Macro Insight: Retail investor bullish sentiment surges, diverging from economic fundamentals—the first time in three years

TechFlow Selected TechFlow Selected

Macro Insight: Retail investor bullish sentiment surges, diverging from economic fundamentals—the first time in three years

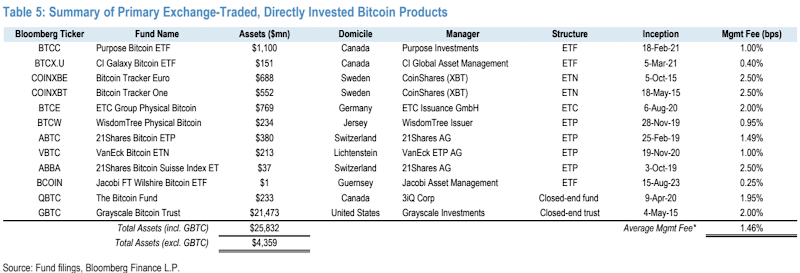

Access to the cryptocurrency market is currently not strictly restricted, and its penetration rate in the U.S. has reached nearly 20%, almost on par with stocks. Even if ETFs are approved, the incremental impact they bring is likely to be limited.

Key Points

-

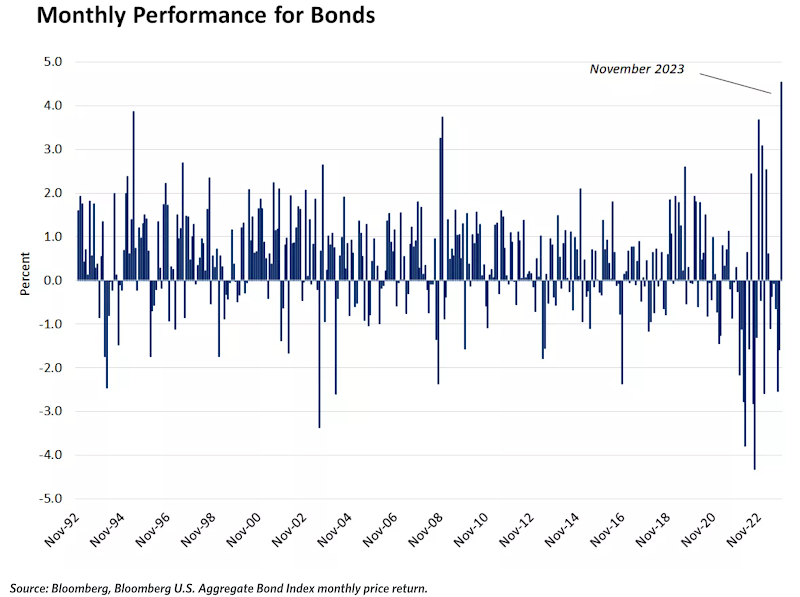

Last week, sectors most sensitive to rate cuts continued to lead, while tech and communication—up over 50% this year—performed worst; bond markets posted their best monthly return in the past 30 years;

-

Data shows slowing GDP growth in the U.S. and globally, with a slight deterioration in U.S. manufacturing momentum, though consumer spending continues to grow;

-

Fed's Waller signaled potential early rate cuts, while Fed whisperer Timiraos wrote that rate hikes may be over, but Powell remained hawkish—yet markets ignored his stance;

-

OPEC+ expanded production cuts, yet oil prices fell sharply—mainly because this meeting may mark the limit of OPEC’s self-restraint, with no further cuts expected, raising market concerns about a potential market share war next year;

-

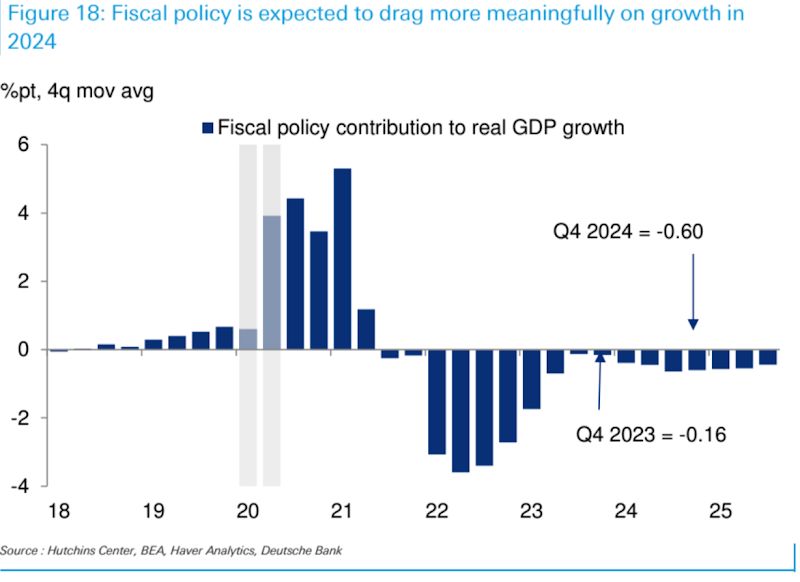

Compared to 2023, fiscal policy will likely weigh more heavily on the U.S. economy in 2024; DB forecasts nominal GDP growth to face approximately 0.8% drag;

-

Cryptocurrency adoption currently faces no strict limitations, with U.S. penetration reaching 20%, nearly matching equities; even if ETFs are approved, incremental inflows should be limited; regardless of whether Bitcoin ETFs succeed or fail in January, it could signal a near-term top;

-

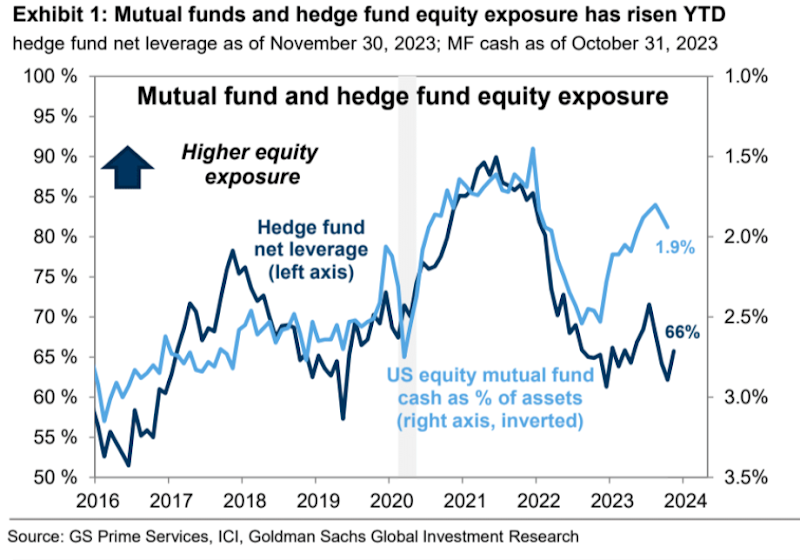

Total equity positioning rose further this week to the 63rd percentile; systematic investors hold neutral exposure, while discretionary investors are relatively overweight;

-

Futures market net longs in U.S. equities rose for the third consecutive week, marking the first significant divergence from economic fundamentals since late 2019;

-

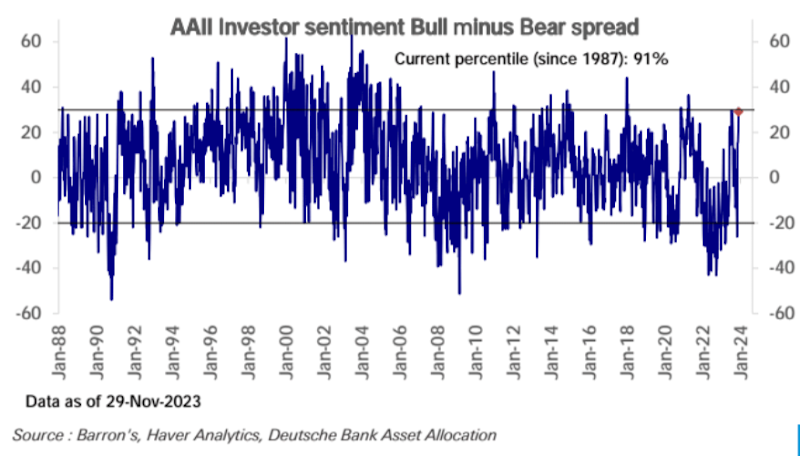

AAII survey shows elevated retail sentiment, with bullish-minus-bearish spread at the 91st historical percentile;

-

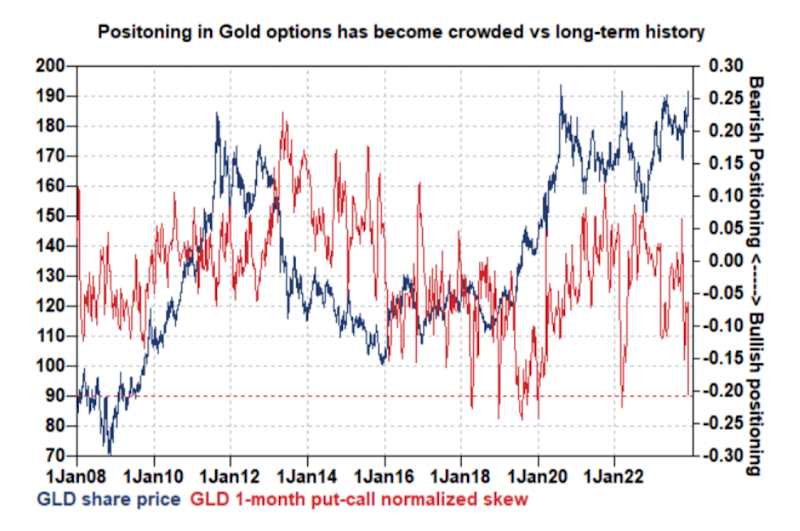

Demand for gold call options is abnormally high, with put-call skew nearing historical extremes;

-

This week’s focus is on the nonfarm payrolls data; given seasonal factors and returning strikers in November, an expectation of 175K jobs is modest; slightly below-forecast numbers could fuel further speculation of rate cuts, while slightly higher figures would still leave room for optimism.

Market & Data Review

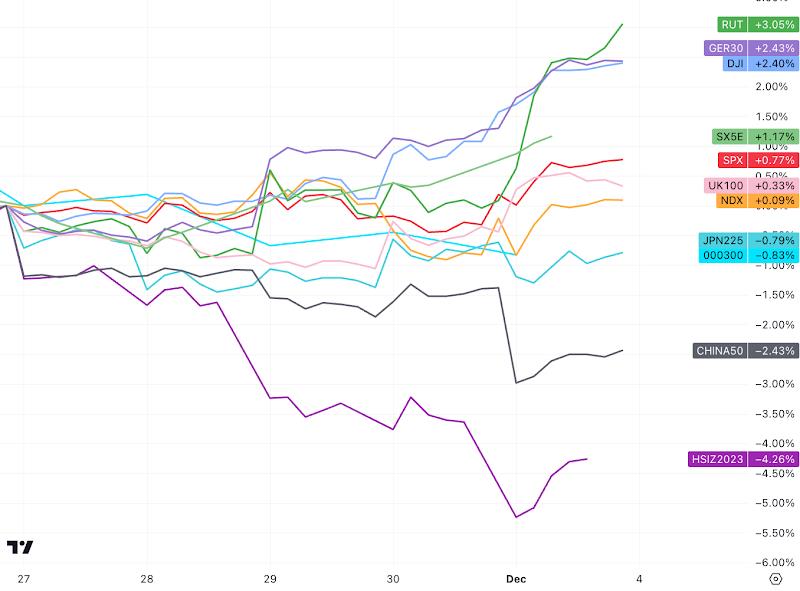

Markets last week were led by cyclical sectors and small-cap stocks—particularly those most sensitive to lower interest rates, including cryptocurrencies, industrial metals, and gold. The weekly performance of major indices shows the small-cap Russell 2000 (RUT) accelerating gains in the second half of the week.

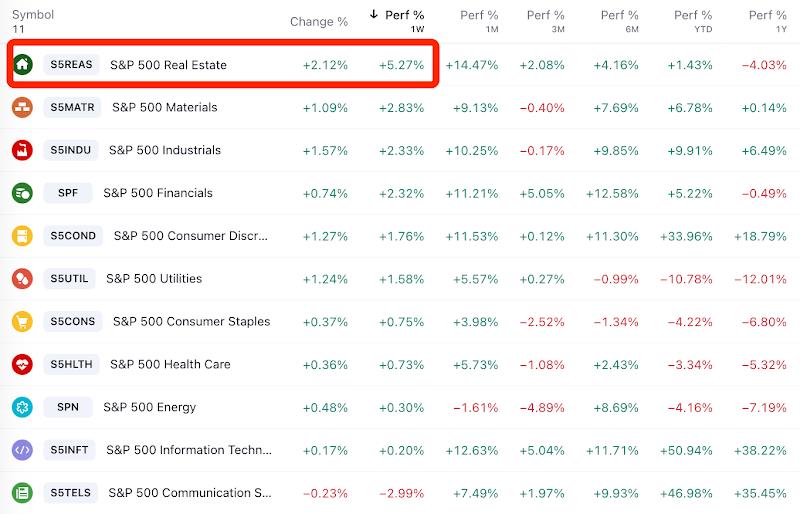

Rate-sensitive sectors such as real estate performed strongly, with the sector rising over 5% for the week—the best among S&P industry indices—and up 14.5% over the past month. Financial services and discretionary consumer goods also gained over 11% in the past month. In contrast, the top-performing tech and communication sectors this year lagged, with communications down 3% last week—making it the only declining sector:

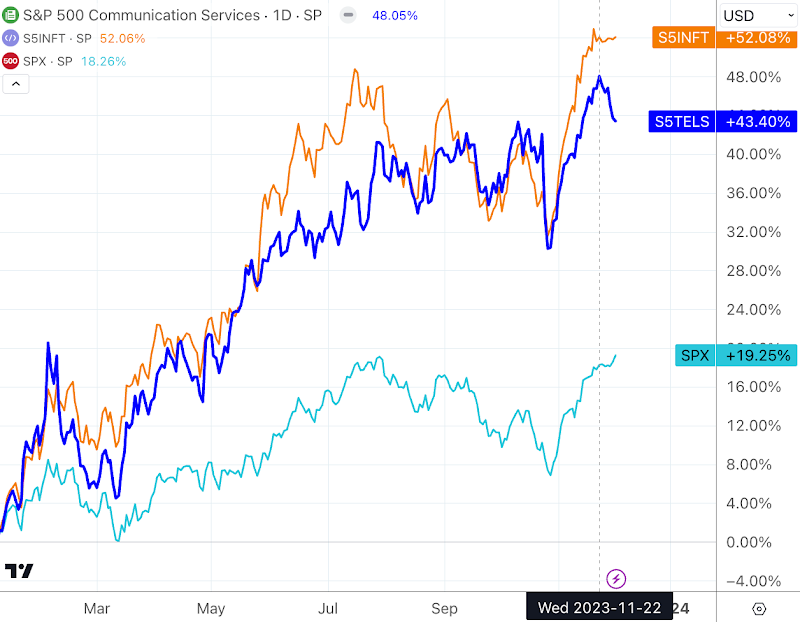

The communication sector (S5TELS) has recently pulled back against the trend, while technology (S5INFT) has stalled, though both still maintain returns more than double that of the broader market this year:

Bond markets delivered their best monthly return in the past 30 years:

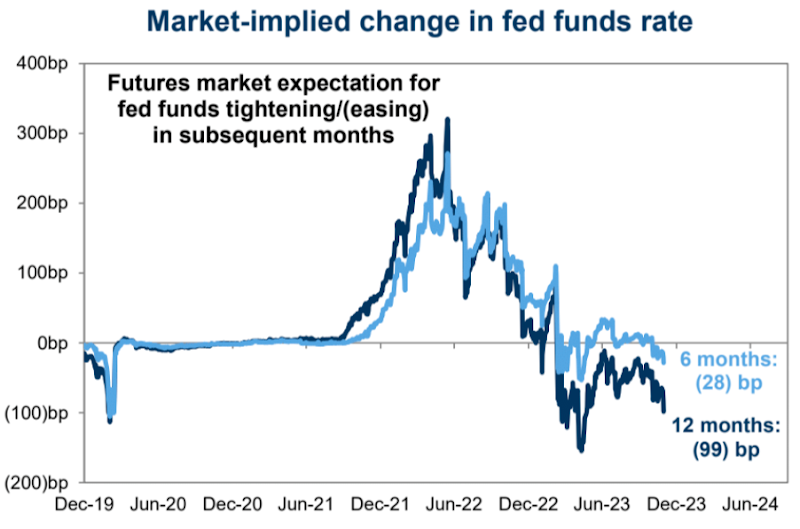

Current rate futures imply 28 bps of cuts within six months—meaning one cut by May—and 99 bps over 12 months, implying roughly four cuts next year, which is quite aggressive. We believe the Fed may verbally push back on these expectations after the December meeting, despite some officials turning dovish—it’s unlikely they’ll collectively endorse such an outlook:

On the data front, U.S. and global GDP growth slowed, with U.S. manufacturing momentum slightly weakening, though consumer spending continues to expand. Core inflation and GDP growth both declined—since markets focus more on inflation, this temporarily supports central bank and market optimism.

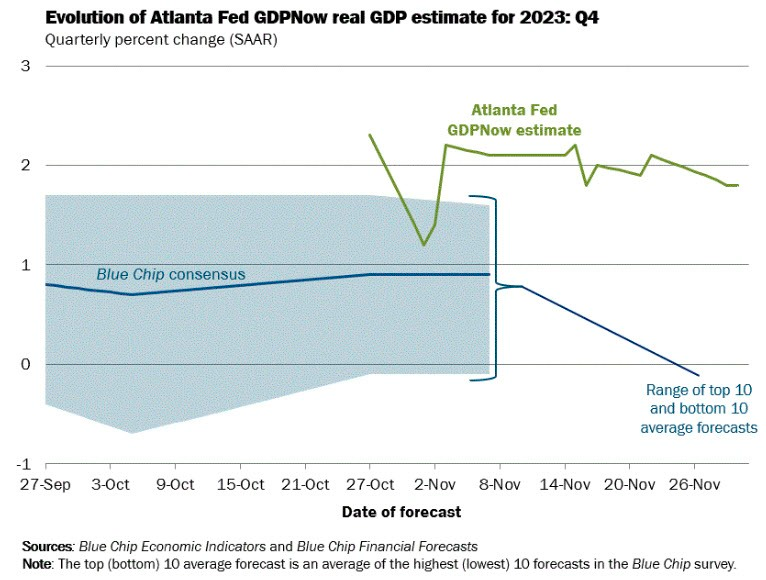

Atlanta Fed GDPNow lowered its Q4 growth forecast last week from 2.1% to 1.8%:

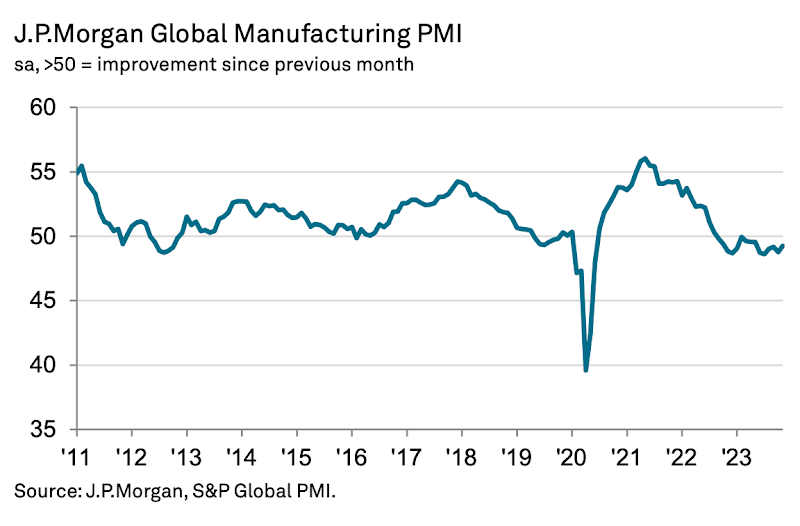

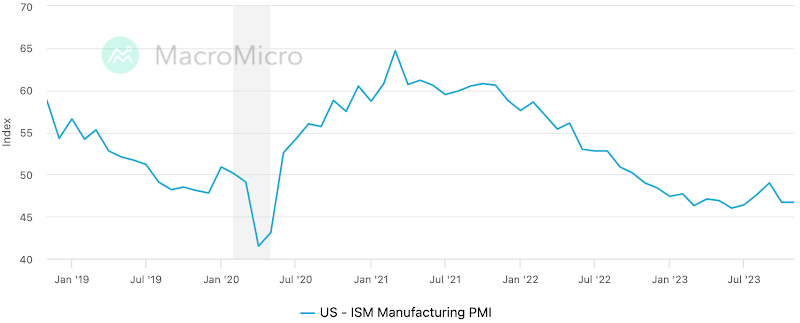

Although the global manufacturing PMI rose to 49.3 in November—the highest in six months—global PMI has remained below 50 for 15 consecutive months, marking the longest contraction period since the 2008 financial crisis:

U.S. manufacturing PMI has contracted for 13 straight months (below 50), the longest slump since the dot-com bubble burst—marking the longest downturn in the past 20 years:

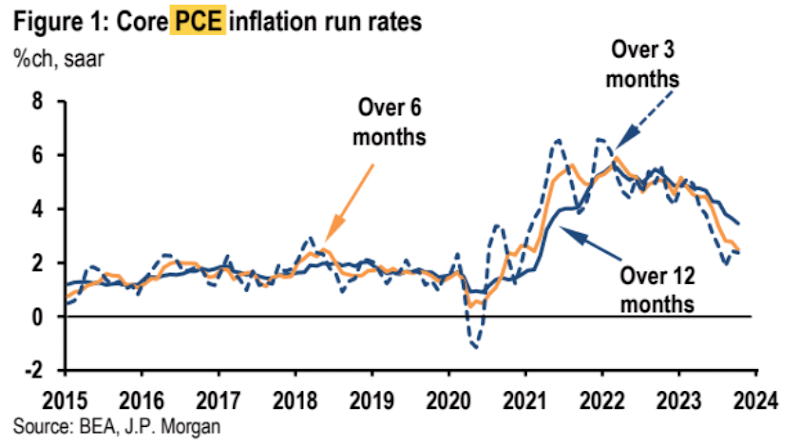

Overall, underlying inflationary pressures in the U.S. continue to ease. Markets broadly expect inflation to remain on a moderating path over the coming months, although not in a linear fashion. Last week’s October PCE core inflation data showed another decline, rising 3.5% year-on-year, drawing closer to the Fed’s 2% target. The latest 3-month and 6-month annualized core inflation rates stand at 2.4% and 2.5%, notably below earlier highs this year:

Personal consumption slowed from 0.7% in September to 0.2% month-over-month. However, the annualized growth rate remains around 5.2%, unchanged from the prior three months.

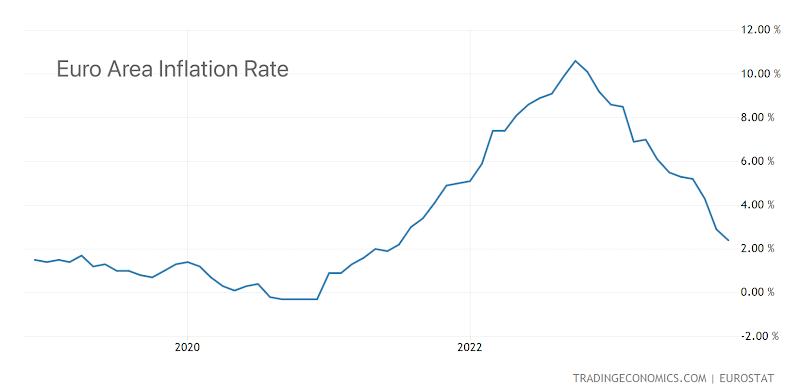

Eurozone nominal inflation in November dropped to 2.4%, far below the peak of 10.6%, exceeding market consensus:

More Hints of Easing

Fed’s Waller stated last week that if progress continues in curbing inflation over the coming months, rate cuts beginning in the first half of 2024 could be justified. These comments contrast sharply with Chairman Powell’s response to rate-cut questions at the November FOMC meeting, when he emphasized: “In fact, the committee is not now thinking about rate cuts at all.”

Fed watcher Timiraos also wrote last week: “Rate hikes by the Fed may already be over, but officials are reluctant to say so.” The Fed will extend its pause in hiking into January 2024. This means that at its December 12–13 meeting, the Fed will focus on how long it can still retain the ability to signal future hikes. Officials are unlikely to remove this so-called tightening bias at the meeting—a necessary first step before considering rate cuts. This serves as advance notice of another unchanged decision in December, albeit with a hawkish tone.

Based on current market pricing, by June next year, core PCE inflation should convincingly fall below 3% year-on-year, while the unemployment rate climbs toward 4.5%—a mild recession scenario—leaving the Fed with little justification to remain restrictive.

On Friday, Powell cooled rate-cut speculation, saying it’s too early to judge when easing might begin and that the Fed stands ready to tighten further if needed. Yet he also noted monetary policy’s lagged effects on the economy and acknowledged that the full impact of prior tightening may not yet be felt. Markets clearly disregarded his “hawkish” remarks, focusing instead on softening economic data forcing a policy shift. Bond prices surged during Friday’s session, sending yields sharply lower.

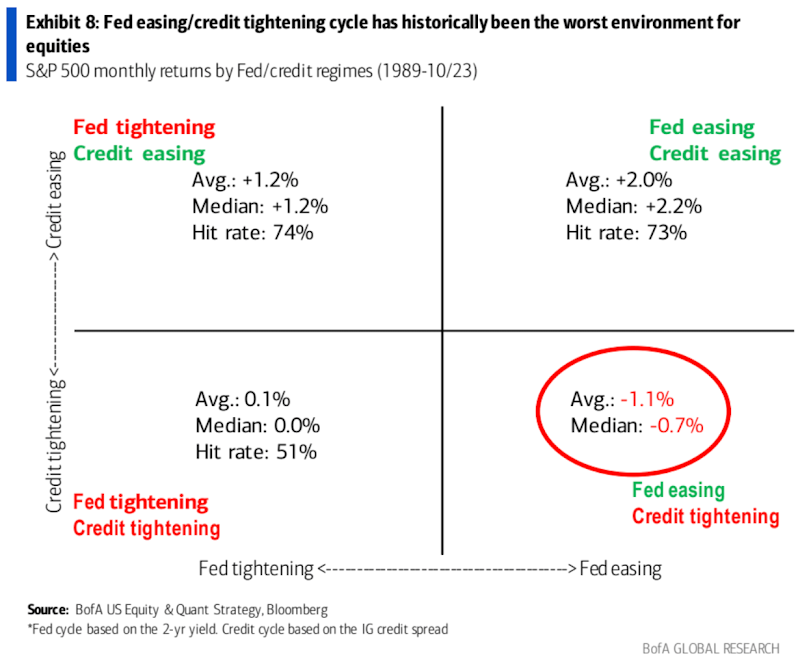

Ideally, the Fed should not ease out of economic weakness. While many see a Fed easing cycle as the next catalyst for equities, history shows that stock markets perform worst when Fed easing coincides with widening investment-grade credit spreads—that is, during recessions. Bulls should hope for improving economic conditions leading to looser credit, rather than a dovish Fed-driven easing due to weakness.

Growing Fiscal Drag

Deutsche Bank: Given the highly uncertain political environment, the projected deficit range for FY2024 is very wide—at $1.6 trillion to $1.9 trillion—with a base case of ~$1.7 trillion, representing a $337 billion narrowing compared to this year. Relative to 2023, fiscal policy will exert greater drag on the economy in 2024. We estimate nominal GDP growth will face approximately 80 basis points of drag.

BTC Nears $40,000

Bitcoin approached the $40,000 level last week, driven by expectations of spot BTC ETF approvals alongside weaker dollar and Treasury yields. Markets are optimistic an ETF could be approved in early January. However, we’ve previously argued that access to crypto markets isn’t currently tightly constrained—whether through Coinbase, existing crypto ETPs like BITO and GBTC, or Bitcoin and Ethereum futures markets.

According to a February 2023 Coinbase survey, 20% of Americans own cryptocurrency, versus 21% who directly hold stocks—indicating crypto penetration in the U.S. is already high (assuming CB’s data isn’t wildly off), leaving limited room for further expansion.

Therefore, we lean toward the view that whether the Bitcoin ETF succeeds or fails in January, it may signal a near-term top.

OPEC+ Expands Cuts, Oil Plunges

After difficult negotiations, OPEC+ reached a supply agreement last Thursday, agreeing to cut output by another 1 million barrels per day. Meanwhile, Saudi Arabia extended its existing voluntary cut of 1 million bpd. Yet oil prices fell nearly 5% post-meeting (from 83 to 79).

Some analysts argue that since the cuts are voluntary, enforcement concerns persist. Additionally, the 1 million bpd reduction was already expected—this outcome merely met baseline expectations, with the cut already priced in. Moreover, this may represent the limit of OPEC’s self-imposed restraint, with no further cuts likely. Next year, a market share battle could erupt, potentially driving oil down to ~$40. OPEC+ currently holds about 5 million bpd in spare capacity, and there’s no sign of slowing U.S. production (the U.S. added 5 oil rigs last Friday). Hopes had been that next year’s demand growth would absorb OPEC’s idle capacity, but OPEC itself forecasts only 2.5 million bpd in demand growth—meaning the market may need another full year to rebalance. These factors likely explain oil’s initial rise followed by a sharp drop.

Positions and Flows

According to Goldman Sachs’ PrimeBook data, both hedge funds and mutual funds increased equity exposure throughout the year. Hedge fund net positioning rose from 61% to 66% in 2023, still below the long-term average of 70%. However, since hedge funds increased both long and short positions simultaneously, overall leverage has hit a record high. This means fund size relative to capital has grown, but risk exposure remains conservative—suggesting fear of sharp drawdowns persists, and animal spirits have not yet fully returned:

Call option demand for gold is abnormally high, with put-call skew nearing historical extremes—indicating extremely optimistic asymmetric upside expectations for gold. This could signal an ongoing major rally, or alternatively, a warning of an impending correction (note comparison between blue price line and red skew line at extremes):

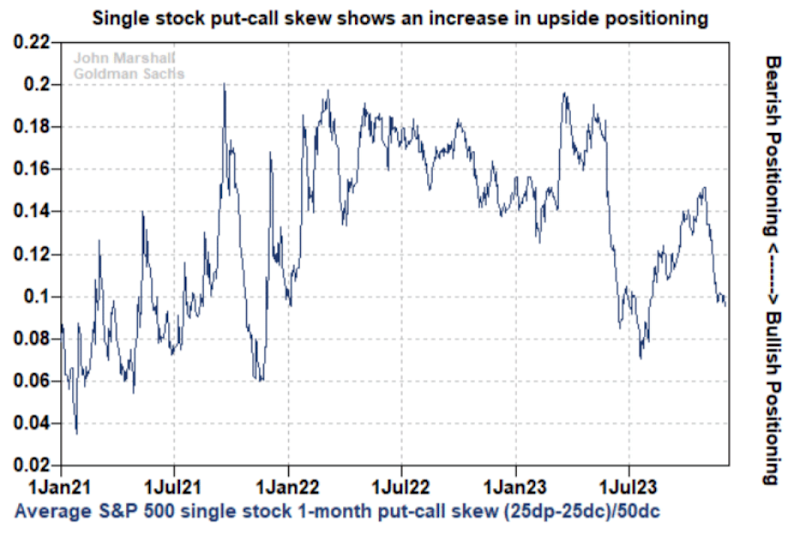

Individual stock put-call spreads are also falling, currently at the 25th historical percentile—indicating elevated bullishness among professional investors but not yet at extreme levels. If call demand rises further, it could become a warning signal for equities:

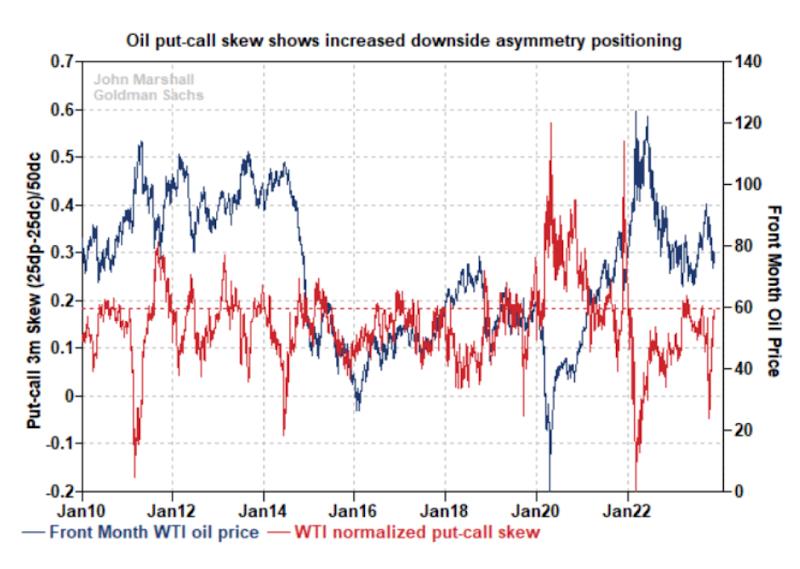

Put option demand for crude oil is rising (skew moving up), indicating growing investor fear and expectation of lower oil prices. This acts as a contrarian indicator—when skew rises further, buying oil calls to hedge inflation and geopolitical risks could present a good opportunity.

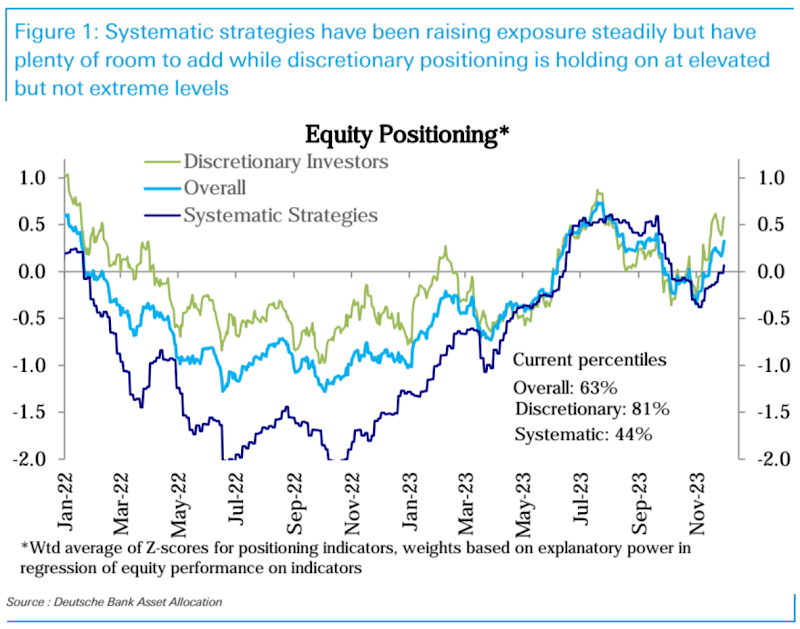

Deutsche Bank’s aggregate equity positioning rose again this week (63rd percentile). Systematic strategies moved from slightly below neutral to slightly above (44th percentile). Although significantly bullish on large-cap U.S. indices, their exposure to small caps, Europe, and EM indices remains low but rising. Discretionary investors increased positions further into overweight territory (81st percentile)—elevated but not extreme:

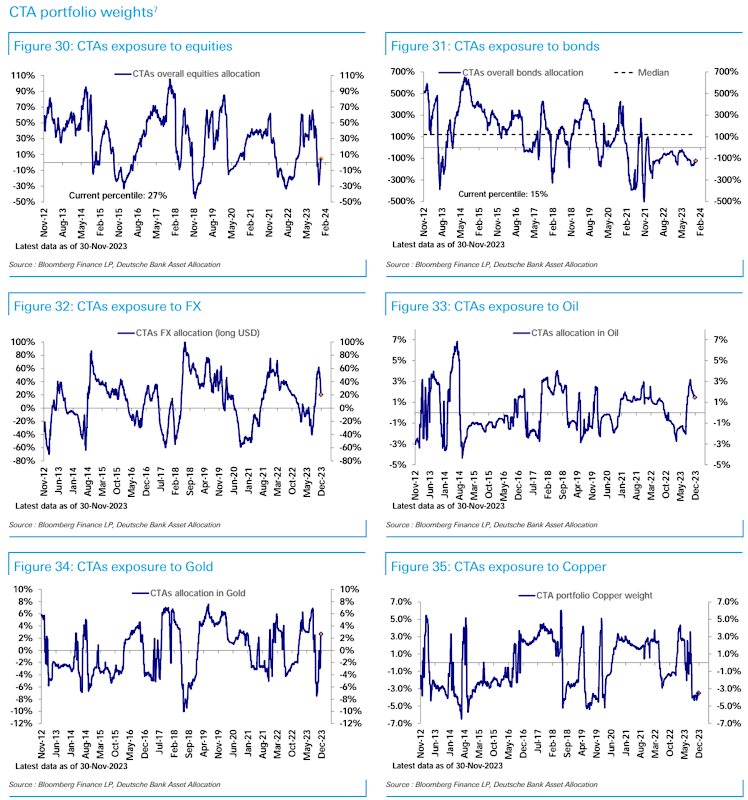

CTA positioning increased for the third consecutive week, turning bullish on equities—but historically still relatively low (27th percentile). Short exposure to bonds appears to be in early stages of unwinding (15th percentile):

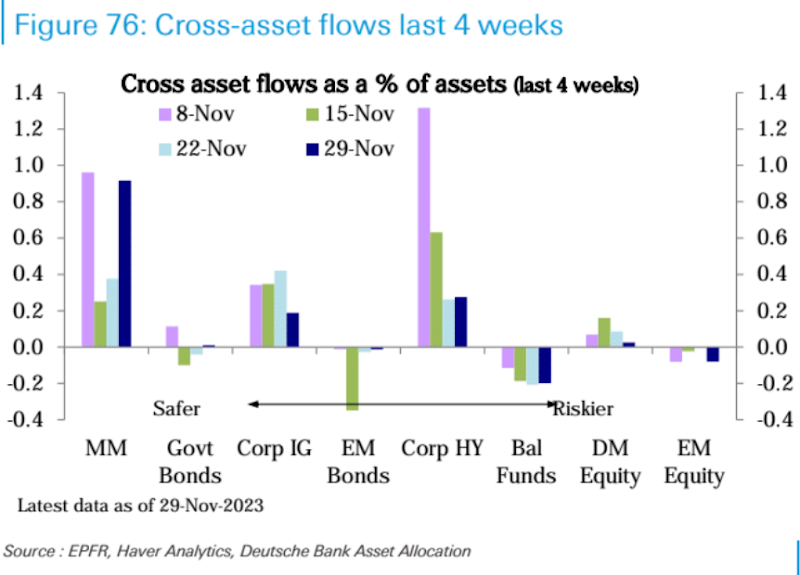

U.S. equity funds ($8.3B) continued to see steady net inflows, while rest-of-world funds (-$5.7B) saw outflows. Money market funds received massive inflows ($75.6B), totaling nearly $3T over the past six weeks and a record $1.29T YTD. Bond fund inflows slowed last week, though corporate debt still saw notable inflows; EM equities and bonds both experienced outflows:

Futures market net longs in U.S. equities rose for the third straight week, marking the first severe divergence from economic fundamentals since late 2019:

Market Sentiment

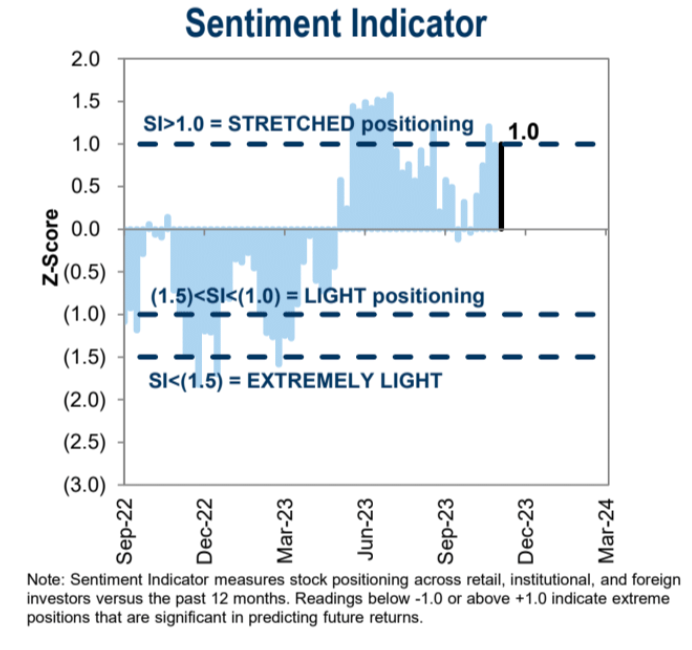

Goldman Sachs’ institutional sentiment indicator returned to 1.0—entering the excessive zone—reflecting relatively optimistic current sentiment:

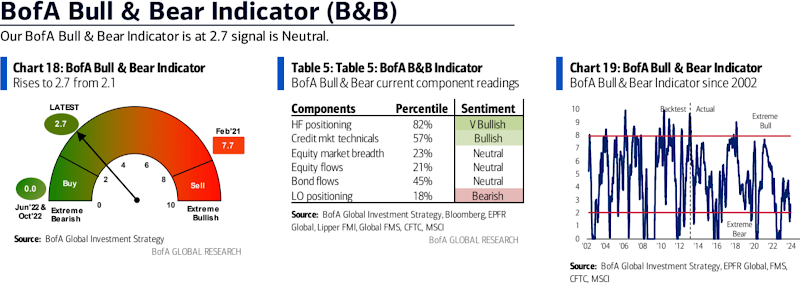

BofA sentiment rose from 2.1 to 2.7, remaining in neutral territory:

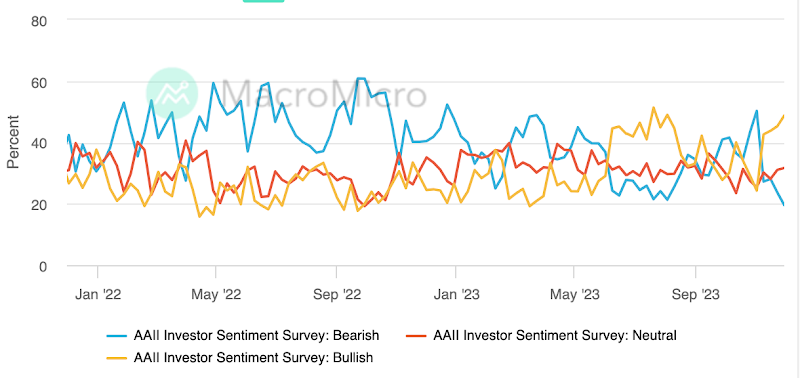

AAII survey shows bullish sentiment rose to 48.76%, with the bull-bear spread matching July’s level—reaching the 91st historical percentile:

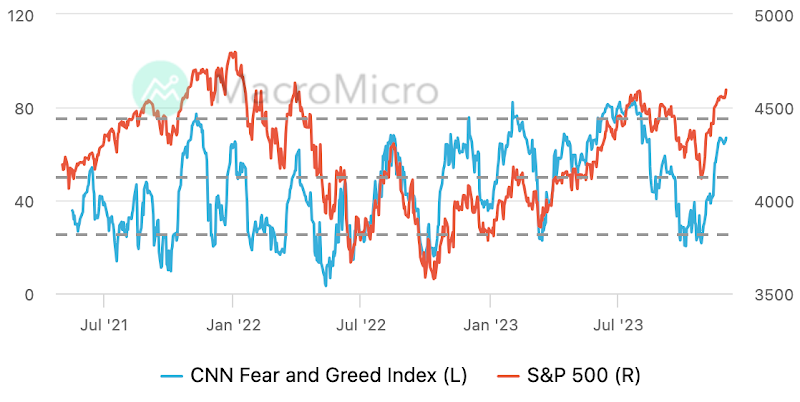

CNN Fear & Greed Index is positive but hasn’t reached excessive greed:

Focus This Week

Only four things could reverse the current momentum: a shift in Fed policy expectations, fears over economic growth, political/fiscal uncertainty, or geopolitical uncertainty.

The nearest potential pivot may come from Friday’s nonfarm payrolls report. Market expects 175K jobs—slightly above October’s 150K—possibly due to returning strikers and seasonal holiday hiring (e.g., retail, logistics), which could distort the trend. It’s important to recognize that even a strong November number wouldn’t negate the broader weakening in labor markets, as confirmed by high-frequency weekly jobless claims data:

Given the modest baseline expectation, a slightly weaker print could fuel further speculation of rate cuts, while a slightly stronger number would still allow bulls to justify optimism. A significantly weaker result, however, could trigger recession fears. Also, markets expect the unemployment rate to remain unchanged at 3.9% between October and November. Average hourly earnings are forecast to rise 0.3% MoM—above the prior 0.2%—but YoY growth is expected to slow further to 4.0% from 4.1%.

Earlier in the week, Tuesday brings the JOLTS job openings data, expected to decline from 9.553M to 9.35M. Though volatile, the downward trend is clear—and this data has noticeably influenced markets over the past two months.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News