Web3 Growth Landscape in 2024: The industry stands on the brink of transformation, with over 100 startups having raised more than $1 billion

TechFlow Selected TechFlow Selected

Web3 Growth Landscape in 2024: The industry stands on the brink of transformation, with over 100 startups having raised more than $1 billion

The Web3 growth sector stands on the brink of transformation, driven by innovation and the willingness to explore uncharted territories.

Author: SAFARY

Translation: TechFlow

Web3 Growth Landscape: Interactive Map and Database

Key Insights

-

101 Web3 growth and social startups have raised over $1 billion¹

-

Since last year, 23 startups have secured $277 million in new funding

-

Few new first-time raises; VCs are doubling down on proven winners

-

Attribution/Analytics, Loyalty, and Social startups received the most new funding, accounting for 80% of total capital raised across all 10 categories

-

Messaging is the second-most funded category with $245 million, trailing only Social & Publishers ($400 million), but received just $7 million in new funding

-

Ad networks and community tools are the most crowded categories with 19 teams each, followed by messaging and loyalty with 18 teams each

-

The loyalty category has shrunk dramatically from over 40 teams in 2023 to 18 surviving teams today

-

The breakout 2023 category "Referrals & Advocacy" declined from 17 to 9 teams, with the two best-funded players having shut down

¹ Note: Not all of these fundraises were public—over 10 teams privately shared their funding details with us for inclusion in this report.

Introduction

-

You might be right about where things are headed over the next decade, but if you're early by a couple of years, you still won't make it. This is the story of those first two years.

The Web3 growth ecosystem seems inevitable—Web3 companies need deep user insights, strong engagement, and effective new user acquisition. Today, more than 160 companies are building the future of this emerging digital media industry, with 101 startups collectively raising nearly $1 billion.

This report dives into this rapidly evolving sector, providing a comprehensive overview of the most promising Web3 growth companies. It includes both publicly announced and privately shared funding data, offering a detailed snapshot of the industry today.

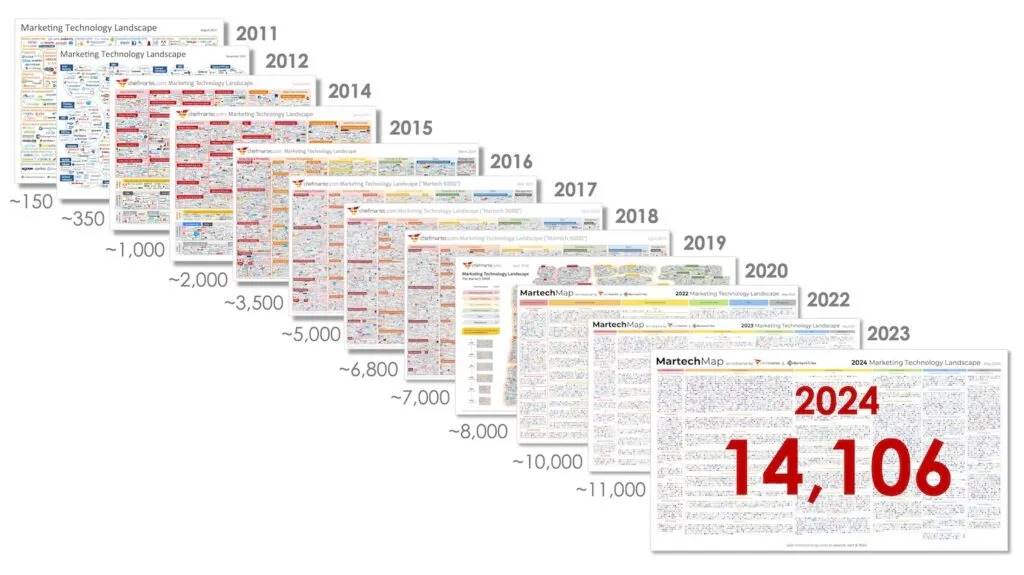

In many ways, the Web3 growth industry parallels the rise and fall of digital marketing in the 2010s. The MarTech space exploded from around 150 companies in 2011 to over 14,000 by 2024.

Chief MarTech’s 2024 Marketing Technology Landscape (Source)

But as the 2020s began, privacy regulations like GDPR and CCPA disrupted this carefully constructed ecosystem. It was in this era that Web3 emerged with a marketing environment more focused on community and privacy. Consumers started interacting on “dark social” channels like Discord, Telegram, and Reddit—platforms notoriously difficult to track. Suddenly, marketers could no longer rely on traditional targeting methods, prompting a wave of new companies aiming to rebuild our digital media landscape.

The first two years of this new digital media industry have been challenging. Most companies have struggled, with over half failing to survive. We’ll examine why certain categories failed to gain traction and what we expect in the 2024–2025 cycle.

This report builds on lessons from last year’s analysis, highlighting the ongoing evolution of the Web3 growth ecosystem and the innovative companies driving it forward.

About Safary

Safary is the home of Web3 growth leaders. Our platform enables top teams to unlock deep user insights and build more direct relationships with users; our community provides the knowledge and network needed to succeed.

We proudly help elevate the Web3 growth ecosystem by connecting the best growth leaders in crypto and sharing their insights with the broader industry.

Category Insights

This market map includes 160+ teams building Web3 growth and social platforms—from quests to analytics, attribution, CRM, loyalty, publishers, and more

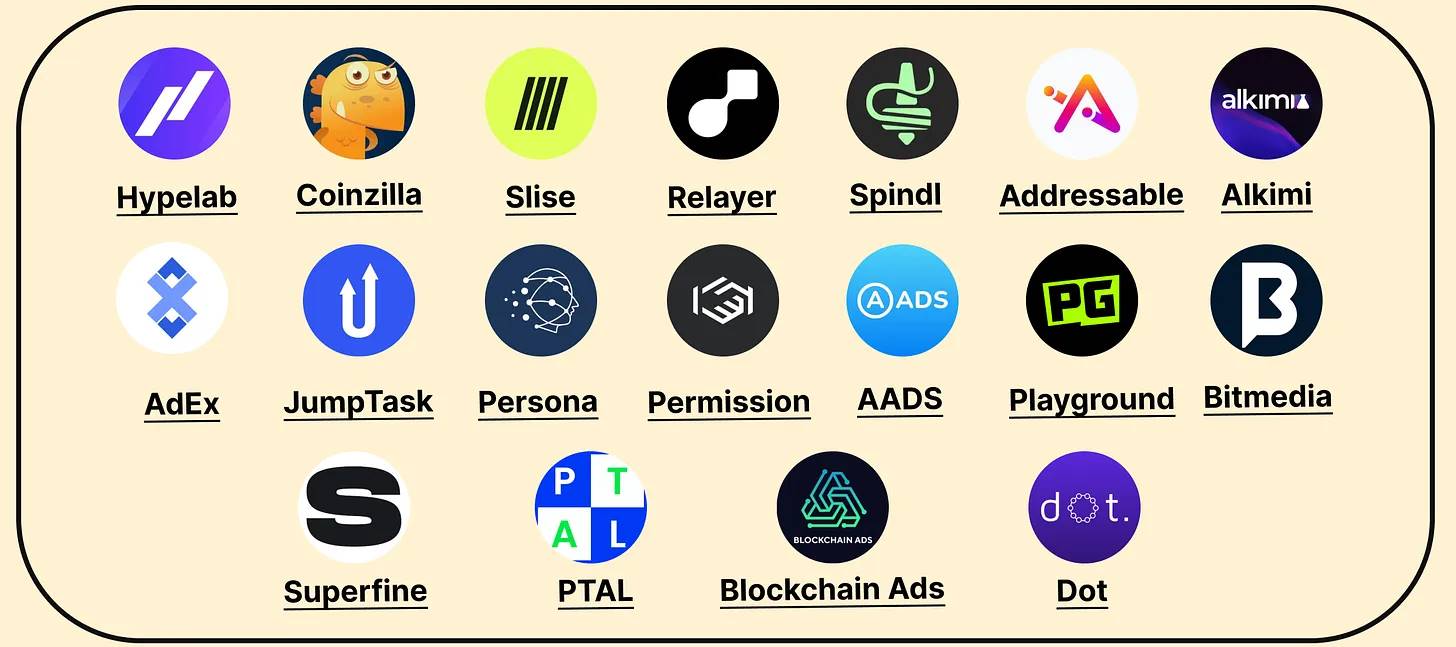

Ad Networks

Note: Each category is divided into: Definition → Challenges → Opportunities

Ad networks connect publishers and advertisers, streamlining the ad buying process. They aggregate ad inventory from multiple publishers, offering advertisers a single platform for ad placement.

There are currently 19 ad networks, with 9 having raised a total of $51 million:

While Web3 ad networks hold significant potential, they face tough challenges navigating competition and acquiring premium publishers:

-

Competition for publishers and advertisers

Although we’re still in the early stages, competition will be fierce. New entrants like Relayer and Spindl are entering the market, competing with category leaders such as Coinzilla and Hypelab.

New networks must solve the classic marketplace dilemma—creating demand (offering advertisers low-cost conversions) and securing supply (paying publishers more for ad inventory).

To compete, they may offer guarantees to publishers and attract advertisers through cost-per-action (CPA) models, where payment occurs only when a user completes a desired conversion event.

Advertisers love CPA models because they guarantee results, but publishers dislike them—they’d rather be paid for traffic generated, not based on users who convert downstream. This forces new ad networks to bear all the risk, and the longer it takes to build the marketplace, the faster their capital depletes.

While this is a difficult position for new ad networks, increased competition is good news for early-adopter publishers and advertisers using this channel!

-

Unlocking premium publishers

In Web2, publishers rely on ads as a primary revenue source, making the value exchange simple—revenue for attention. However, leading Web3 publishers (e.g., wallets, OpenSea, Uniswap) have alternative revenue models and are often skeptical of ads. Category winners will need compelling value propositions to shift this mindset.

These challenges present a unique opportunity—to make the CPA model work for publishers, which would be unique to Web3, even if still theoretical for now.

Imagine your favorite crypto media site, like Blockworks or Messari, publishing news and research on trading data. If they require wallet login, they could embed a Frame-like widget allowing you to buy the token you’re reading about without leaving the article.

This setup could incentivize publishers to share risk since conversions happen directly on their site. It also benefits advertisers—especially in DeFi—who may not need users to visit their own website to generate revenue.

In this arrangement, the publisher provides ad space, the ad network supplies embedded ad units, decentralized exchanges (DEXs) provide trading, and all three earn a revenue share from generated volume.

This model could extend beyond media sites to any wallet-aware channel—Discord, Telegram, or other dapps with large user bases!

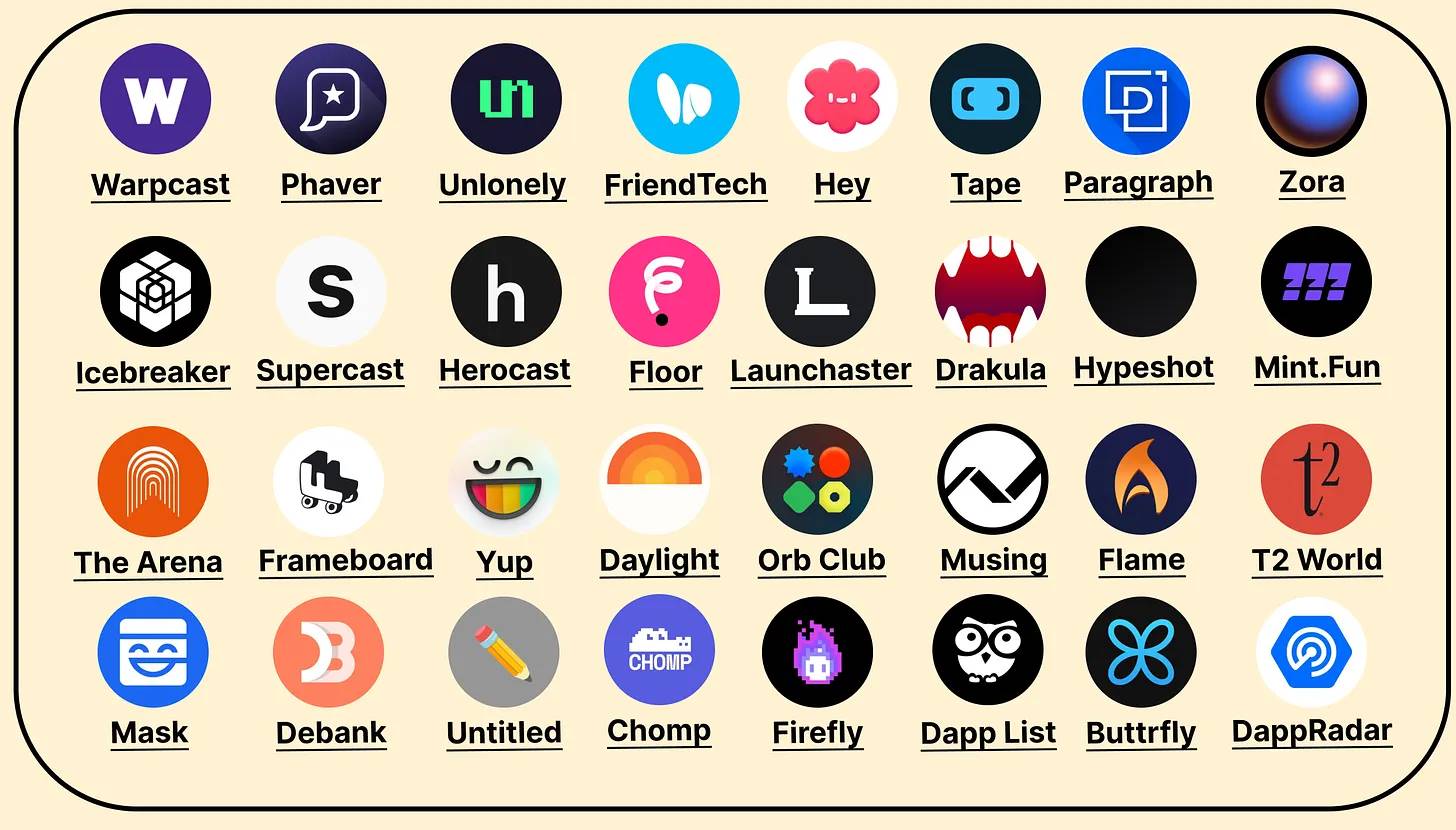

Publishers & Social

Note: Each category is divided into: Definition → Challenges → Opportunities

Publishers and social platforms aggregate Web3 creators and domain-specific information.

This category includes 32 platforms: 20 social platforms (11 raised $375 million) and 12 publishers (8 raised $25 million), totaling $400 million in funding—including $180 million in new funding:

Web3 social faces user retention issues

New social apps struggle to convince users they’ll endure long enough to make building a presence worthwhile. While tokens helped attract crypto-natives and bootstrap networks, long-term retention depends on delivering real value beyond pure speculation.

These platforms have the potential to become the largest crypto publishers (see Ad Networks section on aligned incentives)

If they can create novel, differentiated online interactions, they may become central hubs for on-chain communities. This would mark a shift from platforms like Twitter, where on-chain natives interact through gaming, streaming, and social apps. Wherever users gather, growth opportunities emerge—not just for crypto-native apps, but for the entire ecosystem’s expansion.

Attribution & Analytics

Note: Each category is divided into: Definition → Challenges → Opportunities

Attribution and analytics platforms aggregate on-chain, in-app, and social data to deliver detailed insights into user profiles and consumer behavior.

There are currently 14 attribution and analytics companies, having raised $70 million total—including $25 million in new funding:

Despite their potential, on-chain analytics and attribution platforms face hurdles in realizing their full value:

-

On-chain analytics alone, while interesting, aren’t actionable enough for growth leaders

In Wave 1 (2022–2023), generalized Web3 growth analytics saw limited demand—many pivots proved this. Helika shifted to attribution and focused on gaming, Persona became an ad network, Convrt moved to B2B CRM, Raleon exited Web3 for AI, and others struggled to gain traction.

-

Multi-channel acquisition and performance marketing remain underdeveloped

For attribution to be effective in crypto marketing, companies need to run multi-channel strategies (e.g., Twitter, blogs, ads, referrals, quests). But most don’t operate this way. Instead, they jump from one channel to another—one month doing quests, next month running referral campaigns, then ad pushes—efforts rarely overlapping. This makes cross-channel comparison difficult and limits attribution effectiveness.

-

The Web3 growth capabilities we’ve long envisioned are finally arriving

Teams can now build rich user profiles by combining first-party data with on-chain identity, social graphs, and wallet analytics. Top teams are building direct user relationships—no more tracking blind hopes of users returning. Creating a unified customer data layer for a 360° view of on-chain users is becoming standard.

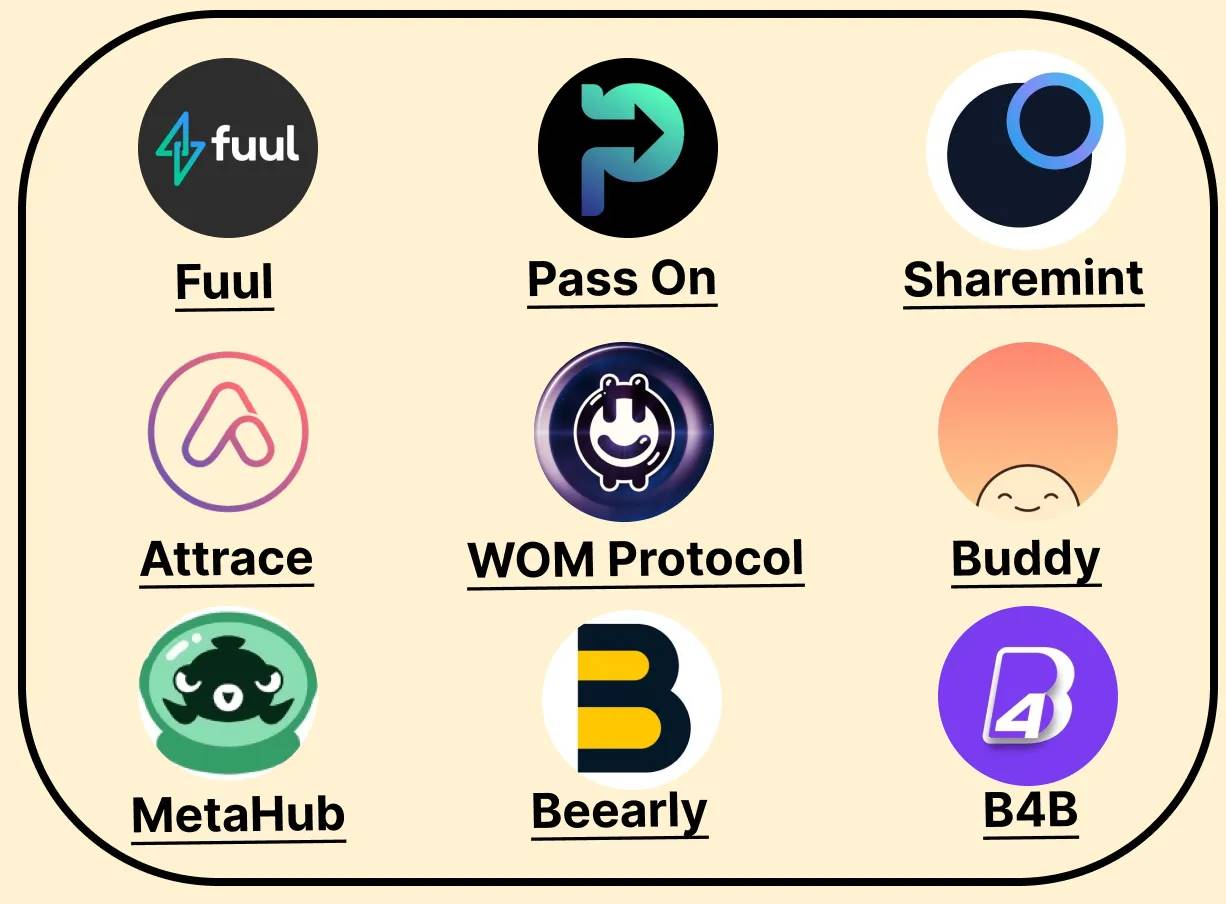

Affiliate & Referral

Note: Each category is divided into: Definition → Challenges → Opportunities

Affiliate and referral platforms streamline the discovery, tracking, and rewarding of B2B partners and B2C advocates. While new Web3 products often use waitlists to drive referrals, “referrals” typically refer to active users who actively recommend friends.

There are currently 9 affiliate and referral companies, with 5 having raised ~$7 million—about half of last year’s total:

Once the fastest-growing category in 2023, affiliate and referral platforms have seen significant consolidation. The two best-funded players, Chainvine and Qwestive, ceased operations in 2023 and returned funds. We believe Web3 referral platforms face several key challenges:

-

Referrals require an established and growing user base to work effectively

Referrals can bring the highest-quality users, but they depend on having an initial user base to fuel further growth.

For example, assume a current user base of 500 real users (common for many DApps):

-

Typically, 2% to 30% of users may refer friends. At a 15% referral rate, 75 of these 500 users might make referrals.

-

If each referrer brings 3 friends and 30% convert, that generates 68 new users.

-

Web3 referrals are not a “set it and forget it” channel

While gaining 68 new users (+13%) from an initial referral campaign may make an impact, maintaining momentum presents challenges.

If you acquire 100 new users monthly, referrals may add only 13 users—making it hard to justify even modest platform costs. To keep the program engaging, you must constantly innovate, which from a platform perspective means frequently adjusting client programs—limiting scalability.

-

Rewards are often insufficient for Web3 users

The promise of Web3 referrals is that referrers can earn more by sharing protocol revenue. For example, referrers might earn 25% of referred users’ trading fees or volume-based payouts.

In practice, most referral rewards are disappointing—often below their Web2 counterparts. For instance, Hashflow (a DEX) launched a referral program offering 1 ARB ($0.80) per $1,000 traded by the referred user. If your friend trades $10,000 on Hashflow, you earn just $8. No wonder people still cite GMX’s successful April 2022 referral program.

This isn’t to say Web3 referral platforms can’t succeed—but at current crypto scale, they face significant hurdles. DApps need thousands of new users monthly to generate enough volume to justify investing in referrals as a growth channel.

Like any incentive program, success depends on targeting the right user segments and offering meaningful rewards to drive action. Instead of using referral programs as broad user acquisition tactics with small rewards, focus on high-value users of the protocol and offer more substantial incentives. These users are more likely to bring similarly valuable users, enhancing the overall quality and impact of the program.

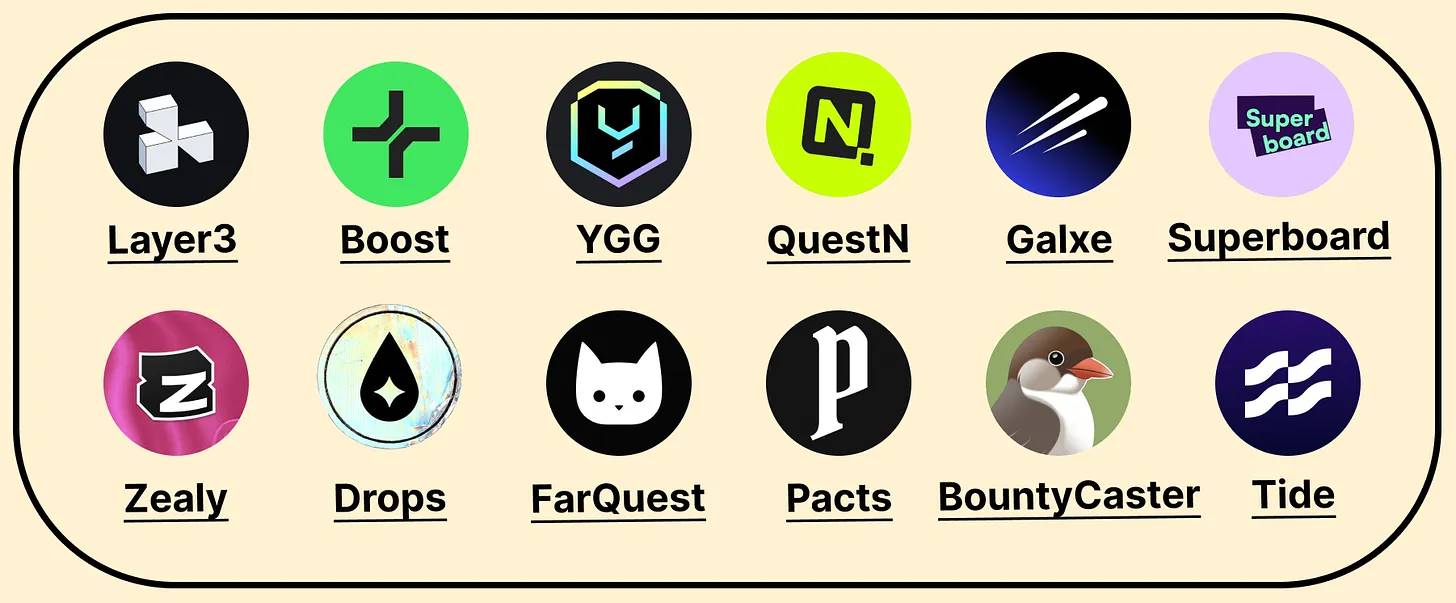

Quests

Note: Each category is divided into: Definition → Challenges → Opportunities

Quest platforms act as engagement marketplaces, connecting networks of Web3 users with company incentives to complete specific actions.

There are currently 12 quest platforms (down from 18 in 2023), with 9 having raised $103 million—including $15 million in new funding driven by Layer3’s Series A:

Quests once boosted metrics effectively via airdrops and social follows, but these tactics are falling out of favor as the market matures.

These strategies worked well for short-term engagement and rapid user acquisition. But the industry now prioritizes authentic user participation and lasting communities. This shift reflects a growing emphasis on long-term value and genuine engagement, pushing quest platforms to rebrand and evolve.

Historically, quest platforms were tied to points metaverses, where users earned points primarily by completing tasks, often aiming for airdrops. As airdrop farming loses effectiveness, reliance on points alone can no longer sustain user interest or platform growth. The current challenge is moving beyond superficial engagement to offer real value—giving users reasons to return not just for points or potential airdrops, but because they find the experience genuinely valuable.

Quest platforms will evolve into experimentation platforms for incentives

Old becomes new again—quests are shifting from simple “click and claim” tasks to ongoing, dynamic engagement, bridging traditional loyalty programs with on-chain actions. Successful platforms will continuously innovate on “do X, get Y” mechanics. They’ll need to design new formats, build supporting features, roll them out to teams, and immediately start the next project. Essentially, they’ll become experimentation platforms—Web3 is too dynamic to stay static.

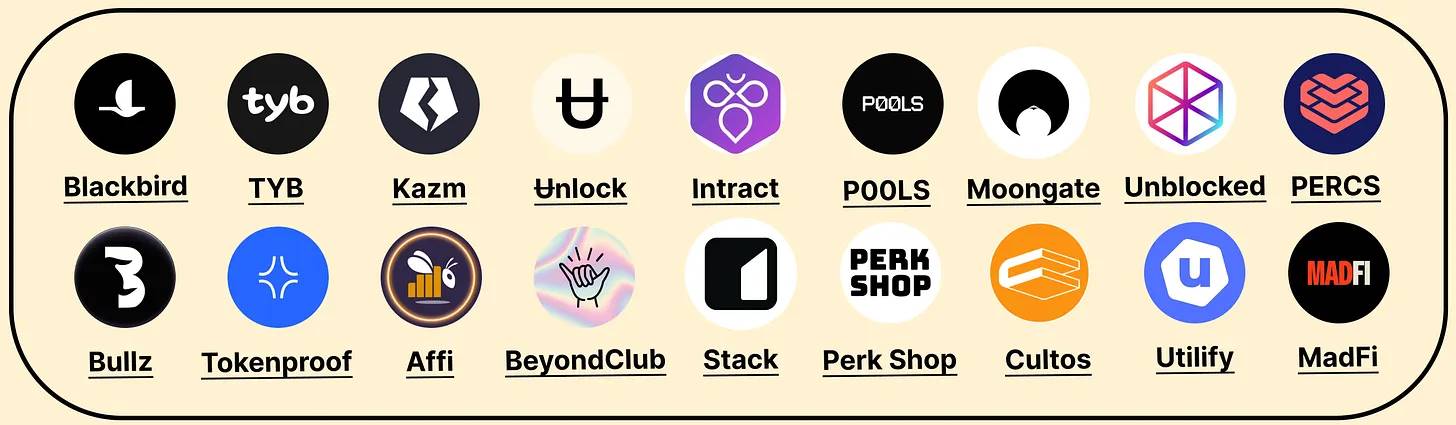

Loyalty

Loyalty programs increase customer satisfaction through rewards like discounts, access, and experiences, while driving repeat purchases and long-term retention.

There are currently 18 loyalty platforms (down from over 40 in 2023). Of these, 12 have raised $88 million, with $30 million in new funding—primarily due to Blackbird’s $24 million Series A:

Most Web2 brands abandoned crypto in 2023—and with them, growth

Many loyalty platforms either shut down or pivoted to non-crypto businesses, unsurprising given the category’s Web2 focus. These companies found it easier to adapt their product without changing target customers. Interestingly, most shifts occurred in the past 6–9 months, not during the early bear market.

Notable exits include Co:Create (raised $25M) and Hang (raised $16M). These pivots make sense—rather than chasing Web2 brands for innovative experiences, many chose to leverage their tech to build consumer experiences, potentially shifting to B2B infrastructure later.

With rising data privacy regulations and the emergence of omnichannel consumer experiences (online, offline, and on-chain), demand grows for a unified data layer—uniquely enabled by blockchain technology

Clearly, everything will become transactional—though not necessarily monetary. As on-chain data is generated, brands will securely access increasingly rich user profiles. These profiles will combine on-chain social behaviors and transactions with first-party online and offline data, creating the ultimate data vault for major brands. This data will enable highly targeted audiences, driving repeat purchases and long-term loyalty.

Community Tools

Community platforms offer tools to manage communities, track engagement, and provide analytics to enhance collaboration, member retention, content creation, and growth.

There are currently 19 community tool companies, with 10 having raised $87 million:

Challenges facing communities lacking a business model and difficulty measuring revenue impact

Community tool companies face major obstacles, mainly two issues. First, many communities lack sustainable business models, making investment in professional tools difficult. Second, it's hard to measure how communities directly contribute to revenue. While communities can boost brand loyalty and advocacy, translating these benefits into clear financial outcomes remains complex. These challenges make it difficult for community tool companies to prove their value and grow in the market.

Reimagining communities: From long-term, full-funnel engagement to deep, short-term group experiences

Web3 community tool companies have the opportunity to redefine what a community means. Rather than focusing on traditional large-scale communities, they can leverage blockchain technology to create dynamic on-chain group chats and short-term experiences with integrated financial transactions. This approach allows for meaningful and measurable outcomes without requiring a full-funnel journey. By prioritizing value-driven, interactive, and financially integrated communities, Web3 tool companies can explore new models of engagement and growth, paving the way for transformative changes in the digital landscape.

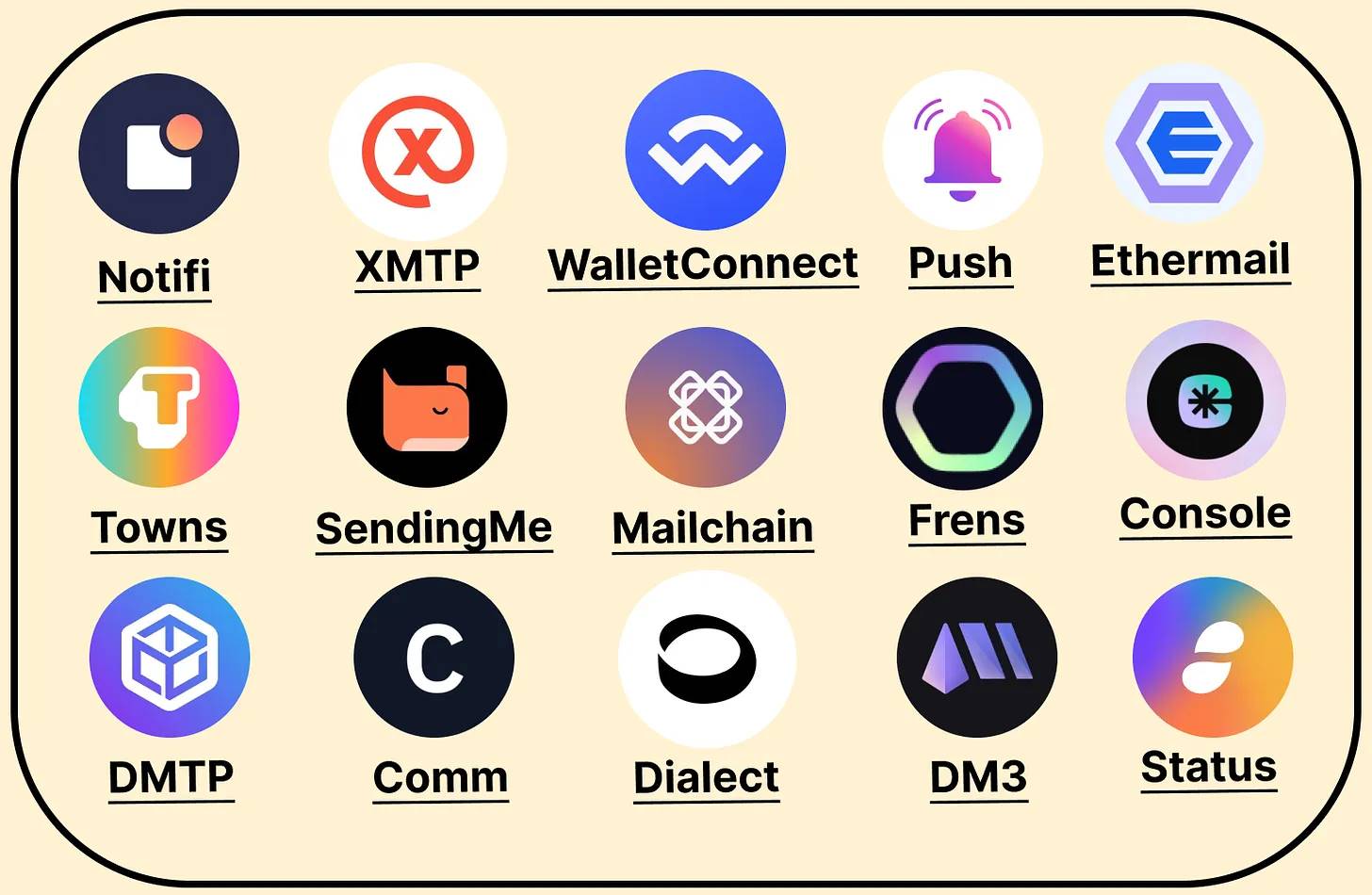

Messaging

Web3 messaging platforms are protocol-level communication networks enabling cross-chain messages and notifications between dapps, wallets, services, and on-chain communities.

There are currently 15 messaging platforms (down from 24 in 2023), with 11 having raised $240 million—but only $7.5 million in new funding from Sending Labs’ February extension:

Messaging to wallets is ineffective unless messages reach where users actually go

Web3 messaging platforms face a dilemma: messages sent to wallets are meaningless if users never see them. Unlike traditional messaging apps that centralize communication in user-friendly interfaces, many Web3 messaging protocols lack a reliable destination where users consistently check messages. This gap means that even when messages are sent, they’re often ignored—undermining communication effectiveness. For success, Web3 messaging platforms must create or integrate with ecosystems where users actively engage, ensuring messages are seen and acted upon.

Web3 social apps may become the messaging layer for wallets

None of the existing messaging platforms may ultimately succeed. Instead, Web3 social apps with integrated messaging layers—like Farcaster, Lens, and DeBank—may take the lead. These platforms allow messages to be sent to wallets within spaces where on-chain users already spend time, making communication more effective and relevant.

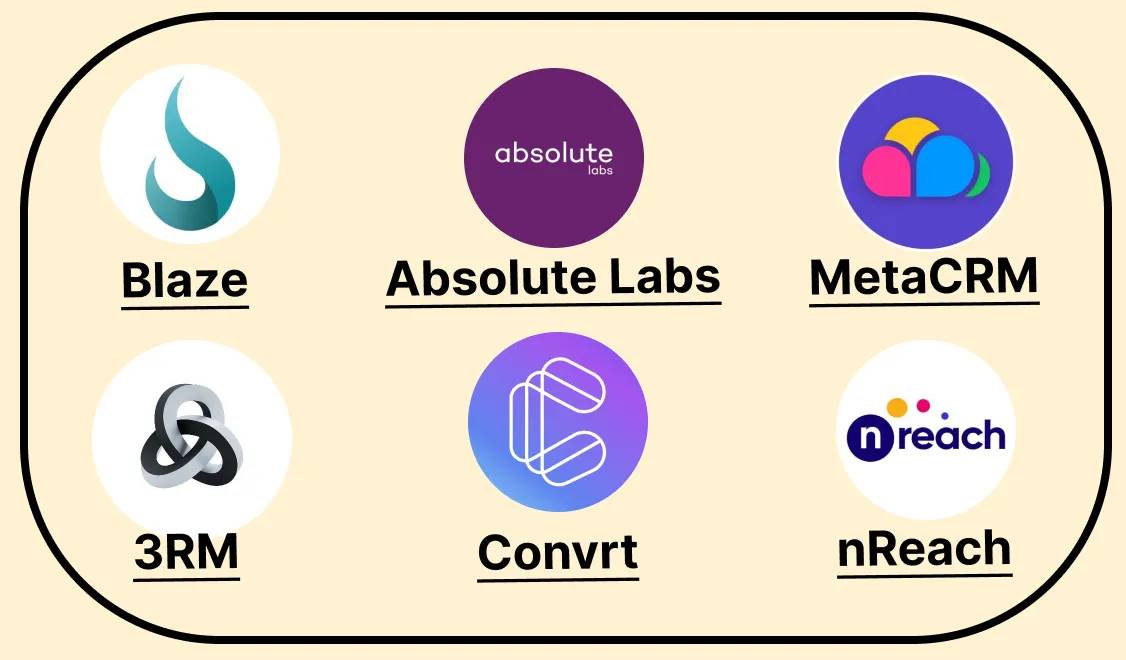

CRM & Go-to-Market Strategy

Web3 Customer Relationship Management (CRM) systems help teams manage and analyze customer interactions, primarily using on-chain data to create personalized, targeted marketing campaigns.

There are currently 6 CRMs (down from 20 in 2023), with total funding of $24 million:

On-chain data alone is insufficient for B2C CRMs to thrive

All Web3 CRMs initially targeted B2C companies (except 3RM), aiming to help them understand their on-chain holders and community members. However, it’s clear that this type of data is in greater demand within the B2B space.

The crypto ecosystem is primarily composed of B2B companies, presenting a larger and underserved market for Web3 CRMs

B2B companies urgently need on-chain data to qualify target companies, while also leveraging unconventional Web2 channels (e.g., Twitter, Telegram) to reach them. This shift presents a significant opportunity for Web3 CRMs to serve a historically overlooked market.

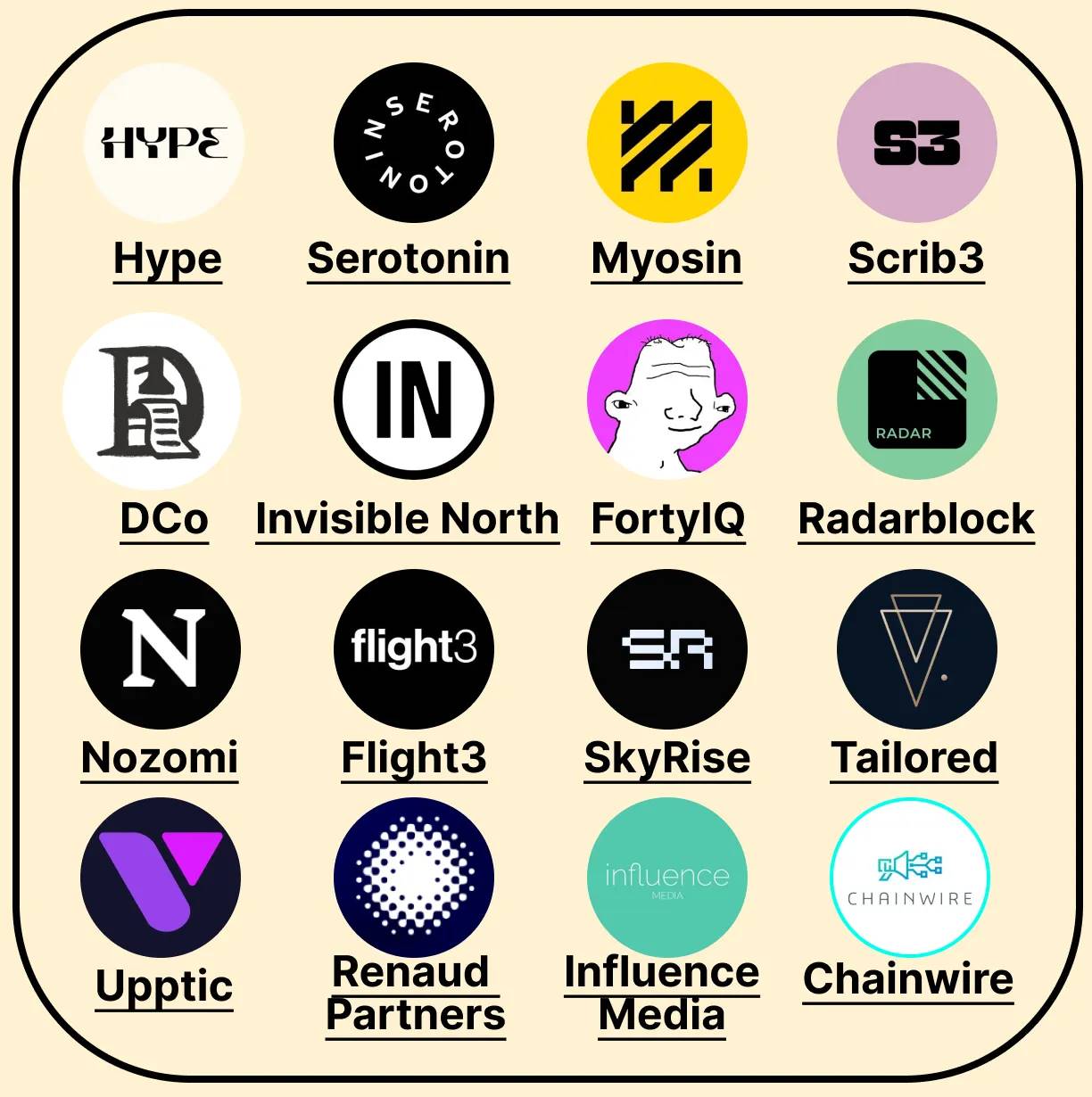

Marketing Agencies

Web3 growth agencies provide strategic guidance and deploy growth strategies for blockchain projects.

There are currently 15 marketing agencies (down from 32 in 2023), all self-funded:

Selling marketing services to tech teams that don’t believe in marketing is challenging

The agency market has become increasingly active, with many new entrants. A wave of small agencies has entered, as many experienced growth leaders transitioned into consulting after layoffs. Yet, many of these consultants struggle to sustain their businesses after six months. If in-house marketers find it hard to keep jobs, independent consultants face an even tougher case externally.

Still, early-stage teams clearly need growth support—especially those requiring non-technical expertise to gain competitive advantage in a saturated market. While large budgets for mature projects from the last cycle have shrunk, emerging teams are seeking help to stand out.

The current market favors large marketing agencies offering integrated services—including design, growth, and development—over individual operators. This holistic approach is more appealing to clients seeking robust marketing solutions.

As large agencies dominate talent competition, continued consolidation is expected

Looking ahead, the marketing agency market may consolidate further, with large agencies dominating top talent. Well-resourced firms can better deliver multidisciplinary services, while small specialists and solo consultants often struggle to compete. However, the best operators with unique expertise in niche areas—such as tokenomics, brand strategy, and founder storytelling—can succeed by differentiating themselves and overcoming market challenges.

What’s Next?

So, what can we expect in the next two-year cycle?

First, we anticipate major innovation in incentive programs—including referrals, quests, and loyalty systems. Companies will experiment with new formats and mechanisms designed to create more engaging and rewarding user experiences.

Second, integrating social elements into messaging platforms will become critical. Web3 social apps may evolve into the primary messaging layer, forcing traditional Web3 messaging platforms to incorporate social features to stay relevant.

Finally, we expect a wave of bold, unconventional ideas that push the boundaries of what’s possible in Web3. While some concepts may seem far-fetched today, they could define the next phase of this rapidly evolving industry.

The Web3 growth landscape stands on the edge of transformation, driven by innovation and a willingness to explore uncharted territory. Those who adapt and lead in these domains will shape the future of digital interaction and media.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News