DeFi Historiography: The History of DeFi Development Before Uniswap

TechFlow Selected TechFlow Selected

DeFi Historiography: The History of DeFi Development Before Uniswap

Let's go on an archaeological journey to explore the difficult path DeFi has traveled, and discover which products and pioneers have made remarkable innovations along the way.

Author: 0xKooKoo, Technical Advisor at GeekWeb3 & MoleDAO, Former Technical Lead at Bybit

Note: This article represents the author's current-stage archaeological research into DeFi and may contain errors or biases. It is intended solely for discussion purposes, and corrections and feedback are welcome.

Introduction

Most people were first introduced to DeFi during the "DeFi Summer" of 2020. In my view, DeFi suddenly gained popularity for several reasons:

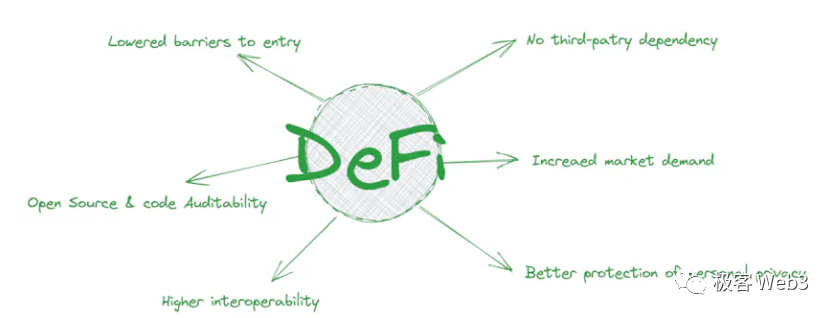

No reliance on third parties. Like Bitcoin, DeFi does not require any third-party intermediaries (except Oracles). Users only need to connect a crypto wallet and sign transactions to conduct fully on-chain trading. As long as smart contracts are secure, no one can take users' assets—Not your keys, not your coins. Those who lived through the Mt. Gox hack or the FTX collapse, where user funds were misappropriated, likely understand this lack of trust all too well.

Increase in market demand. Prior to DeFi Summer, there was massive global demand for liquidity. With traditional financial systems offering low interest rates and loose monetary policies flooding markets with capital, investors sought higher-yielding opportunities. DeFi provided a viable alternative, attracting substantial capital inflows with higher yields and broader investment options.

Better protection of personal privacy. DeFi requires little or no KYC. Built on blockchain technology and powered by smart contracts, DeFi platforms operate without centralized institutions or intermediaries. This decentralized nature means they cannot directly collect or manage users’ personal identity information, making traditional KYC procedures impractical. Pure on-chain alpha opportunities abound, and professional players who capitalize on them prefer not to expose their strategies or personal details—making DeFi an ideal choice for these sophisticated participants.

Lower barriers to entry, permissionless access. DeFi addresses certain shortcomings of traditional finance—for example, anyone can list their token on Uniswap, greatly expanding accessibility. As long as there is demand for a given token, it can be traded on DeFi without waiting for a centralized exchange to go through lengthy listing reviews.

Code audibility. DeFi projects are typically open-source, allowing anyone to audit and verify their smart contract code. This openness and transparency enable scrutiny to ensure there are no hidden malicious behaviors or risks. In contrast, traditional financial institutions often run closed-back-end systems that users cannot directly audit.

High interoperability. Different protocols and platforms within the DeFi ecosystem can interconnect and collaborate seamlessly, forming an integrated financial network. Because of this, the DeFi community generally embraces openness and connectivity to foster further innovation and development.

However, DeFi also has its issues:

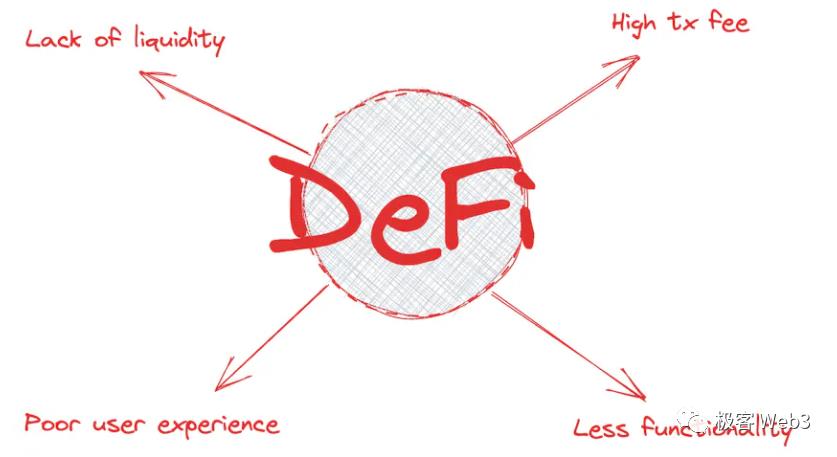

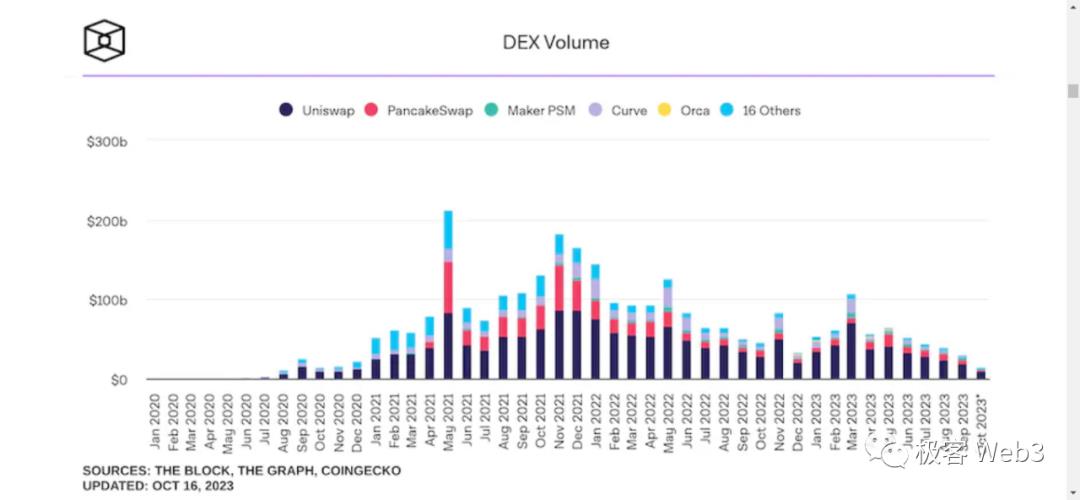

Lack of liquidity. Compared to centralized exchanges (CEX), DEXs still have significant room for improvement. According to theblock.co’s data from October 16, 2023, DEX spot trading volume accounted for only 13.45% of CEX spot volume over the past month. Low liquidity leads directly to high slippage—for instance, while 1,500 USDT might buy 1 Token A on a CEX, the same amount could only purchase 0.9 Token A in a poorly liquid pool, effectively resulting in a 10% loss per trade.

High transaction fees. Since DeFi transactions occur on-chain, they are constrained by the performance and capacity of the underlying public blockchain. For example, Uniswap transaction fees can spike dramatically during Ethereum mainnet congestion—I once paid a $200 gas fee for a simple swap, which felt highly discouraging.

Less functionality. Compared to the wide range of services offered by centralized exchanges—such as grid trading, dollar-cost averaging bots, and wealth management products—current DeFi offerings remain relatively primitive and fragmented, limited mostly to basic swaps, liquidity mining, staking, and farming.

Poor user experience. DeFi interfaces lag far behind mature CEX platforms in terms of usability—delays of several seconds per trade, unclear signature prompts, inconsistent terminology, and clunky navigation flows. However, this issue is relatively manageable, as standardization efforts can lead to reusable front-end templates and product logic, eventually converging across platforms.

The Past: The History of DeFi

Ever since Bitcoin’s inception, people have dreamed of conducting trades in a decentralized manner, leading to continuous innovation in on-chain finance. Due to Bitcoin’s limited programmability, early experimentation was scarce. But with Ethereum’s emergence, new possibilities opened up, and many projects began raising funds via ICOs.

After the ERC-20 standard was established, on-chain asset circulation flourished, giving rise to a wave of financial innovations.

Now let’s dive into some archaeology—exploring the difficult journey DeFi has taken and highlighting the groundbreaking contributions of key figures and products along the way.

The earliest known discussion about decentralized finance dates back to July 2013, when Mastercoin founder JR. Willett launched the first-ever ICO on the bitcointalk forum, stating that only contributors would gain access to advanced features such as decentralized trading and distributed betting built atop Bitcoin. He successfully raised 4,740 BTC, worth around $500,000 at the time.

In 2014, Robert Dermody and others co-founded Counterparty Protocol, a peer-to-peer financial platform and open-source distributed protocol built on the Bitcoin blockchain.

Its primary function: enabling users to create custom tokens on the Bitcoin blockchain. Counterparty has a native currency called XCP, generated via a “proof-of-burn” mechanism using Bitcoin.

Counterparty introduced financial tools unavailable on Bitcoin itself, such as derivatives. Overstock.com used Counterparty to trade regulated securities on-chain. It also created a decentralized asset exchange supporting various digital assets. Users interacted with Counterparty using the counterpartyd node software or the Counterwallet web wallet.

Counterparty even implemented Bitcoin-based equivalents of smart contracts and dApps. It provided an open, decentralized platform enabling financial activities without relying on central authorities. Notable NFT projects like Spells of Genesis and Rare Pepe were built on Counterparty.

Overall, the Counterparty Protocol leveraged Bitcoin’s network and technology to deliver financial products and services missing from Bitcoin itself, evolving into a more comprehensive decentralized finance platform. To this day, Counterparty remains active—one of the oldest and most renowned DeFi platforms in history.

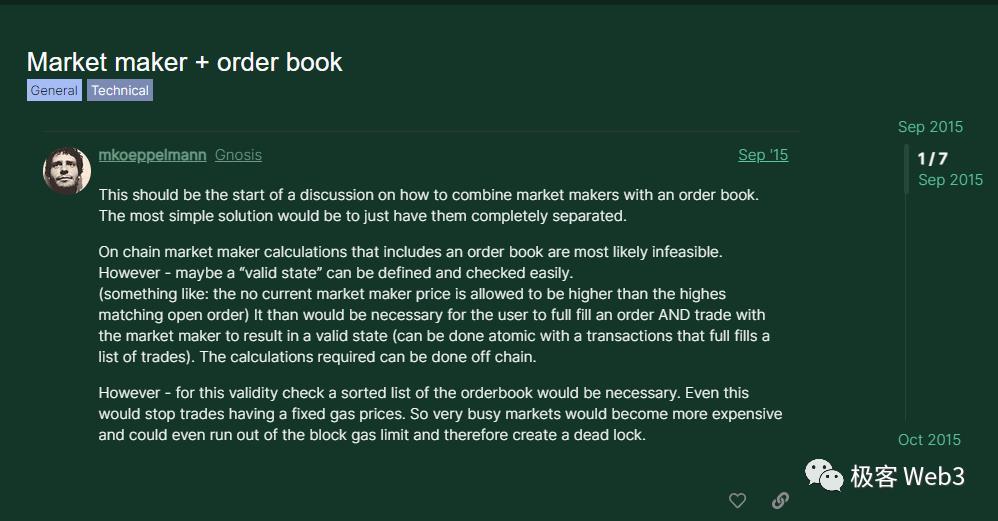

On September 15, 2015, Martin, founder of Gnosis, posted thoughts on his personal forum about combining MarketMaker and OrderBook models— the earliest known discussion I’ve found regarding decentralized prediction markets.

Gnosis is a decentralized prediction market built on Ethereum, offering an open platform for forecasting event outcomes and significantly simplifying the creation of customized prediction market applications. Leveraging blockchain’s trustless execution and smart contracts, Gnosis allows greater flexibility and freedom in participating in prediction markets, vastly expanding their potential.

By the way, Martin is quite influential—the Gnosis Chain (formerly xDai Chain), Balancer, SAFE Wallet, and CowSwap are all connected to him.

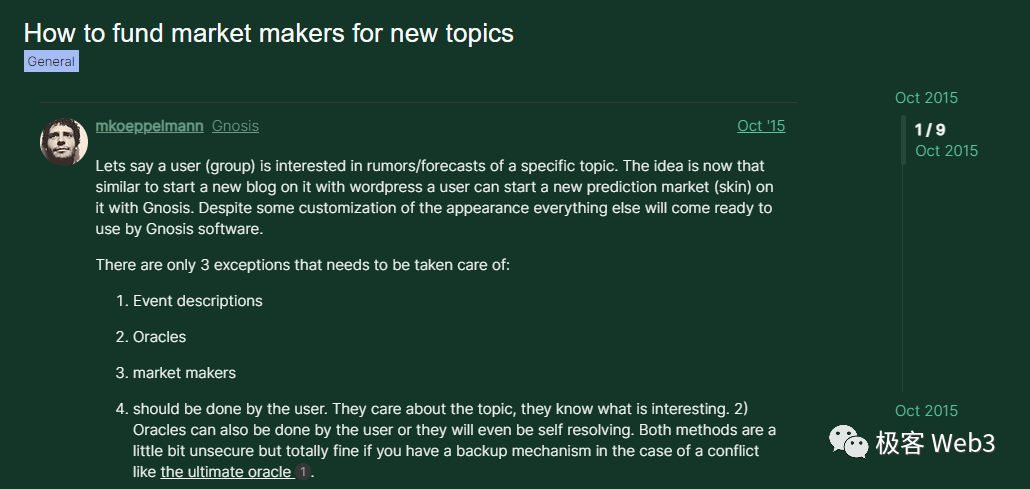

On October 27, 2015, Martin initiated another discussion on his forum, focusing on how to provide initial funding for newly created Prediction Topics to ensure proper market operation.

Ideas included project grants or partnerships with investors and foundations to secure funding. The post emphasized the importance of community participation. This appears to be the earliest known discussion I’ve uncovered about incentivizing liquidity and engagement in DeFi.

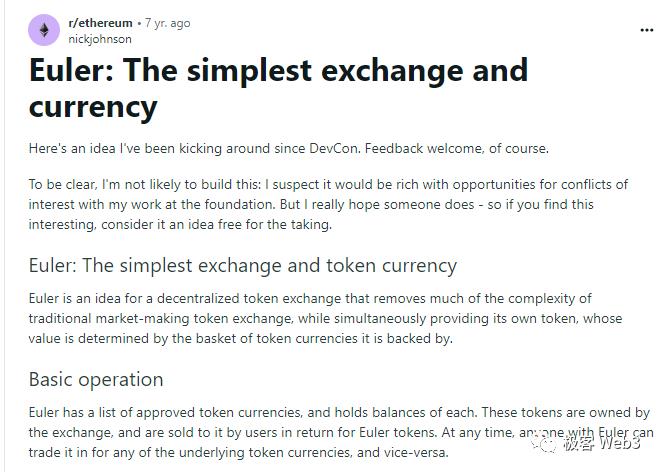

On September 26, 2016, Nick Johnson, lead developer of Ethereum and ENS, posted on Reddit introducing a concept called Euler, a decentralized exchange idea. Key points included:

Euler would allow users to purchase Euler tokens using various other tokens. The number of tokens held determines how many Euler tokens can be redeemed. Buying the first Euler token costs 1 unit of another token, the second e units, the third e² units, and so on—prices growing exponentially.

When adding a new token, a bidding phase would determine its initial price. The total value of all Euler tokens should equal the total value of all tokens held by the system, helping insulate against volatility in individual assets.

Additionally, mechanisms should exist to quickly halt purchases of compromised tokens to prevent exploitation. Overall, this system was elegantly simple and decentralized, though its economic implications required further study.

The Dawn of AMM

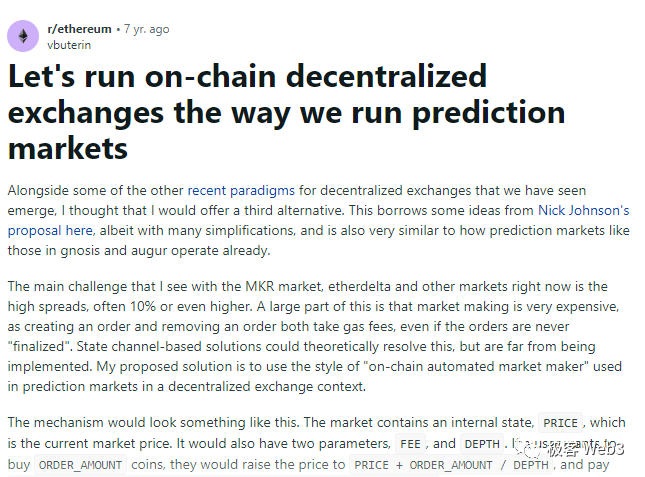

On October 3, 2016, Vitalik published a post on Reddit, inspired by Nick Johnson and emerging DEX concepts, proposing a novel approach to running decentralized exchanges:

Using an on-chain automated market maker (AMM) mechanism similar to prediction markets, eliminating the need for order placement and cancellation typical of traditional exchanges.

Users could “invest” in the market maker, increasing depth and earning a share of profits, thereby reducing risk. Compared to traditional exchanges, this method could drastically reduce spreads, requiring on-chain interaction only during actual trades. The post also addressed challenges like adding new tokens and halting purchases during excessive price swings. Later discussions explored multi-asset support and fee structures for depositors and withdrawers.

This post laid the foundation for AMM-style DEXs, ultimately unlocking a multi-billion-dollar market.

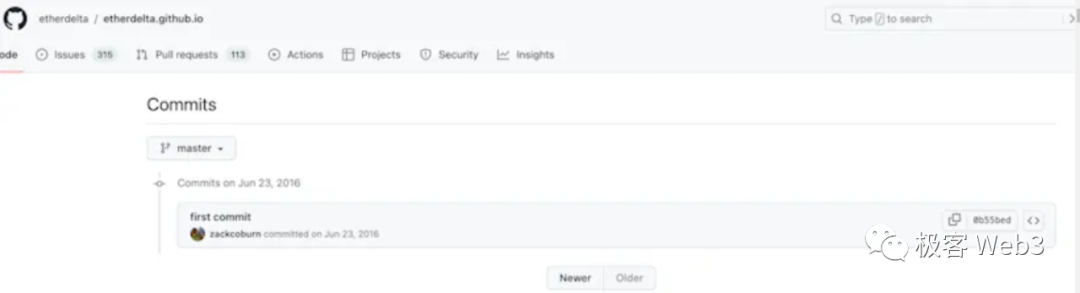

In June 2017, EtherDelta (also known as YiDe) officially launched, becoming the first Ethereum-based DEX recognized by regulators, having completed registration with the U.S. SEC prior to launch.

But as early as June 23, 2016, EtherDelta’s founder Zachary Coburn (“Zack”) had already made the first GitHub commit. EtherDelta was the first DEX to register with the U.S. Commodity Futures Trading Commission (CFTC).

Overall, EtherDelta became the first Ethereum DEX in 2017 largely due to its strong decentralization, low barrier to entry, high anonymity, low cost, and stable performance. Its technical design was as follows:

It used smart contracts to implement an order book trading system. Users publish, cancel, and match buy/sell orders via trading contracts. Order books and trade records are stored on the Ethereum blockchain, enabling full decentralization. Accessible via web or mobile browsers without dedicated apps.

The website uses JavaScript to interact with EtherDelta’s smart contracts, retrieving order book data and facilitating peer-to-peer trades. Publishing or canceling an order requires broadcasting a transaction on Ethereum and paying gas fees. When a taker clicks an order, the contract automatically deducts the buyer’s assets and sends them to the seller—on-chain settlement.

Smart contracts record every trade, including involved addresses, token types, and quantities. User funds remain in their own wallets—not controlled by EtherDelta. The platform charges a 0.3% fee, borne entirely by the buyer. The entire process ensures decentralization and transparency but depends heavily on Ethereum’s network performance.

EtherDelta had several drawbacks at the time:

Manual order matching. Traders had to manually search for suitable orders and confirm matches, meaning both parties needed to agree on price simultaneously—an entirely manual process lacking automation.

Slow order processing speed. Orders could take a long time to fill due to Ethereum’s inherent latency and weak liquidity at the time.

Wasted gas fees. Due to high latency in the order book, multiple takers might attempt to execute the same maker order simultaneously. Only one succeeds, while others fail and lose their gas fees.

EtherDelta later faced controversies, including allegations of insider trading by its former CTO. See the SEC complaint filed on November 8, 2018. The report concluded that certain digital assets (e.g., ERC-20 tokens) qualify as securities subject to SEC regulation. Thus, platforms trading such assets must register as securities exchanges—something EtherDelta failed to do.

Although Coburn neither confirmed nor denied the SEC’s claims, he agreed to settle, paying $300,000 in disgorgement, $75,000 in fines, and $13,000 in pre-judgment interest. The SEC proved that:

EtherDelta violated securities laws, and Coburn caused those violations, knowing or should have known his actions would result in such breaches.

EtherDelta was particularly unfortunate—it had registered with the U.S. CFTC, primarily because it dealt mainly with cryptocurrencies rather than financial securities. However, the SEC later issued guidance classifying many tokens as securities, implying EtherDelta should have registered with the SEC as well. At the time, however, SEC regulations around blockchain innovations were unclear, so EtherDelta did not proactively register.

There was also a messy internal team conflict involving EtherDelta—including a fork called ForkDelta—and due to centralized ownership disputes, it became the first “exit-scammed” decentralized exchange.

Key timeline:

In early 2018, the founding team sold the platform to Chinese businessman Chen Jun. A document dated December 15, 2017, revealed a share transfer, with plans to raise ETH from the market.

On February 9, 2018, the team announced a technical upgrade. On February 18, media reported trading suspension. On February 19, the original foreign tech team, after receiving sale proceeds, forked the project and launched a new platform called “ForkDelta.”

On February 21, 2018, EtherDelta halted trading again, and Chen Jun, the actual controller, disappeared.

The AMM Era Officially Begins

Bancor Protocol launched on June 12, 2017, raising $153 million in its ICO. Bancor’s most important innovation was introducing the AMM mechanism to decentralized exchanges for the first time, solving numerous challenges in decentralized trading and laying the groundwork for AMM applications within the Ethereum ecosystem. Unlike traditional order book models, Bancor used liquidity pools to address pricing and order matching in DEXs, enabling trades without waiting for counterparties.

On September 29, 2017, IDEX, co-founded by brothers Alex Wearn and Philip Wearn, officially launched its beta version, though its source code was first uploaded to GitHub in January 2017.

2017 marked the peak of the ICO bubble, with countless projects launching—many of poor quality. As the ICO market cooled, holders of various tokens sought ways to trade them. At the time, major exchanges were centralized and carried third-party custody risks, creating an opening for IDEX.

Modeled after the Bitcoin-based Counterparty protocol, IDEX delivered first-generation decentralized trading capabilities on Ethereum. Users could trade various Ethereum and ERC20 tokens on IDEX without trusting third-party organizations.

IDEX’s key advantages:

Speed. Using off-chain order book matching, IDEX offered faster trades than EtherDelta, delivering a user experience closer to centralized exchanges.

Security. Built on smart contracts, user assets remained in self-custody, minimizing counterparty risk.

Feature-rich. Supported instant cancellation of unfilled orders (free, as cancellations occurred off-chain), market orders, and other user-friendly functions.

Support for multiple tokens. Already supported over 200 ERC20 tokens at launch, offering broad selection.

Low trading fees. Charged 0.3%, relatively affordable compared to other DEXs.

High anonymity. No KYC required at launch, appealing to privacy-focused users.

However, the entire DEX space was still nascent in 2017, with annual trading volume around $50 million. Though IDEX was popular, volumes remained low—proof that DEX products and ecosystems were immature and needed refinement. An article on November 8, 2018, noted that IDEX consistently ranked #1 among DEXs at the time.

MakerDAO (launched December 2017)

MakerDAO’s key innovations:

Low volatility: By introducing Dai, a USD-pegged stablecoin, MakerDAO enabled users to transact and store value in crypto with reduced exposure to price swings.

Reduced centralization risk: Traditional stablecoins rely on centralized issuers, creating single points of failure. MakerDAO’s decentralized model uses smart contracts and collateralized assets, avoiding reliance on any single entity and allowing direct user participation in governance.

Transparency and autonomy: Adopting a Decentralized Autonomous Organization (DAO) model, MKR holders govern the platform. This enhances transparency, community involvement, fairness, and system reliability.

KyberNetwork (launched February 26, 2018)

KyberNetwork’s main innovations:

Instant swaps: Kyber enables direct, exchange-free token conversions. Users trade via smart contracts without placing orders on centralized exchanges.

Decentralized liquidity pools: Aggregating funds from multiple participants, Kyber creates deeper, more liquid markets. These pools are supplied and managed via smart contracts.

Best-price execution: Smart contracts automatically select optimal prices and liquidity sources, ensuring users get the best rates without comparing exchanges.

Flexible integration: Open APIs and smart contract interfaces allow seamless integration into other DApps and services.

0x Protocol (launched May 2018, raised $24 million in ICO)

Key innovations and problems solved by 0x:

Provided an open-source decentralized trading protocol and API, enabling DApps to build on top with lower development and integration costs. 0x positioned itself as the “settlement layer” for decentralized trading—not a facilitator, but infrastructure upon which any type of marketplace could be built, from eBay or Amazon-like platforms to order-book DEXs—even replicating the granularity and control familiar to traditional finance giants.

Supported arbitrary ERC20 token pairs, not limited to specific pairs. Used a ZRX governance token-based incentive model. Introduced the unique 0x Mesh network connecting relay nodes.

0x built Matcha, a consumer-facing DEX aggregator using 0x API and smart order routing to pool liquidity and deliver optimal trade execution. Other DEX aggregators followed, benefiting from aggregated on-chain liquidity—like wholesalers sourcing from multiple factories and reselling at scale.

Compound (launched September 2018, TVL surpassed $100 million in 2019)

Compound’s key innovations:

First to bring digital asset lending to the Ethereum ecosystem. Compound pioneered cross-asset borrowing and lending of ETH and ERC20 tokens.

No physical collateral required—users simply deposit digital assets into smart contracts to borrow, drastically lowering the barrier to credit access.

Market-driven interest rates: Rates adjust in real-time based on supply and demand, promoting market equilibrium.

Supports multiple mainstream stablecoins and tokens, such as USDC and DAI, offering greater flexibility.

Borrowed assets are immediately usable without settlement delays, streamlining the borrowing process. Users can repay loans anytime and reclaim collateral instantly.

Provides open, non-custodial APIs, greatly accelerating adoption across DApps.

Uses simple, auditable smart contracts— a key reason DeFi went global.

Overall, Compound leveraged digital assets and blockchain technology to deliver efficient, accessible decentralized lending to users worldwide. It addressed cost-efficiency and localization issues in traditional finance, ushering in a new era for DeFi.

dYdX (launched October 2018), once reached over $1 billion in peak TVL. Key innovations and solutions:

Built a decentralized perpetual futures trading platform, allowing users to trade perpetuals on-chain, avoiding risks associated with centralized exchanges and custodial asset holding. Uses a hybrid on-chain/off-chain order book: off-chain for efficiency, on-chain for transparency.Through off-chain order books, dYdX achieves lower slippage, deeper liquidity, high-frequency trading capabilities, and lower transaction costs.

Allows users to stake assets to participate in governance and earn rewards. Offers decentralized leveraged trading across multiple assets, supporting up to 20x leverage. Supports both cross-margin and isolated margin modes, letting users adjust margin ratios based on risk tolerance.

(To be continued)

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News