Do prediction markets need Web3?

TechFlow Selected TechFlow Selected

Do prediction markets need Web3?

Prediction Markets: Belief - Betting - Outcome Resolution, Full Lifecycle Application Practice in Web3.

Author: Sid, IOSG Ventures

Special thanks to Aravind Menon for his insights

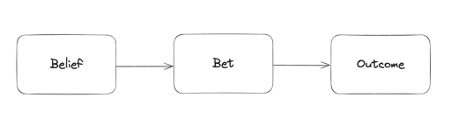

The Lifecycle of a Bet

Investopedia defines prediction markets as: "a market where people can trade contracts based on the outcome of future uncertain events." Essentially, it is a betting/gambling market. To better understand betting markets, let's break down the lifecycle of a bet:

Belief

In the belief phase, a prediction is merely an opinion. When someone turns their opinion into a financial bet—putting money behind it—they stand to gain a return if the outcome supports that belief.

Beliefs are formed through complex interactions of cognitive, social, emotional, and environmental factors. Opinions can arise from immediate convictions or deliberate reasoning, and since expressing them carries no financial cost, opinions are given more freely.

Betting

Bets emerge in two scenarios:

-

To profit from one’s own belief

-

When the potential payout is attractive regardless of belief

The first type stems from calculated opinions; the second arises from a "small bet, big win" mentality.

For any contract to function, there must be both sides:

-

If you bet $50 on Chelsea winning a match, someone (or multiple people) must collectively bet $50 on Chelsea losing (assuming 50/50 odds)

-

On GMX, when a trader opens a long position, GLP acts as the counterparty

-

Casino games like roulette or blackjack require a "house" to serve as the counterparty

Sometimes, incentives are needed to attract counterparties, especially when outcomes aren't equally likely. These include odds adjustments, bonding curves in AMMs (Automated Market Makers), or funding rates in perpetual/leveraged trading platforms.

Market design becomes more complex when focusing on specific types of outcomes. Sports betting, for example, requires unique odds setting since almost no two events have identical outcomes. Additionally, each major event (e.g., league champion) may involve many smaller events (each game result), further increasing complexity.

In prediction events, contracts must also execute correctly. What if your counterparty refuses to pay? This is why derivatives are inherently legally enforceable contracts. On blockchains, contracts can be executed trustlessly based on outcomes.

Therefore, for betting to occur, we need:

-

An event (or non-event) and a published contract for that event/game

-

Sufficient participants holding opinions on these events (maker demand: market participants providing orders)

-

Counterparties available for those participants (taker demand: market participants executing existing orders)

-

Settlement assurance

-

Anti-manipulation safeguards

Outcome

"Gambling games promote the 'illusion of control': the gambler believes they can apply skill to outcomes fundamentally defined by chance." – Dr. Luke Clark

The outcome marks the end of a bet. Once determined, the bet is settled.

Do Prediction Markets Need Web3?

Let’s assess the necessity of Web3 using the criteria above for creating gambling markets:

Event/Game Creation

Beyond permissionless event posting, there’s no clear blockchain use case here. Permissionless posting is a flaw rather than a feature, as it creates high redundancy for the same event, degrading the bettor experience. Bets can be created around real-world events or games like on-chain roulette or blackjack. (Permissionless posting refers to anyone being able to publish information or transactions without centralized review or approval.)

Events can also involve price discovery. We’ve seen prediction markets for unreleased tokens on Aevo, offering a good indicator of market sentiment on token pricing.

Parcl is building a prediction market for better real estate price discovery. It gives homeowners an approximate valuation of their property and helps buyers budget for real estate purchases in specific cities.

Price discovery use cases also depend on liquidity within event contracts, which is why the next section matters.

Maker Demand

Blockchain cannot control maker demand, which is entirely driven by offline factors such as built-in marketing or gamification within the product.

Companies focused on price discovery must generate as much maker volume as possible to derive the most accurate asset prices.

Counterparty Availability

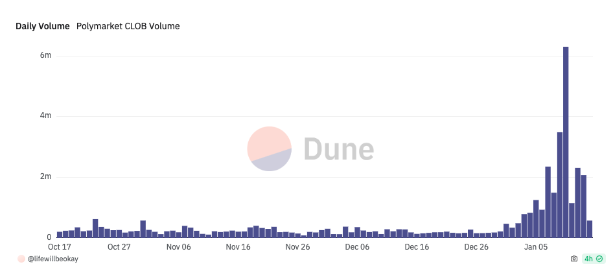

Now we reach an interesting topic. Attractive odds can incentivize counterparties to participate, especially when an event’s outcome is nearly certain. As shown below, due to massive imbalances in Polymarket’s order book, it was possible to win $200 with a $0.50 bet.

One approach is Augur Turbo, where each market operates independently on Balancer AMMs. Here, LPs (liquidity providers) act as counterparties across different markets. While this structure avoids overreliance on odds calculation (or sourcing), it worsens the user experience for launching prediction events.

For order-book-based price discovery platforms like Aevo, lack of liquidity forces the platform to sometimes become its own counterparty—an undesirable situation, especially when downside risks are unknown.

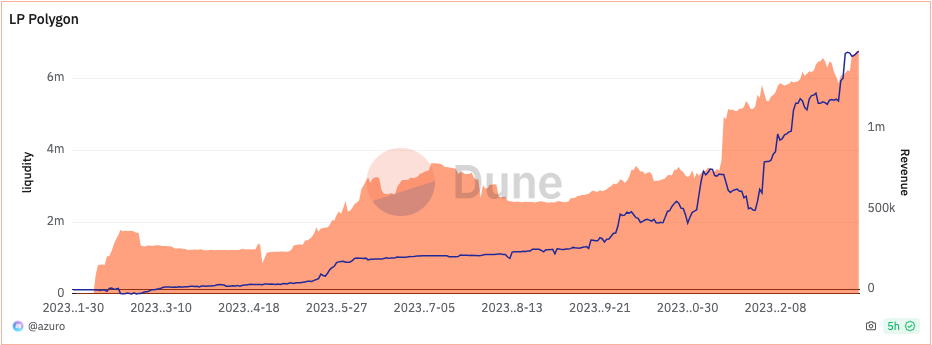

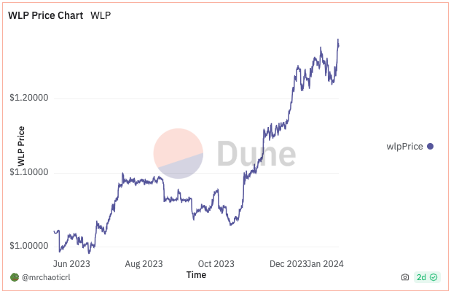

Another method is creating a pooled counterparty LP model like “The House,” as done by Azuro and WINR. A single liquidity pool serves as the counterparty to all bets. Parcl has a USDC liquidity pool acting as counterparty for traders going long or short on real estate prices across different cities.

Both protocols have demonstrated effectiveness:

Azuro LPs’ revenue on Polygon (Source: Dune)

WINR’s LP token (WLP) has risen from $1 to ~$1.27 (indicating a 27% return for those who started LPing around July 1, 2023)

(Source: Dune)

These models show strong product-market fit, where frontends only need to focus on getting users to place bets, without managing order books or making AMM-related trade-offs.

You can view these models as Uniswap v4, where different frontends leverage underlying liquidity (similar to hooks).

The WINR protocol hosts both a casino betting frontend and a margin trading protocol offering up to 1000x leverage, ensuring high pool utilization—but potentially posing significant risk to the pool.

Ensuring Settlement

Once an event concludes, bets must be settled. In AMM structures, everything occurs on-chain and is settled via smart contracts. For Polymarket’s order book model, the book is maintained off-chain. Polymarket could theoretically block withdrawals if needed. For Azuro frontends like Bookmaker.xyz, no deposits are required—each bet is treated as a standalone transaction. The only off-chain components are odds calculation and data sourcing.

Preventing Manipulation

If a centralized data provider manipulates the data source, it could negatively impact outcomes for both makers and takers. This is a primary reason most Web3 prediction markets use oracle systems like Chainlink. Oracles involve trade-offs between latency and data integrity. Platforms choosing oracles must decide between first-party and third-party providers, balancing timeliness. In fast-moving events, latency can be critically important.

In casino games, the integrity of randomness is paramount—the fairness must not be compromised by its source.

Chainlink and other oracles like Supra and Pyth minimize manipulation risks through aggregation, but in broader markets, the authenticity and reliability of data sources remain problematic. These oracle systems strive to provide reliability by aggregating multiple sources, reducing single points of failure, thus protecting markets from improper manipulation. Nevertheless, ensuring data authenticity and preventing manipulation remain ongoing challenges in prediction markets.

Existing Applications: Successes and Failures

When observing crypto markets versus prediction markets, successful examples include cryptocurrencies being used as assets for betting on platforms like Stake.com and Rollbit.

(Blue numbers indicate predicted values)

Although applications like Polymarket have achieved some success, they do not maintain consistent trading volume due to a significant gap between event relevance and platform engagement.

Source: Dune

Product-market fit (PMF) for crypto and prediction markets has begun to emerge in “House”-style pool systems like Azuro and WINR. A clear use case is new frontends focused on specific prediction markets needing only to drive demand-side activity. They can leverage systems like Azuro and WINR, which in turn offer stablecoin holders top-tier yields (currently projecting 40–60% APY).

In most countries, regulations on betting apps and online casinos are very strict. Protocols like Azuro and WINR may face lower regulatory scrutiny compared to companies like Rollbit.

Frontend engagement directly determines participation levels in crypto prediction markets. Currently, there is no fully permissionless and trustless crypto prediction market.

We look forward to seeing potential success from applications like Parcl, which brings transparency to a highly illiquid asset class. From first principles, it appears to have the right structure to achieve its price discovery goals.

Key Web3 use cases include supporting counterparty pool architectures for various prediction markets and enabling prediction markets to improve price discovery.

As cryptocurrency market capitalization grows and more people hold discretionary capital on-chain, the prediction market industry could become profitable—or at least highly useful.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News