In-Depth Analysis of the 2023 Global DeFi Lending Sector: New Opportunities in Financial Technology Development

TechFlow Selected TechFlow Selected

In-Depth Analysis of the 2023 Global DeFi Lending Sector: New Opportunities in Financial Technology Development

This report aims to deeply explore the development trends, key challenges, and future outlook of the Web3 lending sector.

Author: Go2Mars, HKUST Crypto-Fintech Lab

Dear readers,

It is my great honor to introduce to you this Global Decentralized Finance Lending Sector 2023 – Insight Analysis Report. As the director of the Hong Kong University of Science and Technology Digital Finance Lab (HKUST Crypto-Fintech Lab), I have been dedicated to advancing the development of crypto-financial technology and exploring innovative possibilities in this field. This report is a carefully crafted product of shared wisdom and insights, jointly developed by our team and Go2Mars Capital through combining academic research with practical industry experience.

In recent years, the rise of Web3 technology has triggered profound transformations in the financial industry. With decentralization, security, transparency, and programmability as its core characteristics, Web3 has brought unprecedented opportunities and challenges to the lending sector. Leveraging technologies such as blockchain, smart contracts, and cryptocurrencies, financial markets are experimenting with a shift from traditional centralized models toward decentralized paradigms.

This report aims to deeply explore the development trends, key challenges, and future outlook of the Web3 lending space. Researchers from Go2Mars Capital and our lab team have conducted extensive research and analysis in this domain, engaging in in-depth discussions with industry experts and practitioners. We provide a comprehensive overview of critical topics including Web3 lending protocols, decentralized lending markets, asset collateralization, and risk management. Additionally, this report highlights some of the latest innovation cases in lending—Prestare Finance being one such project originating from our lab’s innovation initiative, exploring how Web3 technology can advance and innovate financial markets. We will examine emerging areas such as blockchain-based lending protocols, decentralized lending platforms, and lending derivatives, and discuss their potential impact on traditional financial systems.

We hope that this report provides readers with a holistic perspective on the Web3 lending landscape and serves as a valuable reference for industry practitioners, academic researchers, and policymakers. We believe that with the advancement of Web3 technology, lending markets will become more open, efficient, and inclusive, contributing to the sustainable development of the global financial system.

Finally, I would like to extend my heartfelt thanks to our lab members and partners at Go2Mars Capital for their hard work and support, as well as to our readers for your attention and encouragement. We hope this white paper brings you inspiration and guidance.

May our joint efforts propel better development in the world of finance and pave the way for the future of fintech.

Together, let us strive forward!

Kani CHEN

HKUST, Department of Mathematics (Director)

Fellow of Institute of Mathematical Statistics

Director of HKUST Crypto-Fintech Lab

Preface

Lending is where everything in financial markets begins—it is the origin.

Whether reading Adam Smith's The Wealth of Nations or Mankiw’s economics textbook, we easily understand that the core of financial activities lies in trust among people. Trust enables individuals to lend funds or assets to each other, thus achieving optimal resource allocation.

Lending is a credit activity in which lenders (banks or other financial institutions) lend monetary funds to borrowers (enterprises, individuals, or other organizations) at a certain interest rate and under specific conditions to meet their production or consumption needs. In lending, borrowers can amplify their capital scale to increase returns—this is the effect of leverage. However, leverage also magnifies risks. If borrowers fail to repay on time, it may result in losses or even bankruptcy. To mitigate or transfer such risks, people have invented various financial derivatives such as futures, options, and swaps, which can be used to hedge against or speculate on market fluctuations. It is no exaggeration to say that finance and financial derivatives are all built upon the foundational proposition of “lending.”

Due to the limitations of centralized finance, people have turned to blockchain, hoping to achieve more efficient, fairer, and secure financial services through decentralization. Decentralized lending is one of the most important application scenarios, using smart contracts to match lenders and borrowers, lock assets, calculate interest, and execute repayment—all without relying on any third-party institution or individual.

To date, on-chain DeFi lending has become one of the most significant sectors in the blockchain market, with TVL reaching $14.79 billion. However, innovation in current DeFi lending protocols remains insufficient, and market focus is gradually shifting. The challenge now facing innovators is how to build upon existing models while integrating the latest technologies.

The DeFi lending sector needs a new narrative.

Part 1: DeFi Lending Mechanism Breakdown — How Decentralization Transforms Financial Lending

Distributed Transformation of Financial Infrastructure: From Traditional Finance to "Decentralized Finance"

"Lending promotes the flow and accumulation of capital. Capitalists can lend idle capital to those in need of funding, thereby promoting economic development and capital accumulation."

—Adam Smith, The Wealth of Nations

A core function of the financial sector is directing savings toward productive investment opportunities. Traditionally, uninformed savers deposit money into banks to earn interest; banks then lend these funds to borrowers, including businesses and households. Crucially, as lenders, banks screen borrowers to assess their creditworthiness, ensuring scarce capital is allocated to its best use.

In the screening process, banks combine hard information—such as a borrower’s credit score, income, or education—with soft information, typically obtained through extensive relationships with the borrower. Viewed this way, the history of financial intermediation is essentially an exploration of improving information processing. For borrowers who are difficult to screen, lenders may require collateral to secure loans, mitigating information asymmetry and aligning incentives. For example, entrepreneurs often have to pledge their home equity when applying for loans. In case of default, the lender can seize and sell the collateral to recover losses.

For centuries, collateral has played a universal role in lending—secured loans backed by real estate already existed in ancient Rome. Over time, market vehicles and forms have evolved. DeFi lending platforms now bring together depositors and potential borrowers without central intermediaries like banks. More precisely, lending occurs on platforms—or rather, on a series of smart contracts governed by predefined rules. On one side are individual depositors (also known as lenders), who contribute their crypto assets to so-called liquidity pools and earn deposit interest. On the other side are borrowers, who obtain crypto assets and pay borrowing interest. These two interest rates fluctuate based on demand for the assets and the size of the liquidity pool (representing supply). Platforms typically charge borrowers service fees. Because the process is automated, loan disbursement is nearly instantaneous and associated costs are low.

A key difference between DeFi and traditional lending is DeFi’s limited ability to screen borrowers. Borrower and lender identities are hidden behind cryptographic signatures. Lenders therefore cannot access information such as credit scores or income statements. As a result, DeFi platforms rely on collateral to align borrower and lender incentives. Only assets recorded on the blockchain can be borrowed or pledged, making the system largely self-referential.

Typical DeFi loans are issued in stablecoins, while collateral consists of higher-risk unsecured crypto assets. Smart contracts assign a haircut or margin requirement to each type of collateral, determining the minimum amount borrowers must pledge to receive a given loan. Due to the high price volatility of crypto assets, over-collateralization results—where required collateral far exceeds the loan amount. Minimum collateral ratios on major lending platforms usually range between 120% and 150%, depending on expected price appreciation and volatility.

-

Exploration Phase (2017–2018): This marked the early stage of the DeFi ecosystem, during which a wave of decentralized financial protocols based on smart contracts emerged on the Ethereum platform, offering users various types of crypto-asset lending services. MakerDAO was the earliest stablecoin issuance protocol, allowing users to generate the DAI stablecoin by pledging crypto assets. Compound was the first interest-rate market protocol, enabling users to deposit or borrow crypto assets with dynamically adjusted interest rates based on market supply and demand. Dharma was the earliest bond issuance protocol, enabling users to create, buy, or sell fixed-rate bonds backed by crypto assets. These protocols laid the foundation for the DeFi ecosystem and provided inspiration and reference for future innovators.

-

Explosion Phase (2019–2020): This period saw rapid growth in the DeFi ecosystem, characterized by diversification and innovation in on-chain lending markets. Not only did more DeFi projects enter the competitive landscape, but many lending protocols also introduced innovations and optimizations to meet diverse user needs and market conditions. These protocols involved various crypto assets—including stablecoins, native tokens, synthetic assets, and NFTs—and adopted different risk management approaches such as collateral ratios, liquidation penalties, insurance pools, and credit scoring. They also designed varied interest rate models—fixed, floating, algorithmic, and derivative rates—and implemented different governance mechanisms, including centralized, decentralized, community-based governance, and token incentives. These protocols achieved higher levels of interoperability and synergy, leveraging smart contracts and composability strategies to offer users richer and more flexible financial services and yield opportunities. Notable lending protocols that rose or evolved during this phase include Aave, dYdX, Euler, and Fraxlend, each with distinct strengths and facing unique challenges and risks.

-

Expansion Phase (2021–present): The on-chain lending sector now faces greater challenges and opportunities. On one hand, due to Ethereum network congestion and rising transaction fees, lending protocols are seeking cross-chain and multi-chain solutions to improve efficiency and reduce costs. Some protocols have deployed on alternative public chains or adopted cross-chain bridging tools to enable asset and data interoperability—examples include the omnichain lending protocol Radiant. On the other hand, with growing demand and attention from the real economy and traditional finance, lending protocols are beginning to explore the possibility of bringing real-world assets (RWA) on-chain to expand the scale and influence of lending markets. Some protocols have started converting assets such as real estate, automobiles, and bills into on-chain tokens and providing corresponding lending services. Representative protocols include Tinlake, Centrifuge, and Credix Finance.

Core Elements of Decentralized Lending

Whether blockchain-based decentralized lending or institution-based traditional lending, both share certain similarities in core components. Regardless of the lending method, borrowers, lenders, interest rates, terms, and collateral are essential elements. These components form the basic logic and rules of lending and determine its associated risks and returns. In decentralized lending, various parameters are determined by DAOs, adding a governance module to the overall financial model. Specifically, these include:

-

Borrower: The party needing to borrow funds, typically having funding needs such as investment, consumption, or emergency expenses. Borrowers must submit a loan request to the lender or platform, providing necessary information and conditions such as loan amount, term, interest rate, and collateral. After receiving the loan, they must repay principal and interest according to agreed methods and timelines.

-

Lender: The party willing to lend funds, typically possessing idle capital seeking returns. Lenders must provide their funds to borrowers or platforms, accepting relevant information and conditions such as loan amount, term, interest rate, and risk. After lending, they must recover principal and interest according to agreed methods and timelines.

-

Platform: The intermediary or coordinator in the lending process, which could be a centralized entity such as a bank, credit union, or P2P lending platform, or a decentralized system such as a blockchain, smart contract, or DeFi platform. The platform’s primary function is to provide a trustworthy and efficient lending market, facilitating fund matching and circulation. Platforms typically charge fees or earn profits as compensation for their services.

-

Governor: In decentralized protocols, metrics such as interest rates, eligible collateral, and LTV are determined via voting with governance tokens. Thus, governors play a crucial role in protocol decision-making. Governors typically need to hold or stake a certain amount of governance tokens to gain voting rights and governance rewards. They can influence the protocol’s direction and parameter settings by proposing or supporting proposals.

Breakdown and Analysis of the Lending Process

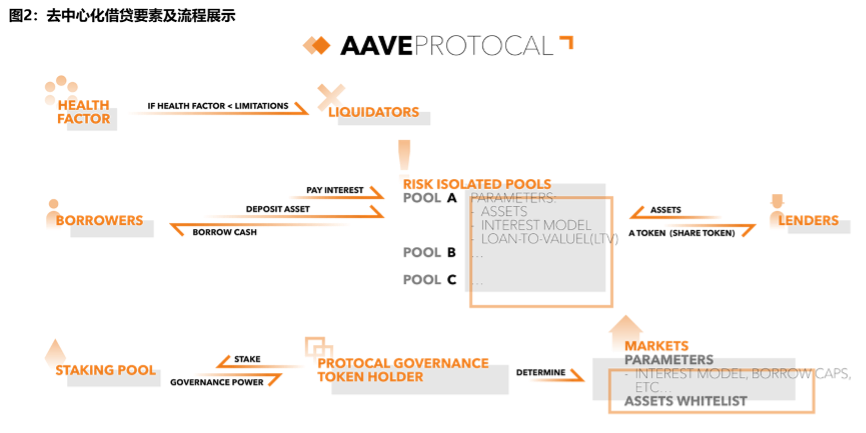

The decentralized lending process shares similar steps with centralized lending, including initiation and processing of loan requests, provision and management of collateral, and loan repayment and liquidation. Below we describe each step. The hallmark of decentralized lending is not requiring trust in any intermediary, instead relying on smart contracts to automatically execute lending agreements. The decentralized lending process works as follows (see Figure 2):

On decentralized platforms, there are generally multiple collateral pools corresponding to assets of different risk levels, each with varying parameters such as interest rates, collateral ratios, and liquidation thresholds. Borrowers first select a collateral pool based on their pledged assets, then deposit their collateral into the pool’s smart contract, after which they receive the borrowed assets. Currently, on-chain identity verification makes credit assessment difficult, so decentralized lending typically employs over-collateralization—i.e., the value of collateral / loan amount > 100%.

After selecting a collateral pool, borrowers input the desired type and amount of asset to borrow. The platform displays corresponding information such as loan term, interest rate, and collateral ratio based on current market conditions and pool parameters for the borrower’s reference. Generally, platforms offer a range of cryptocurrencies as collateral—e.g., Bitcoin, Ethereum, stablecoins. Different cryptocurrencies carry different risk profiles and thus have different parameter settings. Borrowers can choose more stable or more volatile cryptocurrencies as collateral based on their risk preferences and return expectations.

Once borrowers finalize their loan terms, they initiate the request. The platform verifies the borrower’s identity and address, and checks whether the provided collateral meets requirements. If everything is in order, the platform transfers the borrower’s collateral into the smart contract and disburses the corresponding amount of borrowed assets. Simultaneously, the platform records borrower-related information—loan amount, term, interest rate, collateral ratio—and generates a unique loan ID within the contract.

The platform matches suitable lenders from the collateral pool according to the borrower’s request and transfers their funds to the borrower. Lenders can be individual users or institutions, or collective pools. While providing funds, lenders earn interest income and token rewards.

Lenders can increase or decrease their provided funds at any time to adjust their returns and risks. The platform dynamically adjusts interest rates based on market supply and demand to balance interests between lenders and borrowers. During the loan term, borrowers can repay part or all of the principal and interest at any time and withdraw the corresponding amount of collateral from the smart contract. If the borrower fully repays on time, the platform terminates the loan agreement and deletes related records.

Meanwhile, the platform continuously monitors the value of collateral and calculates each loan’s collateral ratio, liquidation threshold, and health factor. The collateral ratio refers to the proportion of collateral value to loan amount. The liquidation threshold is the minimum collateral ratio triggering liquidation. The health factor is the ratio of collateral ratio to liquidation threshold, reflecting the borrower’s repayment capacity and risk level. The platform communicates this information to borrowers through various means and alerts them to potential risks.

If a borrower fails to repay on time or their collateral ratio falls below the liquidation threshold (e.g., 150%), the platform automatically triggers liquidation, selling the collateral at a discount to liquidators to repay the debt and charging a penalty fee.

Liquidators can be the platform itself or third-party entities, who profit by purchasing discounted collateral. After liquidation, if residual collateral value remains, the platform returns it to the borrower; if the collateral value is insufficient to cover the debt, the platform writes it down to zero and absorbs the loss.

Game of Interest Distribution in Lending

For lending protocols, revenue comes from three sources: borrower interest payments, collateral liquidations, and service fees. These revenues are distributed among the protocol itself, LPs (liquidity providers), and secondary market makers. This distribution process can be viewed as a game-theoretic optimization problem.

To achieve higher TVL, project teams may initially sacrifice margins—implementing measures to attract LPs and borrowers. For instance, they might set higher interest rates to incentivize LPs to deposit assets into liquidity pools, while also offering borrower-friendly features such as subsidies to lower borrowing costs. Later, project teams focus more on stabilizing token prices. To achieve this, they may conduct market-making activities in secondary markets to support their token prices—by buying or selling tokens. Additionally, they may adjust interest rates and subsidy policies to balance supply and demand and maintain market stability.

In short, throughout this process, the protocol must balance the interests of all parties. It needs to attract sufficient LPs to provide liquidity while offering borrowers competitive interest rates and convenient borrowing conditions. Moreover, it must support its token price through secondary market making and sustain operations via service fees. Therefore, the protocol must continuously adjust the distribution ratios among stakeholders to achieve optimal outcomes.

DeFi Lending Model Breakdown: How Decentralized Systems Influence Lending Mechanisms

DeFi Lending Mechanism 1: Peer-to-Peer vs. Peer-to-Pool Lending Models

Based on how lending parties are matched, lending models can be categorized into peer-to-peer (P2P) and peer-to-pool (P2Pool). Matching refers to how borrowers and lenders find each other and reach lending agreements. P2P lending involves direct transactions between borrowers and lenders, who can freely negotiate terms but must spend time and cost finding suitable counterparties. P2Pool lending involves both parties transacting through a shared liquidity pool, eliminating the need to know each other’s identity and requiring only adherence to pool rules. This improves efficiency and liquidity but introduces certain risks and constraints.

The P2Pool model is currently dominant—protocols like Aave and Compound follow this approach. It aggregates different assets from liquidity providers into respective liquidity pools. Borrowers pledge tokens to draw assets from the target asset’s liquidity pool. The interest paid by borrowers becomes the liquidity pool’s income, distributed among all liquidity providers in the borrowed asset pool—not allocated to specific providers—hence termed “peer-to-pool” lending.

The P2Pool model offers several advantages. First, it effectively diversifies risk, as bad debt risk is borne collectively by all liquidity providers, reducing individual exposure. Second, it ensures liquidity—since providers pool assets into dedicated pools, borrowers can promptly access needed funds.

However, P2Pool lending also has drawbacks. First, each provider receives diluted returns, since interest is spread across all providers in the pool. Second, capital utilization for liquidity providers is low, as much of the capital remains idle.

The peer-to-peer (P2P) on-chain lending model was originally proposed by ETHLend, attempting to use an orderbook mechanism to achieve 100% capital utilization efficiency. Under P2P lending, both parties negotiate price and interest directly. Protocols like Morpho operate under this model. This approach allows borrowers to capture full interest earnings, achieving 100% capital utilization efficiency.

However, P2P on-chain lending also has disadvantages. First, executing transactions on-chain is challenging—since all prices and trades must be recorded on-chain, both parties incur higher gas fees, resulting in poor user experience. Second, borrowers bear full risk—the risk of under-collateralization or default due to market volatility falls entirely on the borrower.

DeFi Lending Mechanism 2: Over-Collateralized vs. Under-Collateralized Lending Models

Based on the degree of credit enhancement between lending parties, lending can be divided into two models. One is over-collateralized lending, where borrowers must provide collateral exceeding the loan value, ensuring lenders can recover principal and interest by selling collateral in case of market volatility or default. This model suits borrowers with lower credit or higher risk, as they must pay higher costs to access funds.

The other is under-collateralized lending, where borrowers provide collateral worth less than the loan amount, leveraging potential asset appreciation for higher returns. This model suits borrowers with higher credit or lower risk, enabling amplified returns with reduced upfront cost. However, it carries greater risk—as market reversals or defaults occur, lenders may not fully recover losses through collateral sales.

-

Over-collateralization requires collateral value to exceed loan amount—for example, Aave may require $10,000 in collateral to borrow $6,400 in DAI. Given the high price volatility of most assets in DeFi markets, over-collateralized protocols predefine a liquidation threshold. When a user’s LTV (loan-to-value ratio) exceeds this threshold, the protocol introduces external liquidators to liquidate the position, reducing LTV back to a safe range. Various incentives encourage liquidators to act, ensuring pool safety. However, over-collateralization leads to lower capital efficiency. Most on-chain assets are liquid, and the low capital utilization of over-collateralization fails to adequately meet user demands, limiting financial tool effectiveness.

-

Under-collateralized lending: In traditional finance, credit is a key tool, allowing borrowers to spend in advance and stimulate economic activity. However, due to blockchain’s censorship resistance and anonymity, defaulting parties cannot be individually held accountable, and DeFi protocols cannot assess address reputations. Hence, to ensure fund and protocol safety, lending protocols primarily adopt over-collateralization. Nevertheless, some DeFi protocols are now attempting hybrid on-chain/off-chain approaches to offer under-collateralized loans to whitelisted users. One off-chain integration method involves KYC—protocol operators or token holders review and evaluate borrowers’ backgrounds and finances. Upon approval, a loan agreement (specifying amount, term, interest rate, and collateral ratio) is formed, ultimately decided via proposal or voting. Protocols like Maple and TrueFi define borrowers as established crypto institutions or funds.

DeFi Lending Mechanism 3: Floating-Rate vs. Fixed-Rate Lending Models

-

Floating-rate model: Aave’s predecessor Ethlend demonstrated a P2P lending model based on orderbooks, featuring fixed interest rates and maturity dates. However, due to insufficient liquidity and poor fund matching, it was eventually phased out of the DeFi market. Aave pioneered the P2Pool model, where interest rates are controlled by supply and demand. Under this model, loans have no fixed maturity date. To maintain market balance, interest rates are adjusted based on utilization. When utilization rises (demand > supply), rates increase to suppress demand and protect the pool. When utilization falls (supply > demand), rates decrease to stimulate demand. Representative protocols include Aave and Compound, which adjust rates in real time to reflect market changes. This model has pros and cons: it responds quickly to market shifts and maintains pool safety, but floating rates expose users to greater risk, making long-term financial planning difficult. Investors must closely monitor market dynamics and adjust strategies accordingly, while managing risks to avoid over-investment or excessive leverage.

-

Fixed-rate model: In traditional finance, fixed-rate lending is more common, as predictable rates support stronger investment portfolios. However, establishing proper pricing and setting appropriate fixed rates in DeFi is highly challenging. Current DeFi protocols use different methods to establish fixed rates, commonly involving zero-coupon bonds and interest rate markets.

Zero-coupon bonds pay no interest and trade at a discount to face value, redeeming at par upon maturity. Lenders buy these bonds at a discount and receive the face value at maturity. The difference represents interest earned, and the fixed rate equals this interest divided by the holding period. Borrowers can pledge assets to borrow zero-coupon bonds, sell them at a discount for funds, and later redeem collateral by repaying the bond’s face value. The difference between the borrowed bond’s face value and proceeds from sale constitutes the borrowing interest. Based on supply and demand, lenders and borrowers can transact zero-coupon bonds at fixed rates.

A representative fixed-rate lending protocol is Yield Protocol. Yield Protocol is a permissionless market for secured fixed-rate lending on Ethereum. It introduces a derivative model for secured zero-coupon bonds, enabling fixed-rate borrowing. This allows borrowers to lock in fixed rates, protecting against rate volatility.

The protocol defines yToken as an ERC-20 token that settles in a fixed amount of target asset on a specified date. This enables a market for these tokens, where buyers and sellers trade at prices reflecting market expectations for future rates. These tokens are backed by collateral and require maintenance of collateral ratios similar to other DeFi platforms. If collateral value drops below required levels, custodians can partially or fully liquidate positions to repay debts. This provides lenders additional assurance, knowing their funds are collateral-backed.

Beyond zero-coupon bonds, investors can access fixed-rate yield products through other avenues. One method is deriving secondary markets for trading interest rates from existing sources such as floating rates or liquidity mining. In these secondary markets, investors can buy and trade various fixed-rate products for stable returns. Protocols can also generate fixed-rate yield products through other mechanisms, offering investors more choices. Typically, these fall into two categories:

-

Principal-Interest Separation: Tokenizes expected interest returns from DeFi investments, splitting the investment amount into principal and interest portions, priced and sold separately as tokens. At maturity, principal holders receive the initial investment, while interest holders receive all accrued interest. For example, depositing 10,000 DAI into Compound with a 4% expected rate, the principal might be priced at 9,600 and interest at 400. Upon sale and maturity, holders of principal tokens receive 10,000 DAI, while interest token holders get the remaining interest. This product includes a fixed-rate component and a bullish view on Compound’s interest market. Pendle is a representative protocol. Pendle is a yield-trading protocol enabling users to purchase assets at a discount or gain leveraged yield exposure without liquidation risk. It achieves this by deploying fixed-rate derivative protocols on Ethereum and Arbitrum. By separating principal and interest of yield-generating assets into tokens, it enhances investment flexibility and control. Users deposit yield-bearing assets, and smart contracts mint principal and yield tokens, tradable via AMM algorithms on the platform, enabling efficient, transparent trading and more investment management options.

-

Structured Products: Leveraging uncertainty in floating rates and differing investor risk tolerances and opportunity costs, protocols can design structured products to redistribute risk according to individual needs. This allows investors to select suitable structured products based on their risk tolerance and investment goals, helping manage risk and maximize returns in uncertain markets. In structured products, Class A offers lower risk with priority yield distribution (fixed-rate portion), while Class B offers higher risk and higher returns. Again using a 10,000 DAI deposit into Compound: Class A investors earn a stable 4% return, while Class B takes excess returns. If rates fall below 4%, Class B must cover the shortfall to Class A.

DeFi Lending Mechanism 4: Auction Liquidation vs. Partial Repayment Liquidation Models

In DeFi lending, liquidation involves the account’s health factor (also known as health index), which relates to the value of collateral and loan amount. If the health factor reaches a critical threshold (≤1), the loan is under-collateralized and subject to liquidation, causing the user to lose all collateral:

Due to market volatility, the health factor can behave in two ways: when collateral value increases, the health factor increases accordingly, staying above the critical value of 1. When collateral value decreases, the health factor declines similarly, increasing loan risk as it approaches the critical value of 1. If it falls below the threshold, the loan becomes under-collateralized and subject to liquidation. Users can increase their health factor by depositing additional collateral, keeping their loan position safer—both to avoid forced liquidation and to allow further borrowing.

During lending, if a borrower’s health factor drops below 1, they face liquidation. The liquidation process can follow either partial repayment or auction liquidation models. Partial repayment liquidation involves directly listing part of the borrower’s collateral at a discount through the contract, allowing any user to repay the borrower’s debt and immediately resell for arbitrage. This quickly resolves the borrower’s loan issue while offering others arbitrage opportunities. Auction liquidation starts at a base price and publicly auctions the collateral with incrementally increasing bids. This maximizes collateral value and gives borrowers more time to resolve the loan issue.

When choosing a liquidation model, actual circumstances should guide the decision. If borrowers want a quick resolution and accept some asset loss, partial repayment liquidation is preferable. If borrowers aim to preserve assets and are willing to spend more time resolving the issue, auction liquidation is more suitable.

Comparison of Advantages and Disadvantages Across Four DeFi Lending Models

-

P2P vs. P2Pool Models: In terms of security, current P2P lending protocols like Morpho Finance rely on underlying yield-bearing tokens from Compound and Aave. Thus, beyond their own protocol risks, their security also depends on the underlying protocols. However, in efficiency and flexibility, Morpho optimizes traditional P2Pool interest rate models, offering better rates for both lenders and borrowers—undoubtedly improving capital efficiency.

-

Fully Collateralized vs. Under-Collateralized Models: In transparency and security, fully collateralized protocols perform better and withstand market tests more robustly. Most under-collateralized protocols rely on an additional assumption—that a centralized entity or organization is trusted. While attractive during bull markets, under-collateralized or zero-collateral loans to institutions inevitably risk bad debts in bear markets. In terms of lender returns, under-collateralized models may offer higher yields, but due to protocol limitations, they may not support looping loans, restricting usage flexibility.

-

Floating-Rate vs. Fixed-Rate Models: Generally, floating rates are more flexible, changing with pool utilization to better capture market movements. Floating-rate protocols like Aave have simpler product logic, larger TVL, and relatively stronger security assurances. Fixed-rate products are more complex, influenced by more factors, and harder to calculate accurately. At the protocol level, numerous protocols offer fixed-income products, resulting in highly fragmented TVL and uncertain security. Overall, fixed-rate products present a barrier to entry for average DeFi users.

-

Auction Liquidation vs. Partial Repayment Liquidation: Both models have pros and cons in practice. Partial repayment liquidation quickly resolves borrower issues but causes borrowers to lose some asset value due to discounted sales. Auction liquidation maximizes collateral value but may take longer, hindering swift resolution. Therefore, the choice of liquidation model should depend on actual circumstances.

Collateral Ratio Design: Different lending protocols such as MakerDAO, Aave, and Compound set different collateral ratios for different assets. For example, mainstream assets like ETH and WBTC, with high consensus, good liquidity, and relatively low volatility, have lower collateral ratios (or higher loan-to-value ratios), while non-mainstream coins have higher ratios. MakerDAO even offers different collateral ratios for the same asset to encourage higher collateralization and reduce liquidation risk.

Multi-Layer Liquidation Safeguards: To handle extreme market conditions, some leading lending protocols implement multi-tier defense mechanisms. For example, MakerDAO establishes a Maker Buffer Pool, debt auction mode, and emergency shutdown mechanism; Aave designs a safety module, attracting funds into it as insurance capital via protocol revenue sharing. Auction mechanisms are also continuously improved.

Oracle Price Accuracy: The entire liquidation process heavily relies on oracle price feeds, making price accuracy critical. Currently, MakerDAO uses its own oracle system for enhanced security, while Aave relies on top oracle Chainlink.

Liquidator Participation: Active participation by liquidators is essential for effective liquidation. Major protocols incentivize liquidators through reward mechanisms to boost engagement.

Summary: Challenges and Issues in On-Chain Lending

On-chain lending offers users fast, convenient, and low-cost lending services through decentralization. Since its inception, decentralized lending has attracted substantial capital and users, forming a vast and active market that supports crypto asset circulation and investment. However, decentralized lending also faces common and unique challenges:

-

Liquidity: On-chain lending platforms rely on user deposits or borrows of crypto assets to form liquidity pools and provide lending services. Liquidity volume determines whether platforms can meet user demands and influences interest rate levels. Insufficient liquidity reduces user acquisition and retention, weakening competitiveness and revenue. Excessive liquidity depresses interest rates, reducing user incentives. Therefore, on-chain lending platforms must design rational mechanisms to balance liquidity supply and demand—such as dynamic interest rate adjustments, liquidity mining rewards, and cross-chain interoperability.

-

Security: On-chain lending platforms are governed by smart contracts, exposing them to risks of coding errors, logical vulnerabilities, or malicious attacks. Security incidents may lead to user funds being stolen, frozen, or destroyed, causing massive losses. Therefore, platforms must conduct rigorous code audits, security testing, and risk management, and establish emergency response mechanisms and governance models to safeguard user funds.

-

Scalability: On-chain lending platforms are constrained by their underlying blockchain’s performance and capacity—transaction speed, throughput, and fees. When networks are congested or fees are high, user experience and efficiency suffer. Therefore, platforms must seek more efficient and cost-effective blockchain solutions—such as layer-2 scaling, sidechains, and cross-chain bridges.

-

Compliance: Due to their decentralized and anonymous nature, on-chain lending platforms may face legal and regulatory challenges—anti-money laundering, counter-terrorism financing, consumer protection, tax compliance. These issues may affect platform legality and sustainability, undermining user trust and confidence. Therefore, platforms must communicate and coordinate with regulators and stakeholders, comply with applicable laws, and fulfill social responsibilities.

Part 2: Exploring the DeFi Lending Sector—How Decentralized Platforms Deepen Integration with Financial Lending

NFT Collateral Lending Model: Playing NFTs with Decentralized Finance

NFT, or Non-Fungible Token, typically refers to tokens conforming to the ERC-721 standard. Since its introduction, NFTs have become an indispensable asset class in the blockchain world. However, due to their non-fungibility and difficulty in valuation, NFTs suffer from low liquidity, resulting in high capital barriers and inefficient capital utilization.

Beyond being forced to sell at low prices during cash shortages or missing blue-chip projects due to small capital size, NFT holders also face liquidity losses due to valuation difficulties. To address these issues, the market has introduced the concept of NFTFi, aiming to enhance NFT liquidity, valuations, usability, and compatibility through financialization, creating a better experience for NFT players.

NFTFi lending and borrowing protocols unlock liquidity for borrowers and offer lenders novel yield opportunities. These protocols allow NFT holders to lock their digital assets as collateral, unlocking liquidity in another digital asset. Borrowers gain needed liquidity without selling prized NFTs, while lenders earn returns by providing liquidity.

Additionally, NFTFi offers other financial tools such as leasing, borrowing, and fractionalizing NFTs. These tools allow holders to lease their digital assets for use by others or split them into parts for sale or trade—enabling earnings without selling the NFT. NFT owners lock their NFTs with the protocol and borrow fungible digital assets over time by paying interest to lenders. If the owner defaults, the NFT serves as collateral.

NFT owners can repay the loan anytime to reclaim their NFT. Through this process, NFT lending protocols offer a way to unlock NFT liquidity without selling them.

How NFTFi Works

In 2020, the NFT market experienced explosive

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News