolar world order. The value of holding a supranational asset—one not owned or controlled by any single nation—is self-evident. Monetary transitions typically occur during periods of socioeconomic upheaval—often only recognized in hindsight—such as paper money in 11th-century China, bills of exchange in 13th-century Europe, or credit cards in mid-20th-century America.

That said, while digital cash and distributed ledgers will likely form a major part of the next transition, replacing the dollar’s role in global finance won’t be easy. First, the entire crypto market cap is still only a small fraction of the $13 trillion in offshore U.S.-denominated bonds held by non-banks. The dollar’s share of foreign exchange reserves has declined over the past 30 years but still commands a majority at 58%. But Bitcoin doesn’t need to replace the dollar to serve a valuable function as an attractive alternative in turbulent times—which could help it gain a foothold in national reserves. Structural adoption of Bitcoin and crypto does not depend on the dollar’s collapse, explaining why we saw Bitcoin strengthen alongside the dollar in the first half of 2023. In the long run, the ongoing transformation of the monetary system—and crypto’s role within it—could be profound, even if we don’t witness the old order’s collapse firsthand.

Economic Outlook for 2024

The likelihood of the U.S. avoiding a recession in 2024 has risen sharply in recent months, though the possibility is not zero—as underscored by the deeply inverted U.S. Treasury yield curve. This year’s unusual economic resilience has been driven by high levels of government spending and near-shoring efforts to strengthen domestic manufacturing. However, we expect these effects to wane in Q1 2024, leading to weaker economic performance amid relatively tight financial conditions. Still, we do not believe this necessarily leads to recession. Rather, a downturn would depend on endogenous factors—such as renewed weakness in the U.S. banking system or the pace of disinflation.

On the latter, we have argued since March 2023 that inflation has peaked, and slowing aggregate demand should cyclically support stronger disinflation going forward. To a large extent, this has materialized, and structural forces—such as artificial intelligence—could lead to greater automation and lower input costs. However, demographic shifts—such as baby boomers exiting the labor force—may partially offset this effect. Taken together, we believe slowing growth and easing price pressures should pave the way for the Fed to cut rates by mid-2024—or earlier.

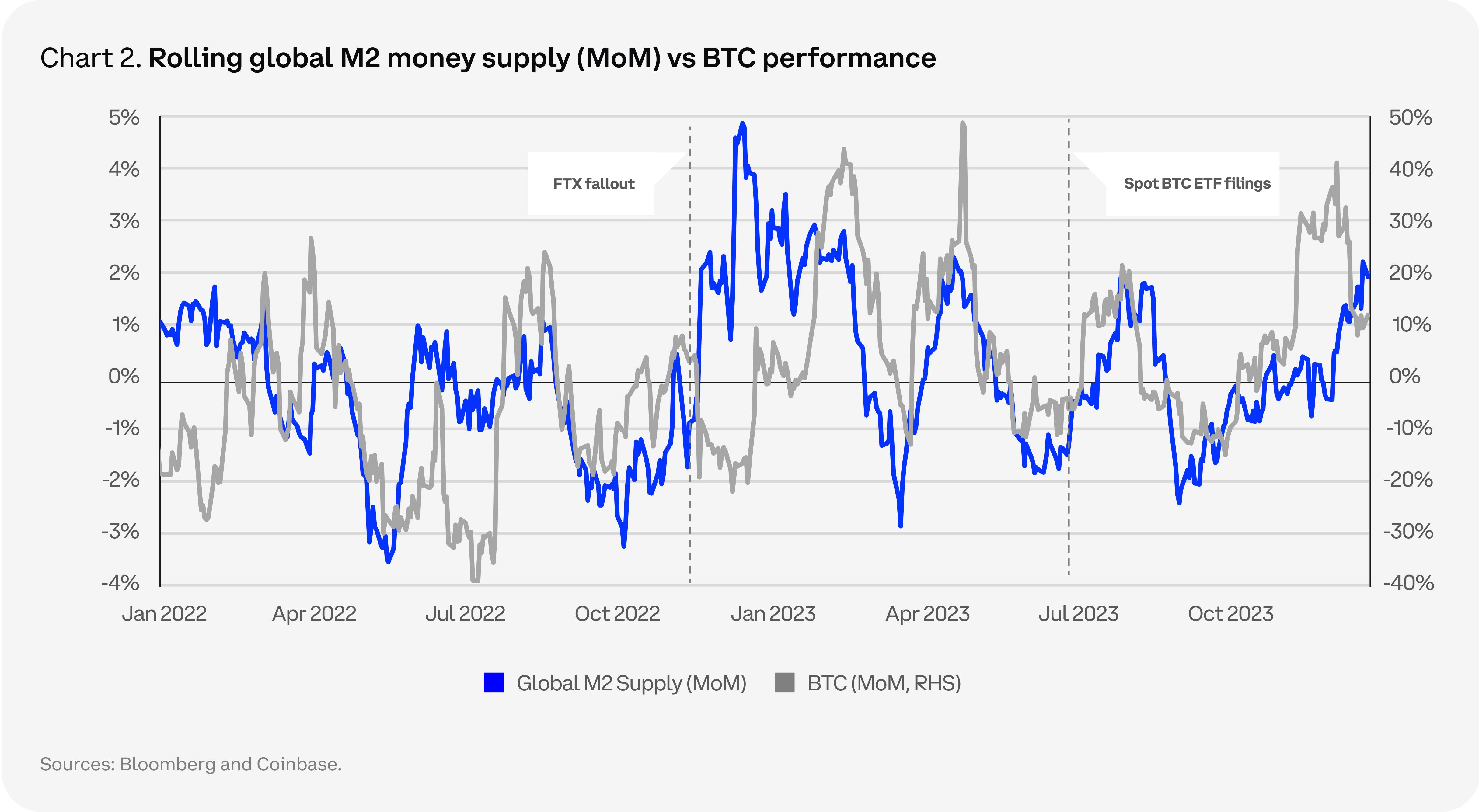

In our view, lower capital costs could support risk assets in Q2 2024, though Q1 may face headwinds depending on how entrenched the Fed’s stance remains. Under such conditions, crypto may not be fully immune. Yet our macro outlook also suggests a weakening dollar in 2024—an opportunity for crypto, as these assets are typically priced in dollars. Although correlations between various macro variables and Bitcoin (and Ethereum) returns have weakened over the past year, an accommodative macro backdrop remains a core component of our constructive market thesis for 2024.

Interpreting Regulation

In a recent institutional investor survey commissioned by Coinbase, about 59% of respondents said they expect their firms to increase allocations to digital assets over the next three years, while a third reported already increasing exposure over the past 12 months. This confirms crypto remains a globally significant asset class with broad commercial and investment appeal. However, while many jurisdictions worldwide are taking decisive steps toward crypto regulation, regulatory uncertainty in the U.S. is causing missed opportunities and market constraints centered on enforcement actions. Indeed, 76% of survey respondents believe the lack of reasonable, clearly defined crypto regulations in the U.S. threatens the country’s leadership position in financial services.

Furthermore, regardless of the specific language used in regulatory guidance and public statements in 2023, market perception is that U.S. banking regulators’ attitude toward the digital asset ecosystem is—at best—unfavorable, and at worst—downright hostile. As a result, all but the largest and most reputable crypto companies may struggle to establish banking relationships. Whether intentional or not, the U.S. regulatory gatekeeping model—built through no-action letters and other licensing requirements—has dampened banks’ incentives to invest in digital asset technology or serve clients actively engaged in these activities.

On a positive note, we believe growing recognition of rising global regulatory arbitrage risks is driving more U.S. lawmakers to act—evidenced by multiple House committees advancing the *Clarity for Payment Stablecoins Act* and the *Financial Innovation and Technology for the 21st Century Act* (FIT 21) in 2023.

Additionally, potential approval of spot Bitcoin ETFs in the U.S. could open crypto to new investor classes and reshape the market in unprecedented ways. Compliant ETFs could become the foundation for a suite of new financial instruments—such as lending and derivatives—tradable among institutional counterparties. We believe 2024 will continue laying the regulatory groundwork for crypto, bringing greater incremental clarity and paving the way for deeper institutional participation.

Theme 3: Connecting to the Real World

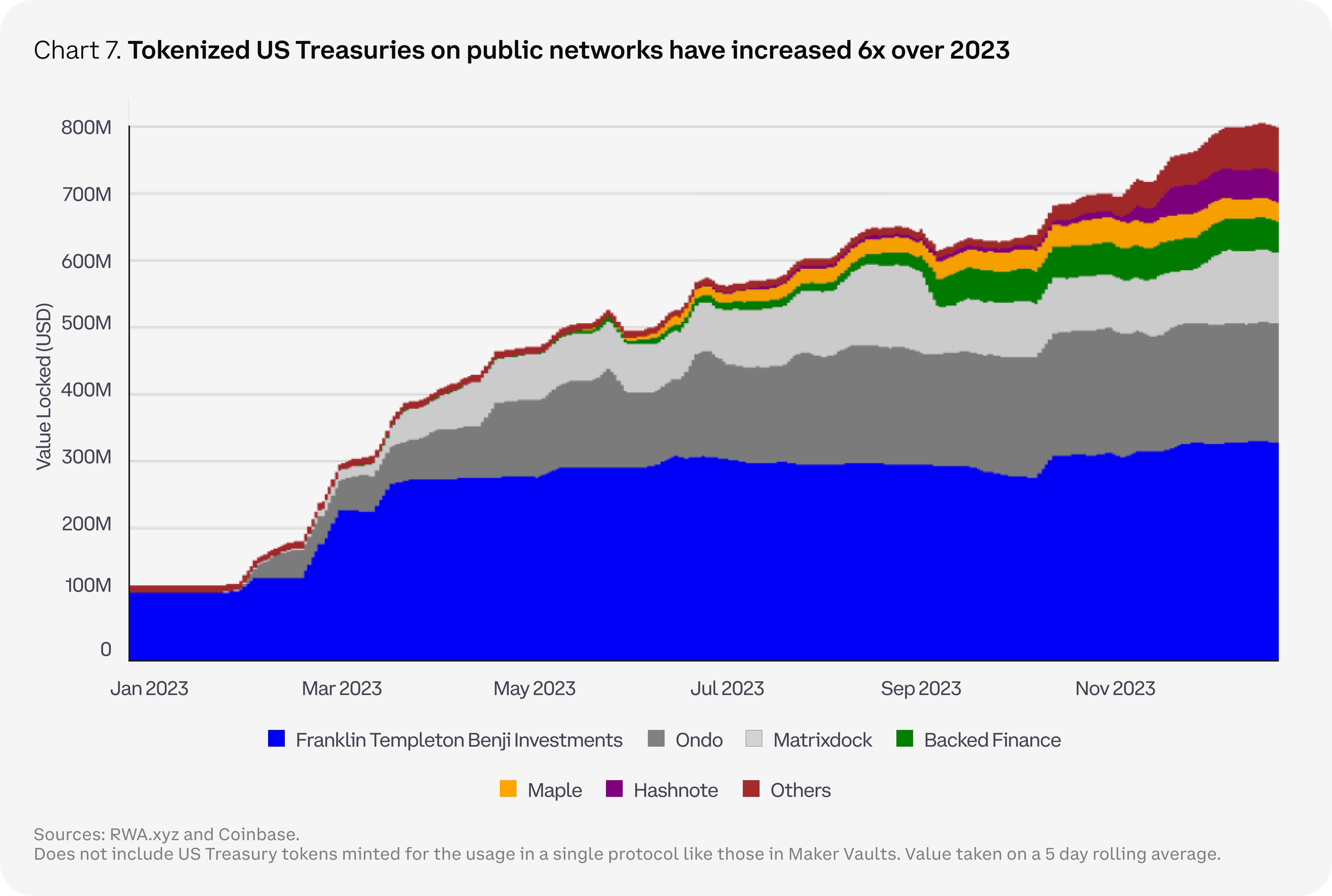

Tokenization is a key use case for traditional financial institutions and is expected to play a major role in the next crypto market cycle, as it represents a critical piece of “modernizing the financial system.” This primarily involves automating workflows and eliminating certain intermediaries no longer needed in asset issuance, trading, and recordkeeping. Tokenization not only offers strong product-market fit for distributed ledger technology (DLT), but the current high-yield environment makes the capital efficiency it enables far more valuable than two years ago. In higher interest rate environments, the cost of tying up capital—even for a few days—is significantly higher for institutions than in low-rate settings.

Throughout 2023, we observed numerous new entrants begin offering tokenized access to on-chain exposure to U.S. Treasuries on public, permissionless networks. Driven by digital-native users seeking yields unrelated to traditional crypto revenue sources, total assets in on-chain U.S. Treasury-like exposures grew sixfold to over $786 million. Given client demand for higher-yielding products and diversified return streams, we may see tokenization expand into other markets in 2024—including equities, private market funds, insurance, and carbon credits.

Over time, we believe more areas of commerce and finance will incorporate tokenization, though regulatory ambiguity and the complexity of navigating different jurisdictions continue to pose significant challenges—alongside integrating new technologies into legacy processes. Risks associated with public networks—such as smart contract vulnerabilities, oracle manipulation, and network outages—have forced most institutions to rely on private blockchains so far. While private blockchains may continue growing alongside public permissionless chains, interoperability barriers could fragment liquidity, making it harder to realize the full benefits of tokenization.

A key area to watch regarding tokenization is regulatory progress in jurisdictions like Singapore, the EU, and the UK. The Monetary Authority of Singapore sponsored “Project Guardian,” which has developed dozens of tokenization proof-of-concepts on both public and private blockchains involving top-tier global financial institutions. The EU’s DLT Pilot Regime establishes a framework allowing multilateral trading facilities to use blockchain for trade execution and settlement instead of central securities depositories. The UK has also launched a pilot program seeking advanced frameworks for issuing tokenized assets on public networks.

While many are now searching for commercially viable “proofs-of-concept,” we still expect full implementation to take years, as this theme requires regulatory coordination, advances in on-chain identity solutions, and scaling of key infrastructure within major institutions.

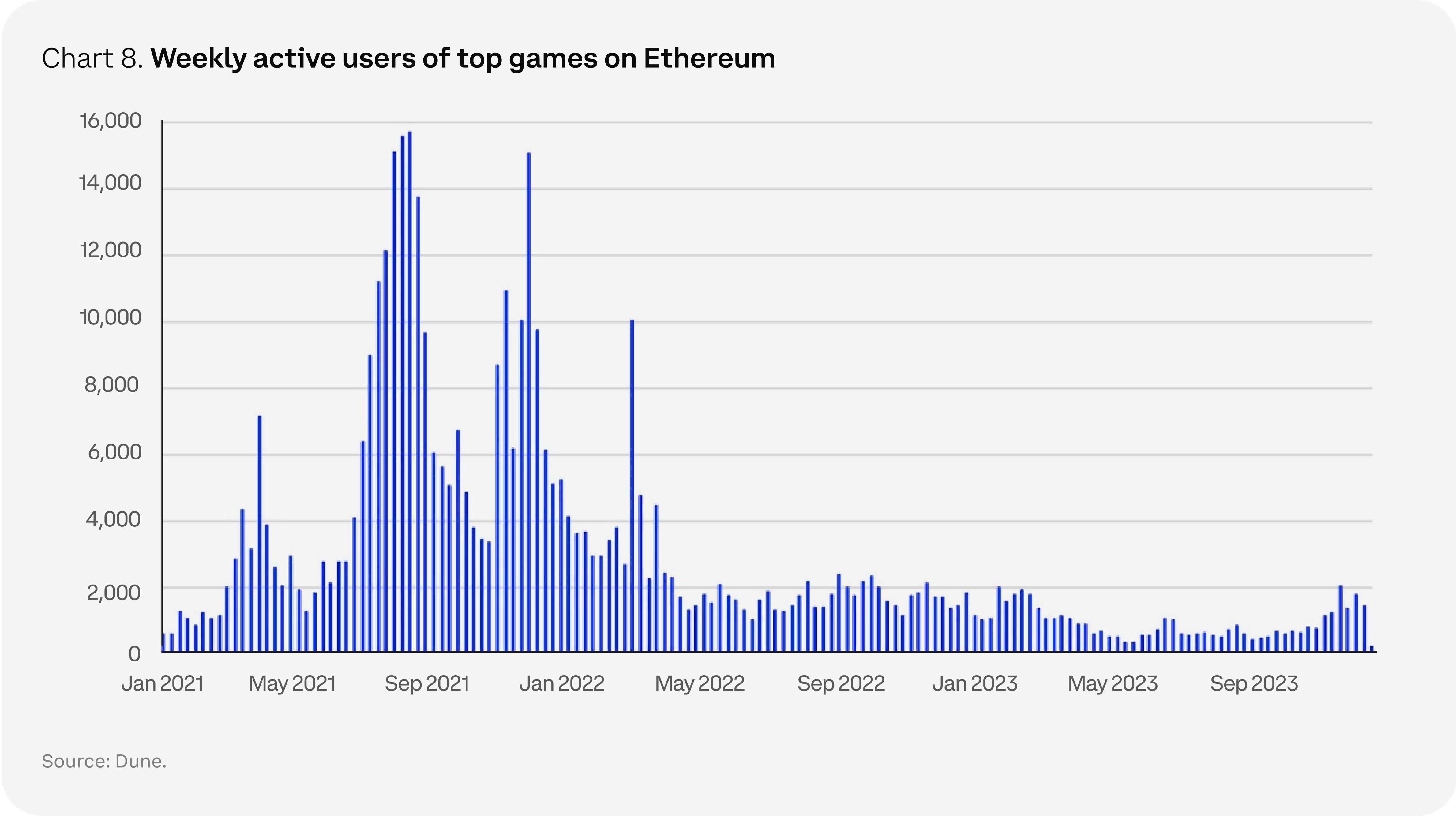

Perspectives on Web3 Gaming

After a sharp decline in trading activity early in the crypto bear market, Web3 gaming has recently regained momentum. Currently, the focus is on capturing the attention of mainstream gamers beyond the “crypto-first” communities. Overall, the gaming industry has a current addressable market of approximately $250 billion, projected to grow to $390 billion over the next five years. However, despite vast investment potential, users have broadly rejected early models exemplified by Axie Infinity’s web3 “play-to-earn” approach. In fact, this model may have deepened skepticism among mainstream gamers toward web3 games.

This has prompted developers to experiment further, attempting to combine the network effects of high-quality AAA games with sustainable monetization mechanisms. For example, game studios are exploring web3 narratives such as non-fungible tokens (NFTs) that can be used, transferred, or sold on designated marketplaces within games. However, surveys show most gamers dislike NFTs—a sentiment reflecting their rejection of “play-to-earn.” For the gaming industry, the added value of leveraging web3 architecture lies in its potential to improve user acquisition and retention, but so far, this remains an unproven hypothesis. With many projects approaching the typical 2–3-year development timeline (following heavy fundraising in 2021–2022), we believe some Web3 game launches in 2024 may soon provide the data needed to better assess this sector.

Building the Decentralized Future

A major theme in 2024 (and likely beyond, depending on development timelines) is the decentralization of real-world resources. We are particularly focused on decentralized physical infrastructure networks (DePIN) and decentralized computing (DeComp). Both leverage token incentives to drive the creation and consumption of real-world resources. In the case of DePIN, these projects rely on economic models that incentivize participants to build physical infrastructure—ranging from energy and telecom networks to data storage and mobile sensors—that isn’t controlled by large corporations or centralized entities. Specific examples include Akash, Helium, Hivemapper, and Render.

DeComp is a specific extension of DePIN, relying on distributed computer networks to fulfill specific tasks. This concept has been revitalized by the mainstream adoption of generative AI. The computational cost of training AI models can be prohibitively high, prompting the industry to explore whether decentralized solutions could help alleviate this burden. It remains unclear whether blockchain-AI convergence is feasible, but the field is growing. One independent yet related research area, zero-knowledge machine learning (ZKML), focuses on privacy and promises to revolutionize how AI systems process sensitive information. ZKML could allow large language models to learn from private datasets without directly accessing the data itself.

DePIN represents a powerful real-world application of blockchain technology with the potential to disrupt existing paradigms, but it remains relatively immature and faces numerous challenges—including high initial costs, technical complexity, quality control, and economies of scale. Moreover, many DePIN projects focus on incentivizing participants to supply necessary hardware, but few have begun developing financialization models to stimulate demand. While value demonstration may come sooner, realizing tangible benefits could take years. Therefore, we believe market participants must maintain a long-term perspective when investing in this sector.

Decentralized Identity

Privacy is the new frontier for blockchain developers, who are leveraging innovations like zero-knowledge (ZK) fraud proofs and fully homomorphic encryption (FHE) to perform computations while keeping user data encrypted. Applications are broad, especially concerning decentralized identity—the end state where users have full control and ownership over their personal data. For example, this could allow medical research institutions to analyze patient data to identify new disease patterns without exposing sensitive health information. However, achieving this requires individuals to have control over their identity data—a stark contrast to today’s reality, where information is stored across many different centralized servers.

Admittedly, we are still in the very early stages of solving this problem. But ZK systems and FHE were once considered purely theoretical concepts—now seeing more experimental implementations within the crypto industry. In the coming years, we expect significant progress that could enable end-to-end encryption in web3 apps and networks. If so, we believe decentralized identity could achieve strong product-market fit in the future.

Theme 4: The Future of Blockchains

Improved User Experience

A recurring theme during the recent bear market has been how to make crypto more user-friendly and accessible. The added responsibility of managing crypto—wallets, private keys, gas fees, etc.—isn't suitable for everyone, making industry maturity difficult unless key user experience challenges are overcome. Progress in account abstraction appears to offer meaningful solutions. The concept dates back to at least 2016, referring to treating externally owned accounts (like wallets) and smart contract accounts similarly to simplify user interaction. Ethereum advanced this effort in March 2023 by introducing ERC-4337, opening new possibilities for users.

For example, on Ethereum, this allows app owners to act as “sponsors” and pay users’ gas fees, or enable users to fund transactions using non-ETH tokens. This is especially valuable for institutional entities that prefer not to hold gas tokens on their balance sheets due to price volatility or other reasons. J.P. Morgan’s proof-of-concept report under Project Guardian highlighted this, with all gas payments processed via Biconomy’s Paymaster service.

With the Dencun upgrade potentially reducing rollup transaction fees by 2–10x, we believe more decentralized applications (dapps) may pursue a “gasless transaction” model, allowing users to focus solely on high-level interactions. This could also spur development of new non-financial use cases. Account abstraction can also enable robust wallet recovery mechanisms, creating safeguards against simple human errors like lost private keys. The goal of the crypto ecosystem is to attract new users and encourage existing ones to become more active participants.

Validator Middleware and Customizability

Advancements like restaking and Distributed Validator Technology (DVT) are giving validators new ways to customize key parameters—better adapting to evolving economic conditions, network demands, and preferences over time. From an innovation standpoint, the growth of validator middleware solutions was a major theme in 2023, but we believe their full potential to enhance customizability and unlock new business models remains unrealized.

Regarding restaking, currently led by EigenLayer, this could be a way for validators to secure data availability layers, oracles, sequencers, consensus networks, and other services on Ethereum. Potential returns from this process could represent a new revenue stream for validators in the form of “security-as-a-service.” EigenLayer officially launched Phase 1 on Ethereum mainnet in June 2023 and plans to begin registering operators for Active Validation Services (AVS) in 2024, after which restakers can delegate their staked positions to these operators. We believe this development warrants close attention—particularly how much staked ETH gets allocated to additional security services once EigenLayer opens fully to the public.

Meanwhile, Distributed Validator Technology (DVT) for proof-of-stake networks offers stakers more design flexibility in setting up and managing validator operations. DVT distributes the responsibilities (and private keys) of a single validator across multiple node operators, eliminating single points of failure. This reduces slashing risks and improves security, as compromising a single node operator doesn’t jeopardize the entire validator. Additionally, for individual stakers, DVT enables participation in validation and earning rewards without meeting the full 32 ETH threshold—assuming collaboration through platforms like Obol, SSV Network, or Diva Protocol—lowering entry barriers and promoting greater decentralization. As a result, we may see DVT enabling geographically dispersed validators to mitigate liveness and slashing risks.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News