DWF Labs: An Overview and Strategic Analysis of the Decentralized Perpetual Contracts Ecosystem

TechFlow Selected TechFlow Selected

DWF Labs: An Overview and Strategic Analysis of the Decentralized Perpetual Contracts Ecosystem

This article examines the current state of perpetual contracts, analyzes the differences between CEXs and DEXs, reviews the evolution of existing DEX perpetual protocols, and discusses potential developments in this field.

Author: DWF Labs Research

Compiled by: Kaori, BlockBeats

In the early articles of our "Hindsight" series, we introduced DWF Ventures’ 2023 investment thesis, detailing three key areas we focused on:

· Derivatives protocols

· Consumer Dapps

· Data and privacy layers within infrastructure

For the first area, derivatives protocols cover a broad range of products. This includes various financial instruments such as futures, options, structured notes, and bonds. However, in this article, we will focus specifically on one of the most prominent derivatives in the crypto space — perpetual contracts. Here, we explore the current state of perpetuals, analyze differences between centralized exchanges (CEX) and decentralized exchanges (DEX), review the evolution of existing DEX perpetual protocols, and discuss potential developments in this space.

Perpetual Contracts: A Product Fit for the Crypto World

For beginners, perpetuals (or perps) are currently the most popular derivative contract in the crypto market. Since their introduction by Bitmex in 2016, perpetual contracts have steadily captured market share from traditional futures contracts.

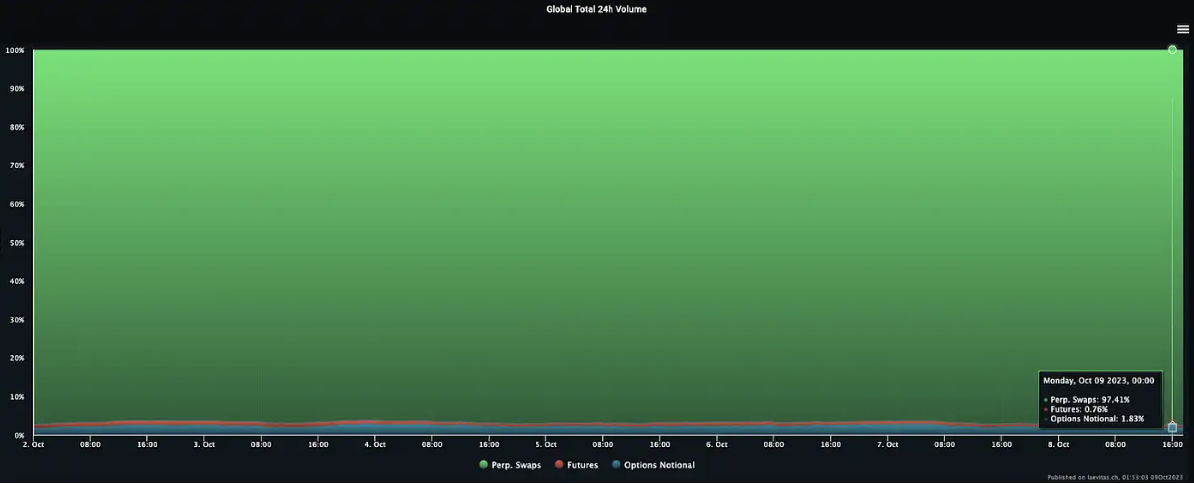

Today, perpetuals account for an astonishing 97% of total trading volume.

The popularity of perpetual contracts can be attributed to two main factors:

· Flexible contract duration: Perpetuals offer flexibility, allowing positions to remain open indefinitely or until traders choose to close them. Fixed expirations in traditional futures serve practical purposes in hedging risk and pricing future production and delivery costs for physical commodities. However, in digital assets like Bitcoin, these costs are negligible, making term- or delivery-based hedging unnecessary.

· Better alignment with spot prices via funding rates: Without expiration dates, perpetual contracts use funding rates to ensure their prices stay closely tied to the spot market. Compared to price volatility during futures expiry periods, this method results in less price fluctuation.

Ultimately, these factors simplify the trading experience, making it easier and more intuitive for users to manage leveraged positions. As a result, perpetuals have become one of the most widely adopted derivatives.

Mismatch Between CEX and DEX Perpetuals

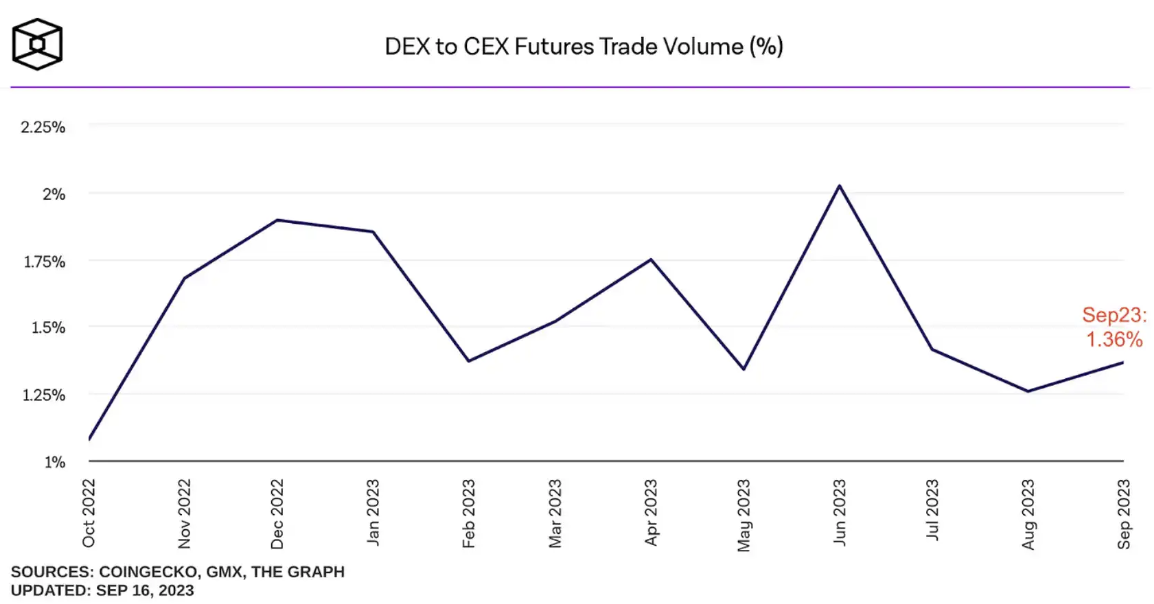

Given the success of perpetual contracts, one might expect this success to extend equally to both centralized and decentralized cryptocurrency exchanges. However, there is currently a severe imbalance in trading volume between DEXs and CEXs, with DEXs accounting for only about 1% of total volume.

This stark contrast highlights that, compared to most decentralized venues, centralized exchanges still hold a clear advantage in central limit order books (CLOB) and trading workflows.

Creating a Decentralized 'CEX Experience': The Limit Order Book Model

CEXs use the CLOB model for trading because it is one of the most efficient ways to match buyers (takers) and sellers (makers). These limit order books can process up to 100,000 orders per second on CEXs like Binance, with average latency as low as 5 milliseconds. The model allows sophisticated participants such as market makers to interact with the system and facilitate fair price discovery. This helps users obtain the best possible prices with minimal slippage.

However, due to blockchain limitations such as block finality, speed, and gas fees, replicating the limit order book (LOB) model in DeFi has proven challenging. This challenge led to the emergence of automated market makers (AMMs) as an alternative solution. AMMs allow permissionless token trading without relying on centralized exchanges or market makers, as liquidity providers (LPs) assume responsibility for facilitating trades.

Nevertheless, inherent AMM algorithms come with drawbacks. They tend to result in higher slippage, especially for larger trade sizes and during periods of market volatility. This fundamental limitation underscores why market makers are inherently more incentivized to participate in the LOB model. The LOB model allows market makers to enter positions at favorable bid-ask prices, significantly reducing the risk of being in losing positions. In contrast, liquidity providers (LPs) in AMMs primarily rely on user trading fees as their revenue source. However, when traders profit, these fee earnings may be offset by impermanent loss. This makes AMMs less attractive to LPs compared to the potential profitability demonstrated by the LOB model.

DYDX: Pioneer Leading the Decentralized Perpetual Market

Recognizing this market gap, dYdX pioneered the introduction of the order book model into the decentralized perpetual space. As a first mover, dYdX gained necessary market share and established itself as the top decentralized exchange (DEX) for perpetual contracts by trading volume. Through its order book (LOB) model, it offers the lowest maker and taker fees among all DEX perpetual protocols—a key factor in its dominant position. Currently, dYdX operates on Layer 2 (L2) infrastructure powered by StarkEx, enabling higher transaction throughput.

However, due to inherent limitations of the underlying blockchain, dYdX has not yet achieved full decentralization. It employs an off-chain matching engine because an on-chain model would be too slow and inefficient for users. StarkEx scales dYdX by processing and verifying transactions off-chain, only submitting STARK proofs on-chain. Processing transactions on-chain means they occur on Ethereum, which is inefficient given that each block update supports roughly every 12 seconds.

To achieve full decentralization, attempts have been made to introduce fully on-chain order books at the cost of running on other chains, such as Solana. Protocols like Zeta and Mango Markets leverage Solana’s fast block times (~0.5 seconds) to deliver optimal on-chain experiences. However, even Solana’s on-chain order books still lag significantly behind CEXs—Zeta can accommodate no more than 910 bids and asks simultaneously, and speeds remain noticeably slower than CEXs. The limited growth of these protocols suggests that decentralization alone isn’t a critical advantage for users.

Therefore, increasing trading volume and liquidity remains key to competing with CEXs. dYdX is moving toward building its own L1 on Cosmos, leveraging the Tendermint Byzantine Fault Tolerance (BFT) consensus mechanism. Beyond a 1-second block time and performance of up to 1,000 transactions per second (TPS), Tendermint BFT allows customization of validator sets and responsibilities. Each validator ensures that orders and cancellations are consistently propagated across the network. However, this is not an on-chain operation since it does not commit to consensus. Orders are still matched off-chain, then submitted on-chain every block.

Thus, concerns arise about dYdX facing high centralization risks, as validators may have incentives to collude with market makers for MEV profits through front-running or reordering. To address this, dYdX is collaborating with Skip Protocol and Chorus One to mitigate malicious validator behavior. Slashing could be used to deter collusion between market makers and validators, with penalties set at levels where validators are unwilling to take on additional income risks.

Pushing the Boundaries of Decentralized LOB Perpetual DEXs: Hyperliquid

Other protocols are also following suit by creating their own L1s—for example, Hyperliquid, which is still in testnet. This appchain was manually built by the team using only Tendermint for consensus. It reportedly handles up to 20,000 operations per second (including orders, cancellations, liquidations), approximately 20 times the capacity of dYdX v3. It uses a hybrid of external and internal market makers (HLP LPs), promoting greater decentralization since anyone can provide liquidity. Through optimizations in infrastructure and application code, it manages to place the entire order book on-chain. This ensures ordering transparency, unlike off-chain order books where validators can capture MEV for themselves. Additionally, a DAO will manage the insurance fund, contrasting with dYdX’s team-controlled insurance fund. Overall, Hyperliquid decentralizes more aspects of the protocol compared to dYdX.

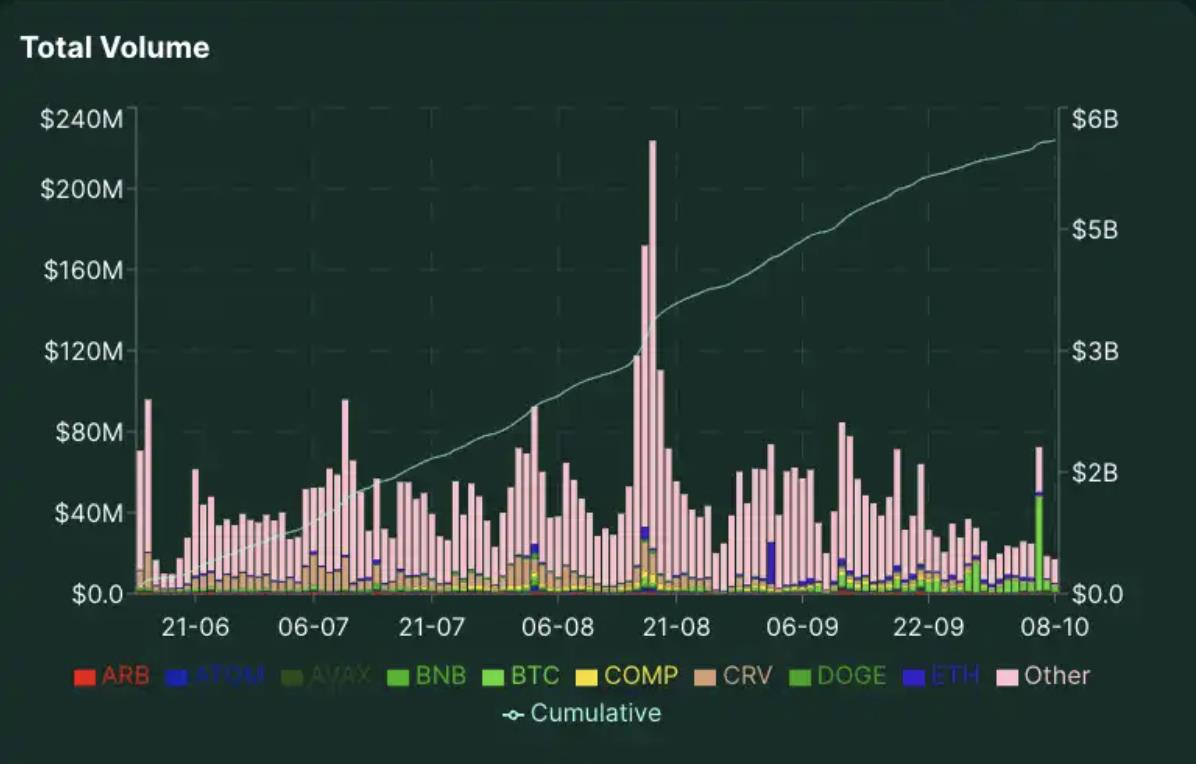

Since launching its alpha mainnet on June 14, the protocol has processed over $5.6 billion in trading volume, averaging $47.8 million daily. While this is only a small fraction of dYdX’s volume, it is comparable to GMX and exceeds Perpetual Protocol’s daily trading volume.

However, current trading volume and liquidity may be driven by airdrop speculation, and it remains unclear whether these levels can be sustained without incentives. Initially, the protocol may be quite centralized, with most validators being the core team to ensure smooth operation and uptime. Gradual decentralization may bring consensus issues—a challenge dYdX may also face. Overall, the appchain model is relatively new, and it will be interesting to see how the protocol performs under stress during volatile periods.

Nonetheless, dYdX remains the clear market leader in the decentralized perpetual space, thanks to its low fees, deep liquidity, and battle-tested model across varying volatility conditions. Immediately following the collapse of FTX in November 2022, dYdX saw a 39% increase in user numbers. Since then, dYdX’s average monthly trading volume has continued to rise, indicating it provides a solid alternative to CEX traders.

Adapting the AMM Model for DeFi: Introducing vAMM for Perpetuals

Within DeFi, AMMs (automated market makers) helped solve the issue of high gas fees associated with numerous trading orders. Perpetual Protocol advanced this field further by introducing the concept of virtual automated market makers (vAMMs), specifically designed for perpetual contracts.

How Virtual Automated Market Makers Work: Insights from Perpetual Protocol

In the virtual automated market maker (vAMM) model, liquidity providers (LPs) play a unique role. Unlike traditional setups where LPs directly hedge against traders, here traders provide liquidity to each other through a collateral vault located outside the vAMM ecosystem. This vault plays a crucial role in generating virtual tokens, facilitating perpetual contract trading.

The vAMM mechanism relies on the x*y=k constant product formula, a well-established concept in decentralized finance (DeFi). However, there's a key difference: in this case, the value of “k” is not determined by real assets in a pool but is manually set by the platform team. This manual control ensures the value of “k” remains balanced to prevent users from suffering slippage (if “k” is too low) or encountering significant price deviations relative to the index price (if “k” is too high).

Compared to order book systems, where long and short open interest levels remain equal, the vAMM model allows freely floating net open interest. To maintain price stability and align with the index price, funding rates play a role. These rates incentivize arbitrageurs to participate and push perpetual prices closer to spot prices.

Challenges Faced by Perp v1

However, Perp v1 posed significant risks to the protocol due to persistent long-short imbalances. The protocol had to intervene by paying funding to traders, funded from the insurance pool. In theory, trading fees should always exceed the total amount paid out to traders to make the protocol model sustainable. Unfortunately, during highly volatile periods—when deviations between mark and index prices were large—the model proved unsustainable. As markets declined, overestimating the “k” value increased funding rate payments, eventually draining the insurance fund. Consequently, Perp v1 was phased out.

Evolution of Perp v2

Perp v2 attempts to mitigate the risks that plagued v1 by utilizing Uni v3 pools as the execution layer for liquidity. Although LPs still provide “single-sided liquidity,” collateral is converted into two virtual tokens (e.g., USDC collateral generates equivalent vUSDC and vETH, which are then deposited into a Uniswap vUSDC-vETH pool) for range orders. This approach ensures every long order corresponds to a short order taken by a market maker, and vice versa. Thus, funding payments are limited to counterparty-to-counterparty interactions, excluding the protocol and traders as seen in v1. By concentrating liquidity, LPs can achieve higher capital efficiency while traders enjoy better prices and reduced slippage. However, if LPs do not hedge their positions accordingly, they will still experience impermanent loss in this model.

V2 uses Uniswap v3 TWAP and Chainlink oracles to determine the index price. Theoretically, as long as an asset has a price data source on either oracle platform, it enables permissionless listing. However, listing other assets still carries risks, and the process is managed by a DAO, adding complexity to new market creation. Because the protocol defaults to cross-margin, users’ collateral is automatically shared across different positions in their accounts. Long-tail assets, due to their inherent volatility and lack of liquidity, pose significant risks to these portfolios, presenting major challenges for the protocol in listing such assets.

Overall, vAMMs offer a good option for traders seeking decentralization and instant liquidity. However, in the Perp v2 model, liquidity providers (LPs) must bear the risk of impermanent loss. They are compensated through higher fees collected from trades, effectively passing the cost onto traders. Additionally, vAMMs are constrained by the amount of liquidity in the pool, leading to price slippage for larger trades. The model still heavily relies on arbitrageurs to reduce the gap between mark and index prices, who are incentivized by funding rates. As a result, the top 10 traders on Perp v2 account for approximately 88% of the daily trading volume across all pairs. Therefore, the protocol better suits market-savvy LPs and arbitrageurs, as traders could enjoy lower fees and deeper liquidity on other platforms.

Combining the Best of Both Worlds: Connecting Order Books with AMMs for Optimal Trading

Lessons from Perp v1 and Drift v1 show that pure vAMM models are unsustainable in the long run. A similar situation occurred with Drift v1, which used a dynamic vAMM (dAMM) model adjusting virtual reserves (k) based on trading demand. However, during the LUNA price crash, long-short imbalances escalated rapidly. Simultaneously, smart contract settlement issues allowed traders to withdraw large positive PnLs without corresponding negative PnLs, causing bad debt to exceed the insurance fund. This triggered a bank-run scenario, forcing trading and withdrawals to be suspended.

Drift v2: A Hybrid Solution

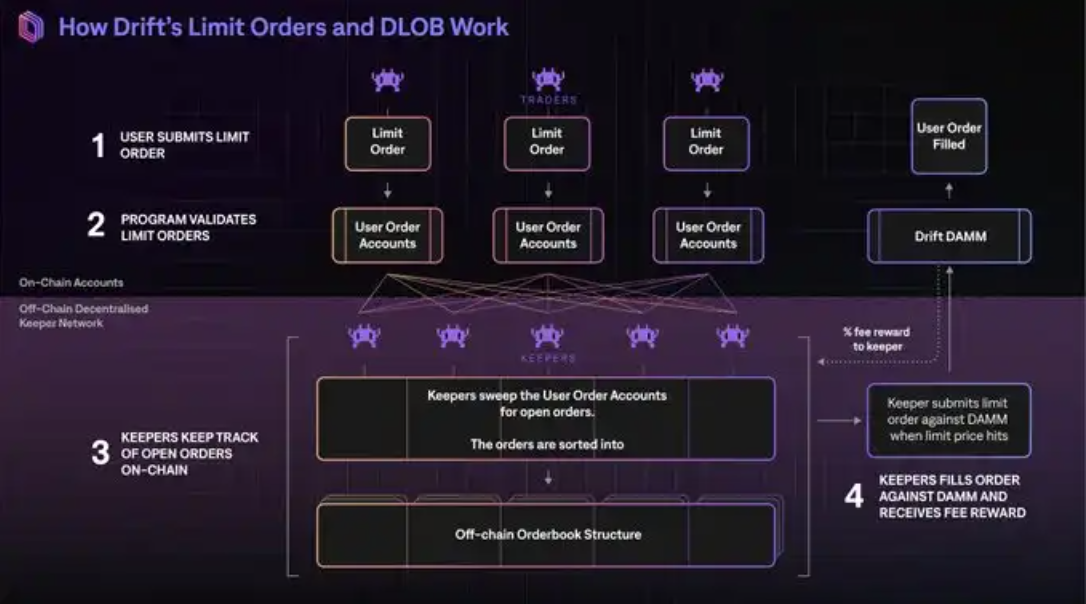

Drift v2 aims to resolve the dAMM model issues in v1 by introducing a hybrid approach that leverages both order books and dAMM as sources of liquidity. Drift v2 allows trades to be routed through three liquidity sources, ensuring large orders can be efficiently matched on-chain.

1. Just-in-Time (JIT) Liquidity: Market makers compete via Dutch auctions to fill market orders. Auctions start at the market order price and gradually change. The auction lasts 5 seconds.

2. Decentralized Limit Order Book (DLOB): Orders are routed through a decentralized limit order book managed by keepers, matched with market makers who earn a percentage of fees from trades.

3. AMM: This component ensures user orders are always filled, even without active market makers. Funding rates are used to target neutrality (i.e., premium on short positions if net long).

Advantages of the Hybrid Model

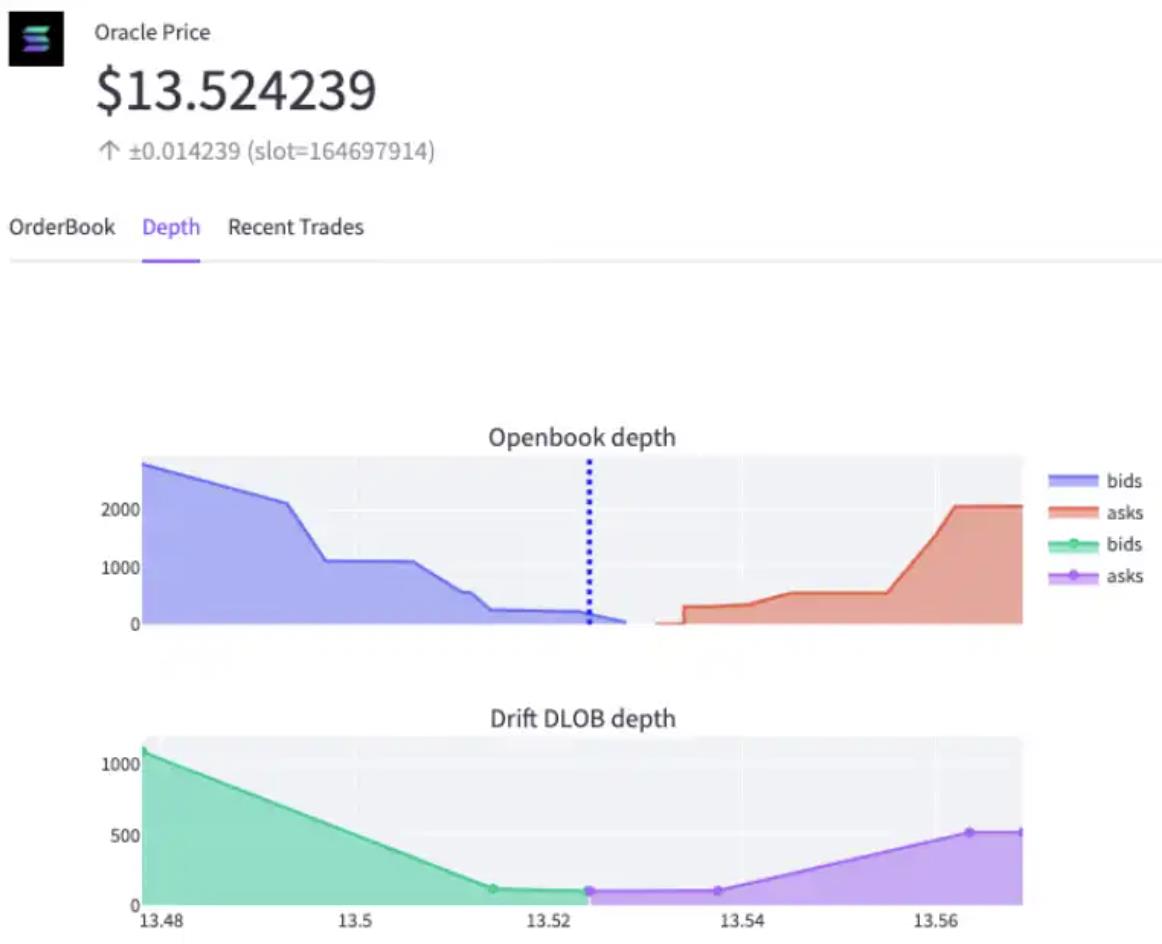

By combining the order book and AMM models, Drift bridges the gap in reducing slippage for large trades—an obstacle preventing full migration to on-chain trading. Another benefit of this model is tighter bid-ask spreads on Drift’s decentralized limit order book (DLOB) compared to other Solana perpetual DEXs. This stems from market makers’ ability to input limit orders based on real-time oracle prices and price offsets—known as oracle-offset orders.

Combined with the reversal of the maker-taker sequence found in traditional order books (i.e., makers are “passive” because takers specify their orders before makers compete to execute), this enhances competition and incentivizes market makers to quickly fill orders. Compared to traditional LOBs, this method is also more efficient, as market makers don’t need to actively manage positions (e.g., repricing as prices move). Thus, incentives are aligned with both counterparties—encouraging market makers to continue providing liquidity, as the protocol reduces toxic liquidity for takers while ensuring takers get the best execution price through competition among makers.

The hybrid model significantly improves liquidity, enhancing trader experience through better pricing and faster execution. On Drift, over half of the trading volume is now handled by market makers rather than dAMM, demonstrating the effectiveness of adding an extra liquidity layer. Having external liquidity sources also helps balance AMM inventory skew, lowering the likelihood of impermanent loss for LPs and reducing the need for arbitrageurs to step in. In the near future, more iterations may refine this model further, with protocols like Vertex and Syndr also building toward hybrid order book-AMM models.

Rise of the Liquidity Pool Model in Perpetual DEXs

Driven by the growth of protocols like Synthetix and GMX, the liquidity pool model is gaining increasing popularity in perpetual contract trading. Over the past year, we’ve observed a growing number of new decentralized exchanges adopting this model.

GMX’s Unique Approach

A notable example is GMX. GMX is a decentralized spot and perpetual trading platform built on Arbitrum and Avalanche. Unlike typical AMM models, GMX adopts a peer-to-pool model.

GMX v1 features a multi-asset pool and a dynamically aggregated oracle provided by Chainlink to determine true asset prices. GLP consists of an index of assets used for swapping and leveraged trading, such as BTC, ETH, AVAX, UNI, LINK, and stablecoins. Depositing any index asset mints GLP tokens. GMX v2 also introduces a separate GM pool (GMX Market Pool), allowing liquidity providers to customize exposure by selecting specific tokens they prefer to support.

GLP essentially acts like the “house” in a casino. When a trader opens a long position on ETH, they are capturing ETH’s upside from the GLP pool. When a trader opens a short position on ETH, they are capturing the upside of other assets relative to ETH from the GLP pool.

If the trader wins, profits are paid from the GLP pool in the form of the longed or shorted token. If the trader loses, losses are deducted from collateral and paid into the GLP pool.

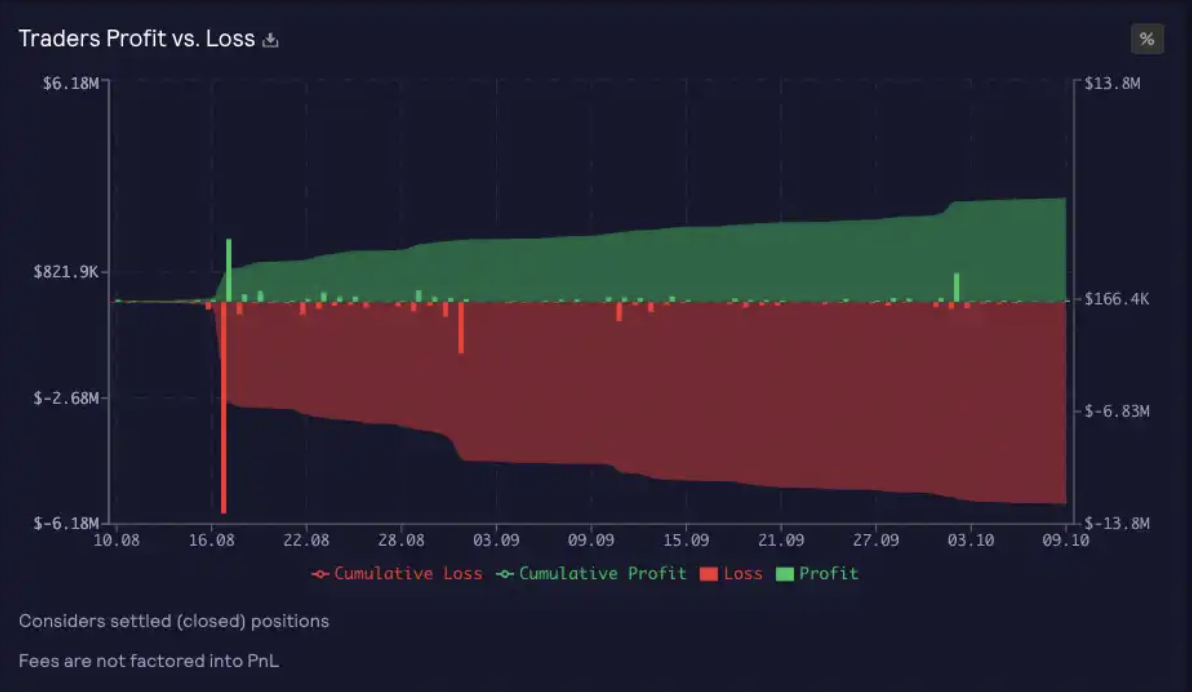

Although there is a risk that liquidity providers may lose principal when traders profit, historical data shows that most LPs actually profit from hedging against traders. For instance, in the example below, it’s noteworthy that most traders on GMX v1 lost money to LPs.

Synthetix’s Revolutionary Role

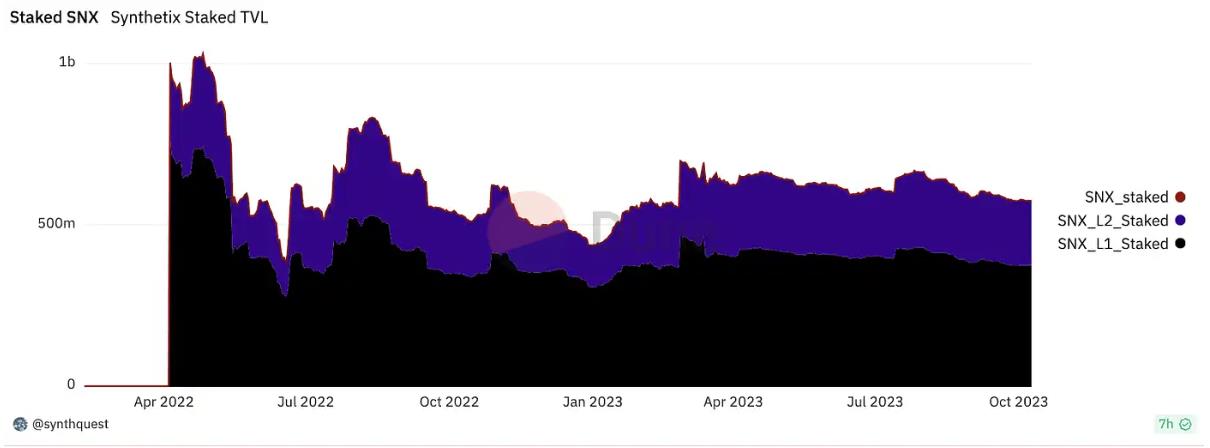

Synthetix, as a decentralized liquidity layer built on Ethereum and Optimism, has been at the forefront of this transformation. Synthetix derivatives, facilitated through platforms like Kwenta on Optimism, rely on liquidity provided by the Synthetix debt pool. The Synthetix debt pool plays a critical role in enabling synthetic asset and perpetual futures trading. Leveraging the Synthetix liquidity pool along with Chainlink and Pyth oracles, the need for traditional order books and counterparties is eliminated. This approach allows Synthetix liquidity to be pooled and transferred across markets, effectively solving slippage issues.

Moreover, Synthetix’s native token $SNX plays a vital role as collateral in the Synthetix debt pool. Currently, about 93% of $SNX is staked, with a total collateral value of approximately $573 million and a fully diluted valuation of $617 million (as of October 10, 2023).

Differentiating Liquidity Pools from vAMMs

In this context, understanding the core differences between the liquidity pool model and vAMMs is crucial. While both approaches eliminate traditional intermediaries like market makers and centralized exchanges, their mechanisms differ significantly.

In vAMMs, the pool merely replicates AMM liquidity depth. Perp v2 is built on Uni v3, where perp pools are essentially Uni v3 pools composed of virtual tokens minted by the clearinghouse. In contrast, the liquidity pool model does not replicate liquidity like Perp v2 or GMX—traders directly trade against pool liquidity.

Additionally, in vAMMs, funding rates play a crucial role. They incentivize arbitrageurs to minimize deviations between market and index prices. In contrast, for liquidity pool models, oracle prices play a more important role than funding rates. Notably, GMX v1 did not rely on funding rates to maintain consistency with spot market prices—a situation that persisted until the launch of GMX v2.

Finally, in terms of risk management, vAMMs typically use an insurance fund as a safety net. This fund absorbs traders’ PnL. Conversely, in liquidity pool models, liquidity providers (LPs) must fully bear traders’ PnL.

The rise of the liquidity pool model in perpetual contract trading reflects a transformative shift in the DeFi landscape. This innovative approach promotes direct and decentralized interaction between traders and liquidity providers, while offering profit opportunities for the latter. Pioneering protocols like Synthetix and GMX are paving the way for a more efficient and inclusive trading ecosystem. As DeFi continues to evolve, ongoing exploration of innovative trading models promises greater diversity and efficiency for the entire space, meeting the needs of a broader range of users and investors.

Beyond Decentralization: Insights into the Future of Perpetual DEXs

In the ever-evolving landscape of perpetual DEXs, this article delves into their evolutionary journey and explores case studies of several well-known models. Ideally, choosing between a perpetual CEX or DEX should be a simple binary decision between centralization and decentralization. However, reality is far more complex.

While perpetual trading is undoubtedly well-suited for the crypto trading domain, the challenges faced by perpetual DEXs go far beyond improving speed, volume, and trading fees. Transitioning from CEX to DEX is multifaceted, and many complex factors must be addressed before users can confidently migrate to perpetual DEXs.

Key Components of Building a Perpetual Trading Platform

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News