ETF decision moment approaching, countdown to BTC price volatility

2024.01.02

Share Share to X (Twitter) Navigating Web3 tides with focused insights

Navigating Web3 tides with focused insights

Share to WeChat

Share to WeiboShare to WeChat

Share by Link

Share by Image

TechFlow Selected TechFlow Selected

ETF decision moment approaching, countdown to BTC price volatility

A Comprehensive Overview of Key Information on Bitcoin Spot ETFs

2024.01.02 - 04:13:11

A Comprehensive Overview of Key Information on Bitcoin Spot ETFs

Written by: Yilan, LD Capital

Bull Engine Ignites

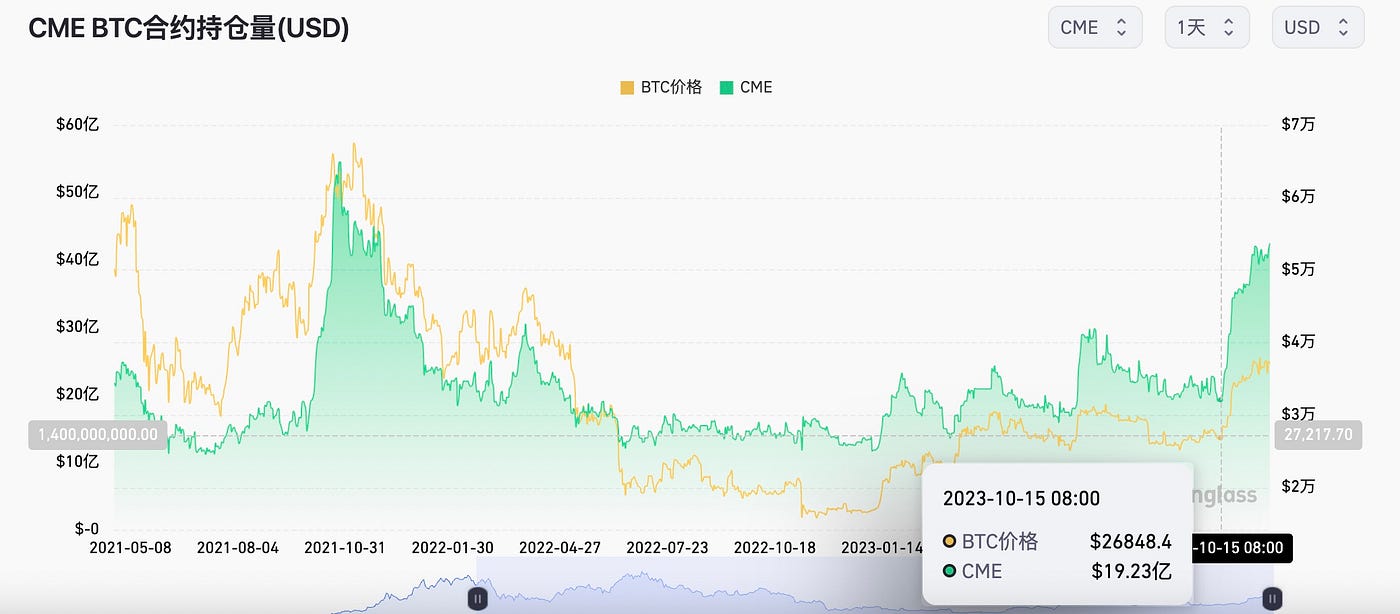

On October 13, the U.S. Securities and Exchange Commission (SEC) announced it would not appeal a court ruling regarding Grayscale’s lawsuit over the SEC's rejection of its application to convert GBTC into a spot ETF. This ruling, issued in August, determined that the SEC’s denial of Grayscale Investments’ request to convert GBTC into a spot Bitcoin exchange-traded fund (ETF) was unjustified.

This pivotal event triggered the current market rally (as shown in the CME BTC OI chart below, open interest began surging sharply starting October 15). The momentum was further amplified by favorable signals such as the Fed pausing rate hikes, sustaining strong BTC performance. Subsequent developments—including Hashdex, Franklin, and Global X reaching key milestones in their applications—and the extension of the review window on November 17 merely provided the market with opportunities for consolidation. However, the most critical date remains January 10—the final decision deadline for Ark & 21Shares' application—toward which market anticipation is strongest. Results could potentially be known as early as next Wednesday, January 3.

Will the Spot ETF Be Approved Under Current Conditions?

Regarding the likelihood of spot ETF approval, Bloomberg ETF analyst James Seyffart estimates a 90% chance of approval for a Bitcoin spot ETF before January 10 next year. As one of the individuals closest to the SEC, his view is widely circulated and influential in the market.

Griffin Ardern, Head of BloFin Options Desk & Research Department—an integrated crypto financial services firm—published research analyzing potential seed capital purchases by authorized participants (APs) ahead of a possible January approval of a spot BTC ETF.

Griffin’s findings indicate that since October 16, an institution has transferred $1.649 billion via the same account to compliant exchanges including Coinbase and Kraken to continuously buy BTC and small amounts of ETH. Very few institutions in the entire crypto market possess the capacity to deploy $1.6 billion in cash. Combined with evidence that the transfer channel used was Tron rather than Ethereum, along with transaction trail analysis, this account likely belongs to a traditional institution headquartered in North America.

In theory, there are no size limits on seed funds, provided sufficient liquidity can be demonstrated on the day of trading. Traditionally, seed procurement occurs 2–4 weeks before ETF launch to minimize position risk for APs such as market makers or ETF issuers. However, due to December holidays and settlement impacts, procurement may begin earlier. While these observations lend some credibility to expectations of a January approval, they do not guarantee it.

From a regulatory timeline perspective, the maximum review period is 240 days, after which the SEC must issue a final decision. As Ark & 21Shares filed the earliest application, the SEC must render a decision by January 10, 2024. If Ark is approved, subsequent applicants are highly likely to follow.

If rejected, Ark would need to resubmit, restarting the 240-day clock. However, if any other applicant receives approval between March and April 2024 or later, Ark could also be fast-tracked for approval.

The SEC previously rejected Grayscale’s proposal to convert GBTC into a spot ETF primarily for two reasons: First, concerns about cryptocurrency trading on unregulated platforms, making oversight difficult, and longstanding issues of market manipulation in the spot market. Although the SEC has approved crypto futures ETFs, those products trade exclusively on platforms regulated by U.S. financial authorities. Second, many investors in BTC spot ETFs use pension funds or retirement savings, which cannot afford high-volatility, high-risk products that might lead to investor losses.

However, the SEC’s decision not to appeal Grayscale’s case, coupled with increasingly proactive communication during recent ETF applications, signals a higher probability of approval. Recently, the SEC published two memoranda on its website indicating discussions held on November 20 (Eastern Time) with Grayscale regarding proposed rule changes for listing and trading its Bitcoin Trust ETF. On the same day, the SEC also met with BlackRock, the world’s largest asset manager, to discuss similar rule changes for its iShares Bitcoin Trust ETF. Attached to the latter memo were two slides prepared by BlackRock outlining two ETF redemption models: In-Kind Redemption Model and In-Cash Redemption Model. The in-kind model involves redeeming actual Bitcoin holdings from the ETF, while in-cash uses equivalent cash value instead. BlackRock appears to favor the former, though the SEC has reportedly accepted the in-cash condition. As of January 20, the SEC has held 25 meetings with various ETF applicants. These new requirements—(1) requiring all ETFs to use cash creation and eliminate physical redemptions entirely, and (2) requiring applicants to disclose AP (Authorized Participant) information in the next S-1 filing update—are outcomes of extensive negotiations. If fulfilled by the January 10 deadline, all procedural conditions appear satisfied—positive signs suggesting a shift in the SEC’s stance.

From a multi-party博弈 (game theory) perspective, approving a spot BTC ETF represents a complex interplay among a Democrat-majority SEC, the CFTC, major asset managers like BlackRock, and key industry lobbying forces such as Coinbase. Coinbase is widely expected to serve as the custodian for most asset management firms, benefiting its revenue growth. However, custody fees (typically ranging from 0.05% to 0.25%) are relatively insignificant compared to potential gains from new international perpetual trading income and increased spot trading volume. Nevertheless, Coinbase remains one of the biggest potential beneficiaries should spot BTC ETFs be approved, especially given its rise as the primary lobbying force in the U.S. crypto industry following FTX’s collapse.

BlackRock has already launched a crypto-related equity fund—iShares Blockchain and Tech ETF (IBLC). Despite being live for over a year, its assets under management (AUM) remain below $10 million. Thus, BlackRock has strong incentives to push for spot BTC ETF approval.

Moreover, the entry of traditional financial giants like BlackRock, Fidelity, and Invesco brings unique influence in regulatory circles. As the world’s largest asset manager overseeing approximately $9 trillion in assets, BlackRock maintains close ties with the U.S. government and the Federal Reserve. American investors are eager to legally hold cryptocurrencies like Bitcoin as a hedge against fiat inflation—a demand BlackRock and others recognize well, leveraging political influence to pressure the SEC.

In the 2024 election cycle, cryptocurrency and artificial intelligence have emerged as hot-button political issues.

Democrats, including President Biden, the White House, and appointed regulators (SEC, FDIC, Fed), have largely opposed crypto. However, many younger Democratic lawmakers support crypto, reflecting the views of their constituents—leaving room for potential shifts.

Republican presidential candidates are more likely to back crypto innovation. Republican leader Ron DeSantis has pledged to ban central bank digital currencies (CBDCs) and support innovation around Bitcoin and blockchain technology. As governor, DeSantis made Florida one of the most crypto-friendly states in the U.S.

While Trump has previously made negative comments about Bitcoin, he launched an NFT project last year. Moreover, his key supporter states—Florida and Texas—are largely supportive of the crypto industry.

The greatest uncertainty lies with SEC Chair Gary Gensler, a Democrat appointee. Gensler believes most tokens traded on Coinbase are illegal securities. Under his leadership, the SEC has taken a hardline stance toward crypto. Coinbase is currently facing litigation from the SEC over core business practices. Binance faces a similar lawsuit and is defending itself in court. In the worst-case scenario, regulatory crackdowns could cut more than a third of Coinbase’s revenue, according to Berenberg Capital Markets analyst Mark Palmer. “There is little hope of changing the stance of the SEC’s majority commissioners in the short term.”

Rather than waiting for court rulings, Coinbase and other firms hope Congress will carve crypto out of existing securities regulations. Executives are actively lobbying for legislation that limits the SEC’s authority over tokens and establishes clear rules for “stablecoins” like USDC, in which Coinbase holds equity.

Crypto companies are also mounting defensive efforts—lobbying against bills imposing anti-money laundering (AML) requirements, arguing compliance is costly or impossible in a decentralized blockchain-based system. However, each ransomware attack or terrorist funding incident involving tokenized payments makes their task harder. Before and after the Hamas attack on Israel, affiliated groups solicited crypto donations.

Some legislative progress is underway. For example, the House Financial Services Committee passed pro-crypto bills on market structure and stablecoins backed by Coinbase, paving the way for full House votes. But there is no sign yet that Senate Democrats will bring these bills forward, nor whether President Joe Biden would sign any crypto legislation.

Given that spending bills are likely Congress’s top priority this year—and with Congress entering 2024 election mode—controversial crypto legislation may stall for now.

“FTX’s collapse was a setback, but some in Congress recognize crypto is inevitable,” said Kristin Smith, CEO of the Blockchain Association. For now, the industry may have to settle for Bitcoin ETFs, while its lobbying army continues pushing for broader legislative victories in the coming year.

According to a recent Grayscale study, 52% of Americans—including 59% of Democrats and 51% of Republicans—agree that crypto is the future of finance; 44% of respondents said they want to invest in crypto assets in the future.

For the SEC, the fundamental objection remains unresolved: inherent manipulability within the BTC market. But we are about to find out whether the SEC will yield to mounting pressure from powerful stakeholders and approve a spot BTC ETF.

Spot BTC ETF & BTC Price Impact Sensitivity Analysis

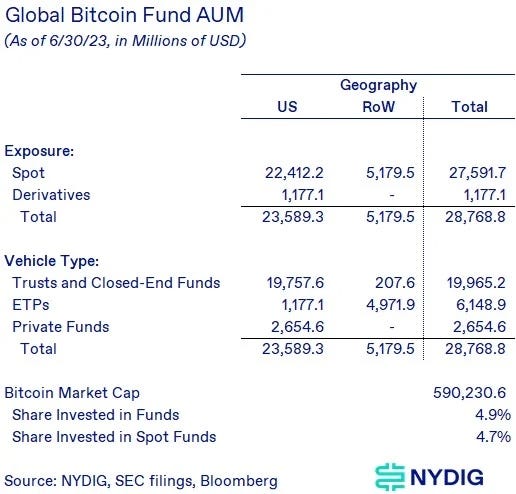

Although the U.S. has not yet launched a direct spot Bitcoin ETF, investors have already participated in the Bitcoin market through existing product structures. Total assets managed across these vehicles exceed $30 billion, with about 95% invested in products tied to spot Bitcoin.

Prior to a U.S. spot BTC ETF, investment options included trusts (e.g., Grayscale Bitcoin Trust GBTC), BTC futures ETFs, spot ETFs launched outside the U.S. (such as in Europe and Canada), and private funds holding BTC. GBTC alone accounts for $23.4 billion in AUM, the largest BTC futures ETF BITO has $1.37 billion, and Canada’s largest spot BTC ETF BTCC has $320 million. Private fund allocations remain opaque, meaning the true total may far exceed $30 billion.

Will the Spot ETF Be Approved Under Current Conditions?

Regarding the likelihood of spot ETF approval, Bloomberg ETF analyst James Seyffart estimates a 90% chance of approval for a Bitcoin spot ETF before January 10 next year. As one of the individuals closest to the SEC, his view is widely circulated and influential in the market.

Griffin Ardern, Head of BloFin Options Desk & Research Department—an integrated crypto financial services firm—published research analyzing potential seed capital purchases by authorized participants (APs) ahead of a possible January approval of a spot BTC ETF.

Griffin’s findings indicate that since October 16, an institution has transferred $1.649 billion via the same account to compliant exchanges including Coinbase and Kraken to continuously buy BTC and small amounts of ETH. Very few institutions in the entire crypto market possess the capacity to deploy $1.6 billion in cash. Combined with evidence that the transfer channel used was Tron rather than Ethereum, along with transaction trail analysis, this account likely belongs to a traditional institution headquartered in North America.

In theory, there are no size limits on seed funds, provided sufficient liquidity can be demonstrated on the day of trading. Traditionally, seed procurement occurs 2–4 weeks before ETF launch to minimize position risk for APs such as market makers or ETF issuers. However, due to December holidays and settlement impacts, procurement may begin earlier. While these observations lend some credibility to expectations of a January approval, they do not guarantee it.

From a regulatory timeline perspective, the maximum review period is 240 days, after which the SEC must issue a final decision. As Ark & 21Shares filed the earliest application, the SEC must render a decision by January 10, 2024. If Ark is approved, subsequent applicants are highly likely to follow.

If rejected, Ark would need to resubmit, restarting the 240-day clock. However, if any other applicant receives approval between March and April 2024 or later, Ark could also be fast-tracked for approval.

The SEC previously rejected Grayscale’s proposal to convert GBTC into a spot ETF primarily for two reasons: First, concerns about cryptocurrency trading on unregulated platforms, making oversight difficult, and longstanding issues of market manipulation in the spot market. Although the SEC has approved crypto futures ETFs, those products trade exclusively on platforms regulated by U.S. financial authorities. Second, many investors in BTC spot ETFs use pension funds or retirement savings, which cannot afford high-volatility, high-risk products that might lead to investor losses.

However, the SEC’s decision not to appeal Grayscale’s case, coupled with increasingly proactive communication during recent ETF applications, signals a higher probability of approval. Recently, the SEC published two memoranda on its website indicating discussions held on November 20 (Eastern Time) with Grayscale regarding proposed rule changes for listing and trading its Bitcoin Trust ETF. On the same day, the SEC also met with BlackRock, the world’s largest asset manager, to discuss similar rule changes for its iShares Bitcoin Trust ETF. Attached to the latter memo were two slides prepared by BlackRock outlining two ETF redemption models: In-Kind Redemption Model and In-Cash Redemption Model. The in-kind model involves redeeming actual Bitcoin holdings from the ETF, while in-cash uses equivalent cash value instead. BlackRock appears to favor the former, though the SEC has reportedly accepted the in-cash condition. As of January 20, the SEC has held 25 meetings with various ETF applicants. These new requirements—(1) requiring all ETFs to use cash creation and eliminate physical redemptions entirely, and (2) requiring applicants to disclose AP (Authorized Participant) information in the next S-1 filing update—are outcomes of extensive negotiations. If fulfilled by the January 10 deadline, all procedural conditions appear satisfied—positive signs suggesting a shift in the SEC’s stance.

From a multi-party博弈 (game theory) perspective, approving a spot BTC ETF represents a complex interplay among a Democrat-majority SEC, the CFTC, major asset managers like BlackRock, and key industry lobbying forces such as Coinbase. Coinbase is widely expected to serve as the custodian for most asset management firms, benefiting its revenue growth. However, custody fees (typically ranging from 0.05% to 0.25%) are relatively insignificant compared to potential gains from new international perpetual trading income and increased spot trading volume. Nevertheless, Coinbase remains one of the biggest potential beneficiaries should spot BTC ETFs be approved, especially given its rise as the primary lobbying force in the U.S. crypto industry following FTX’s collapse.

BlackRock has already launched a crypto-related equity fund—iShares Blockchain and Tech ETF (IBLC). Despite being live for over a year, its assets under management (AUM) remain below $10 million. Thus, BlackRock has strong incentives to push for spot BTC ETF approval.

Moreover, the entry of traditional financial giants like BlackRock, Fidelity, and Invesco brings unique influence in regulatory circles. As the world’s largest asset manager overseeing approximately $9 trillion in assets, BlackRock maintains close ties with the U.S. government and the Federal Reserve. American investors are eager to legally hold cryptocurrencies like Bitcoin as a hedge against fiat inflation—a demand BlackRock and others recognize well, leveraging political influence to pressure the SEC.

In the 2024 election cycle, cryptocurrency and artificial intelligence have emerged as hot-button political issues.

Democrats, including President Biden, the White House, and appointed regulators (SEC, FDIC, Fed), have largely opposed crypto. However, many younger Democratic lawmakers support crypto, reflecting the views of their constituents—leaving room for potential shifts.

Republican presidential candidates are more likely to back crypto innovation. Republican leader Ron DeSantis has pledged to ban central bank digital currencies (CBDCs) and support innovation around Bitcoin and blockchain technology. As governor, DeSantis made Florida one of the most crypto-friendly states in the U.S.

While Trump has previously made negative comments about Bitcoin, he launched an NFT project last year. Moreover, his key supporter states—Florida and Texas—are largely supportive of the crypto industry.

The greatest uncertainty lies with SEC Chair Gary Gensler, a Democrat appointee. Gensler believes most tokens traded on Coinbase are illegal securities. Under his leadership, the SEC has taken a hardline stance toward crypto. Coinbase is currently facing litigation from the SEC over core business practices. Binance faces a similar lawsuit and is defending itself in court. In the worst-case scenario, regulatory crackdowns could cut more than a third of Coinbase’s revenue, according to Berenberg Capital Markets analyst Mark Palmer. “There is little hope of changing the stance of the SEC’s majority commissioners in the short term.”

Rather than waiting for court rulings, Coinbase and other firms hope Congress will carve crypto out of existing securities regulations. Executives are actively lobbying for legislation that limits the SEC’s authority over tokens and establishes clear rules for “stablecoins” like USDC, in which Coinbase holds equity.

Crypto companies are also mounting defensive efforts—lobbying against bills imposing anti-money laundering (AML) requirements, arguing compliance is costly or impossible in a decentralized blockchain-based system. However, each ransomware attack or terrorist funding incident involving tokenized payments makes their task harder. Before and after the Hamas attack on Israel, affiliated groups solicited crypto donations.

Some legislative progress is underway. For example, the House Financial Services Committee passed pro-crypto bills on market structure and stablecoins backed by Coinbase, paving the way for full House votes. But there is no sign yet that Senate Democrats will bring these bills forward, nor whether President Joe Biden would sign any crypto legislation.

Given that spending bills are likely Congress’s top priority this year—and with Congress entering 2024 election mode—controversial crypto legislation may stall for now.

“FTX’s collapse was a setback, but some in Congress recognize crypto is inevitable,” said Kristin Smith, CEO of the Blockchain Association. For now, the industry may have to settle for Bitcoin ETFs, while its lobbying army continues pushing for broader legislative victories in the coming year.

According to a recent Grayscale study, 52% of Americans—including 59% of Democrats and 51% of Republicans—agree that crypto is the future of finance; 44% of respondents said they want to invest in crypto assets in the future.

For the SEC, the fundamental objection remains unresolved: inherent manipulability within the BTC market. But we are about to find out whether the SEC will yield to mounting pressure from powerful stakeholders and approve a spot BTC ETF.

Spot BTC ETF & BTC Price Impact Sensitivity Analysis

Although the U.S. has not yet launched a direct spot Bitcoin ETF, investors have already participated in the Bitcoin market through existing product structures. Total assets managed across these vehicles exceed $30 billion, with about 95% invested in products tied to spot Bitcoin.

Prior to a U.S. spot BTC ETF, investment options included trusts (e.g., Grayscale Bitcoin Trust GBTC), BTC futures ETFs, spot ETFs launched outside the U.S. (such as in Europe and Canada), and private funds holding BTC. GBTC alone accounts for $23.4 billion in AUM, the largest BTC futures ETF BITO has $1.37 billion, and Canada’s largest spot BTC ETF BTCC has $320 million. Private fund allocations remain opaque, meaning the true total may far exceed $30 billion.

Spot ETF vs. Existing Alternatives

Compared to existing alternatives, a spot ETF offers lower tracking error than trusts/closed-end funds (CEF)—products like BITO, BTF, and XBTF lag behind spot Bitcoin prices by 7%-10% annually—better liquidity than private funds, and potentially lower management fees than GBTC. For instance, Ark proposed a fee of just 0.9% in its filing.

Potential Capital Inflows:

Existing Demand

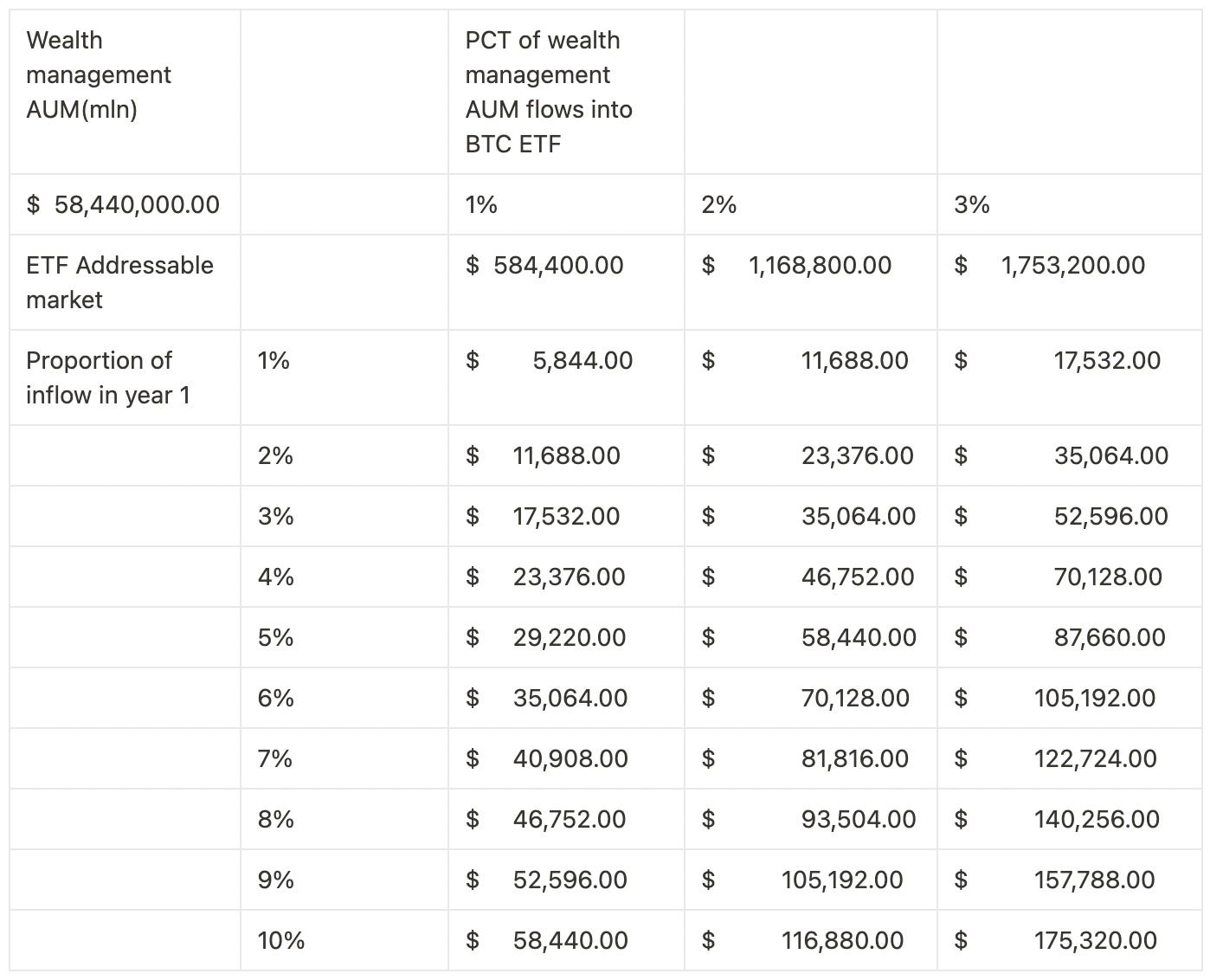

It is foreseeable that unless GBTC improves its fee structure significantly, substantial outflows from its AUM will occur—though these will likely be offset by inflows into new ETFs. Assuming 1% of the current $58.44 trillion wealth management AUM flows into BTC, with 5% entering in the first year, this would generate $58.44T × 1% × 5% = $29 billion in existing wealth management inflows. If 10% enters on day one, that creates $2.9 billion in immediate buying pressure ($29B × 10%). Combined with technical resistance levels, and considering only ETF-driven inflows without other factors, Bitcoin’s price target rises to $53,000 (based mainly on resistance levels; the precise impact of inflows on price is hard to model due to dynamic trading volumes). However, due to complex market sentiment, a "buy the rumor, sell the news" dump after the initial pump is certainly possible.

Spot ETF vs. Existing Alternatives

Compared to existing alternatives, a spot ETF offers lower tracking error than trusts/closed-end funds (CEF)—products like BITO, BTF, and XBTF lag behind spot Bitcoin prices by 7%-10% annually—better liquidity than private funds, and potentially lower management fees than GBTC. For instance, Ark proposed a fee of just 0.9% in its filing.

Potential Capital Inflows:

Existing Demand

It is foreseeable that unless GBTC improves its fee structure significantly, substantial outflows from its AUM will occur—though these will likely be offset by inflows into new ETFs. Assuming 1% of the current $58.44 trillion wealth management AUM flows into BTC, with 5% entering in the first year, this would generate $58.44T × 1% × 5% = $29 billion in existing wealth management inflows. If 10% enters on day one, that creates $2.9 billion in immediate buying pressure ($29B × 10%). Combined with technical resistance levels, and considering only ETF-driven inflows without other factors, Bitcoin’s price target rises to $53,000 (based mainly on resistance levels; the precise impact of inflows on price is hard to model due to dynamic trading volumes). However, due to complex market sentiment, a "buy the rumor, sell the news" dump after the initial pump is certainly possible.

By comparison, gold ETFs have $209 billion in AUM. With BTC’s market cap at roughly 1/10th of gold’s, assuming BTC spot ETF AUM reaches 10% of gold ETF AUM—that is, $20.9 billion—and 10% of that amount flows in during the first year (mirroring gold ETF patterns where ~1/10th of total AUM was retained in Year 1, growing at ~1.2x per year until peak inflows occurred in Years 6–7, then gradually declining), net inflows in Year 1 would be $2.1 billion.

Alternatively, comparing to SPDR Gold (issued by State Street Global Advisors and the largest, most popular gold ETF), which has $57 billion in AUM, assume BTC spot ETF AUM reaches 10%–100% of SPDR’s level—$5.7 billion to $57 billion. This implies Year 1 inflows of $540 million to $5.4 billion (again, based on the pattern of retaining ~1/10th of total AUM in Year 1, with gradual accumulation afterward). Using SPDR Gold as a benchmark, first-year inflows of $540 million to $5.4 billion represent a very conservative estimate.

Using both conservative analogies—comparing to gold ETFs and assuming 1% of $58.44 trillion wealth management AUM flows into BTC—it is reasonable to expect first-year inflows into a BTC spot ETF to range between $5.4 billion and $29 billion.

By comparison, gold ETFs have $209 billion in AUM. With BTC’s market cap at roughly 1/10th of gold’s, assuming BTC spot ETF AUM reaches 10% of gold ETF AUM—that is, $20.9 billion—and 10% of that amount flows in during the first year (mirroring gold ETF patterns where ~1/10th of total AUM was retained in Year 1, growing at ~1.2x per year until peak inflows occurred in Years 6–7, then gradually declining), net inflows in Year 1 would be $2.1 billion.

Alternatively, comparing to SPDR Gold (issued by State Street Global Advisors and the largest, most popular gold ETF), which has $57 billion in AUM, assume BTC spot ETF AUM reaches 10%–100% of SPDR’s level—$5.7 billion to $57 billion. This implies Year 1 inflows of $540 million to $5.4 billion (again, based on the pattern of retaining ~1/10th of total AUM in Year 1, with gradual accumulation afterward). Using SPDR Gold as a benchmark, first-year inflows of $540 million to $5.4 billion represent a very conservative estimate.

Using both conservative analogies—comparing to gold ETFs and assuming 1% of $58.44 trillion wealth management AUM flows into BTC—it is reasonable to expect first-year inflows into a BTC spot ETF to range between $5.4 billion and $29 billion.

New Demand

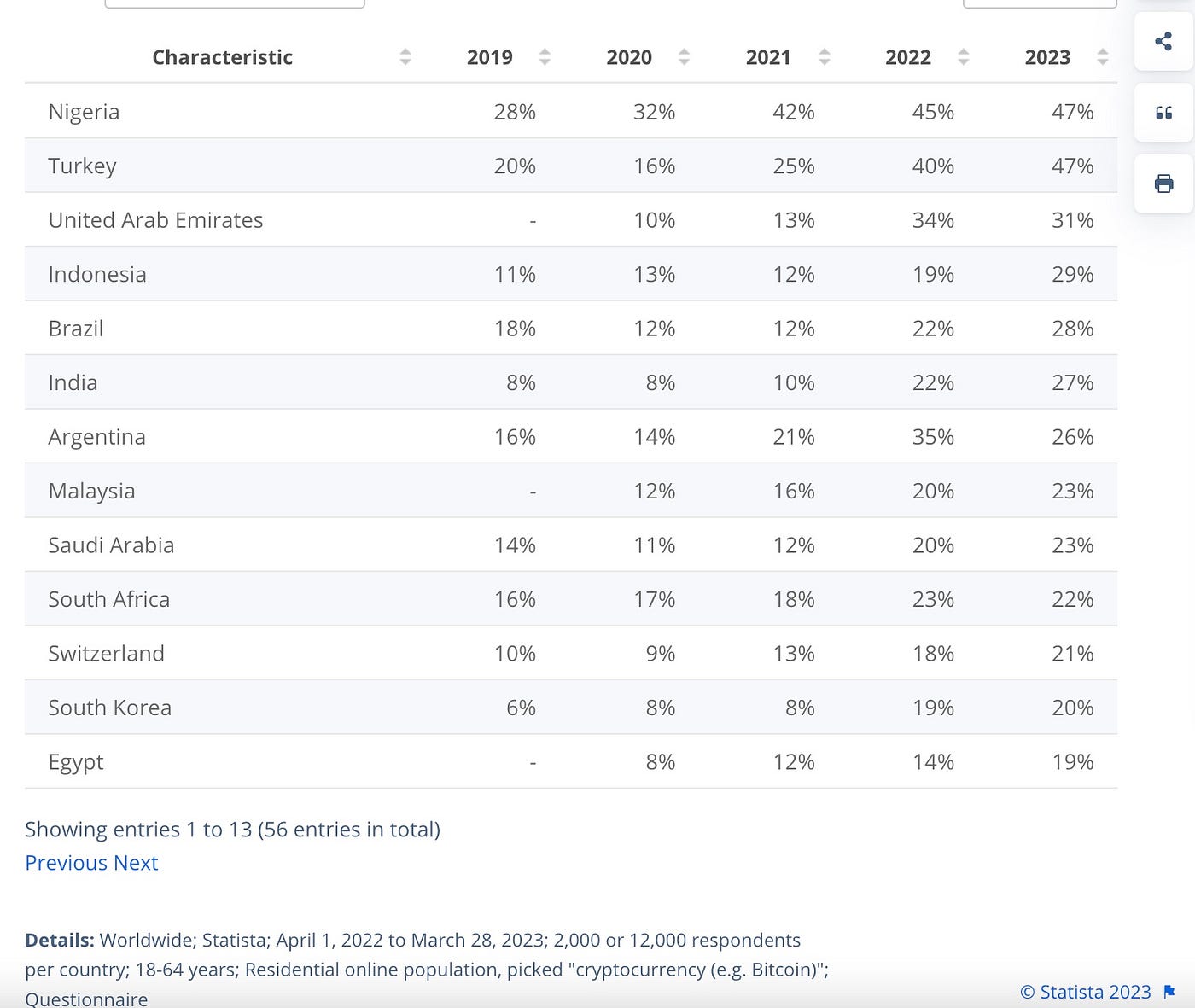

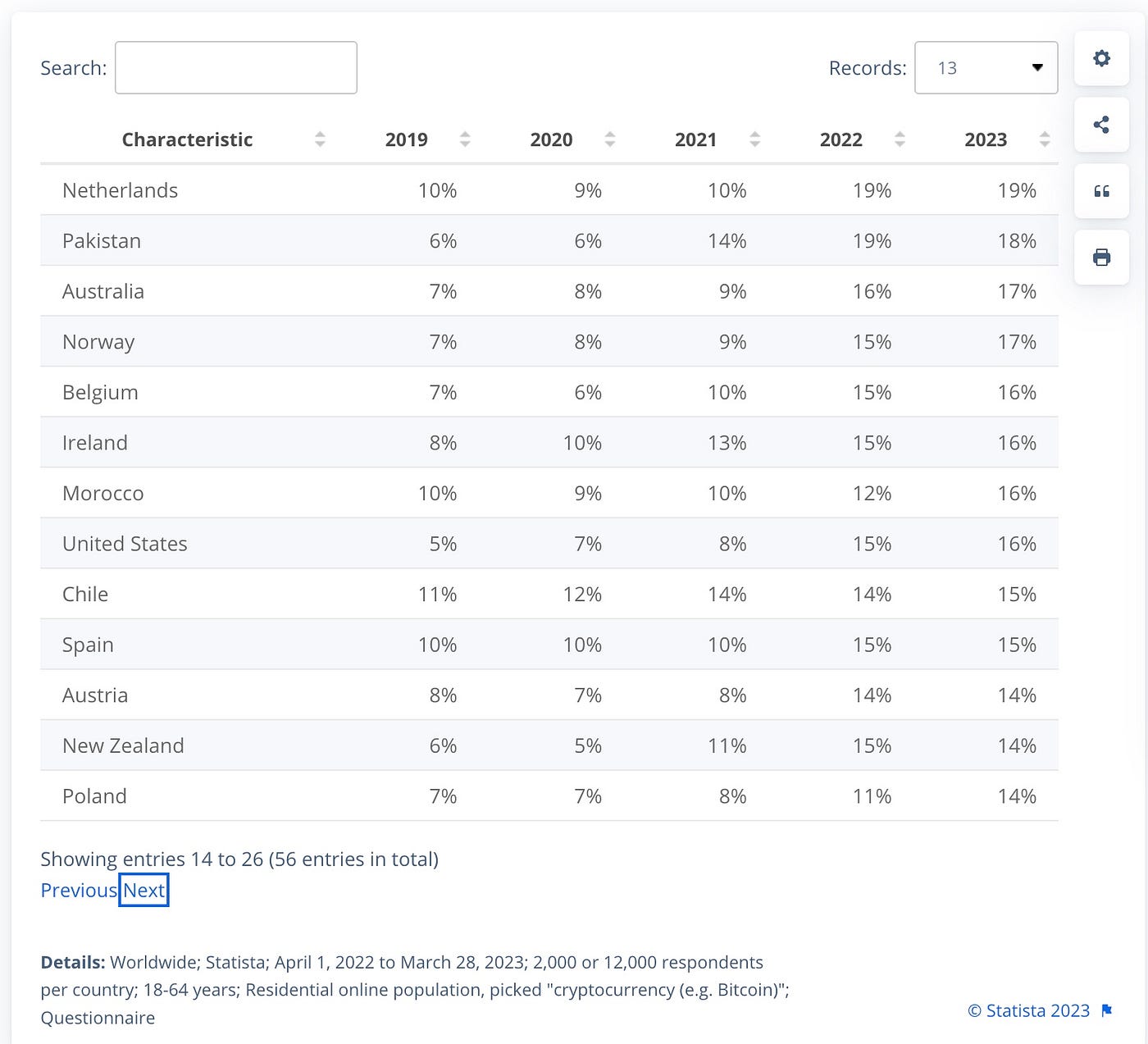

Considering new retail adoption, U.S. BTC ownership rates from 2019 to 2023 were 5%, 7%, 8%, 15%, and 16%, respectively, ranking 21st globally. A spot BTC ETF approval is highly likely to increase this further. Assuming ownership rises to 20%, adding 13.2 million retail investors, and using an average household income of $120,000 with each holding $1,000 worth of BTC, this would generate $13 billion in new demand.

New Demand

Considering new retail adoption, U.S. BTC ownership rates from 2019 to 2023 were 5%, 7%, 8%, 15%, and 16%, respectively, ranking 21st globally. A spot BTC ETF approval is highly likely to increase this further. Assuming ownership rises to 20%, adding 13.2 million retail investors, and using an average household income of $120,000 with each holding $1,000 worth of BTC, this would generate $13 billion in new demand.

Conclusion

As increasing numbers of investors recognize Bitcoin’s value as a store of value or digital gold, combined with rising certainty around ETF approval, the upcoming halving event, and the Fed pausing rate hikes, BTC’s price is highly likely to reach $53,000 in the first half of next year.

Ethereum spot ETF approval, subject to the same 240-day application process and complicated by ongoing debates over whether ETH qualifies as a security, is expected to come significantly later than Bitcoin’s. Perhaps only when Gensler is replaced by a more crypto-friendly leader will Ethereum finally see its own ETF-driven bull run.

Conclusion

As increasing numbers of investors recognize Bitcoin’s value as a store of value or digital gold, combined with rising certainty around ETF approval, the upcoming halving event, and the Fed pausing rate hikes, BTC’s price is highly likely to reach $53,000 in the first half of next year.

Ethereum spot ETF approval, subject to the same 240-day application process and complicated by ongoing debates over whether ETH qualifies as a security, is expected to come significantly later than Bitcoin’s. Perhaps only when Gensler is replaced by a more crypto-friendly leader will Ethereum finally see its own ETF-driven bull run.

Will the Spot ETF Be Approved Under Current Conditions?

Regarding the likelihood of spot ETF approval, Bloomberg ETF analyst James Seyffart estimates a 90% chance of approval for a Bitcoin spot ETF before January 10 next year. As one of the individuals closest to the SEC, his view is widely circulated and influential in the market.

Griffin Ardern, Head of BloFin Options Desk & Research Department—an integrated crypto financial services firm—published research analyzing potential seed capital purchases by authorized participants (APs) ahead of a possible January approval of a spot BTC ETF.

Griffin’s findings indicate that since October 16, an institution has transferred $1.649 billion via the same account to compliant exchanges including Coinbase and Kraken to continuously buy BTC and small amounts of ETH. Very few institutions in the entire crypto market possess the capacity to deploy $1.6 billion in cash. Combined with evidence that the transfer channel used was Tron rather than Ethereum, along with transaction trail analysis, this account likely belongs to a traditional institution headquartered in North America.

In theory, there are no size limits on seed funds, provided sufficient liquidity can be demonstrated on the day of trading. Traditionally, seed procurement occurs 2–4 weeks before ETF launch to minimize position risk for APs such as market makers or ETF issuers. However, due to December holidays and settlement impacts, procurement may begin earlier. While these observations lend some credibility to expectations of a January approval, they do not guarantee it.

From a regulatory timeline perspective, the maximum review period is 240 days, after which the SEC must issue a final decision. As Ark & 21Shares filed the earliest application, the SEC must render a decision by January 10, 2024. If Ark is approved, subsequent applicants are highly likely to follow.

If rejected, Ark would need to resubmit, restarting the 240-day clock. However, if any other applicant receives approval between March and April 2024 or later, Ark could also be fast-tracked for approval.

The SEC previously rejected Grayscale’s proposal to convert GBTC into a spot ETF primarily for two reasons: First, concerns about cryptocurrency trading on unregulated platforms, making oversight difficult, and longstanding issues of market manipulation in the spot market. Although the SEC has approved crypto futures ETFs, those products trade exclusively on platforms regulated by U.S. financial authorities. Second, many investors in BTC spot ETFs use pension funds or retirement savings, which cannot afford high-volatility, high-risk products that might lead to investor losses.

However, the SEC’s decision not to appeal Grayscale’s case, coupled with increasingly proactive communication during recent ETF applications, signals a higher probability of approval. Recently, the SEC published two memoranda on its website indicating discussions held on November 20 (Eastern Time) with Grayscale regarding proposed rule changes for listing and trading its Bitcoin Trust ETF. On the same day, the SEC also met with BlackRock, the world’s largest asset manager, to discuss similar rule changes for its iShares Bitcoin Trust ETF. Attached to the latter memo were two slides prepared by BlackRock outlining two ETF redemption models: In-Kind Redemption Model and In-Cash Redemption Model. The in-kind model involves redeeming actual Bitcoin holdings from the ETF, while in-cash uses equivalent cash value instead. BlackRock appears to favor the former, though the SEC has reportedly accepted the in-cash condition. As of January 20, the SEC has held 25 meetings with various ETF applicants. These new requirements—(1) requiring all ETFs to use cash creation and eliminate physical redemptions entirely, and (2) requiring applicants to disclose AP (Authorized Participant) information in the next S-1 filing update—are outcomes of extensive negotiations. If fulfilled by the January 10 deadline, all procedural conditions appear satisfied—positive signs suggesting a shift in the SEC’s stance.

From a multi-party博弈 (game theory) perspective, approving a spot BTC ETF represents a complex interplay among a Democrat-majority SEC, the CFTC, major asset managers like BlackRock, and key industry lobbying forces such as Coinbase. Coinbase is widely expected to serve as the custodian for most asset management firms, benefiting its revenue growth. However, custody fees (typically ranging from 0.05% to 0.25%) are relatively insignificant compared to potential gains from new international perpetual trading income and increased spot trading volume. Nevertheless, Coinbase remains one of the biggest potential beneficiaries should spot BTC ETFs be approved, especially given its rise as the primary lobbying force in the U.S. crypto industry following FTX’s collapse.

BlackRock has already launched a crypto-related equity fund—iShares Blockchain and Tech ETF (IBLC). Despite being live for over a year, its assets under management (AUM) remain below $10 million. Thus, BlackRock has strong incentives to push for spot BTC ETF approval.

Moreover, the entry of traditional financial giants like BlackRock, Fidelity, and Invesco brings unique influence in regulatory circles. As the world’s largest asset manager overseeing approximately $9 trillion in assets, BlackRock maintains close ties with the U.S. government and the Federal Reserve. American investors are eager to legally hold cryptocurrencies like Bitcoin as a hedge against fiat inflation—a demand BlackRock and others recognize well, leveraging political influence to pressure the SEC.

In the 2024 election cycle, cryptocurrency and artificial intelligence have emerged as hot-button political issues.

Democrats, including President Biden, the White House, and appointed regulators (SEC, FDIC, Fed), have largely opposed crypto. However, many younger Democratic lawmakers support crypto, reflecting the views of their constituents—leaving room for potential shifts.

Republican presidential candidates are more likely to back crypto innovation. Republican leader Ron DeSantis has pledged to ban central bank digital currencies (CBDCs) and support innovation around Bitcoin and blockchain technology. As governor, DeSantis made Florida one of the most crypto-friendly states in the U.S.

While Trump has previously made negative comments about Bitcoin, he launched an NFT project last year. Moreover, his key supporter states—Florida and Texas—are largely supportive of the crypto industry.

The greatest uncertainty lies with SEC Chair Gary Gensler, a Democrat appointee. Gensler believes most tokens traded on Coinbase are illegal securities. Under his leadership, the SEC has taken a hardline stance toward crypto. Coinbase is currently facing litigation from the SEC over core business practices. Binance faces a similar lawsuit and is defending itself in court. In the worst-case scenario, regulatory crackdowns could cut more than a third of Coinbase’s revenue, according to Berenberg Capital Markets analyst Mark Palmer. “There is little hope of changing the stance of the SEC’s majority commissioners in the short term.”

Rather than waiting for court rulings, Coinbase and other firms hope Congress will carve crypto out of existing securities regulations. Executives are actively lobbying for legislation that limits the SEC’s authority over tokens and establishes clear rules for “stablecoins” like USDC, in which Coinbase holds equity.

Crypto companies are also mounting defensive efforts—lobbying against bills imposing anti-money laundering (AML) requirements, arguing compliance is costly or impossible in a decentralized blockchain-based system. However, each ransomware attack or terrorist funding incident involving tokenized payments makes their task harder. Before and after the Hamas attack on Israel, affiliated groups solicited crypto donations.

Some legislative progress is underway. For example, the House Financial Services Committee passed pro-crypto bills on market structure and stablecoins backed by Coinbase, paving the way for full House votes. But there is no sign yet that Senate Democrats will bring these bills forward, nor whether President Joe Biden would sign any crypto legislation.

Given that spending bills are likely Congress’s top priority this year—and with Congress entering 2024 election mode—controversial crypto legislation may stall for now.

“FTX’s collapse was a setback, but some in Congress recognize crypto is inevitable,” said Kristin Smith, CEO of the Blockchain Association. For now, the industry may have to settle for Bitcoin ETFs, while its lobbying army continues pushing for broader legislative victories in the coming year.

According to a recent Grayscale study, 52% of Americans—including 59% of Democrats and 51% of Republicans—agree that crypto is the future of finance; 44% of respondents said they want to invest in crypto assets in the future.

For the SEC, the fundamental objection remains unresolved: inherent manipulability within the BTC market. But we are about to find out whether the SEC will yield to mounting pressure from powerful stakeholders and approve a spot BTC ETF.

Spot BTC ETF & BTC Price Impact Sensitivity Analysis

Although the U.S. has not yet launched a direct spot Bitcoin ETF, investors have already participated in the Bitcoin market through existing product structures. Total assets managed across these vehicles exceed $30 billion, with about 95% invested in products tied to spot Bitcoin.

Prior to a U.S. spot BTC ETF, investment options included trusts (e.g., Grayscale Bitcoin Trust GBTC), BTC futures ETFs, spot ETFs launched outside the U.S. (such as in Europe and Canada), and private funds holding BTC. GBTC alone accounts for $23.4 billion in AUM, the largest BTC futures ETF BITO has $1.37 billion, and Canada’s largest spot BTC ETF BTCC has $320 million. Private fund allocations remain opaque, meaning the true total may far exceed $30 billion.

Spot ETF vs. Existing Alternatives

Compared to existing alternatives, a spot ETF offers lower tracking error than trusts/closed-end funds (CEF)—products like BITO, BTF, and XBTF lag behind spot Bitcoin prices by 7%-10% annually—better liquidity than private funds, and potentially lower management fees than GBTC. For instance, Ark proposed a fee of just 0.9% in its filing.

Potential Capital Inflows:

Existing Demand

It is foreseeable that unless GBTC improves its fee structure significantly, substantial outflows from its AUM will occur—though these will likely be offset by inflows into new ETFs. Assuming 1% of the current $58.44 trillion wealth management AUM flows into BTC, with 5% entering in the first year, this would generate $58.44T × 1% × 5% = $29 billion in existing wealth management inflows. If 10% enters on day one, that creates $2.9 billion in immediate buying pressure ($29B × 10%). Combined with technical resistance levels, and considering only ETF-driven inflows without other factors, Bitcoin’s price target rises to $53,000 (based mainly on resistance levels; the precise impact of inflows on price is hard to model due to dynamic trading volumes). However, due to complex market sentiment, a "buy the rumor, sell the news" dump after the initial pump is certainly possible.

By comparison, gold ETFs have $209 billion in AUM. With BTC’s market cap at roughly 1/10th of gold’s, assuming BTC spot ETF AUM reaches 10% of gold ETF AUM—that is, $20.9 billion—and 10% of that amount flows in during the first year (mirroring gold ETF patterns where ~1/10th of total AUM was retained in Year 1, growing at ~1.2x per year until peak inflows occurred in Years 6–7, then gradually declining), net inflows in Year 1 would be $2.1 billion.

Alternatively, comparing to SPDR Gold (issued by State Street Global Advisors and the largest, most popular gold ETF), which has $57 billion in AUM, assume BTC spot ETF AUM reaches 10%–100% of SPDR’s level—$5.7 billion to $57 billion. This implies Year 1 inflows of $540 million to $5.4 billion (again, based on the pattern of retaining ~1/10th of total AUM in Year 1, with gradual accumulation afterward). Using SPDR Gold as a benchmark, first-year inflows of $540 million to $5.4 billion represent a very conservative estimate.

Using both conservative analogies—comparing to gold ETFs and assuming 1% of $58.44 trillion wealth management AUM flows into BTC—it is reasonable to expect first-year inflows into a BTC spot ETF to range between $5.4 billion and $29 billion.

New Demand

Considering new retail adoption, U.S. BTC ownership rates from 2019 to 2023 were 5%, 7%, 8%, 15%, and 16%, respectively, ranking 21st globally. A spot BTC ETF approval is highly likely to increase this further. Assuming ownership rises to 20%, adding 13.2 million retail investors, and using an average household income of $120,000 with each holding $1,000 worth of BTC, this would generate $13 billion in new demand.

Conclusion

As increasing numbers of investors recognize Bitcoin’s value as a store of value or digital gold, combined with rising certainty around ETF approval, the upcoming halving event, and the Fed pausing rate hikes, BTC’s price is highly likely to reach $53,000 in the first half of next year.

Ethereum spot ETF approval, subject to the same 240-day application process and complicated by ongoing debates over whether ETH qualifies as a security, is expected to come significantly later than Bitcoin’s. Perhaps only when Gensler is replaced by a more crypto-friendly leader will Ethereum finally see its own ETF-driven bull run.Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News

Add to Favorites

Share to Social Media