Cryptocurrency Payment Applications

TechFlow Selected TechFlow Selected

Cryptocurrency Payment Applications

The most important cryptocurrency application has yet to be conceived.

By: Thejaswini M A

Translated by: Block Unicorn

Introduction

We’ve tried everything.

NFTs were supposed to attract creators. Web3 games promised to bring blockchain to the masses. Social protocols like Farcaster and Lens promised a decentralized future for digital communities. Zora aimed to prove content could become a financial asset. Friend.tech turned social capital into something truly tradable. Meme coins—well, no one claimed they were building civilization, but someone always said they’d bring the next wave of retail investors.

NFTs were originally intended to attract creative talent. Web3 games promised to bring blockchain to the mainstream. Social protocols such as Farcaster and Lens heralded a decentralized future for digital communities. Zora sought to demonstrate that content could become a financial asset. Friend.tech made social capital genuinely tradable. As for meme coins—while no one claimed they’d build civilizations, some always insisted they’d usher in the next wave of retail investors.

Then there are prediction markets. Polymarket may be the closest thing we’ve had to a true breakthrough so far—but its peak coincided with the U.S. election cycle. Now the open question is whether it can sustain user engagement when stakes shrink. And there’s an uncomfortable truth few admit publicly: the platform’s accuracy partly stems from users who possess real-world information trading on it—a tricky issue for both regulators and ordinary users.

So here we are in March 2026. Bitcoin is widely custodied by institutions (let’s set aside exact figures for now). Stablecoins were instantly standardized overnight by the GENIUS Act. Infrastructure is more mature than ever before. If you open the App Store and filter by “Finance,” the top-ranked crypto apps are Coinbase, Kraken, and Crypto.com—all exchanges. They’ve been operating for a decade. Truly breakthrough consumer applications remain absent.

Why?

Why Haven’t We Reached the Goal Yet?

Crypto evolves through violent bull-and-bear cycles. Most innovation only becomes visible during crashes. The public often associates cryptocurrency with chaos. When Bitcoin crashes, people say, “I told you so.” They don’t understand how it works—but we can’t blame them. After all, crypto’s signal-to-noise ratio is abysmal.

Cryptocurrency was never designed for the masses. Developers focused on their ideological path—decentralization, censorship resistance, and self-sovereignty—and expected the public to gradually come around. But the public never asked for these things. They want faster payments, higher savings yields, and easier cross-border remittances. Instead, crypto offers seed phrases, gas fees, and declarations of financial system disruption.

Meanwhile, the world beyond crypto has transformed dramatically. Artificial intelligence (AI) dominates the discourse. ChatGPT hit 100 million users in just two months. People who’d never heard of Transformers suddenly use AI daily. Crypto never experienced a similar explosion. A technology once touted as the next internet was ultimately overshadowed by something that actually *feels* like the next internet.

A trust crisis followed, while macroeconomic turbulence became the norm. Within crypto, recurring scandals continually validated skeptics’ concerns. Do Kwon and Terra Luna, Three Arrows Capital, Celsius, FTX—every few months, another “reputable” crypto firm is exposed for insolvency or misuse of customer funds. Regulatory responses—like Operation Chokepoint 2.0—and the SEC’s enforcement-only approach have only pushed legitimate projects offshore while leaving real fraudsters untouched, worsening the situation.

And critically: UX still falls short of consumer-grade standards.

Compare the UX of crypto social apps with Instagram: On Instagram, you download the app, register with your phone number, log in—and content appears instantly. It’s intuitive, effortless, requires zero learning.

Now compare Farcaster or Lens. First, you need a wallet. Write down a 12-word seed phrase on paper and store it securely. Lose your wallet, and everything vanishes forever—with no customer support to call. Then you need ETH to pay gas fees to create your profile. You must understand what gas is, why it fluctuates, and why the same action sometimes costs $5 and other times $50. Connect your wallet, approve transactions, sign messages you can’t decipher—and pray you don’t click a phishing site. Only after clearing all these hurdles can you begin using social features—features still missing algorithmic feeds, creation tools, and network effects—the very things that make Instagram compelling.

Or compare setting up a crypto wallet to opening Cash App: download, enter your phone number, link your bank account—done. Three steps, five minutes.

Crypto wallets? Choose among dozens of options (MetaMask, Phantom, Coinbase Wallet), download the wallet, generate a seed phrase, write it down, store it securely, grasp the difference between Layer 1 and Layer 2, fund it via crypto exchange (requiring KYC and bank transfers), then learn to manage gas fees, approve token allowances, and avoid scams.

For most people, this is an impenetrable wall.

Friction is enormous—but developers don’t feel it. The entire feedback loop—who builds, who tests, who gives feedback, who invests—is highly insular. When your test users all have MetaMask installed and understand gas fees, you won’t sense the friction blocking mainstream adoption. It’s like asking fish to notice water.

Graveyards are instructive. Cemeteries are illuminating.

Friend.tech attempted to financialize social relationships. Its business model: buy and sell “keys” granting access to private chats with crypto influencers. At its peak, the platform generated $90 million in volume, then plunged to $7.1 million daily—before developers abandoned it. The problem wasn’t technical—it was that no one actually wants their social graph turned into a financial instrument.

Farcaster raised $150 million from a16z to build decentralized social media. Its founder was formerly a Coinbase co-founder—genuinely technically capable. Daily active users briefly hit 100,000, then collapsed to 4,360. Monthly revenue fell to $10,000. The founder eventually left Farcaster to launch a stablecoin company. The issue? No one cares whether their “Twitter alternative” is truly decentralized.

During the pandemic, Axie Infinity built a full parallel economy in the Philippines. Players earned above-minimum-wage income breeding digital creatures. Later, the token economy collapsed—and everyone quit playing. The issue wasn’t gameplay—it was that nobody wants to play a game that feels like a job unless they desperately need money.

Who’s Actually Doing This Right Now?

The companies closest to genuine consumer success are financial platforms integrating crypto rails.

Coinbase

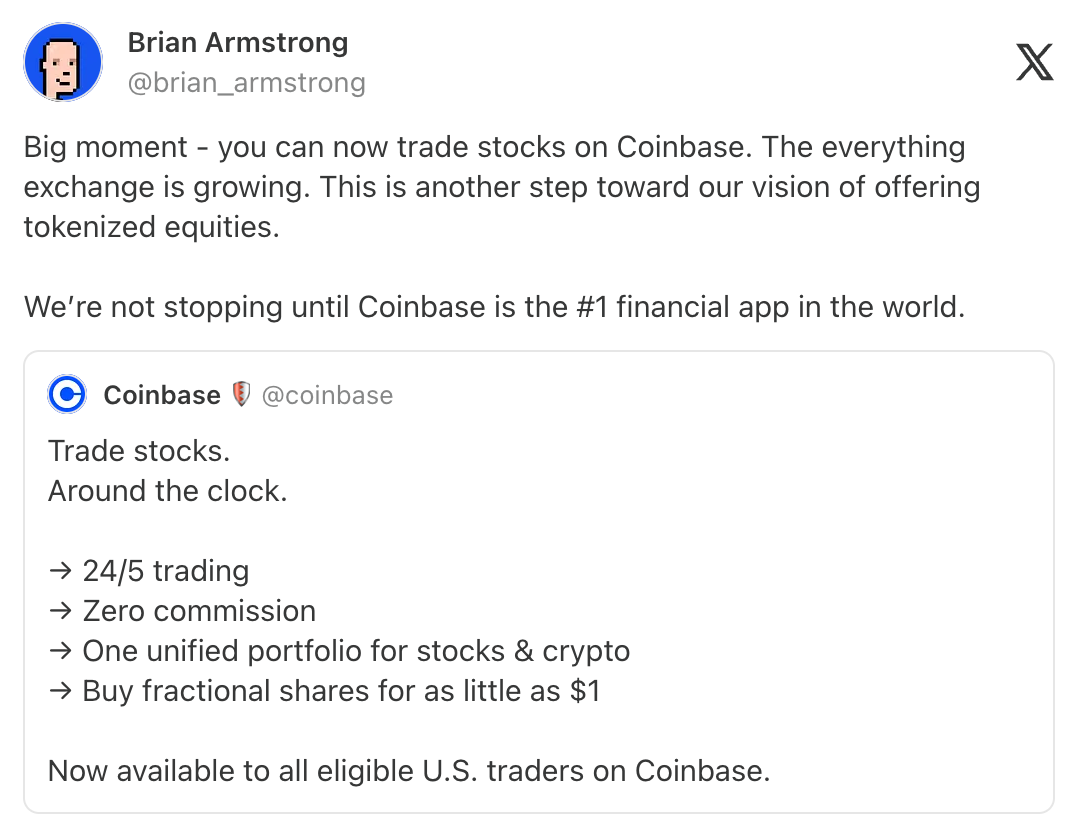

Coinbase is building what CEO Brian Armstrong calls the “everything exchange.” In his 2026 roadmap, this is listed as the company’s top priority—integrating crypto, stocks, prediction markets, and commodities across spot, futures, and options trading.

Their launched products:

Stock trading. Zero-commission stock trading. Five days a week, 24 hours a day—all within the same app where you trade crypto. Their messaging isn’t “Learn about blockchain”—it’s “Trade everything, in one place.”

Prediction markets integrated via Kalshi. Bet on elections, Fed decisions, and sports outcomes without leaving Coinbase. Crypto components are fully transparent.

Perpetual futures for international users. Lending supports borrowing up to $5 million against BTC collateral, and up to $1 million against ETH. Token primary sales will also launch, enabling retail users to purchase tokens pre-listing using USDC.

Brands can mint their own USDC-backed branded stablecoins. Stablecoin payments are embedded in Shopify; Checkout.com and PPRO go live in 2026. UK savings accounts offer 3.75% APY, protected by the FSCS. They’re applying for a national trust charter—granting broader banking authority.

Coinbase is building infrastructure to onboard everyone onto blockchain—not just its super-app for end users, but crucially, Rails backend support for institutions, fintechs, and traditional banks entering crypto.

Base hosts over $7 billion in onchain assets. cbBTC ranks as the second-largest asset, valued at ~$2.5 billion. Its integration with Morpho shows $2 billion in collateral backing over $1 billion in loans.

Robinhood

Robinhood is taking the opposite path: starting as a stock-trading app, it’s rapidly evolving into a full-stack crypto platform.

Features launched include: ETH and SOL staking for U.S. users; perpetual futures with up to 7x leverage for European users; over 1,000 tokenized stocks, U.S. equities, and ETFs for EU customers—traded 24/5, zero commission. Their Ethereum Layer-2 blockchain, “Robinhood Chain,” built on Arbitrum, is currently on testnet.

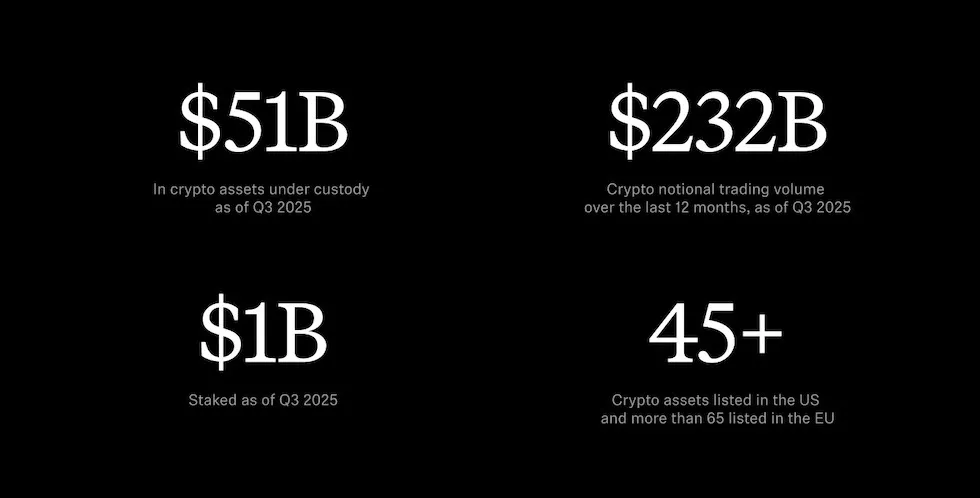

As of Q3 2025, custodied crypto assets totaled $51 billion. Nominal crypto trading volume over the past 12 months reached $232 billion. An AI assistant named Cortex delivers insights and market analysis for Gold members. A cashback credit card auto-converts rewards into crypto. Staking is positioned as the “core feature” and primary driver of user engagement in 2026.

They acquired Bitstamp to strengthen global crypto infrastructure. Expansion into Indonesia is underway. Robinhood Social—a platform where traders post actual trades and P&L—is under development.

They already possess neobank infrastructure—direct deposit, credit cards, cash management—and are layering crypto atop it.

Then there’s crypto enthusiasts’ favorite:

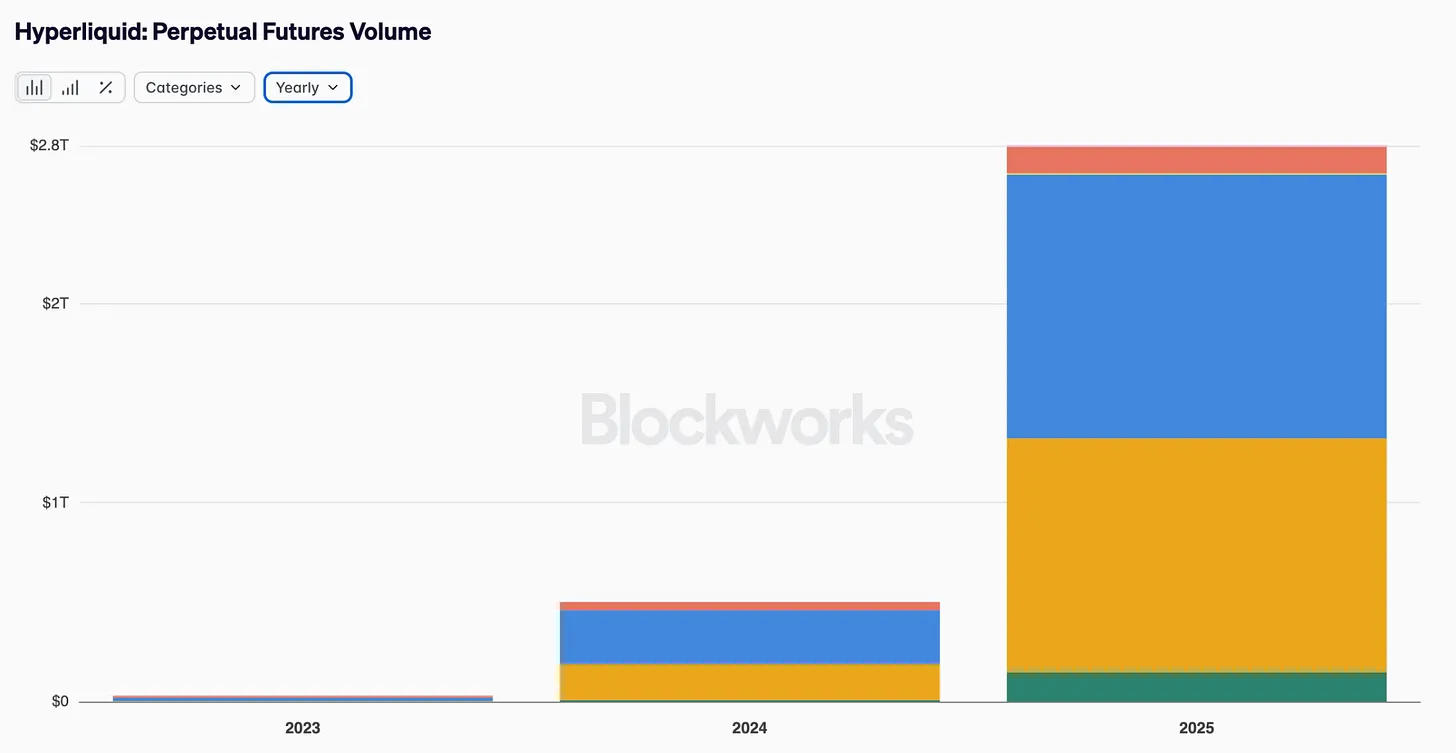

Hyperliquid processed $2.8 trillion in perpetual futures volume in 2025. The company cracked the Forbes Fintech 50 with zero funding. Arguably, this is crypto’s most successful consumer product case study.

But Hyperliquid isn’t a consumer-facing breakthrough technology—it’s a success *within* crypto. It serves users who already understand perpetual futures, leverage, and order-book dynamics. Its volume comes primarily from traders already active in crypto, seeking better execution. Hyperliquid simply provides existing users a superior trading venue.

What Are We Missing?

What should the ideal crypto consumer application actually look like? Not vague platitudes—specific details.

Invisible wallets. No seed phrases to worry about. Social recovery or biometric security. Progressive custody—simple and easy to start, scaling up security as balances grow. The tech exists: account abstraction, passkeys, smart contract wallets. But adoption remains slow because developers prioritize decentralization purity over UX.

Seamless fiat on/off ramps. Instant settlement. No waiting three to five business days for ACH transfers. No need to understand the difference between USDC and USDT. No minimum deposit requirements. Just link your bank account and transfer.

No jargon. “Send $50 to Sarah,” not “Enter recipient address and specify gas limit.” Natural-language interaction that understands user intent. Error recovery—letting you undo transactions or cancel pending actions.

Clean, intuitive interfaces—not spaceship control panels. One-tap operations for payments, swaps, yield checks, social features, etc. Gradually introduce crypto concepts to those who want to learn, while offering fully abstracted UIs for those who don’t.

A consumer-grade trust layer. AI-driven risk alerts warning “This looks like a scam” before you approve a transaction. Automated portfolio management optimizing DeFi yields. Seamless, automated tax reporting. The safeguards ordinary users expect from financial products.

Compliance baked in—but invisible to users. Selective disclosure lets you share specific balances without exposing your full wallet. Shielded transfers protect privacy when needed. Identity protection defaults to pseudonymity. Data sovereignty puts users in full control of personal information.

A strong narrative explaining *why this matters*—without requiring any belief system. Not “overthrow the financial system” or “be your own bank,” but “it does what you’re already doing—better.”

It shouldn’t feel like “using crypto”—it should feel like a better banking app.

The problem is that most crypto apps are built, tested, and funded by crypto insiders. When your test users all have MetaMask installed and fluency in gas fees, you won’t feel the friction blocking others.

Crypto solves problems most people in developed economies don’t have. Self-custody and censorship resistance are vital principles—but for those with functioning bank accounts and stable currencies, they’re abstract threats, not daily pain points. Crypto marketing emphasizes “You *should* want this because of its potential impact,” not “It delivers tangible benefits *right now*.” That argument doesn’t stand up against Venmo or Cash App.

What Have We Overlooked?

We assume crypto failed because it lacked flashy consumer apps. But look closer—its infrastructure is already highly mature.

Stablecoins work. They’re functional infrastructure moving real value across borders daily. Security has improved markedly. Smart contract audits are standard. Multisig wallets are widespread. Insurance protocols exist. The catastrophic hacks of 2021–2022 have declined sharply as the industry learned hard lessons.

DeFi exchanges are highly efficient. Protocols like Uniswap, Aave, and Compound process billions in volume with minimal downtime. Total value locked in DeFi exceeds $300 billion. Institutional investors are using these platforms to boost efficiency.

Institutions are adopting the tech. BlackRock launched tokenized money-market funds. JPMorgan processes blockchain-based repo trades. Traditional finance quietly uses crypto infrastructure where it outperforms legacy systems.

Liquidity is deeper than ever. Bid-ask spreads that plagued early DeFi have narrowed significantly. Arbitrage bots ensure price efficiency across venues. Professional market makers provide abundant liquidity.

Institutional users adopted crypto before retail—unusual, yet critical. If you believe AI represents the future, AI agents need stablecoins. They need programmable settlement systems. They need crypto infrastructure. Chris Dixon agrees: AI agents require programmable money—and traditional banks can’t supply it. As AI proliferates, crypto infrastructure becomes indispensable. So infrastructure may matter more than hype. The foundation is laid; what’s missing isn’t technology.

Crypto consumer apps will ultimately win—but only if they stop pretending to be crypto.

The winners won’t ask people to “use crypto.” Instead, they’ll solve real problems people already face—delivering demonstrably better solutions: higher savings yields, faster payments, lower remittance costs, portable identity, and true ownership.

Banking accounts will feel familiar. Interfaces will be intuitive. Behind the scenes, stablecoins settle, smart contracts execute, and blockchains confirm—none of which users need to think about.

Every generation builds tools it doesn’t yet fully understand. Those laying the transatlantic telegraph cable in 1858 thought they were merely building faster communication. They likely never imagined they were constructing the nervous system of the global economy.

We judge new infrastructure by the first things built on it—and those first things are almost always wrong. They’re just old ideas dressed in new tech: horseless carriages, moving pictures, electronic newspapers.

Real transformation comes later—when someone who grew up with the infrastructure builds something impossible without it. Something the original builders never imagined.

The apps built a decade from now will bear no resemblance to what we debate on crypto Twitter today. They won’t be incremental upgrades—they’ll be things we can’t yet describe in words.

Our job isn’t to build that thing. We can’t. Our job is to ensure the infrastructure is in place, working reliably, and usable by the people who’ll build on it tomorrow—people who won’t need to read whitepapers to get started.

Finance is our vehicle to reach that goal—because it puts essential tools in enough hands to empower the real builders—the ones we haven’t met yet.

That’s the strategy that actually works. Neither transformation nor surrender—we’re just perpetually distracted by irrelevant things.

The most important crypto application hasn’t even been conceived yet. And that’s my greatest optimism for this industry.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News