Arthur Hayes: China-U.S. rivalry, capital outflows—where is the crypto world headed amid economic power struggles?

TechFlow Selected TechFlow Selected

Arthur Hayes: China-U.S. rivalry, capital outflows—where is the crypto world headed amid economic power struggles?

The cryptocurrency market has never been an isolated realm. Understanding macroeconomic trends and international economic and political influences greatly benefits our perspective and ability to anticipate market movements.

Author: ARTHUR HAYES

Translated by: TechFlow

TechFlow Commentary

Arthur Hayes is undoubtedly an experienced and globally-minded insider in the crypto space.

In this article, Hayes discusses the套路 (modus operandi) of Federal Reserve policy within traditional finance and how it impacts the crypto market. Additionally, he examines the reasons, methods, and outcomes behind the entry and exit of America’s affluent middle class into cryptocurrency—starting from a rarely discussed perspective on U.S. social class structure.

Looking eastward as a Westerner, Hayes, through a series of detailed data comparisons, thoroughly envisions the brewing currency war between China and Japan—and how this may channel some Chinese capital into cryptocurrencies via Hong Kong's financial markets. Thus, what appears to be an isolated crypto market has, amid capital inflows and outflows shaped by great-power competition, become an inevitable battleground for economic confrontation—whether willingly or passively.

The crypto market has never been a self-contained entity. Understanding macroeconomic forces and international political-economic dynamics greatly enhances our vision and predictive ability regarding market trends. For this reason, we have translated Hayes’ article for your reading.

(Note: The views expressed below are solely those of the author and should not be taken as investment advice, recommendations, or grounds for making investment decisions.)

Last week, I met with my favorite volatility fund manager David Dredge and several of his colleagues. Our conversation began with how Japanese financial markets once flourished—when ordinary people and corporations had ample cash, and rising inflation pulled them away from low- or zero-yield bank deposits into stocks and real estate.

Then we turned to the current state of the crypto market, and Dave asked me: "What exactly is going on with the SEC’s crackdown on Coinbase and Binance?"

I replied that this was just another example of the fiat financial system trying to restrict capital from leaving its casino. There are massive debts to repay, and the system needs all available liquidity to stay afloat. He nodded in agreement. Dave likes to refer to the fragile fiat financial system as Sharpe World. (Note: Named after the Sharpe ratio, which most risk managers consider the standard measure of portfolio “risk”—yet it’s entirely fictitious because it focuses on probabilistic possibilities rather than actual outcomes of investment decisions.)

I then added that I don’t think America’s stance on crypto actually matters much, because capital is fungible.

Finally, we discussed the impending depreciation of the Chinese yuan (CNY). The topic arose from our shared skepticism about the current upward trend in Singapore’s residential property market. Chinese capital doesn't care how high taxes on real estate purchases are because the yuan is overvalued while the Singapore dollar is undervalued. So even if they must pay 60% in taxes to the Singapore government, Chinese investors still see Singaporean properties as cheap bank accounts where they can safely store their wealth.

David argued further that Beijing will eventually allow the CNY to depreciate against the Japanese yen (JPY), since Japan is China’s true global export competitor. While the Bank of Japan (BOJ) continues its money-printing activities—known as Yield Curve Control (YCC)—all other major central banks have been raising interest rates and shrinking their balance sheets. As a result, the yen has rapidly depreciated against both the dollar and the yuan. Since the pandemic, the People’s Bank of China (PBOC) and the Chinese government have been relatively restrained in printing money—which is why the yuan appears so “strong” against the USD and JPY.

We briefly touched upon the fact that with the global economy slowing down, China’s exports are beginning to slow as well. The government will soon need to stimulate growth to appease the public, meaning the PBOC will need to adjust its monetary policy to weaken the yuan against the yen and the dollar. A weaker yuan would help boost China’s exports at the expense of its Japanese competitors.

As I prepared to head home, a small idea popped up. The current market reminds me of the summer of 2015. After the brutal bear market triggered by Mt. Gox’s collapse in early 2014, volatility and trading volume plummeted; sideways price action became boring. Bitcoin hovered around $200. But in August 2015, the PBOC suddenly sparked Chinese interest in Bitcoin by devaluing the yuan against the dollar. From August to November 2015, Bitcoin tripled in price, driven by Chinese traders. I believe something similar could happen in 2023.

Since 2021—when China’s major exchanges ceased operations on the mainland—capital inflows from Chinese retail investors into the crypto market have collapsed. The most influential and profitable retail segment has shifted from China to the United States.

Starting in 2020, the U.S. government (USG) did something unexpected when deciding how to distribute stimulus funds. Instead of simply handing free money to the wealthy who already held financial assets, the USG distributed cash directly to everyone—rich or poor. For the mass affluent class (which I’ll define more precisely later in this article; for now, let’s call them households earning between $100K and $200K annually), many didn’t actually need government aid because they hadn’t lost their jobs (as they were white-collar workers capable of remote work). They took this free money and went straight into financial markets, having a field day. Stocks, cryptocurrencies, NFTs—all were pushed higher by American retail investors. As usual, some made enough to buy Lamborghinis, but the vast majority bought near the top and were doomed when Fed Chair Powell began hiking rates in March 2022.

Now, due to troubles created for Satoshi loyalists by traditional finance, there’s panic in the market about the possibility of U.S. retail investors withdrawing from the crypto capital markets. I believe this concern is misplaced. If you’re forced to sell—or prevented from offering services to Americans—alongside institutions pushing such actions, you’ll merely be another fool buying at the top and selling at the bottom.

Because on the other side of Asia, the silent currency war between China and Japan over export competitiveness will drive the world’s second-largest economy to issue massive amounts of credit. This credit issuance—that is, money printing—will ultimately lead to a depreciation of the yuan and prompt China’s mass affluent class to move their capital elsewhere. Given the sheer number of wealthy individuals in China, whenever their money wants to “escape,” prices of all hard assets will be pushed upward.

In this article, I’ll cover a lot. I’ll begin by discussing Sharpe World, then explain why the U.S. goes to great lengths to convince its citizens that their money is “safest” in the hands of American financial institutions. Then I’ll discuss capital fungibility—how even if U.S. affluent retail investors face difficulty accessing crypto markets, the rich in America can still easily exit the fiat system and purchase hard crypto assets. This will ultimately lead me—and hopefully you—to conclude that all the anxiety over what’s happening in the “land of the free” is mere mental anguish. Then I’ll turn to the brewing currency war between China and Japan, and how it might channel some Chinese capital into crypto through Hong Kong’s financial markets.

Sharpe World

David is one of the smartest and most brilliant derivatives traders I’ve ever met. Every time we talk, I learn something new about market structure. He spent much of his banking career in the Asia-Pacific region. During our last meeting, we swapped stories about favorite bars in Jakarta—he lived there in the late 1980s, while I frequented them in the 2010s.

He maintains close ties with economic institutions in both East and West. U.S. Treasury Secretary Janet Yellen was one of his university professors. He also serves on advisory committees for multiple central banks. Each time we meet, he talks about getting the “adults in the room” to understand that their approach to risk is completely wrong. As I mentioned earlier, he calls it Sharpe World.

“How do humans manage the risk of death?” Dave retorted.

“You avoid doing things that will certainly kill you—even if the probability each time is small—because this extends your life.”

I thought of simple things humans do to extend lifespan:

-

Not smoking;

-

Not driving under the influence;

-

Wearing motorcycle/bicycle helmets;

-

Buckling seatbelts.

If you consistently follow these simple rules, you can completely eliminate preventable causes of death and likely extend your life. But humans don’t consciously assess every single action at every moment to determine the likelihood of death. For instance, an average cyclist wouldn’t look at a helmet and say like a finance professional:

“This thing is annoying. If I don’t wear it today, the chance of an accident killing me is a 3-sigma event (<1%), so the odds are low.” Then that day turns out to be a 3-sigma day—you can’t ask God for another life just because you adhered to a +/- 2-sigma log-normal probability decision rule and thus took appropriate risk… and you die.

Yet in Sharpe World, financial institutions constantly bet on probabilities and engage in high-risk activities. Their main reason is knowing that roughly every 5–7 years, the U.S. central bank and government will bail them out when they inevitably face collapse. This system always rescues residents of Sharpe World by printing money and devaluing the public’s wealth.

Governments and financial institutions love Sharpe World because it’s governed by ultra-smart scholars from “elite universities” who set the rules and tell everyone what to do. Everyone follows the rules, so when things blow up, no one claims they acted unethically. Therefore, when the public must foot the bill to save yet another regulated-to-failure institution (like Credit Suisse), they shouldn’t feel it’s unfair.

The core purpose of the entire monetary confidence game is to disguise unproven economic theories as natural laws to keep investors buying and holding government bonds long-term. If I, as a government, can persuade my citizens to defer consumption and invest their savings in me long-term, then I am a successful, credible state actor. Conversely, if investors are only willing to lend short-term (if at all), then the nation lacks credibility and must resort to unpopular measures (e.g., high taxes).

Indoctrination into Sharpe World begins early for elite financiers. If you’ve taken any university-level finance course, you’re already familiar with the efficient frontier and the supposed magic of certain assets—government bonds—that supposedly increase returns while reducing overall portfolio volatility. Hence, all portfolio managers need only lever up long-dated government bonds and stop worrying about returns.

With U.S. and developed-market bond yields enjoying a 40-year bull run, everyone thought they were geniuses. People like Ray Dalio needed only to go long bonds to become billionaires. Whenever markets wobbled, they’d apply more leverage, knowing authorities would print money to suppress any real price discovery.

But now, after the fastest rise in inflation and short-term interest rates in decades, there seems little rationale for investors to hold long-dated government bonds. And you, the readers, are part of this story. Your retirement plans are managed by public or private pension funds filled with residents of Sharpe World. Fund managers are legally required to allocate most of your savings to long-dated government bonds—well, because the government says so. These are the same bonds that get hammered when inflation rises, yet financial institutions in Sharpe World obediently direct client capital to the slaughterhouse because rules are rules! In Sharpe World, no one uses their own money to buy long-dated government bonds.

Dave repeatedly emphasizes this point in his monthly newsletter. His view is that investors should abandon the notion that holding government bonds reduces volatility and increases returns, because at low interest rates, these instruments no longer perform their magical role. Instead, investors should hold equities, gold, crypto, and long-volatility tail hedges.

“Participate and protect,” he says. “My fund provides protection via derivatives, while you, as investors, should simply buy a basket of equities to participate in upside moves.”

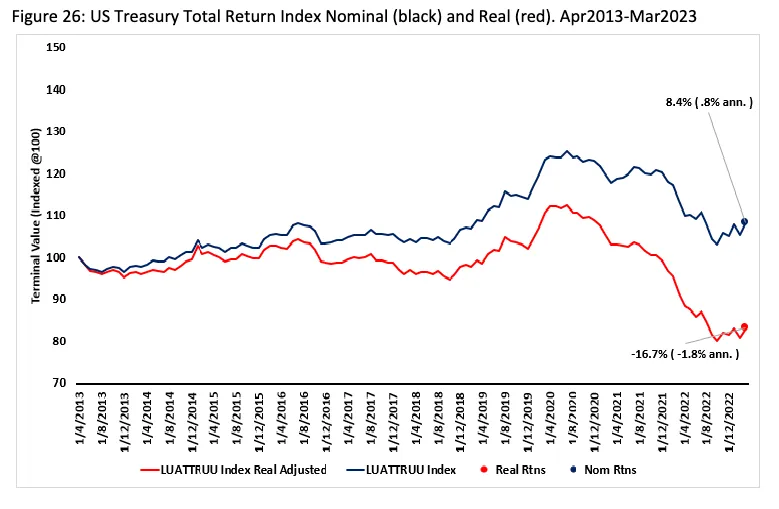

This chart clearly shows that over the past decade, holding a basket of U.S. Treasuries (UST) resulted in losses both nominally and in real terms.

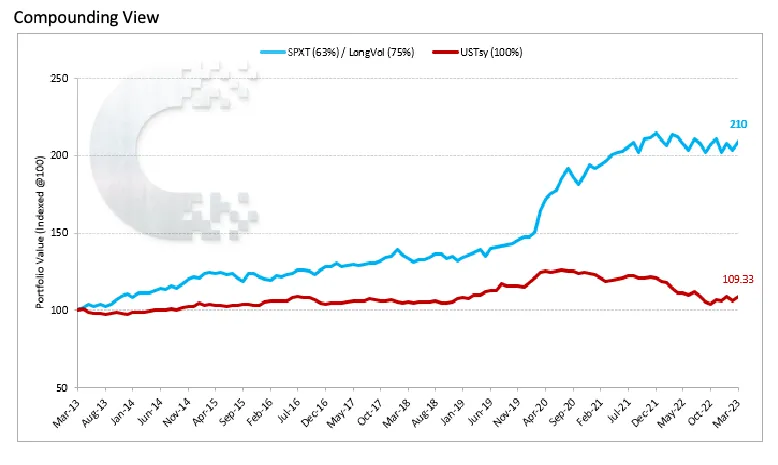

The red line in the above chart represents the performance of the standard 60/40 portfolio—the most commonly recommended strategy—where 60% is allocated to equities and 40% to bonds via the Bloomberg U.S. Aggregate Index. The blue line shows a portfolio maintaining the standard 60% equity allocation, but allocating the remaining 40% to bonds, investing 62.5% of that portion into equities and leveraged long volatility (LongVol) for the other 37.5% (resulting in 75% risk exposure). As you can see, this bond-free blue portfolio outperformed the traditional 60/40 portfolio over the past decade.

This raises an important question: Why do your fund managers still hold long-dated government bonds? The answer is that the entire structure of the U.S. fiat financial system is designed to force or strongly encourage your pension fund managers to hold government bonds. Failing to comply could cost them their jobs—an outcome no citizen of Sharpe World wants. Being a mediocre puppet in Sharpe World, obediently defrauding clients while earning millions annually, isn’t a bad gig.

But eventually, after losing enough client money, clients will demand change. That’s what central bankers must manage. Facing persistent inflation, bank failures, and strong performance of alternative hard assets like gold and Bitcoin—which preserve or increase purchasing power over time—how do you convince investors to keep losing money by holding government bonds?

The reality is, there aren’t enough persuasive arguments left to keep investors committed to this losing bet. Therefore, the U.S. government must force investors to act—usually by erecting barriers to prevent capital from exiting the system. For the U.S., this is tricky—if it imposes explicit capital controls targeting crypto or other off-system assets, the dollar will cease being the global reserve currency. However, it seems the U.S. has realized that if access to crypto becomes painful and expensive enough, most of the mass affluent and below will give up—their short attention spans will push them back to Instagram and TikTok subscriptions.

The U.S. is deeply invested in supporting Sharpe World because it benefits most from its existence. American universities serve as brainwashing centers for citizens of Sharpe World. These individuals spread globally to ensure everyone adheres to the global financial system that keeps the dollar, long-dated Treasuries, and major banks (JPMorgan, Goldman Sachs, Citibank, etc.) on a pedestal. Considering the U.S. stopped manufacturing decades ago and decided to export financial engineering instead, it makes sense for America to ensure continued adherence to Sharpe World’s rules. When the existing order is threatened, the entire system unites to take whatever measures necessary to ensure capital never leaves.

Fungible Capital

The U.S. population makes up only about 4% of the world’s total—a very small share, but this 4% is relatively wealthy compared to the rest of the globe. That’s why, as investors, we care about what this small group does with their money.

However, this wealth is not evenly distributed among Americans—it’s highly concentrated at the top. 70% of U.S. wealth is held by 10% of Americans.

In fact, most Americans are broke, making them irrelevant to global capital markets. You might counter that casinos make a lot from the poor. My response: although the casino floor is full of gamblers dreaming of easy riches, the real profits—and what drives quarterly revenue—are made by whales in private rooms upstairs. You can’t build Las Vegas, Macau, or Monaco on slot-machine-playing “degenerate gamblers.”

Setting aside the richest 10%, let’s focus on the next tier up the U.S. economic ladder: the affluent class. As I mentioned earlier, I define this group as households earning between $100K and $200K annually—roughly 25% of the nation.

This group is significant because during the outbreak of COVID, they likely continued working from home. So when lockdowns hit, they didn’t need government relief to survive. They essentially had extra income to spend or invest as they pleased.

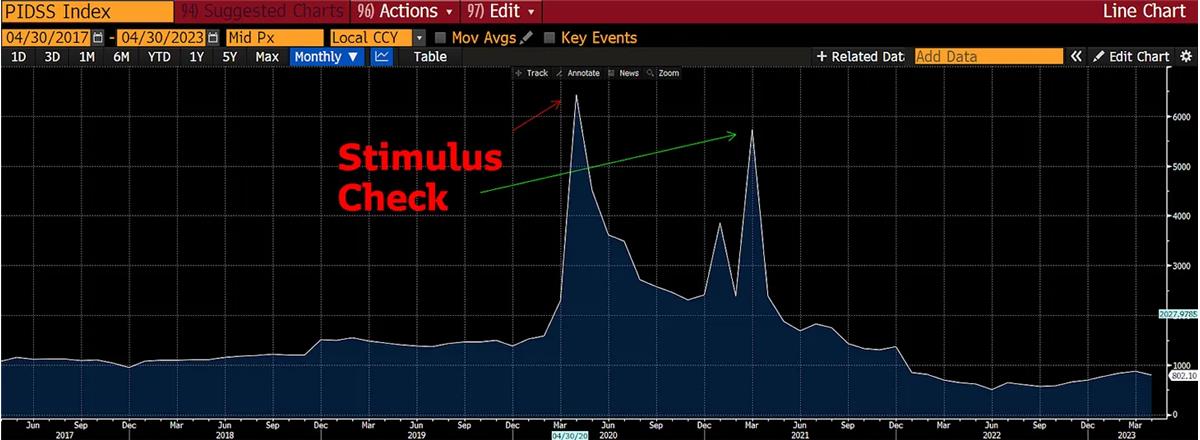

It was this class that drove the surge in online broker (e.g., Robinhood) registrations. This group first experimented with crypto trading in 2020 and 2021.

The two spikes in the U.S. personal savings rate were due to government stimulus checks. Most of that money was used between 2020 and 2021, which is why savings are now reverting to long-term averages.

This class drove the market rally during the COVID-era crypto boom. Yet this group isn’t truly wealthy. They may have some savings, but financial intermediaries serving the rich won’t open accounts for them. This affluent class falls squarely into the retail domain, making easy access to crypto markets difficult. Platforms like Coinbase, Kraken, Gemini, Crypto.com, Binance.us, and Robinhood are among the few options these retail investors are forced to use.

During the last bull run, these exchanges and fintech firms were highly valued for serving the affluent class—individuals with substantial disposable income boosted by U.S. government aid. Without these retail-focused fintech services, however, the affluent class would have struggled to access global crypto markets easily.

Let’s brainstorm: suppose changes in U.S. regulatory policy force these fintech companies to delist most tokens and/or completely halt crypto trading services (Crypto.com recently exited the U.S. market as an example). This would fully exclude the U.S. affluent class, eliminating what seems like a large pool of capital. Sounds bad—but actually, it doesn’t matter.

This class entered crypto initially because of government handouts. However, the degree of overt, deep inflation caused by pandemic-era money printing was so extreme that I doubt monetary authorities will repeat it anytime soon. Instead, the Fed and U.S. Treasury will likely distribute newly printed money via interest payments on government bonds and central bank deposit facilities—their usual method of propping up financial markets.

If the government chooses to distribute new money via interest rather than direct checks, these funds won’t flow to the affluent class, who have little savings. Money will go directly to the top 10%, possibly even just the top 1% who hold most U.S. wealth. This wealth will flow into various forms of physical assets and stores of value. Since the 1% have numerous advisors helping them maximize returns,

These are the world’s most active bank users. Even if they’re American, they can trade any and all financial assets globally—meaning if this wealthy cohort starts believing Bitcoin and crypto perform well in inflationary environments, they can easily buy from dealers specializing in selling crypto to the rich. I’m talking about firms like Cumberland, NYDig, and OTC desks at U.S.-registered crypto exchanges such as Coinbase and Kraken.

My point is, despite widespread anxiety in the crypto market, whether the mass affluent class and below can own or trade Bitcoin or certain altcoins is actually irrelevant—they have no money, and the government isn’t sending checks anymore. Even if Robinhood still allows trading of certain coins, they lack surplus capital to buy. Meanwhile, the capital of the truly rich is abundant and globally accessible—thanks to numerous intermediaries serving wealthy Americans who faithfully do whatever they’re told, as long as the commissions are fat.

The Real Trade War

China and Japan hold more U.S. Treasuries than any other nations. This is because they both adopted the same economic model:

-

Undermining labor’s collective organizing power.

-

Undervaluing national currencies so productivity gains flow offshore as dollar-denominated revenues to entrepreneurs and the state.

-

An undervalued currency keeps goods cheap, allowing developed nations to continue outsourcing manufacturing to these countries.

This is the simple “Asian” economic model. Competition among major Asian exporters today is primarily price-based, largely determined by each country’s currency value. Thus, China and Japan care more about the CNY/JPY cross than their currencies’ value against the dollar.

So which country is currently more price-competitive?

I indexed the USD/CNY and USD/JPY exchange rates from January 1, 2009, to June 12, 2023, setting both at 100. As you can see, relative to this period, the yen has depreciated about 50% more than the yuan—but perhaps most notably, the gap between the two has widened significantly since the onset of COVID.

Below, I added CNY/KRW (China vs. South Korea, white) and CNY/EUR (China vs. mostly Germany, yellow) to illustrate the competitive landscape among global export powerhouses.

By this simple metric, Chinese goods are 3% cheaper than Korean ones, but 25% more expensive than German ones.

The yen’s sharp depreciation against the yuan makes perfect sense, as the Bank of Japan continues printing more money to keep Japanese government bond yields at targeted levels—a policy known as Yield Curve Control (YCC). Post-COVID, China hasn’t engaged in similarly large-scale money printing or credit expansion to artificially fix bond yields at specific levels. Therefore, the yen’s 46% depreciation against the yuan since 2009 is entirely logical.

Chinese goods are more expensive than Japanese goods. This affects export volumes, confirmed by recent data.

The main impact of China’s zero-COVID lockdowns began in summer 2022—we can see exports collapsing at that time in the chart above. Then China abruptly abandoned its zero-COVID policy and reopened. As people returned to work, exports surged again. This trajectory from depression to boom masks general weakness in global consumer demand and declining price competitiveness of Chinese goods.

This chart tells a similar story to exports.

China is now fully open, so there should be no lingering effects from 2022’s lockdowns. Yet exports are now declining year-on-year. That’s not good. And all this happens while the yen sharply depreciates against the yuan. If global markets are shrinking, China needs to be more competitive against its key export rivals to maintain stable growth and appease its population. Its top rival is Japan (remember, same economic model). The yuan must depreciate against the yen to help boost China’s growth.

The biggest reason the Chinese government needs economic growth is the massive unemployment problem. Specifically, urban youth unemployment exceeds 20%. High school and college graduates can’t find enough jobs.

For those unaware, graduating from university in China is a big deal because getting in is hard. Students take the so-called Gaokao exam. If your score isn’t high enough, you don’t get into university. There’s no rapper career path or anything like that. So from elementary school onward, children and parents pour all their energy into this exam. In such a populous country, how do you evaluate who to hire? HR relies on proxies like exam scores and university attendance.

For the past 40 years, parents who invested all effort and money into guiding their children through the education system were rewarded. University grads found better-paying jobs than factory work, moved families to cities, obtained hukou, and achieved class mobility.

But now, even after ruining their childhood with endless studying, you graduate and can’t find a job. China has a huge number of educated but disillusioned young people. For stability, this is a nightmare scenario. Authorities surely realize they must create jobs to bring youth back to work.

When in trouble, China resorts to export support and infrastructure projects to stimulate growth and employment. The supply-side economic measures that brought China this far may be repeated, even if it means adding more useless debt atop an already massive pile. This requires a weaker yuan.

To weaken the currency, the PBOC will encourage credit growth in “good” sectors of the economy. Loan rates in semiconductors, AI, clean energy, real estate, etc., will be lowered. Banks will be instructed to lend a certain amount of yuan to these sectors. Whether these businesses actually need the capital is irrelevant.

As credit expands, the currency will be allowed to depreciate. The PBOC might execute a shock devaluation, then gradually guide the yuan downward, slowly weakening it against the yen.

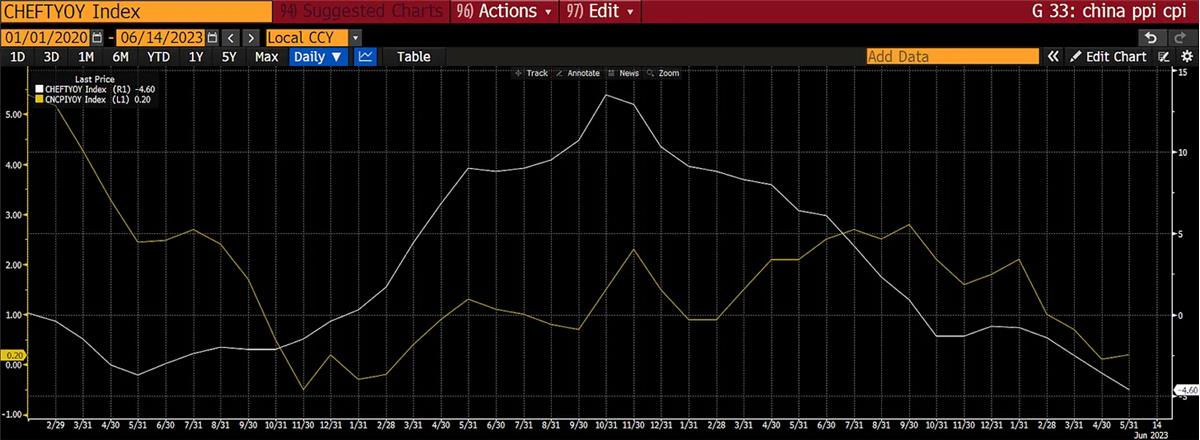

With both PPI and CPI in negative territory, the PBOC can ease policy without worrying about triggering inflation.

Since some high-quality firms don’t need this capital, it will “leak” into financial assets (just like U.S. stimulus checks to the affluent). Companies meant to produce parts end up taking loans and speculating in financial markets. Most importantly for this article, forward-looking wealthy Chinese may start moving capital out of China.

In the past, the PBOC might have worried about capital flight, but China’s holdings of Western fiat financial assets have become liabilities, not assets. This is because the West has shifted from ally to adversary. Who knows what might happen to Chinese capital within Western political circles? We could wake up one day to find portions of Chinese assets frozen due to disfavor in Western politics.

As you can see, China has about $3 trillion in “problematic” assets.

A better policy would be to allow the wealthy to purchase hard assets like crypto and ensure they’re stored under trustees owned or controlled by them within China. I’ve predicted before, and continue to believe, that Hong Kong will become the channel through which Chinese capital is permitted to hold crypto financial assets.

When I say financial assets, I mean ownership of financial returns derived from underlying crypto tokens or currencies, possibly achieved via funds or derivatives—because China doesn’t want its citizens holding technology that enables non-state-backed economic freedom. In this way, Chinese investors swap liabilities off the national balance sheet and replace them with Bitcoin and other cryptos. Overall, this strengthens China’s national financial position.

Here’s how I envision the process:

-

Hong Kong permits various asset managers to offer exchange-traded funds (ETFs) backed by cryptocurrencies. Let’s take a Bitcoin ETF as an example.

-

Wealthy Chinese investors somehow convert RMB into HKD. This can’t be too hard—otherwise Hong Kong’s real estate market wouldn’t be so active.

-

Chinese investors then buy one of the Bitcoin ETFs listed on the Hong Kong Stock Exchange.

-

The ETF manager buys physical Bitcoin from global markets and holds it with a licensed Hong Kong custodian.

-

The Chinese investor now owns an ETF—an instrument derivative to Bitcoin—but not physical Bitcoin itself. The investor participates only in Bitcoin’s price performance, not in holding the token.

This solves several problems for China:

-

Provides a hard-asset outlet for wealthy Chinese seeking to escape ongoing RMB depreciation. The rich feel smart and happy because their capital is “protected.”

-

The endpoint of this outlet is an institution bound by Hong Kong regulators’ rules—effectively meaning physical Bitcoin is under Chinese government control. This is no different from Bitcoin held in ETFs or trusts listed in the U.S., ultimately under U.S. government control. Same principle.

-

Reduces the amount of Western fiat assets held by China. When wealthy Chinese sell RMB and buy HKD, the PBOC buys RMB and sells HKD—essentially selling dollars due to HKD’s fixed peg to the USD. China can do this because it holds vast dollar reserves.

For crypto holders, this is a fantastic outcome. The return of Chinese crypto traders via Hong Kong’s financial pipeline will reignite the market, while the U.S. affluent class is effectively locked out. Every action by either country pushes the other to do more of the same.

China weakening its currency and allowing loyal comrades to buy Bitcoin derivatives—this simple act reduces the amount of Western fiat assets it holds. The less willing China is to use export earnings to buy U.S. Treasuries or hold dollar assets in any form, the harder the U.S. must work to ensure its citizens’ capital doesn’t leave Sharpe World—because the buyer of long-term debt—China—is no longer buying.

Trading Strategy

Due to ongoing confusion over what kind of crypto industry U.S. regulators want (if any), U.S. firms will stop offering or drastically scale back many crypto trading services. Many small-cap tokens will be delisted, and many U.S. financial intermediaries will dump small-cap tokens indiscriminately on public markets—anything that gives their compliance teams headaches.

Negative sentiment + forced selling = lower prices

Buy when others sell. Some of the dumped tokens are indeed worthless—for example, why does an L2 even need a token? That’s questionable… but actually, some tokens are building the tech needed for the AI economy.

Timing is crucial, and I can’t predict when large U.S.-facing crypto trading firms will stop serving Americans and/or liquidate their crypto holdings. So I must buy in batches and avoid leverage.

Last weekend was a perfect example. Someone had to sell a large amount of crypto quickly, regardless of market impact. Great—I bought tokens at excellent prices there. But next weekend’s prices might drop another 20%. My point is, I must have absolute conviction in the product and service value to keep buying through severe drawdowns.

Many crypto Twitter warriors might counter, “ARTHUR, the market is flat or down, yet you’re still fantasizing about a bull run.”

That’s a fair critique. But if my timing is off (which it almost certainly will be), I’ll slow my dollar-cost averaging and avoid leverage. I’m confident in my macro outlook, and things are unfolding as expected—albeit slower. For short-term traders, I agree my analysis is useless, as you’re plagued by false breakouts and corrections.

I don’t expect news flow to improve. Many future-betting companies targeting large pools of U.S. retail investors will fail. Any firm relying on trading fees for revenue will suffer. More well-known companies may exit the market due to blindness toward the coming future. When failure is all around you, it’s hard to imagine the beauty of the next bull market.

At some point, selling will stop, and we’ll enter a sideways phase. Boring price action will persist until something reignites speculative spirit among crypto traders. I propose one possibility—the sudden depreciation of the yuan against the yen. I’ll monitor CNY/JPY and China’s export data. The weaker China’s economic growth, the more credit will be issued. Then the currency will weaken, capital will be allowed to “escape” into suitable vehicles, and finally, the crypto capital market will receive the spark it needs—hopefully starting a rebound this fall.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News