The Golden Age of Decentralized Stablecoins: Finding the Next Opportunity Amidst a Flourishing Landscape

TechFlow Selected TechFlow Selected

The Golden Age of Decentralized Stablecoins: Finding the Next Opportunity Amidst a Flourishing Landscape

We are entering the golden age of decentralized stablecoins, but which stablecoin is the safest?

Written by: IGNAS

Compiled by: TechFlow

Do you hold any stablecoins? If so, which ones, and what do you do with them? Are you farming for maximum yield, or simply holding them to buy the dip when markets fall?

Perhaps you've converted your stablecoins into fiat to avoid the associated risks. That’s understandable, especially after USDC briefly lost its peg. Or maybe you’ve chosen fiat because it now offers higher yields than lending on blue-chip DeFi protocols.

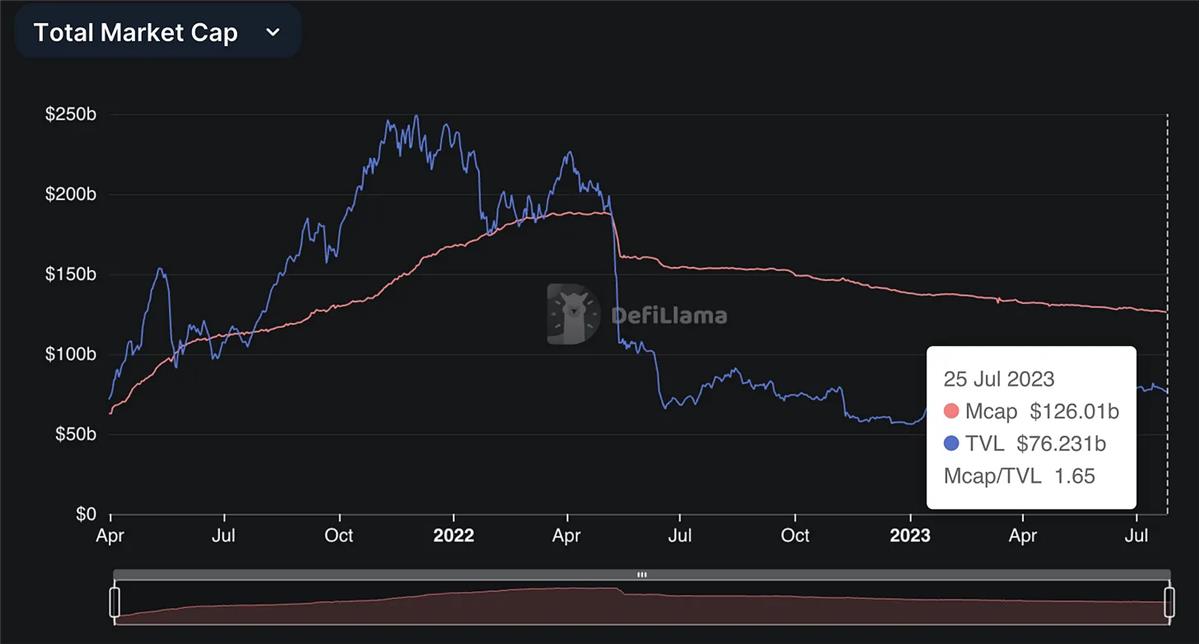

Combined with an overall bearish crypto market, the total market cap of stablecoins has dropped from a record high of $200 billion to the current $126 billion—unsurprising, but notable.

Don’t worry. The stablecoin market is becoming increasingly interesting. In fact, Synthetix’s founder says we’re entering a golden age of decentralized stablecoins.

But which stablecoin is the safest?

This is the most important question, because you don’t want to wake up one day and find your stablecoin has lost 50% of its value.

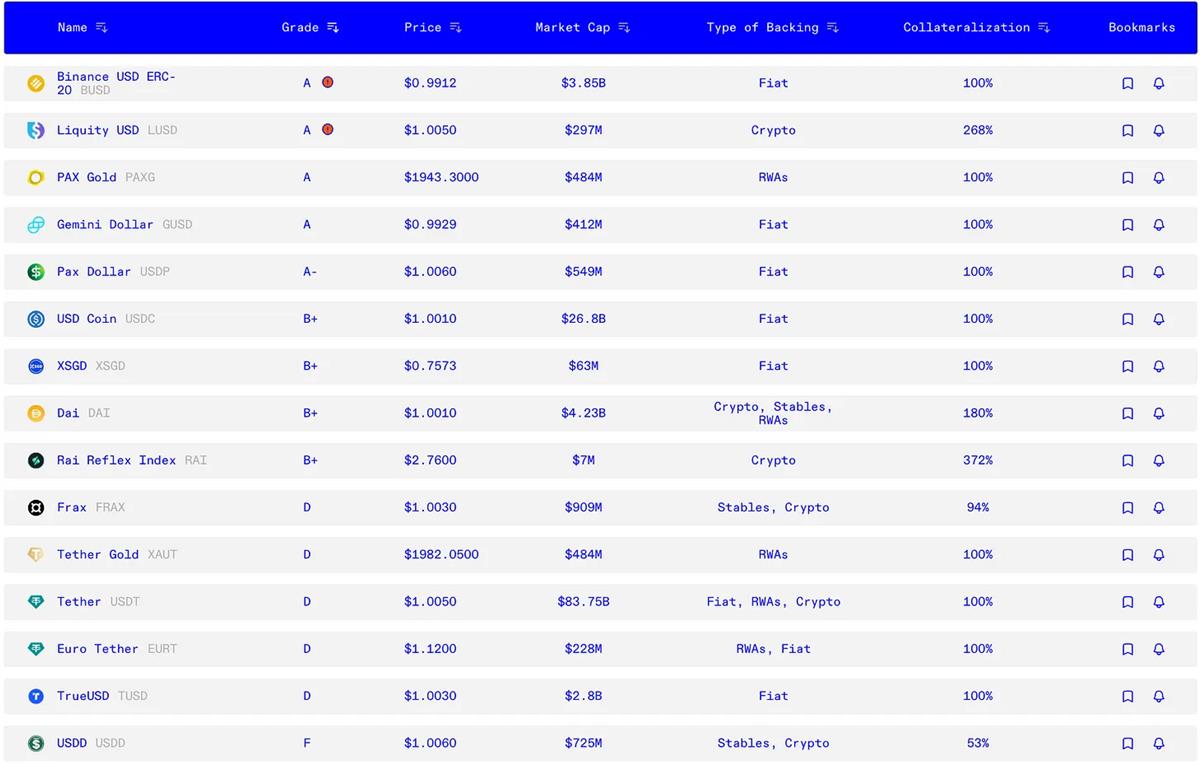

Fortunately, this week a nonprofit called Bluechip released an economic security rating for top stablecoins. The safety score considers stability (S), management (M), implementation (I), decentralization (D), governance (G), and external factors (E).

And the safest stablecoin is…

... BUSD, PAXG, GUSD, and Liquity's LUSD. This makes LUSD the most economically secure decentralized stablecoin, even safer than USDC.

Not surprising. During the severe March event when USDC lost its peg, LUSD acted as a safe haven.

Interestingly, other DeFi stablecoins vary across the spectrum—Dai and Rai earned B+ ratings, while USDD received an F.

Tron’s USDD received an F because its reserves include TRX (69%), BTC (29%), and TUSD (2%). However, Bluechip does not count TRX as collateral. The Terra/Luna collapse showed how quickly endogenous collateral can lose value.

If you're interested in these findings, here's a brief summary of the report on selected stablecoins:

BUSD ERC-20 (Rating: A): Issued by Paxos, considered safe for general public use. Although NYDFS halted issuance in 2023, BUSD’s backing remains unaffected.

LUSD (Rating: A): Part of the Liquity protocol, highly decentralized. Considered safe, ideal for users who prefer code over human control. Note smart contract and oracle risks, and avoid buying LUSD above $1.

USDC (Rating: B+): One of the safest stablecoins, backed by short-term U.S. Treasuries and cash deposits. Widely usable; could improve rating by proving bankruptcy remoteness of reserves and including redemption timelines in terms of service.

Dai (Rating: B+): The first on-chain stablecoin, primarily backed by centralized assets. Still considered safe, ideal for users seeking permissionless protocols.

Rai Reflex Index (Rating: B+): RAI is a floating-price decentralized stablecoin not pegged to any fiat currency. Despite being experimental, it has proven to be a reliable low-volatility alternative to traditional stablecoins. Backed by ETH collateral, ideal for advanced users wanting a decentralized, censorship-resistant stablecoin.

USDT (Rating: D): Despite being the earliest and largest stablecoin, USDT suffers from transparency issues and mixed reserves. Best suited for institutional users, high-net-worth individuals, and sophisticated traders with direct access to redemption mechanisms.

Frax (Rating: D): FRAX maintains a tight peg and performs well under market stress, but concerns remain due to partial collateralization and reliance on centralized assets. Ideal for yield farmers and liquidity providers comfortable with the protocol’s complexity.

USDD (Rating: F): Managed by Tron DAO Reserve, similar to the failed UST stablecoin. With only 50% of supply backed by non-TRX collateral (mainly Bitcoin), its use is strongly discouraged due to asset commingling concerns.

You might wonder: what does this safety rating have to do with the golden age of decentralized stablecoins?

It's relevant because upcoming developments will feature experimental DeFi stablecoins that could either become the next big thing—or completely collapse.

Given the importance of fund safety, let’s explore what makes the DeFi stablecoin space so exciting.

Lybra — Challenger to LUSD

Take a look at the top 10 stablecoins by market cap. What stands out to you?

First, surprisingly, USDT holds 66% of the market share despite being rated unsafe (“D”) by Bluechip. Second, only two stablecoins—USDT and LUSD—have seen market cap growth this month; all others have declined, some sharply.

However, outside the top 10, there's eUSD, issued by Lybra Finance.

Interestingly, Lybra is a fork of Liquity, differentiated by accepting stETH as collateral—whereas Liquity only accepts ETH. Thanks to stETH, eUSD holders earn around 7.2% APY.

eUSD’s yield exceeds stETH’s because eUSD requires 159% over-collateralization using stETH.

A potential risk is stETH depegging, since Lybra uses Liquity’s ETH:USD price feed.

Another issue with eUSD is that yields are distributed via rebase—meaning you get more eUSD tokens at an annualized rate. To address this and other issues, Lybra has launched v2 and introduced a new stablecoin—peUSD.

Key upgrades include:

-

Multi-chain functionality: peUSD is a cross-chain version of eUSD (via LayerZero), allowing holders to use their stablecoin across different blockchains.

-

Multiple collateral types: Users can now directly mint peUSD using non-rebasing LSTs like Rocket Pool’s rETH, Binance’s WBETH, or Swell’s swETH. Yield accrues through the underlying LST—even if peUSD is spent, the LST value grows.

-

Ongoing yield: When converting eUSD to peUSD, users continue earning interest on their underlying eUSD collateral even after spending peUSD.

-

Usable in DeFi activities: peUSD is not a rebasing token, making it more widely applicable across the crypto ecosystem.

Overall, eUSD poses the biggest threat to LUSD, alongside competitors like Raft (backed solely by stETH) and Gravita (multi-LST backed).

But Liquity also has some cards up its sleeve to fight back.

Liquity V2

The beauty of Liquity lies in its simplicity. You can mint LUSD at 0% interest using ETH as collateral, plus a one-time 0.5% borrowing fee.

Liquity originally emerged as an alternative to the governance-heavy Dai. LUSD has almost no governance and immutable (non-upgradable) smart contracts—great for economic security, though not necessarily for growth.

To stay competitive, Liquity will launch a v2 supporting LSTs. But unlike an upgrade, “V2” will be an entirely new and separate product.

Liquity v2 aims to solve the “stablecoin trilemma” (decentralization, stability, scalability) using a reserve-backed, risk-free hedging model with principal protection.

While complex, here's a simplified explanation:

Suppose Alice owns 1 ETH worth $2,000. She deposits it into Liquity v2 and receives 2,000 v2 LUSD. Liquity holds her ETH, and Alice holds 2,000 v2 LUSD. If ETH price drops below $2,000, Alice’s v2 LUSD becomes undercollateralized, risking a price spiral.

To prevent this, Liquity v2 introduces:

Principal-protected leverage: Users can take leveraged positions (bet on future prices) where they only risk the premium paid, not the principal amount. This should boost demand and support v2 LUSD.

Secondary market: Users can sell these principal-protected positions. If unsold, Liquity subsidizes them, ensuring all positions are bought and keeping subsidies within the system.

This creates multiple opportunities for DeFi users: principal-protected leverage, yield for miners, and trading in secondary markets.

v2 is expected to launch in 2024.

Synthetix’s sUSD

Wondering why Synthetix founder Kain is bullish on decentralized stablecoins?

Because Synthetix V3 is rolling out gradually. Synthetix is one of the more complex DeFi protocols, with sUSD—the SNX-backed stablecoin—at its core.

V3 addresses two key pain points for sUSD minter:

-

Multi-collateral staking: V3 is collateral-agnostic, allowing any asset to back synthetic assets. V2 only allowed SNX. This increases sUSD liquidity and expands the range of markets Synthetix can support.

-

Synthetix Loans: Users can now deposit collateral to generate sUSD without exposure to debt pool risk, and without paying interest or issuance fees.

If you've ever tried minting sUSD, you know how significant these changes are!

Now, sUSD has real potential to compete with established stablecoins like FRAX, LUSD, or DAI.

MakerDAO

Maker is now in its Endgame phase. One key point: if regulatory pressure arises, Dai may even abandon its dollar peg. For now, Maker seems to be in a frenzy:

-

MKR surged 66% in 30 days, with Maker founders actively buying MKR.

-

DAI now pays holders a 3.49% return thanks to the reactivated Dai Savings Rate.

-

Spark Protocol, an Aave fork focused on DAI, has reached $75 million in total value locked (TVL).

-

Maker reduced its reliance on USDC from 65% in March to just 17% today.

-

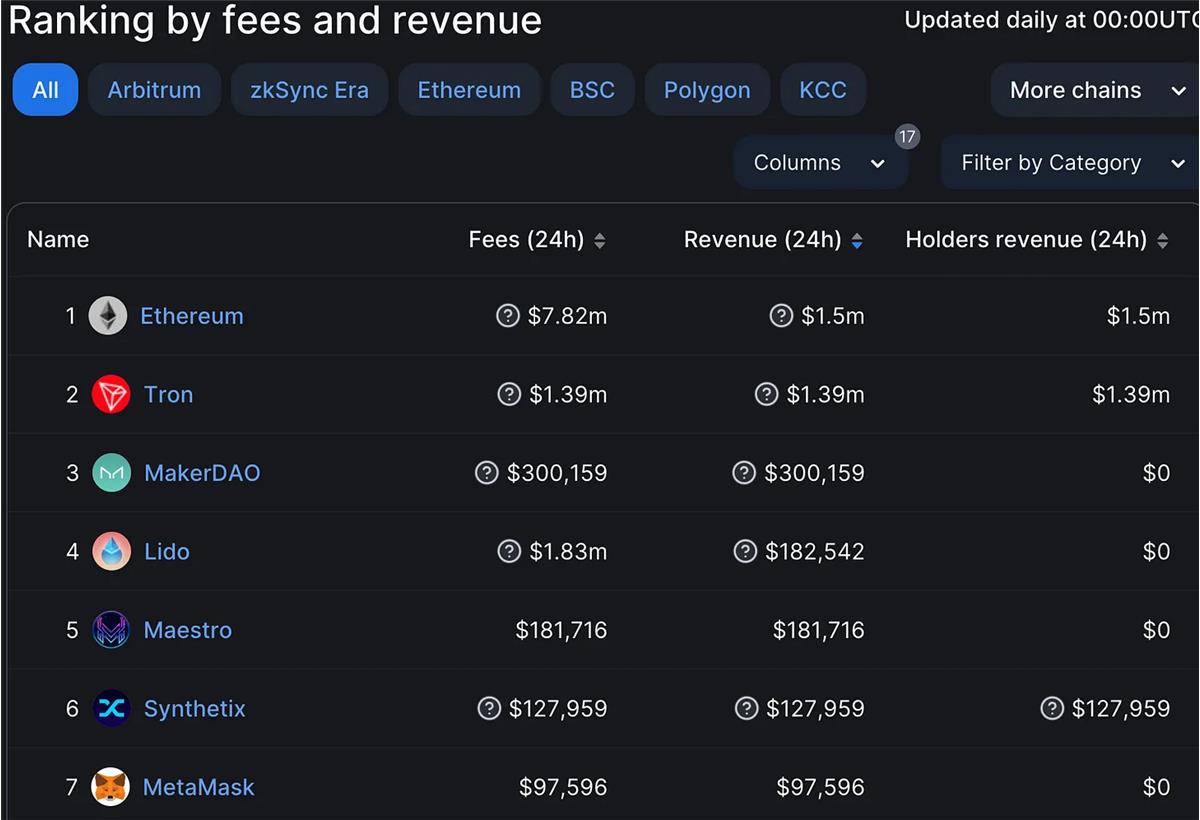

Maker is now the third-highest revenue-generating protocol—above Lido, Synthetix, and MetaMask.

Frax V3 — Dropping USDC?

Frax received a D rating (unsafe) from Bluechip. According to the report, FRAX carries risks due to partially volatile FXS token collateral, heavy reliance on centralized assets (USDC), and significant control by the core team over voting and monetary policy.

It suits yield-seeking farmers and liquidity providers who can handle the protocol’s complexity.

Like DAI, FRAX lost its peg during the USDC depeg event—and appears to have learned from it.

Frax founder Sam Kazemian said on Telegram that V3 is expected to launch within 30 days.

Details are scarce, but DeFi Cheetah reported V3 will be “a fully fiat-independent system,” including no reliance on USDC.

This would be a major shift. If true, V3 will be fundamentally different from V2.

Sam previously stated their long-term goal is a Federal Reserve master account, enabling direct USD holdings and transactions with the Fed—making FRAX the closest thing to a risk-free digital dollar.

This would allow FRAX to drop USDC collateral and scale to hundreds of billions in market cap.

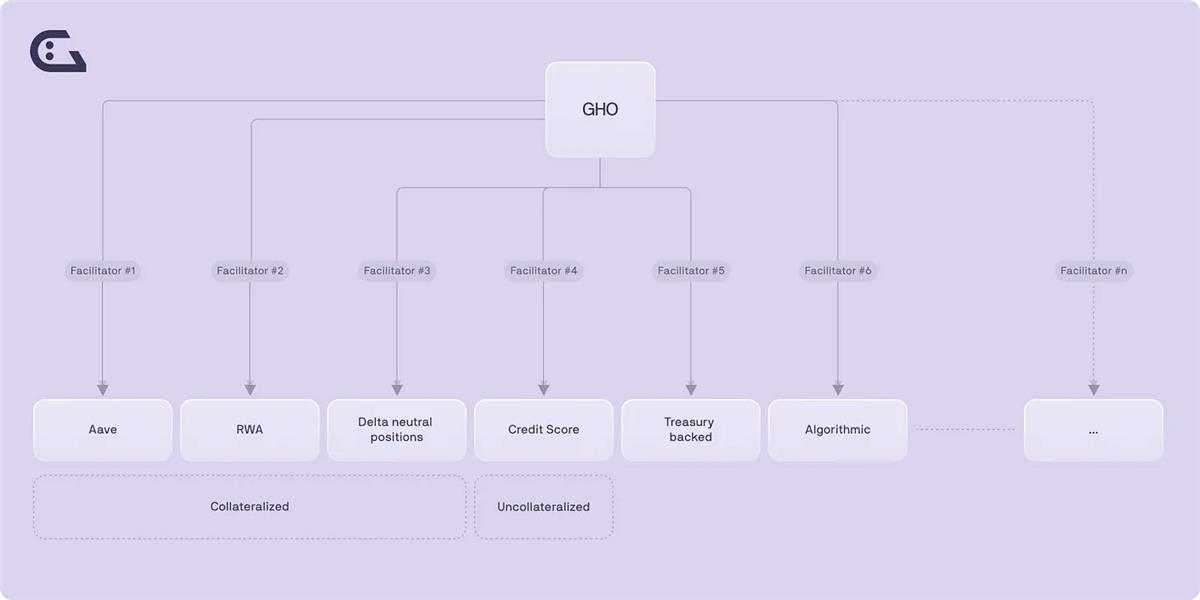

GHO — The New Stablecoin Toy

Despite pre-launch hype, growth has been steady but slower than I expected. While Aave claims $58 billion in TVL, GHO’s market cap has only reached $8 million.

Three factors to consider: First, GHO launched just 11 days ago—still early days. Second, integrating GHO into multiple DeFi protocols takes time, but growth could accelerate. Third, it’s a bear market.

Here are key things to know about how GHO works:

-

Uses over-collateralization to maintain stable value.

-

Only approved addresses (like the Aave protocol itself, possibly others) can mint/burn GHO, each with limited capacity.

-

Generates interest when provided to liquidity protocols, with rates set by Aave governance (currently 1.51%).

-

Cannot be supplied to Aave Ethereum markets—critical for security.

-

Burned upon repayment or liquidation; interest goes to Aave DAO treasury.

-

Interest rate adjusted by Aave governance, not by supply-demand dynamics.

-

Discount model for stkAave holders (30% discount on interest for borrowing 100 GHO).

-

Pegged to $1 by Aave protocol (no oracle needed); arbitrage opportunities arise when price deviates.

GHO provides a new revenue stream for Aave DAO. At the current 1.5% borrowing rate and assuming market cap comparable to LUSD, GHO could bring in an additional $4.4 million in fees for the DAO.

What truly interests me about GHO is its expansion potential.

Aave DAO could introduce new GHO minting addresses backed by real-world assets, Treasuries, or even adopt a partially algorithmic model similar to current FRAX.

GHO’s potential is huge—but actual execution remains to be seen.

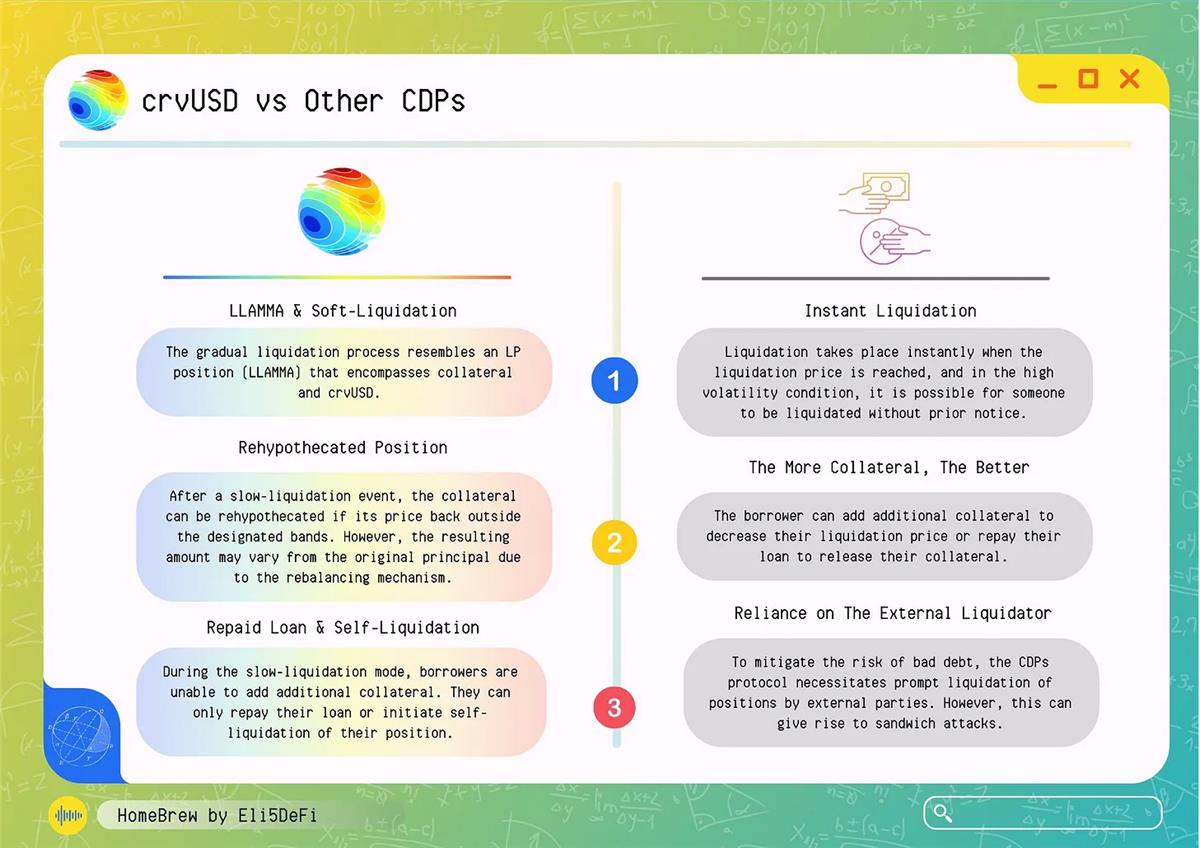

crvUSD — The True Pro DeFi Stablecoin

I think crvUSD is one of the hardest stablecoins to understand. Its unique features include LLAMA, soft liquidations, and reverse liquidations. Here’s a quick summary:

-

crvUSD uses a special automated market-making algorithm called Lending Liquidation AMM Algorithm (LLAMA) for soft liquidations.

-

In typical DeFi lending protocols, if collateral value falls below a threshold, forced liquidation occurs—often causing borrowers significant losses due to liquidation penalties.

-

LLAMA gradually converts depreciating collateral into crvUSD, enabling soft liquidations—helping maintain crvUSD’s peg and protecting borrowers during sharp market drops.

-

However, if collateral price continues to plummet and soft liquidation can't cover losses, forced liquidation occurs—this is the risk of using crvUSD.

-

If collateral price recovers, LLAMA reverses the process by converting crvUSD back into original collateral—known as “reverse liquidation.”

-

To maintain the peg, Curve uses PegKeeper contracts to mint or burn crvUSD as needed, keeping price near $1.

These mechanisms make crvUSD unique in DeFi, offering a more resilient approach to collateral liquidation events. Here’s how the game theory works:

-

Borrow crvUSD using ETH or LST as collateral

-

ETH price rises: Your collateral appreciates, potentially allowing you to borrow more crvUSD.

-

ETH price falls: LLAMA gradually converts your ETH collateral into crvUSD to maintain a healthy collateral ratio.

-

Forced liquidation: In extreme ETH price drops, forced liquidation occurs. But due to soft liquidation, you still retain some crvUSD.

-

Lower liquidation fees: Compared to other protocols, crvUSD’s soft liquidation may offer lower liquidation costs.

Thanks to lower fees and gradual liquidation, this could be a more efficient way to exit positions at the top—compared to borrowing via other lending protocols. Only hope the crvUSD peg holds.

Final Thoughts: A Golden Age for Decentralized Stablecoins?

Innovation doesn’t stop with the stablecoins above. Lower-market-cap projects offer novel approaches:

-

Beanstalk: A unique stablecoin using credit instead of collateral to maintain its $1 peg, dynamically adjusting Bean supply, Soil supply (borrowing capacity), and max rate (Temperature) via its proprietary Sun, Silo, and Field mechanisms.

-

Reserve Protocol: Allows permissionless creation of asset-backed, yield-bearing, over-collateralized stablecoins. Anyone can create a stablecoin backed by a basket of ERC20s—including eUSD backed by stablecoins deposited in Aave and Compound v2.

-

Reflexer’s RAI: Received a B+ safety rating from Bluechip. RAI is a flexible stablecoin whose value is determined by supply and demand, with target exchange rate constantly adjusted by the protocol. Unlike traditional stablecoins, RAI’s target rate changes based on market conditions, creating balance between generating and holding RAI.

Will recent changes usher in a new golden age for DeFi stablecoins?

After UST collapsed, DeFi stablecoins took a hit—then USDC’s depeg exposed DAI, FRAX, and all DeFi’s dependence on USDC.

Yet, Maker’s recent shift away from USDC toward more censorship-resistant models, and Frax V3’s move from USDC to more decentralized collateral, signal progress in the right direction.

Moreover, Liquity’s V2 could provide a scalability solution for stablecoins by addressing the blockchain trilemma, since current LUSD design compromises on scalability.

Synthetix’s sUSD V3 upgrade will also enhance sUSD’s utility beyond the Synthetix ecosystem by supporting multiple collateral types and removing debt pool risk for sUSD minter.

Finally, the launches of crvUSD and GHO suggest new strategies for maximizing DeFi yields beyond TradFi returns—and could even help DeFi enthusiasts strategically exit positions during the next bull run.

Individually, these changes may seem minor—but viewed together within the broader DeFi landscape, they genuinely inspire hope for a true golden age of decentralized stablecoins.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News