Vitalik: Two Thought Experiments for Evaluating Automated Stablecoins

2023.07.07

Share Share to X (Twitter) Navigating Web3 tides with focused insights

Navigating Web3 tides with focused insights

Share to WeChat

Share to WeiboShare to WeChat

Share by Link

Share by Image

TechFlow Selected TechFlow Selected

Vitalik: Two Thought Experiments for Evaluating Automated Stablecoins

What we need is not stablecoin advocacy or stablecoin doom-mongering, but a return to principle-based reasoning.

2023.07.07 - 08:18:41

稳定币

What we need is not stablecoin advocacy or stablecoin doom-mongering, but a return to principle-based reasoning.

Special thanks to Dan Robinson, Hayden Adams, and Dankrad Feist for their feedback and review.

The recent LUNA collapse, which led to tens of billions of dollars in losses, has triggered a wave of criticism against the category of "algorithmic stablecoins," with many calling them a "fundamentally flawed product." Greater scrutiny of DeFi financial mechanisms—especially algorithmic stablecoin designs that aggressively optimize for "capital efficiency"—is welcome. Even more welcome is broader recognition that past performance does not guarantee future returns (or even continued existence). However, market sentiment goes wrong when it uses the same narrative to paint all decentralized crypto algorithmic stablecoins with the same brush, condemning all algorithmic stablecoin projects indiscriminately.

While many algorithmic stablecoin designs are fundamentally flawed and ultimately doomed to collapse, there are also many that could theoretically survive—albeit with high risk—and others that are theoretically sound and have already withstood extreme stress tests under real-world crypto market conditions. Therefore, what we need is not stablecoin advocacy or stablecoin doom-mongering, but a return to principle-based thinking. What principles can we use to evaluate whether a given algorithmic stablecoin is truly robust? For me, I begin by testing two thought experiments.

What determines the price of the volatile token (LUNA)? Its value may be purely speculative, based on expectations of future demand for the stablecoin (which would require burning volcoin to mint UST). Alternatively, value may come from fees: transaction fees from stablecoin/LUNA exchanges, annual holding fees paid by stablecoin holders, or a combination. But in all cases, the volcoin’s price derives from expectations about future activity in the LUNA ecosystem.

What determines the price of the volatile token (LUNA)? Its value may be purely speculative, based on expectations of future demand for the stablecoin (which would require burning volcoin to mint UST). Alternatively, value may come from fees: transaction fees from stablecoin/LUNA exchanges, annual holding fees paid by stablecoin holders, or a combination. But in all cases, the volcoin’s price derives from expectations about future activity in the LUNA ecosystem.

There are two primary reasons to become a RAI lender:

1. Going long on ETH: If you deposit 10 ETH and withdraw 500 RAI, your final position is worth 500 RAI but has exposure to 10 ETH—so its value changes by approximately 2% for every 1% change in ETH’s price.

2. Arbitrage: If you find a fiat-denominated investment that appreciates faster than RAI, you can borrow RAI, invest the funds, and profit from the difference.

If ETH’s price falls and a vault becomes undercollateralized (i.e., RAI debt exceeds two-thirds of the deposited ETH’s value), a liquidation event occurs. The vault is then auctioned off to others who provide additional collateral.

Another key mechanism is the redemption rate adjustment. In RAI, the target is not a fixed dollar amount; instead, it drifts up or down, and the rate of drift adjusts based on market conditions:

- If RAI’s price is above target, the redemption rate decreases, reducing the incentive to hold RAI and increasing the incentive to be a negative holder (lender), pulling the price down.

- If RAI’s price is below target, the redemption rate increases, increasing the incentive to hold RAI and decreasing the incentive to lend, pushing the price up.

There are two primary reasons to become a RAI lender:

1. Going long on ETH: If you deposit 10 ETH and withdraw 500 RAI, your final position is worth 500 RAI but has exposure to 10 ETH—so its value changes by approximately 2% for every 1% change in ETH’s price.

2. Arbitrage: If you find a fiat-denominated investment that appreciates faster than RAI, you can borrow RAI, invest the funds, and profit from the difference.

If ETH’s price falls and a vault becomes undercollateralized (i.e., RAI debt exceeds two-thirds of the deposited ETH’s value), a liquidation event occurs. The vault is then auctioned off to others who provide additional collateral.

Another key mechanism is the redemption rate adjustment. In RAI, the target is not a fixed dollar amount; instead, it drifts up or down, and the rate of drift adjusts based on market conditions:

- If RAI’s price is above target, the redemption rate decreases, reducing the incentive to hold RAI and increasing the incentive to be a negative holder (lender), pulling the price down.

- If RAI’s price is below target, the redemption rate increases, increasing the incentive to hold RAI and decreasing the incentive to lend, pushing the price up.

First, LUNA’s price falls. Then, the stablecoin begins to waver. The system tries to prop up demand by issuing more LUNA. With weak market confidence and few buyers, LUNA’s price plummets. Finally, once LUNA approaches zero, the stablecoin collapses too.

In theory, if the decline were very gradual, expectations of future revenue for the LUNA ecosystem—and thus its market cap relative to the stablecoin—might remain sufficient. But successfully managing such a slow decline is unlikely; far more probable is a sudden, rapid drop followed by a loud crash.

First, LUNA’s price falls. Then, the stablecoin begins to waver. The system tries to prop up demand by issuing more LUNA. With weak market confidence and few buyers, LUNA’s price plummets. Finally, once LUNA approaches zero, the stablecoin collapses too.

In theory, if the decline were very gradual, expectations of future revenue for the LUNA ecosystem—and thus its market cap relative to the stablecoin—might remain sufficient. But successfully managing such a slow decline is unlikely; far more probable is a sudden, rapid drop followed by a loud crash.

Safe gradual exit: At each step, LUNA’s market cap remains justified by sufficient expected future revenue to keep the stablecoin secure at current levels.

Safe gradual exit: At each step, LUNA’s market cap remains justified by sufficient expected future revenue to keep the stablecoin secure at current levels.

Unsafe gradual exit: At some point, expected future revenue is insufficient to justify the LUNA market cap needed to secure the stablecoin, risking collapse.

Unsafe gradual exit: At some point, expected future revenue is insufficient to justify the LUNA market cap needed to secure the stablecoin, risking collapse.

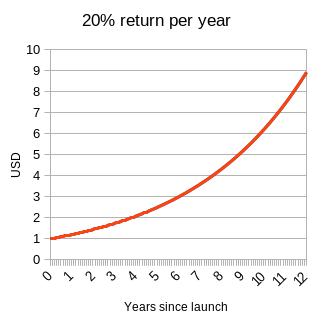

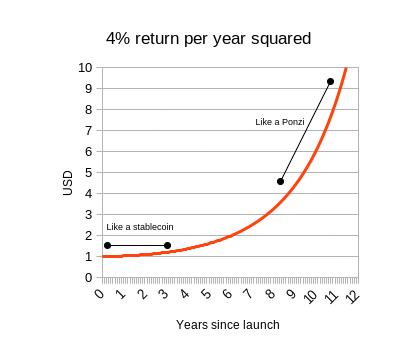

Clearly, no real investment yields nearly 20% annual returns indefinitely, nor can any sustain 4% forever. But what happens if you try?

I argue that a stablecoin essentially has two ways to track such an index:

1. It charges holders a negative interest rate, roughly offsetting the dollar-denominated growth rate of the index.

2. It becomes a Ponzi scheme, delivering impressive returns for a while before suddenly collapsing.

It should now be clear why RAI follows (1) and LUNA follows (2)—and why RAI is superior. But this also reveals a deeper, more important truth: for a collateralized algorithmic stablecoin to be sustainable, it must allow for the possibility of negative interest rates in some form. If RAI were programmatically prevented from implementing negative rates (as early single-collateral DAI was), and were pegged to a rapidly appreciating index, it too would become a Ponzi scheme.

Even outside the absurd assumption of pegging to a Ponzi-like index, a stablecoin must be able to handle situations where holding demand exceeds borrowing demand—even at zero interest rates. If it cannot, the price will rise above the peg, making the stablecoin vulnerable to unpredictable bidirectional volatility.

Negative interest rates can be implemented in two ways:

1. RAI-style: a floating target that can drift downward over time if the redemption rate is negative.

2. Balance decay: account balances gradually decrease over time.

Option (1) has UX drawbacks—the stablecoin no longer clearly tracks “$1.” Option (2) has developer experience challenges—developers aren’t used to receiving N tokens not meaning they can later send N coins unconditionally. But choosing one seems unavoidable—unless you follow MakerDAO’s path and become a hybrid stablecoin, using both pure (decentralized) crypto assets and centralized assets (like USDC) as collateral.

Clearly, no real investment yields nearly 20% annual returns indefinitely, nor can any sustain 4% forever. But what happens if you try?

I argue that a stablecoin essentially has two ways to track such an index:

1. It charges holders a negative interest rate, roughly offsetting the dollar-denominated growth rate of the index.

2. It becomes a Ponzi scheme, delivering impressive returns for a while before suddenly collapsing.

It should now be clear why RAI follows (1) and LUNA follows (2)—and why RAI is superior. But this also reveals a deeper, more important truth: for a collateralized algorithmic stablecoin to be sustainable, it must allow for the possibility of negative interest rates in some form. If RAI were programmatically prevented from implementing negative rates (as early single-collateral DAI was), and were pegged to a rapidly appreciating index, it too would become a Ponzi scheme.

Even outside the absurd assumption of pegging to a Ponzi-like index, a stablecoin must be able to handle situations where holding demand exceeds borrowing demand—even at zero interest rates. If it cannot, the price will rise above the peg, making the stablecoin vulnerable to unpredictable bidirectional volatility.

Negative interest rates can be implemented in two ways:

1. RAI-style: a floating target that can drift downward over time if the redemption rate is negative.

2. Balance decay: account balances gradually decrease over time.

Option (1) has UX drawbacks—the stablecoin no longer clearly tracks “$1.” Option (2) has developer experience challenges—developers aren’t used to receiving N tokens not meaning they can later send N coins unconditionally. But choosing one seems unavoidable—unless you follow MakerDAO’s path and become a hybrid stablecoin, using both pure (decentralized) crypto assets and centralized assets (like USDC) as collateral.

What Is an Algorithmic Stablecoin?

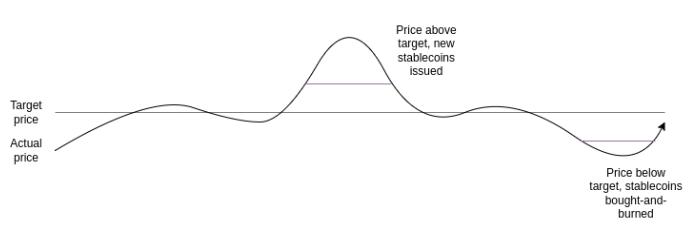

For the purposes of this article, an algorithmic stablecoin is a system with the following properties: 1. It issues a stablecoin that attempts to track a specific price index. Usually, the target is $1, though other targets are possible. There exists a targeting mechanism that continuously pushes the price toward the stable index (e.g., $1) whenever it deviates in either direction. This excludes ETH and BTC from being considered stablecoins. 2. The targeting mechanism is fully decentralized, with no reliance on specific trusted participants. In particular, it must not depend on custodians of assets, which means USDT and USDC do not qualify as stablecoins under this definition. In practice, (2) implies that the targeting mechanism must be some form of smart contract managing a reserve of crypto assets, using those assets to support the price when it falls.How Does Terra Work?

Terra-style stablecoins (similar in concept to Seigniorage Shares, despite differing implementation details) operate using two tokens: a stablecoin and a volatile token (volcoin). In Terra, UST is the stablecoin and LUNA is the volcoin. The stablecoin maintains its peg via a simple mechanism: - If the stablecoin’s price exceeds the target, the system auctions new stablecoins (using the proceeds to burn LUNA), until the price returns to target. - If the stablecoin’s price falls below target, the system buys back and burns stablecoins (issuing new LUNA to fund the purchase), until the price returns to target.

What determines the price of the volatile token (LUNA)? Its value may be purely speculative, based on expectations of future demand for the stablecoin (which would require burning volcoin to mint UST). Alternatively, value may come from fees: transaction fees from stablecoin/LUNA exchanges, annual holding fees paid by stablecoin holders, or a combination. But in all cases, the volcoin’s price derives from expectations about future activity in the LUNA ecosystem.

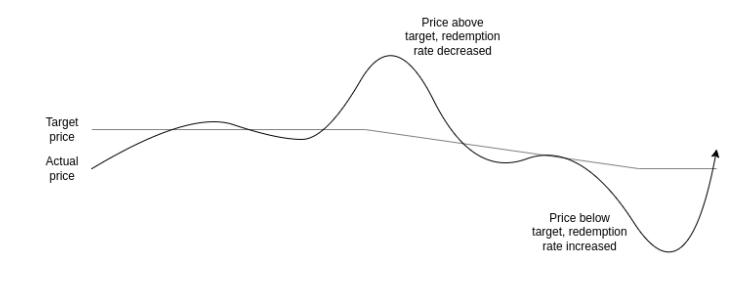

How Does RAI Work?

In this article, I focus on RAI rather than DAI because RAI better represents the pure (decentralized) “ideal type” of an algorithmic stablecoin backed solely by ETH. DAI is a hybrid system, backed by both centralized and decentralized collateral—a reasonable design choice, but one that complicates analysis. In RAI, there are two main types of participants (FLX holders, the speculative token, play a less central role):

There are two primary reasons to become a RAI lender:

1. Going long on ETH: If you deposit 10 ETH and withdraw 500 RAI, your final position is worth 500 RAI but has exposure to 10 ETH—so its value changes by approximately 2% for every 1% change in ETH’s price.

2. Arbitrage: If you find a fiat-denominated investment that appreciates faster than RAI, you can borrow RAI, invest the funds, and profit from the difference.

If ETH’s price falls and a vault becomes undercollateralized (i.e., RAI debt exceeds two-thirds of the deposited ETH’s value), a liquidation event occurs. The vault is then auctioned off to others who provide additional collateral.

Another key mechanism is the redemption rate adjustment. In RAI, the target is not a fixed dollar amount; instead, it drifts up or down, and the rate of drift adjusts based on market conditions:

- If RAI’s price is above target, the redemption rate decreases, reducing the incentive to hold RAI and increasing the incentive to be a negative holder (lender), pulling the price down.

- If RAI’s price is below target, the redemption rate increases, increasing the incentive to hold RAI and decreasing the incentive to lend, pushing the price up.

Thought Experiment 1: Can a Stablecoin Theoretically Survive a Reduction to "Zero Users"?

In the non-crypto real world, nothing lasts forever. Companies fail—either because they never gain enough users, because demand for their product vanishes, or because they’re overtaken by stronger competitors. Sometimes, partial collapses occur, with products falling from mainstream to niche status (e.g., MySpace). Such churn is necessary to make room for innovation. But in the traditional world, when a product shuts down or declines, users are usually not severely harmed. Sure, there are edge cases, but overall, shutdowns are orderly and manageable. But what about algorithmic stablecoins? If we take a bold and radical view, a robust algorithmic stablecoin should be able to withstand systemic decline and massive user loss without collapsing—without relying on a constant influx of new users.Can Terra Exit Safely?

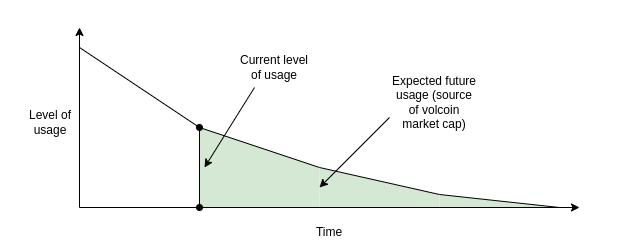

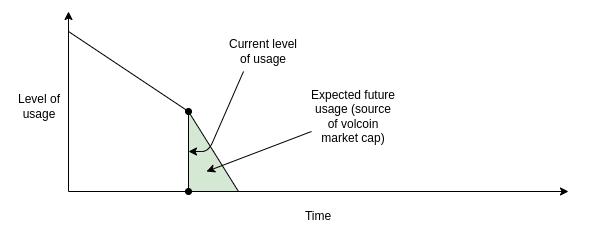

In Terra, the volatile token (LUNA) derives its price from expectations of future system activity and fees. What happens if these expected future activities drop close to zero? LUNA’s market cap declines until it becomes very small relative to the stablecoin supply. At this point, the system becomes extremely fragile: even a small shock to stablecoin demand triggers the mechanism to mint large amounts of volcoin (LUNA), leading to hyperinflation of LUNA and eventual collapse of the stablecoin’s value. This collapse can become a self-fulfilling prophecy: if a crash seems likely, future expected value of LUNA drops, reducing its market cap further, making the system even more fragile, potentially triggering a catastrophic crash—as we saw in May.

First, LUNA’s price falls. Then, the stablecoin begins to waver. The system tries to prop up demand by issuing more LUNA. With weak market confidence and few buyers, LUNA’s price plummets. Finally, once LUNA approaches zero, the stablecoin collapses too.

In theory, if the decline were very gradual, expectations of future revenue for the LUNA ecosystem—and thus its market cap relative to the stablecoin—might remain sufficient. But successfully managing such a slow decline is unlikely; far more probable is a sudden, rapid drop followed by a loud crash.

Safe gradual exit: At each step, LUNA’s market cap remains justified by sufficient expected future revenue to keep the stablecoin secure at current levels.

Unsafe gradual exit: At some point, expected future revenue is insufficient to justify the LUNA market cap needed to secure the stablecoin, risking collapse.

Can RAI Exit Safely?

RAI’s security relies on an external asset (ETH), making it far more capable of a safe exit. If declining demand creates imbalance (either holding or lending demand drops faster), the redemption rate adjusts to restore equilibrium. Lenders maintain leveraged ETH positions, not FLX, so there’s no positive feedback loop where declining confidence in RAI reduces lending demand. In an extreme case where all demand for holding RAI vanishes except for one holder, the redemption rate would spike, eventually forcing all lenders into liquidation. The last remaining holder could then buy vaults in the liquidation auction, use their RAI to immediately repay debt, and withdraw ETH. This gives them a fair opportunity to redeem their RAI at a price derived from the ETH in the vault. Another extreme worth considering is if RAI became Ethereum’s dominant application. In that case, reduced future demand for RAI could impact ETH’s price, potentially triggering cascading liquidations and systemic chaos. But RAI is far more resilient to this scenario than Terra-style systems.Thought Experiment 2: What Happens If You Try to Peg a Stablecoin to an Index That Grows 20% Per Year?

Currently, most stablecoins are pegged to the US dollar. RAI is a minor exception—their peg drifts over time due to redemption rate adjustments, starting at $3.14 rather than $1 (the exact starting value is friendly to non-mathematicians; a true math nerd would pick tau = $6.28). But they don’t have to be. You could peg a stablecoin to a basket of assets, a consumer price index, or even a complex formula (“the value of one hectare of forest in Yakutia divided by (global average CO₂ concentration minus 375)”). As long as you can find an oracle to verify the index and attract market participants, such a stablecoin could function.

Clearly, no real investment yields nearly 20% annual returns indefinitely, nor can any sustain 4% forever. But what happens if you try?

I argue that a stablecoin essentially has two ways to track such an index:

1. It charges holders a negative interest rate, roughly offsetting the dollar-denominated growth rate of the index.

2. It becomes a Ponzi scheme, delivering impressive returns for a while before suddenly collapsing.

It should now be clear why RAI follows (1) and LUNA follows (2)—and why RAI is superior. But this also reveals a deeper, more important truth: for a collateralized algorithmic stablecoin to be sustainable, it must allow for the possibility of negative interest rates in some form. If RAI were programmatically prevented from implementing negative rates (as early single-collateral DAI was), and were pegged to a rapidly appreciating index, it too would become a Ponzi scheme.

Even outside the absurd assumption of pegging to a Ponzi-like index, a stablecoin must be able to handle situations where holding demand exceeds borrowing demand—even at zero interest rates. If it cannot, the price will rise above the peg, making the stablecoin vulnerable to unpredictable bidirectional volatility.

Negative interest rates can be implemented in two ways:

1. RAI-style: a floating target that can drift downward over time if the redemption rate is negative.

2. Balance decay: account balances gradually decrease over time.

Option (1) has UX drawbacks—the stablecoin no longer clearly tracks “$1.” Option (2) has developer experience challenges—developers aren’t used to receiving N tokens not meaning they can later send N coins unconditionally. But choosing one seems unavoidable—unless you follow MakerDAO’s path and become a hybrid stablecoin, using both pure (decentralized) crypto assets and centralized assets (like USDC) as collateral.

What Can We Learn?

Overall, the crypto space must move away from the mindset that endless growth ensures safety. Claiming that “the world can continue operating this way” is unacceptable. The world isn’t offering real returns through rational economic growth—it’s exhibiting pathological growth patterns that deserve strong criticism. Instead, while we should expect growth, we should evaluate system safety by examining their steady-state behavior, how they perform under pessimistic or extreme conditions, and whether they can safely wind down. Passing these tests doesn’t guarantee safety—there may still be vulnerabilities due to inadequate collateral ratios, bugs, or governance flaws—but stress resilience should be our first line of evaluation.Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News

Add to Favorites

Share to Social Media