In the later stage of a Kondratiev depression, "cash is king"

TechFlow Selected TechFlow Selected

In the later stage of a Kondratiev depression, "cash is king"

In the late stage of a downturn cycle, asset allocation still follows the principle of "cash is king," with a defensive approach being holding gold, and a more proactive strategy involving opportunistically buying bonds at阶段性 lows.

Author: Thought Steel Seal

The Two Driving Forces and Four Phases of the Kondratiev Wave

Cycles are the most important macro force affecting investment. There are long cycles such as the 50-year Kondratiev wave, and short cycles like the 40-month inventory cycle. While identifying turning points is critical for short cycles, for long cycles, the key lies in understanding the driving forces, because long cycles span decades—turning points aren't single moments in time. However, by grasping the underlying drivers, one can better navigate the rhythm of the cycle.

In my previous article "Get Rich in Life Through K-Waves: Knowing Where We Are Matters," I analyzed the two core elements of the Kondratiev cycle: capital expenditure and technological revolution. Both experience peaks and troughs—capital cycles reflect subjective human sentiment fluctuations, while scientific progress in technological revolutions follows objective laws. The latter drives the former. Their interplay creates four distinct phases:

1. Boom Phase: Rising Technology & Rising Capital

During this phase, continuous innovation fuels growing capital investment and improves productivity. High growth does not trigger resource constraints, allowing strong economic expansion to coexist with low inflation.

2. Recession Phase: Declining Technology & Rising Capital

Technological gains in productivity begin to diminish at the margin, yet capital continues increasing investment to maintain prior growth rates. This leads to resource bottlenecks, rapidly rising costs, widespread inflation, several notable financial crises, and eventual bursting of bubbles.

3. Depression Phase: Declining Technology & Declining Capital

Capital investment unsupported by innovation becomes unsustainable. Combined with volatile resource prices, the K-wave enters a depression phase where not only speculation disappears, but even normal business operations suffer severe disruption.

4. Recovery Phase: Rising Technology & Declining Capital

New technologies begin emerging, but due to weak corporate profits, there is little new investment. Only under stimulus from low interest rates do surviving firms gradually return toward equilibrium operational levels.

Some argue that this framework “doesn’t apply to China’s A-shares,” which reflects a misunderstanding of the Kondratiev wave. It is not a stock-picking theory—it is first and foremost an economic theory explaining price cycle phenomena. In investing, the K-wave primarily guides asset allocation across major categories, as each phase favors different optimal investments—even if it relates to equities, it won’t tell you what stocks to buy in A-shares, but rather whether it's suitable to invest in stocks at all.

My conclusion in the earlier article "Get Rich in Life Through K-Waves: Knowing Where We Are Matters" was that we are currently near the inflection point between the Kondratiev depression and recovery phases. Although this turning point spans years rather than a precise moment, understanding the causes and characteristics of these two phases remains crucial.

What Happens in the Late Depression Phase?

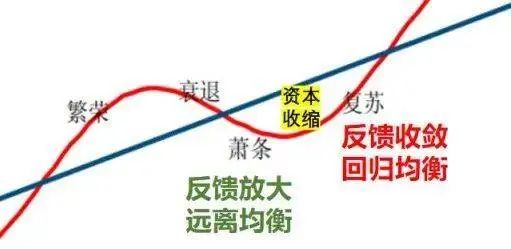

The depression and recovery phases share a common feature: both belong to the stage of “positive feedback caused by capital contraction.”

Positive feedback means price signals (rising or falling) are extrapolated linearly by investors and entrepreneurs who assume trends will continue, prompting them to increase or reduce capital spending accordingly—thus fulfilling their own expectations.

In the depression phase, lack of innovation momentum causes technology to mature into stagnation and declining efficiency of capital investment. Economic expansion slows gradually, leading to shrinking investment, rising inventories, prolonged decline in neutral interest rates, and increasing deviation of growth from its long-term equilibrium level. Innovation isn’t entirely absent during depressions—for example, in this cycle, rapid cost reductions in solar, wind, and lithium batteries have sparked a new energy revolution. Some believe this signals an early arrival of the K-wave recovery.

However, a true technological revolution doesn’t just create a new industry—it enhances efficiency across most traditional sectors. Past revolutions—the steam engine, railways, electrification, automobiles, and IT—transformed nearly every sector and ordinary life. In contrast, upon closer examination, the new energy revolution mainly replaces fossil fuels; it has neither created massive new demand nor significantly boosted productivity across industries so far.

Without broad-based incremental demand, large-scale capital expenditures (from 2021 to present) quickly result in overcapacity and insufficient demand, reinforcing the defining features of a Kondratiev depression phase.

By contrast, during the boom phase of the last K-wave, the internet revolution drove capital spending expansion while unleashing vast new human demands—without triggering sharp inflation or overcapacity. These differences highlight how distinct types of technological revolutions operate within different stages of the K-wave.

The difference between depression and recovery lies in this: late-stage depression sees amplifying positive feedback from capital contraction, pushing the economy further from its long-term growth equilibrium; whereas recovery represents converging feedback, bringing the economy back toward equilibrium growth.

Why does capital contraction shift from amplifying to converging feedback?

As mentioned previously, the turning point from “recession → depression” coincides with a cyclical trough in commodity prices, driven by oversupply. For instance, around 2015, supply peaked globally due to capital spending-driven capacity expansion, particularly in China. On the demand side, after passing the smartphone upgrade peak, diminishing marginal utility from the tech revolution led to shrinking demand. Combined with other short cycles, this created a deep commodity price trough.

This commodity price trough reinforced widespread belief in recession and depression, prompting further cuts in capital spending. Since much of the capacity expansion occurred in China, this triggered China’s supply-side reform beginning in 2016.

The original goal of capacity reduction was simply to address overcapacity, but if investment declines without corresponding efficiency gains, the result is only further demand contraction—as seen in the shrinking private investment starting in 2018. Capacity keeps being cut, yet overcapacity worsens, signaling entry into a stage of "amplified feedback."

From the perspective of the Kondratiev depression, regardless of policy intent, any industrial or economic policy will generate strong “feedback amplification” effects if aligned with long-cycle dynamics—often undermining its original goals.

Of course, policymakers attempt corrections during this phase—using loose monetary or fiscal stimulus to counteract the alternating contraction of capacity and demand (“feedback amplification”). This prevents capacity decline from following a straight downward path, instead creating multiple reversals.

For example, in 2020, global fiscal expansions to combat the pandemic, combined with shipping bottlenecks from lockdowns, briefly ignited a global commodities bull market. Subsequent Fed tightening then drove up interest rates and the dollar index.

Such repeated swings during capital contraction, driven by institutional “muscle memory,” sometimes produce alternating inflation and recession—or even make stagflation more likely.

During the last K-wave depression, oil embargoes from Middle East wars and aggressive Fed policies led Western economies into prolonged stagflation, punctuated by two recessions (1974–1975 and 1980–1982).

The second recession (1980–1982) overlapped with the initial phase of the fifth Kondratiev recovery—and also marked the lowest point in capital spending. Bearish sentiment dominated; few companies had confidence to invest. Yet precisely because the economy had deviated so far below its long-term growth trend, corporate earnings stopped declining. With some industries beginning to adopt information technology, internal recovery forces slowly broke the self-reinforcing “amplified feedback” of capital contraction, transitioning into a “converging feedback” phase—i.e., the onset of the Kondratiev recovery.

Thus, the transition from depression to recovery can span several years—in market terms, not a V-bottom, but a rounded bottom.

Still, certain economic markers appear near the turning point—for example, it may coincide with the inflection point of one or two inventory cycles marked by severe overcapacity.

Although similar to the “recession → depression” trough—a commodity bear market low—the causes differ fundamentally. The “recession → depression” trough stems from absolute overcapacity due to upstream supply expansion and high corporate inventories; the “depression → recovery” trough results from extreme demand collapse causing relative overcapacity. Actual inventory levels aren’t necessarily high, but pessimistic entrepreneurs perceive them as excessive. These reflect differing confidence levels among capital and entrepreneurs.

The fourth Kondratiev depression (1974–1982) differed significantly from prior ones. Structurally, deflation should dominate depressions, but after moving from the gold standard to the dollar standard, governments gained greater intervention capacity. To combat exogenous inflation from the oil crisis, persistently high interest rates instead pushed the global economy into prolonged stagflation—an atypical depression trait.

Yet external policy cannot override internal long-cycle forces. In the late depression phase (1979–1982), the simultaneous decline in GDP and CPI revealed classic recessionary traits. Prolonged high rates crushed demand faster than supply could adjust, creating a negative output gap. Months later, when CPI stabilized, the long cycle officially entered the recovery phase of the fifth Kondratiev wave.

The inventory cycle lasts about 40 months—an intermediate cycle. Long-cycle turning points often emerge through resonance with other short-cycle inflections.

So, when might this current turning point occur? Let’s speculate boldly.

What Happens Near the Turning Point?

Each cycle carries unique era-specific traits. Today, China accounts for the largest share of global manufacturing capacity, hence faces the highest degree of domestic overcapacity. As some production relocates abroad, existing Chinese facilities sit idle—creating a fragmented imbalance: overcapacity in China, undercapacity and strong investment in recipient regions, though not enough to offset China’s surplus.

Currently, deflation appears only in China. But the “depression → recovery” turning point should be global in nature. Therefore, this inflection hasn’t arrived yet—it may require waiting until after the U.S. enters recession and easing cycles, hitting a global demand trough in some future year.

Meanwhile, since Q3, China’s economy has entered an upward phase of weak recovery driven by an inventory cycle inflection—this leg will take about a year to play out. After another year or more following a global downturn or stagflation episode, a plausible timing would be 2025 or later.

But as I’ve argued, rather than a sharp turning point, this is better described as a “long season”—a phase where inventory levels diverge, prices rebound and retreat multiple times, and bankruptcies of financial institutions, large corporations, or small economies spark recurring crises. Unlike the sudden 2008 crash from prosperity to crisis, this process involves repeated oscillations between hope and despair, culminating in resignation—watching the crisis unfold and consciously choosing to “lie flat” instead of fighting.

This closely mirrors the psychological state at the bottom of a stock market bear phase.

Drawing parallels with the deep 1979–1982 recession: although inflation eased, interest rates fell even slower, while GDP declined faster. Manufacturing accelerated its offshoring, and Japan’s high-value goods flooded Western markets. Market confidence evaporated—S&P 500 PE ratio dropped to a historic low of 9x.

In reality, transformative new technologies were already emerging. Yet near this bottom, public perception of technology was at its most conservative. Most firms felt no change. Many believed technological progress had permanently stalled—that the world would remain static forever.

In “Get Rich in Life Through K-Waves: Knowing Where We Are Matters,” I described early recovery mindset:

The last recovery began in 1982. Though PC and internet—the core technologies of that K-wave—had been invented, their impact on daily life remained minimal. That year, Microsoft had just defined its OS direction; Macintosh, which shaped personal computers, wouldn’t launch for two more years; Windows 3.0, the world-changing system, was eight years away. Internet use was limited to universities and the military. Ordinary lives hadn’t changed in years—people used century-old telephones, watched 30-year-old TVs, read 200-year-old newspapers, drove cars invented a century prior. Chemical industry breakthroughs dated back 30 years. No major drugs significantly extended human lifespan in the 40 years since penicillin. To today’s youth, 1982 might as well be medieval times.

Therefore, claims that AI has already ushered us into a new Kondratiev recovery overlook a key fact: behind every technological advance lies capital—especially true for today’s GPT-style AI algorithms, which rely heavily on chip computing power and energy consumption. Unless revolutionary changes occur soon—like room-temperature superconductors, controlled nuclear fusion, or ultra-high-performance chips—algorithmic advances will quickly hit resource limits and lose economic viability.

Moreover, in the short term, high-interest-rate environments make capital too expensive to sustain massive burn rates. Without endless funding, AI’s evolution is unlikely to accelerate significantly.

Only when interest rates fall—near the “depression → recovery” inflection—will capital cautiously re-enter. Even then, sustained investment won’t resume until a truly revolutionary product emerges, akin to Windows 3.0.

So practically speaking, what major assets should one hold in the late depression phase?

What to Buy in the Late Depression?

The economic depression phase features stagnant technological progress and frozen capital spending, with prices shaped by simultaneous declines in demand and supply. Especially in the later stage, economic policy becomes ineffective: tight money during inflation fails to fix supply issues, while expansionary fiscal policy in downturns risks debt traps.

Therefore, major asset allocation in the late depression phase still favors “cash is king”: defensive investors hold gold, while proactive ones selectively accumulate bonds during dips.

Equities offer no sustained opportunities. Growth stocks may rise temporarily after rate hikes pause, but will likely face one final deep drawdown within the cycle. Consumer stocks are worth accumulating, as they typically outperform once recovery begins. Value stocks perform relatively well, but upside is limited—investors risk getting trapped in the final rally wave. Only overseas healthcare stocks offer persistent potential, though domestic performance depends on medical insurance policy.

Regarding tech stocks, for long-term investors, this phase may indeed be time to position early. Microsoft and Intel—giants of the next boom—were founded during the prior depression. But in 1977, few could foresee Apple and Microsoft becoming titans, while IBM, Xerox, and Kodak faded. Moreover, tech stocks underperformed the broader market throughout the last depression and recovery phases; real gains came only in the subsequent boom.

Commodities: sometimes during depressions, supply drops too fast, creating temporary imbalances and price spikes—such as the two oil price surges last year and this year. Intermediate rallies remain possible, but with both supply and demand declining in late depression, most commodities are unlikely to surpass prior highs.

Furthermore, traditionally cyclical sectors see reduced elasticity—price rebounds occur only when supply falls too sharply (e.g., display panels, hog farming). Oversized capacity planning consistently outpaces demand, turning them into weak cycles.

After publishing the last piece, some asked whether China could develop its own Kondratiev cycle. This idea made sense historically—China did have independent cycles. But after joining the WTO in 2001, it increasingly became the world’s manufacturing base and factory, tied to the global economic cycle “in sync.” The clearest example: in early 2008, China’s leadership feared overheating; by year-end, it launched unprecedented fiscal stimulus—all triggered by the U.S. subprime crisis.

Once globalization starts, it cannot be fundamentally reversed. Whether it’s Western talk of decoupling or tech blockades against China, none can alter the fundamental trajectory of this cycle.

Moreover, while the U.S. led the last Kondratiev cycle, the next cycle’s leader may not necessarily be China—but our influence will undoubtedly exceed that of the previous cycle.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News