69,000 BTC for sale, risk-off sentiment surges—could Bitcoin drop to $70K?

TechFlow Selected TechFlow Selected

69,000 BTC for sale, risk-off sentiment surges—could Bitcoin drop to $70K?

Macro tensions escalate, selling pressure intensifies, and the market enters garbage time.

Author: Tuoluo Finance

The year 2025 has begun, but the market seems to have entered a period of "garbage time."

Even Bitcoin didn’t expect that $100,000 would become the benchmark for bull and bear markets. After briefly surpassing $100,000 on Monday—initially seen as the start of a new upward wave—BTC quickly lost momentum. During Tuesday’s U.S. trading session, it dropped to a low of $92,600, falling nearly 10% from Monday’s peak above $102,000. It is currently trading at $94,212.

While Bitcoin watched from the sidelines, altcoins surrendered completely. ETH fell back to $3,300, SOL dipped below $200, and the broader altcoin sector declined by around 10%, with institutional tokens like ADA, RNDR, and Aptos leading the losses. Even U.S. equities were affected—share prices of major mining firms such as TeraWulf, Bit Digital, Bitdeer, IREN, and Hut 8 dropped 5–8%.

Although the decline remains manageable so far, Bitcoin's recent lows have approached its pre-year levels, cooling off previously elevated market sentiment. The news about the potential sale of Silk Road-seized Bitcoin further chilled the market, sparking widespread speculation—even prompting some analysts to predict that Bitcoin could fall to $70,000 before Trump’s inauguration speech. For instance, analyst Ali Martinez stated that BTC’s key support zone currently lies between $97,041 and $93,806. He warned that if demand in this range fails to materialize, a sharp drop to $70,085 could follow.

To assess whether this prediction will come true, we must first analyze the causes behind this downturn.

The market widely attributes Tuesday’s sell-off to macroeconomic data releases. The U.S. Bureau of Labor Statistics reported that job openings under the JOLTS survey for November surged past 8 million, significantly exceeding expectations and topping estimates from all economists surveyed by media outlets—an unexpected six-month high. This surge was primarily driven by growth in business services, while labor demand across other industries showed mixed results.

In detail, U.S. job openings reached 8.098 million in November, compared to an expected 7.74 million and an upwardly revised 7.8 million in October (previously reported as 7.744 million). The November figure extended the rebound seen in October. Just two months earlier, in September, JOLTS job openings had unexpectedly plunged to a more than three-year low, triggering recession fears.

Released alongside JOLTS data was the U.S. ISM Services PMI. The index rose to 54.1 in December, surpassing both the forecast of 53.3 and the prior reading of 52.1. This increase was largely fueled by a significant jump in the prices paid sub-index, which soared from 58.2 in November to 64.4—the highest level since February 2023.

Overall, these macroeconomic figures can be described as strong—but ironically, their strength triggered market declines. The prevailing view is that robust data reinforces the likelihood of continued hawkishness from the Federal Reserve, necessitating a re-pricing of rate cut expectations. In simpler terms, better economic conditions reduce the urgency for monetary stimulus, inevitably tightening liquidity for risk assets. Following the data release, traders scaled back bets on a Fed rate cut before July, sending the S&P 500 and Nasdaq lower, while the U.S. 10-year Treasury yield and the dollar index spiked sharply.

Adding to this, the Fed released minutes from its December FOMC meeting today, echoing last month’s tone: rate cuts will proceed with greater caution. Committee members now anticipate a significantly slower pace of easing in 2025, projecting only 75 basis points of total rate cuts for the year.

Macro conditions form the critical backdrop, but Trump’s sensational statements have further amplified market risk aversion.

Yesterday, CNN reported that four sources revealed President-elect Trump is considering declaring a “national economic emergency,” which would legally justify imposing broad tariffs on allies and competitors alike. Once such a state is declared, Trump could invoke the International Emergency Economic Powers Act (IEEPA), granting him unilateral authority to regulate imports during national emergencies.

Earlier, on January 7, during a 70-minute press conference at Mar-a-Lago in Florida, Trump made several extreme remarks—claiming he would make Canada the 51st U.S. state “through economic means,” not ruling out using military force to seize the Panama Canal and Greenland, and vowing to rename the Gulf of Mexico as the “Gulf of America.” On Middle East issues, he warned that if Hamas does not release Israeli hostages before his inauguration, “the Middle East will descend into chaos.” These provocative comments sparked backlash from countries including Canada and Denmark and deepened global concerns over economic stability.

Given uncertainties surrounding interest rate cuts and trade policy, risk-off sentiment intensified. U.S. equity indices weakened amid volatility, the dollar index surged, and non-U.S. currencies tumbled. Naturally, the crypto market was not spared. Institutional capital flows reflected this shift: on January 8, U.S. spot Bitcoin ETFs recorded a net outflow of $583 million, while Ethereum spot ETFs saw a net outflow of $159 million—both indicating capital withdrawal.

Compounding the situation, DB News reported early this morning that, according to an official, the U.S. Department of Justice has approved the liquidation of 69,370 BTC seized in the Silk Road case, worth approximately $6.5 billion. This rumor isn’t baseless; as early as December 3, the U.S. government transferred nearly $2 billion worth of Silk Road-related Bitcoin (19,800 BTC) to Coinbase Prime—a move widely interpreted as preparation for eventual sales. Anticipated selling pressure heightened market anxiety, pushing BTC down over 1% in the short term and back below $94,000.

Despite ongoing panic, there are reasons for cautious optimism. With less than ten days until Trump’s formal swearing-in and inaugural address, and with February being earnings season, positive outlooks still outweigh negatives. Moreover, favorable developments continue to emerge.

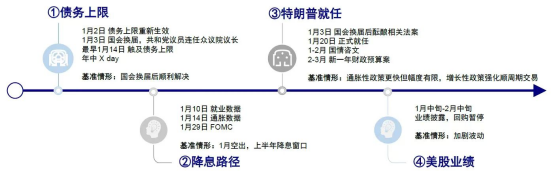

Key trading themes and milestones for 2025. Image source: CICC

First, the legal battle between Coinbase and the SEC may be turning in favor of the exchange. The U.S. District Court for the Southern District of New York granted Coinbase’s motion for interlocutory appeal, allowing it to appeal SEC charges directly to the Second Circuit Court. Pending review, the case is temporarily paused. The judge cited inconsistencies in how different courts have ruled on cryptocurrency legality, underscoring the need for higher-level clarification. If the Second Circuit agrees to hear the case, it could resolve a pivotal legal question: the SEC’s statutory authority over digital assets. Notably, because this is an appeal mid-litigation, it increases the chance of dismissal, potentially placing the SEC in a difficult position. A successful appeal might also clarify the securities status of coins listed on Coinbase, paving the way for altcoin ETF approvals.

Second, the chair of the CFTC—the agency once vying to become the top crypto regulator—has resigned. However, in his final public speech, he expressed positive sentiments toward crypto regulation. Trump’s team is already identifying crypto-friendly candidates for the successor, including current CFTC commissioner Summer Mersinger, a16z crypto policy head and former CFTC commissioner Brian Quintenz, and Kraken’s chief legal officer Marco Santori. Clearly, there is strong consensus within Trump’s circle about loosening crypto regulations.

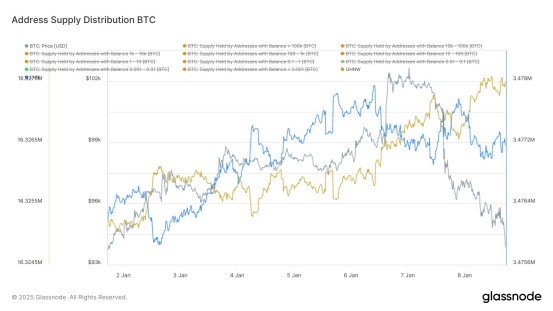

Against this backdrop, whales’ attitudes toward Bitcoin’s future price trajectory remain notably bullish, with bargain-hunting and bottom-fishing becoming common whale strategies.

Data compiled by @Phyrex_Ni shows clear divergence in investor behavior: small holders exhibited obvious signs of panic, with those holding less than 10 BTC showing clear trends of selling during the recent dip, and exchange balances continuing to decline. In contrast, large holders remained confident, with investors holding more than 10 BTC showing evident accumulation patterns.

Cauê Oliveira, research director at Blocktrends, confirmed this trend. He noted that institutional investors sold large amounts of Bitcoin at the end of 2024, but have recently resumed buying at prices below $100,000. In the week following December 21, wallets holding 1,000–10,000 BTC offloaded 79,000 BTC. Recently, however, this group began accumulating again when prices fell below $95,000.

As for the Silk Road liquidation causing panic, its actual impact may be smaller than expected. First, Trump has publicly pledged not to sell any Bitcoin held by the U.S. government after taking office—making any forced sale politically awkward and likely subject to reversal. Even if the sale proceeds, the process won’t happen overnight and could take months of administrative approval. Second, large-scale disposals are typically conducted via OTC deals to maximize returns and minimize market disruption. Third, even if dumped all at once, given current market liquidity, absorption would likely take no more than a week or so—hardly enough to trigger systemic panic. Ki Young Ju, CEO of CryptoQuant, remarked: “Based on realized market cap, around $379 billion flowed into the market last year—about $1 billion per day in liquidity. The $6.5 billion in Bitcoin the U.S. government plans to sell could be absorbed within a week.”

Hence, some institutions remain highly optimistic, viewing the pullback caused by selling pressure as a buying opportunity. Arthur Hayes, co-founder of BitMEX, commented on the Silk Road development: “Diamond hands are ready to buy the dip.”

Overall, while sentiment has cooled and fear persists, the presence of institutional and whale accumulation makes a full-blown crash unlikely. Bitcoin’s current consolidation zone remains around $95,000, with prices fluctuating near this level. A deeper correction might push it below $90,000, but a drop to $70,000–$80,000 appears improbable.

Beyond monitoring Trump’s policy moves, the next key event for markets is Friday night’s release of the U.S. December Nonfarm Payrolls report. Although Wednesday’s ADP “payroll precursor” came in below expectations—offering slight relief—actual NFP data often diverges significantly from ADP. As one of the Fed’s key decision-making indicators, it remains a focal point. Weaker-than-expected employment data could prompt the Fed to turn dovish again.

Currently, markets broadly expect U.S. nonfarm payroll growth in December to slow to 153,000, with the unemployment rate holding steady at 4.2%.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News