Permettez aux joueurs de prouver comment KGeN redéfinit l'acquisition d'utilisateurs

TechFlow SélectionTechFlow Sélection

Permettez aux joueurs de prouver comment KGeN redéfinit l'acquisition d'utilisateurs

KGeN est devenu l'un des plus grands réseaux de jeux Web3, maîtrisant plus de 270 millions d'attributs de données et couvrant plus de 13 millions de comptes enregistrés.

1. Introduction

The gaming industry has now surpassed both film and music in size, with overall growth trends continuing upward—yet it faces significant challenges. After record-breaking expansion during the pandemic, the sector experienced waves of layoffs and consolidation between 2023 and 2024, as development costs surged while investment sharply declined.

Moreover, game distribution has become increasingly difficult. With AI-generated content flooding platforms already saturated by supply, and players favoring established IPs, new projects struggle to stand out. Acquiring highly engaged users is now more challenging than ever.

Despite these hurdles, substantial opportunities remain. Gen Z and Gen Alpha—digital natives raised within virtual worlds like Roblox and Minecraft—are entering their prime spending years, driving sustained market expansion.

Simultaneously, the long-overlooked "Global South" markets are witnessing explosive growth. Driven by rising smartphone penetration, improved internet infrastructure, and increasing incomes, these regions are poised to become major sources of incremental demand for games over the next decade.

This report first examines current challenges in game publishing and analyzes high-growth opportunities across the Global South. The second half focuses on KGeN—a blockchain-based gaming network aiming to reshape incentives between publishers and players. We will also assess the viability of Web3 quest platforms and explore structural shifts in value distribution within the gaming ecosystem.

2. Challenges in Distribution

One of the most pressing issues facing the gaming industry today is undoubtedly distribution. Changes in consumer behavior, regulatory adjustments, lower barriers to entry, and an oversaturated content landscape have made successfully launching a game to millions of users harder than ever before.

Players tend to spend most of their time on familiar titles or franchises, making it extremely difficult for new releases to break through. In 2023, all top ten games ranked by average monthly active users (MAU) had been released more than seven years ago. Moreover, 60% of player time spent on new games still went to series that release annual sequels.

In 2024 alone, Steam saw a record 19,000 new game launches—but those newly released titles accounted for only 15% of total gameplay hours.

Mobile gaming once offered a mature distribution model. The rise of mobile ad networks such as Facebook and Google, combined with widespread smartphone adoption, enabled many games to reach hundreds of millions of users and generate billions in annual revenue. However, in 2021, Apple and Google implemented major privacy policy changes that directly impacted how publishers could target and acquire users.

While these changes did not end mobile advertising altogether, they significantly disrupted user acquisition (UA) strategies and business models. Many publishers have adapted with new scaling methods, but the market is increasingly tilting toward well-funded companies, placing greater competitive pressure on smaller teams.

Looking ahead, the environment appears unlikely to improve. While AI can make UA campaign management more efficient, it simultaneously lowers entry barriers, leading to even greater content volume. UGC platforms like Roblox and Fortnite Creative have become common testing grounds for indie developers, yet they themselves face growing difficulties in content curation and promotion—an issue further exacerbated by the proliferation of AI tools.

This leads us to the Web3 gaming space, where development teams must overcome additional hurdles. Beyond the aforementioned challenges, Web3 games face stricter policies on mobile devices, Steam (the largest PC game platform), and console systems. Furthermore, Web3 games are outright banned in several key markets, including South Korea and China.

Notably, the situation for Web3 game distribution on consoles is beginning to shift. The recent launch of Off The Grid set a precedent for Web3 games entering what was previously considered a “forbidden zone,” offering hope for future expansion along this path.

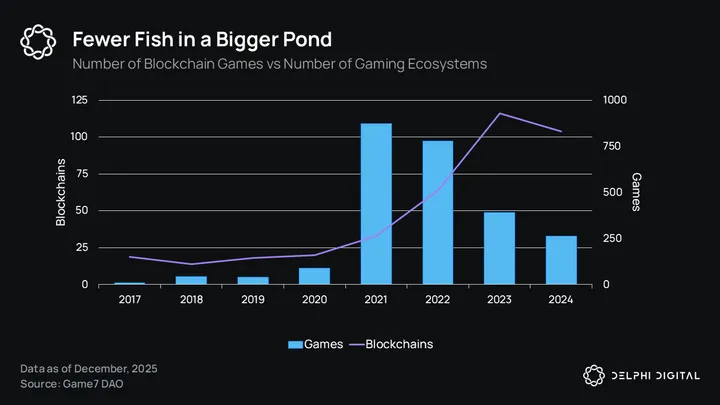

Additionally, the Web3 gaming market remains a niche segment within the broader gaming industry. Currently, around 6–7 million active wallet addresses interact with over 3,000 on-chain gaming protocols. However, this data does not account for the large number of bot accounts prevalent in the Web3 space, and only about 200 protocols maintain more than 100 genuinely active on-chain accounts.

Given its relatively small scale—especially when compared to the global gaming population exceeding 3 billion—the sector’s challenges have been intensified over the past two years by a surge in emerging Web3 ecosystems. According to Game7 data, although the number of new Web3 games has declined by an average of 45% since 2021, the number of new networks has grown by 187%. In 2024 alone, 104 new networks or ecosystems were announced, while only 263 new Web3 games launched.

The problem is that most of these emerging networks fail to attract new players. All these factors contribute to a phenomenon we’ve explored in depth across multiple reports—the battle for player liquidity. As competition intensifies across the entire gaming landscape, Web3 projects are fighting over the same limited pool of wallet users, with few effective means to突破 this bottleneck and achieve scalable growth.

Amid these challenges, a wave of Web3 companies is exploring blockchain-powered user acquisition (UA) models. Innovative incentive mechanisms and on-chain reputation systems are emerging as potential pathways for gaining competitive advantage through Web3 integration.

Many Web3 firms are demonstrating strong product-market fit (PMF) in emerging markets. Compared to saturated Tier-1 markets dominated by Web2 giants, businesses capable of leveraging blockchain’s global payment rails may unlock massive opportunities in underserved regions.

Among these regions, one consistently stands out for above-average growth rates and demonstrated openness to blockchain applications: the Global South.

3. The Global South

The term “Global South” refers to countries and regions with relatively lower economic development, typically located south of industrialized nations. Thanks to rapid improvements in internet infrastructure, high smartphone penetration, and rising disposable incomes, this vast region is widely seen as an underpenetrated but high-potential gaming market.

Key characteristics of gaming markets in the Global South include a large player base, heavy reliance on mobile devices, and generally low monetization levels. Historically, these markets have often been used by publishers for soft-launch user testing and front-end data optimization.

However, the younger generation in these regions represents the first cohort to grow up with smartphones and exhibits a strong preference for digital entertainment—including games, video content, and esports. As this demographic ages and benefits from economic development and income growth, many believe they will evolve into a new generation of paying gamers, fueling the next phase of industry expansion.

Below are key insights into several critical markets within the Global South, highlighting their growing importance in the future of gaming.

India

Despite a relatively late start, India is rapidly emerging as the largest gaming market in the Global South. In 2017, the country had just 44.9 million gamers; today, that number has surged to approximately 466 million, with projections exceeding 640 million by 2027.

Market revenue is expected to grow 13.6% in 2024 (reaching $943 million), surpassing $1 billion in 2025 and reaching $1.4 billion by 2028, representing a five-year compound annual growth rate (CAGR) of 11.1%. This growth is driven by improving in-app purchase habits and rising average revenue per user (ARPU) due to increased disposable income nationwide.

India shows a strong preference for mobile gaming, supported by being one of the world’s fastest-growing 5G markets and possessing a robust digital payments infrastructure—Unified Payments Interface (UPI). UPI transaction volumes rose from 10.78 billion in 2019 to 83.75 billion in 2023, reflecting the rapid rise of the digital economy. Internet penetration has also grown significantly—from 14% in 2015 to 52% today—still below other major Global South markets, indicating substantial room for future expansion.

These technological advances are underpinned by strong macroeconomic fundamentals, including GDP growth of 7–9% over the past three years and a young, expanding middle class with rising incomes.

Indian gaming preferences exhibit distinct patterns compared to other major markets:

- Mobile gaming dominates, accounting for 77.9% of total revenue;

- PC and console gaming account for only 14.5% and 7.7%, respectively.

By revenue composition, different game categories generate the following:

- Real-money gaming (RMG) is the largest segment, generating $2 billion annually;

- Casual and hyper-casual games follow closely, with total revenue of $700 million;

- Other game categories represent a market size of around $400 million.

Southeast Asia (SEA)

Southeast Asia (SEA), comprising Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam, is one of the most mature gaming markets in the Global South. According to Niko Partners, the region generated $5.1 billion in gaming revenue in 2023, up 8.8% year-on-year, with projections reaching $7.1 billion by 2028—a five-year CAGR of 6.7%. In 2023, SEA had 277 million gamers, expected to grow to 332 million by 2028, a CAGR of 3.7%.

According to Sensor Tower’s H1 2024 report:

- Indonesia leads in mobile game downloads with 2.4 billion (41% of regional total);

- Thailand leads in IAP revenue at $400 million, followed by Indonesia at $300 million.

Despite national differences, community and competitive culture are shared traits across the region. Word-of-mouth is the primary source of information, and top-performing games typically feature strong social components.

As in most Global South countries, smartphone adoption and broadband infrastructure are key drivers of market growth. Southeast Asia excels in both:

- In 2022, smartphone penetration exceeded 80% in all major countries;

- Average penetration is projected to reach 90.1% by 2026.

Latin America (LATAM)

Latin America (LATAM) is another market of significant interest, characterized by a large population and vibrant gaming culture—particularly in esports. In 2022, the region had an estimated 316 million gamers, with Brazil being the dominant force, hosting 101 million players and generating $2.7 billion in revenue.

Brazil shows a particularly strong preference for mobile gaming:

- 60% of players have played a mobile game at least once in the past six months;

- Smartphone penetration is expected to reach 83% by 2025, suggesting continued room for mobile gaming growth.

In terms of monetization, Brazilian players show strong spending habits: 43% have made in-game purchases, primarily motivated by unlocking exclusive content (39%), character customization (35%), and game progression (30%). This indicates a maturing market moving beyond basic monetization models toward more sophisticated game economies.

Brazil will continue to lead LATAM’s gaming growth, driven by: 140 universities offering over 4,000 game-related courses, 1,042 game studios nationwide generating ~$251.6 million in revenue, and recently passed legislation formally recognizing game development as a profession and providing tax incentives.

Africa

Africa’s gaming market is at a pivotal stage of development, projected to exceed $1 billion in revenue in 2024, up from $863 million in 2022. Mobile gaming drives this growth, capturing nearly 90% of the market share—reflecting both infrastructure realities and consumer preferences.

Domestic research shows that 92% of African gamers use smartphones to play games, compared to 51% for PCs and 31% for consoles. While this mobile-first trend is validated, the sample size of 2,588 limits its representativeness across the continent.

Main challenges: high data costs (42%) are the biggest barrier, followed by hardware prices (31%) and connectivity issues (31%).

Payment systems present both challenge and opportunity: while 63% of players make in-game purchases, payment methods vary regionally. Kenya leads in mobile payments, with 67% using mobile wallets. Overall, credit cards (45%) and mobile payments (40%) are the most common across Africa.

Middle East and North Africa (MENA)

The MENA region is the world’s fastest-growing gaming market, with revenue rising 4.7% in 2023 to $7.1 billion—far outpacing the global average of 0.6%. It is expected to maintain strong momentum, with a projected CAGR of 9.4% from 2024 to 2030.

By 2027, the core markets of Saudi Arabia, UAE, and Egypt (collectively known as MENA-3) are expected to reach $2.9 billion in revenue, growing at a CAGR of 8.3%. Key drivers include a young population boosting engagement, rising internet penetration in Qatar and UAE, and broad adoption of new technologies.

The region’s gaming landscape is dominated by three powerhouse markets—Saudi Arabia, UAE, and Egypt—known as MENA-3. These markets have shown exceptional performance, growing 7.8% year-on-year to $1.92 billion in 2023, with projections reaching $2.9 billion by 2028 (CAGR: 8.3%). Saudi Arabia leads the pack, contributing 60.6% of total gaming revenue and 30.3% of the region’s gamer base, underscoring its dominance in the regional ecosystem.

4. What Is KGeN?

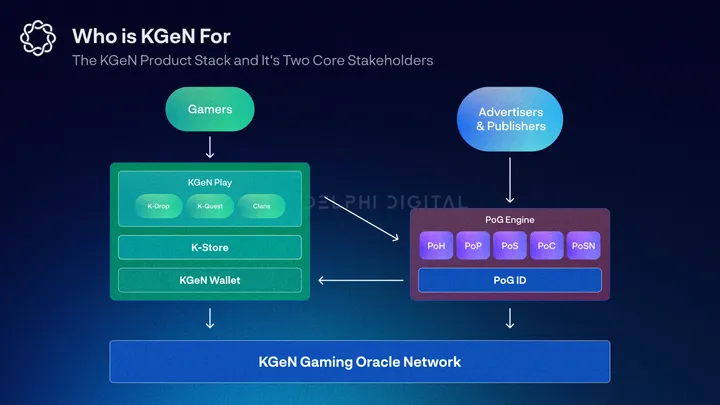

KGeN is a blockchain-powered gaming network that leverages on- and off-chain data, incentivized quest platforms, and decentralized reputation systems to drive cross-game user engagement. Unlike traditional user acquisition (UA) platforms, KGeN redirects publisher funds back to users, fueling a self-reinforcing growth flywheel.

At its core, KGeN operates a decentralized player data network spanning millions of micro-gaming communities (“KGeN tribes”). It employs a novel data model called the Proof of Gamer (PoG) engine to create a cross-chain player reputation layer, delivering highly engaged target audiences to publishers at a fraction of the cost of existing networks.

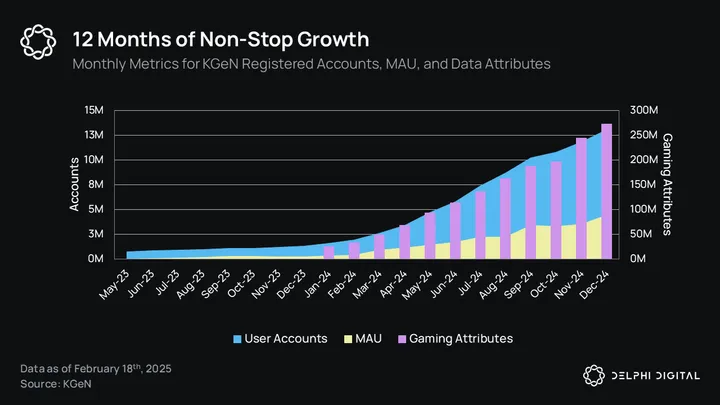

As more players join KGeN and the PoG dataset expands, more game studios and publishing partners are attracted. This increases ecosystem rewards, enhancing the value of participating players. Since January 2024, this flywheel has demonstrated remarkable results: registered accounts grew over 700%, monthly active users (MAU) surged by 1,333%, and total data attributes increased by 992%, establishing KGeN as the most active Web3 quest and player reputation network in the market.

The KGeN ecosystem is gradually decentralizing through a distributed oracle network that secures the PoG engine and provides greater transparency for all core stakeholders. Both the oracle network and the KGeN Store are powered by the KGEN token.

4.1 Grassroots Growth

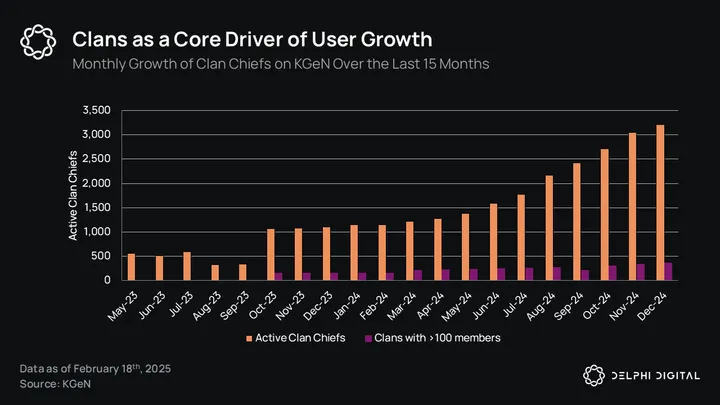

The foundation of KGeN’s growth lies in its grassroots tribe and tribal leader network—a key driver of its expansion across the Global South. Tribes represent thousands of micro-communities joining the KGeN ecosystem, such as coworkers, esports organizations, influencers, and gaming-focused social groups. By December 2024, KGeN reported 2,525 tribes, with 152 having over 100 members.

Tribes serve as a core mechanism for referral-based user acquisition. When creating a tribe, tribal leaders earn points by inviting up to five members and getting them to complete at least one task. These points feed into the KGeN leaderboard—one of the main reward systems (detailed later). This incentive-driven funnel has proven highly effective: approximately 1.7 million KYC-verified KGeN accounts (39% of MAU, 13% of total registrations) were acquired through tribes.

Tribal leaders are not only incentivized to bring in new members but must also coordinate activities and maintain community engagement to maximize earnings. A portion of the tribe’s total rewards flows back to the leader, forming a crucial growth incentive within the ecosystem.

India is currently KGeN’s largest market, benefiting from the company’s origins and strong influence among local micro-gaming communities. However, over 30% of independent active wallets and transactions occur on Kaia, the proprietary blockchain of the LINE messaging app. LINE’s largest markets are Japan (86 million users), Thailand (47 million), Taiwan (21 million), and Indonesia (13 million), signaling strong growth potential for KGeN across Asia.

To replicate its Indian success in other Global South markets, KGeN is encouraged to adopt similar grassroots strategies. Partnering with local micro-gaming communities—such as schools, internet cafes, small esports groups, and online forums—will allow gradual expansion while creating deeper social dynamics that boost engagement and retention.

Another potential issue is the relative lack of social features within KGeN’s PC portal and mobile app. As discussed later in this report, enhancing social functionality is a viable way to increase ecosystem engagement. The longer users stay on the platform, the richer their data becomes, increasing opportunities to interact with K-Quest and K-Drop features—and ultimately expanding monetization potential.

4.2 Engaging Users via KGeN Play

KGeN Play serves as the primary frontend interface where most players engage, hosting all reward quests. It marks the typical starting point of the user journey and functions as the main gateway for interacting with the KGeN network while building their PoG reputation score.

KGeN Play is accessible via PC portal or mobile app. The PC version offers the best experience, but the mobile app provides a convenient solution for on-the-go users and will play a vital role in expanding into the Global South.

Upon account creation, a blockchain wallet is automatically generated in the background, storing all user assets and a non-transferable player reputation NFT. Once users meet the minimum withdrawal threshold, they are prompted to verify their phone number via OTP and gain full control of their wallet—this step is essential for direct input into the PoG engine. The KGeN wallet has limited functionality but offers a smooth onboarding process, supports multi-chain and gas-free transactions, and efficiently performs its three core functions: balance viewing, transaction history, and withdrawals.

Before realizing they have a blockchain wallet, users first need to start earning rewards. To do so, they participate in various activities hosted on the KGeN Play portal. Quests are categorized into K-Drops and K-Quests.

Both K-Drops and K-Quests are limited-time events offering rewards in K-Points, leaderboard achievements, K-Cash, or tokens. The key difference is that K-Drops use endpoint API integrations for automatic real-time validation, whereas K-Quests rely on manual verification processes.

Unsurprisingly, quest platforms employing real-world financial incentives—especially those targeting Global South users—see higher-than-average completion rates. KGeN’s uniqueness lies in combining KGeN Play with the PoG engine to deliver high-conversion targeted campaigns.

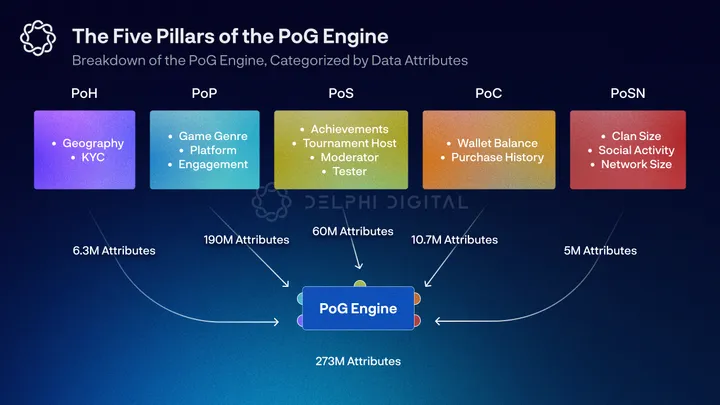

4.3 The PoG Engine

The PoG engine is a decentralized player scoring system hosted by a distributed node network. Composed of five core pillars, each containing five to ten attributes, it tracks player skill, “humanness,” engagement, wealth, and social networks to build a multifaceted, cross-chain reputation system.

The result is a vanity PoG score. Leveraging blockchain’s inherent composability, players can showcase their gamer ID across different ecosystems. Meanwhile, publishers and advertisers can access a competitively priced, highly engaged player base in the Global South via the PoG engine.

The five core pillars are Proof of Humanity (PoH), Proof of Participation (PoP), Proof of Skill (PoS), Proof of Contribution (PoC), and Proof of Social Network (PoSN).

- PoH, as the name suggests, tracks various data points to reduce the likelihood of users being bots. This may include KYC status or the number of connected social apps, making it one of the most valuable attributes in the eyes of publishers. Beyond verifying “humanness,” PoH further segments users based on platform preferences and geography. This pillar enhances both targeting precision and trust in user quality and the overall network.

- PoP determines a player’s engagement with the KGeN network and the types of games they play. It tracks metrics related to retention, gameplay patterns, preferences, and habits. By further differentiating user types, this pillar improves targeting accuracy and is highly valued by publishers.

- PoS recognizes a player’s ability, competitiveness, engagement, and achievements over time. It pulls data from in-game accomplishments, tournaments, and ecosystem activities to rank players. This pillar highlights the most active participants and grants them social capital.

- PoC identifies a user’s monetization potential, derived from direct purchases, on-chain transactions, transaction history, or net worth. This not only increases UA efficiency but also reveals diverse ways users add value. Beyond early-stage activities (like game testing), PoC is poised to become the most valuable dataset for post-IDFA-era publishers.

- PoSN maps the scale of a user’s social profile and builds their social graph within the KGeN network. It filters out non-gaming data, tracking social accounts, tribe activity, and network size to understand their social preferences, influence, and reach within gaming communities.

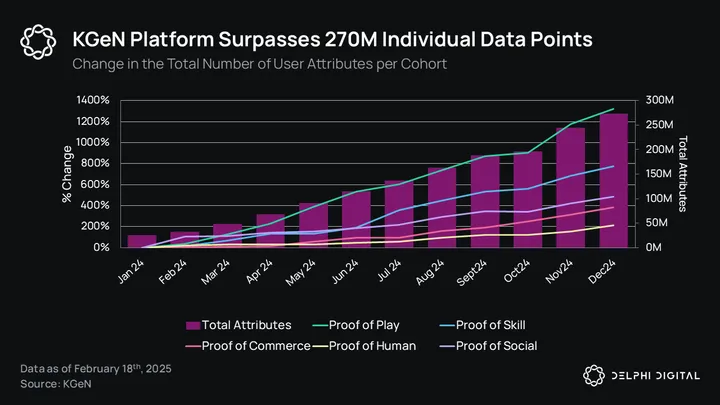

The PoG engine currently comprises over 270 million data attributes from more than 13 million registered accounts and 4.4 million MAUs. Since January 2024, the PoH, PoP, PoS, PoC, and PoSN datasets have grown by approximately 214%, 1,320%, 777%, 384%, and 487%, respectively. The significant growth in PoP and PoS data underscores how ecosystem engagement continues to rise over time.

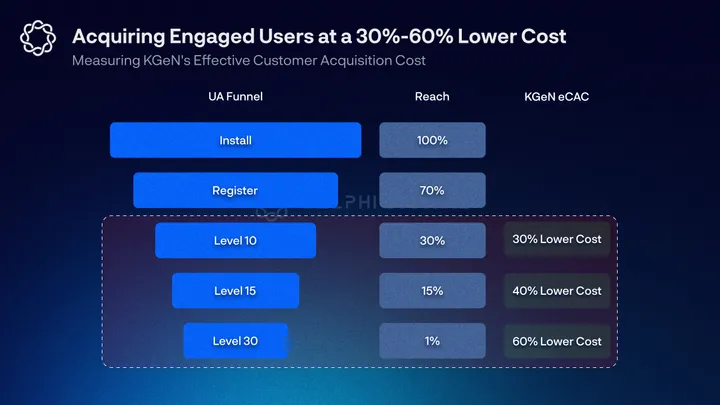

Leveraging the PoG engine, KGeN is pioneering an alternative UA framework called “effective Customer Acquisition Cost” (eCAC). Instead of charging for simple impressions or top-of-funnel installs, KGeN only charges for users who reach mid- or bottom-funnel stages.

For example, in a campaign with Karate Combat, KGeN reported nearly a 40% reduction in eCAC, charging nothing for top-of-funnel installs and achieving a 5% bottom-funnel conversion rate. In a four-week quest campaign with Game7, KGeN claims to have delivered 50,000 PoH-verified users at an eCAC 55% lower than competitors. Events like registration, wallet connection, and avatar creation are free, meaning clients only pay for users who complete at least four tasks and mint an SBT (estimated 20% conversion).

PoH and PoP data are especially valuable, offering commercial clients relatively high ROI on engagement. This is particularly important for Web3 projects using financial incentives, which often suffer from bad actors and bots. However, these data points aren’t flawless—even KYC can be manipulated.

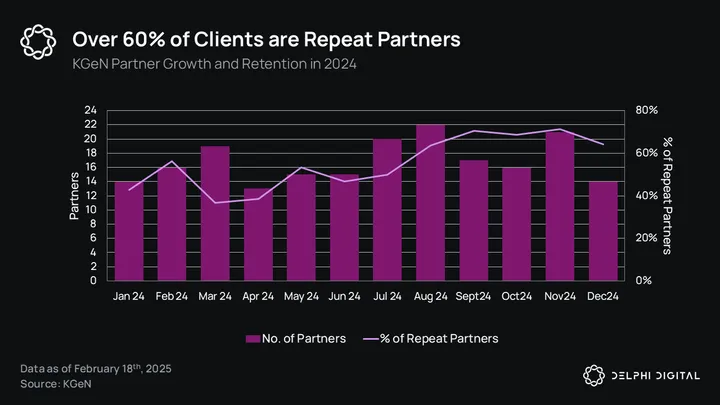

Nonetheless, KGeN’s ability to confidently determine user quality delivers significant added value to its partners. As detailed in this report, ad fraud wastes approximately $84 billion in digital ad spending annually. This explains why over 60% of KGeN’s partners have returned since August 2024.

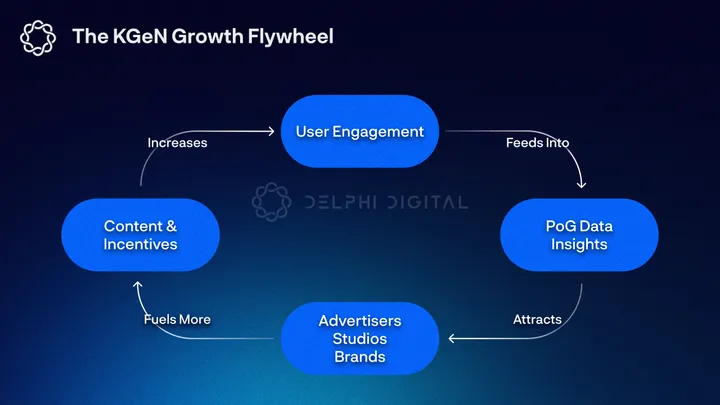

Over time, the growth flywheel crucial to KGeN’s future scalability will gain momentum. As long as there is demand for positive PoG scores, engagement on KGeN Play will increase (further accelerated by financial incentives tied to PoG rankings). This activity fuels the PoG engine, increasing total attributes and enriching KGeN’s user database. More publishers are then drawn to the ecosystem, expanding offerings on KGeN Play and KGeN Store, attracting even more users.

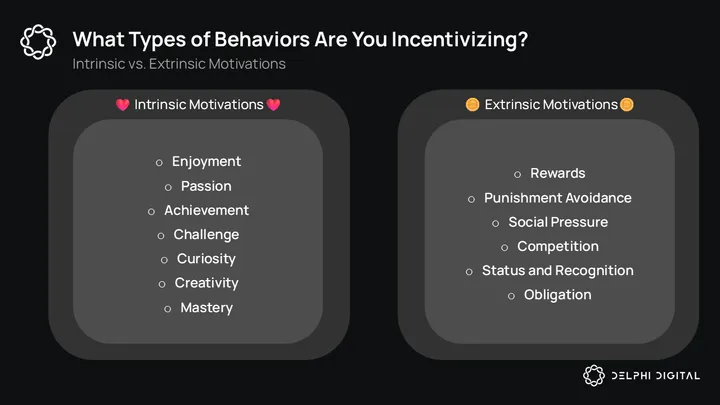

The PoG score is central to KGeN’s business model and key to delivering competitively low eCAC. A critical question remains: what motivates this user behavior?

As long as incentives are financial, the platform will inevitably show promising results. However, this creates extrinsic motivation, shaping how users interact with the platform and its partners.

Users driven by extrinsic rewards are less likely to continue playing games they initially joined for incentives. Moreover, research shows that offering external rewards for intrinsically rewarding behaviors reduces intrinsic motivation—a phenomenon known as the overjustification effect.

Intrinsically motivated users find value in enjoyment, social interaction, recognition, progress, and fun. If strong network effects can transform the core value proposition of PoG scores into something rooted in social capital and enjoyment, motivation will gradually become internalized, increasing the potential value offered to partner publishers.

4.4 KGeN Tokenomics

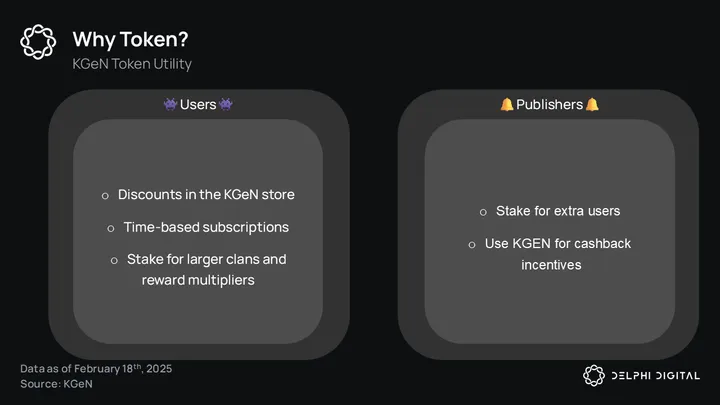

KGeN’s economy will feature two core assets: KCash and the KGEN token. KCash has been live for some time as an off-chain reward currency, though it can also be purchased directly with fiat. Its primary use is in the KStore, where it can buy in-app purchases (IAP), gift cards, or entries to VIP tournaments and quests.

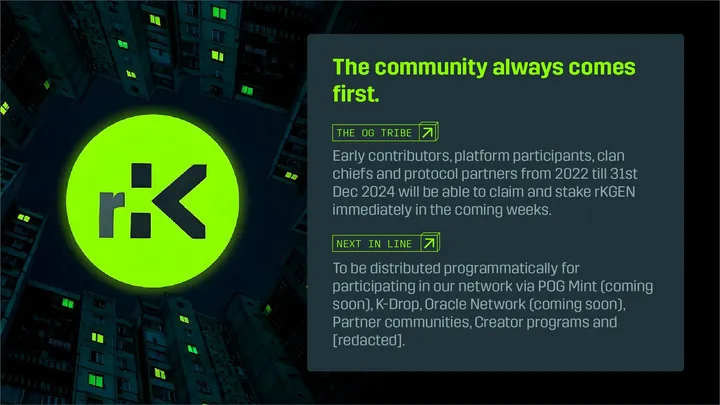

The KGEN token powers the ecosystem’s growth flywheel. A utility token, 40% of the community allocation is reserved (with 8% unlocked at TGE), while team and investor allocations are subject to a four-year lockup. At TGE, 12.6% of the total token supply will be unlocked, excluding circulating supply held by market makers or exchanges.

Recently, KGeN announced a pre-TGE K-Points → rKGEN airdrop campaign. rKGEN allocation is based on a user’s total K-Points, time spent on KGeN, and connectedness. Upon token launch, rKGEN can be converted 1:1 to KGEN. However, select users will be able to stake rKGEN before TGE to earn additional token yields.

The K-Points → rKGEN airdrop model prioritizes transparency and clear communication to maximize community sentiment and token distribution before TGE. If executed successfully, this could help build momentum at launch and secure additional CEX listings, though it carries its own risks.

Ambiguous reward systems have been shown to boost engagement across domains. Pure point-based airdrops, while less transparent, offer teams greater flexibility in token distribution. This design raises a question: post-TGE, will KGeN Play use a K-Points → KGEN reward system, or switch to direct token payouts?

At launch, we assume KGEN will primarily serve as an incentive. Over time, as the network matures, we expect more users to spend KGEN in the KGeN Store, enjoying better discounts than fiat purchases.

Another potential token sink could be subscription fees. As users grow reliant on the network to host their reputation scores, achievements, and social touchpoints, KGeN might limit the number of free tasks available. This would cap much of the network’s earning potential and act as an anti-bot measure.

Nevertheless, unless non-financial rewards hold significant intrinsic value, many users won’t spend tokens unless they see positive ROI. To prevent this from becoming an inflationary sink (more tokens released than removed), KGeN should offer third-party tokens, KCash, or NFTs. Ultimately, the most sustainable sinks are driven by intrinsic motivations like entertainment and social capital.

Beyond direct consumption, staking will also play a role. Beyond users seeking passive yield, tribal leaders can stake tokens to increase member caps and access advanced platform tools. Publishers can participate in tiered staking programs to receive more free top-of-funnel users in their UA campaigns—a feature we expect to grow in popularity if current growth trends continue.

Traditional token staking is an inflationary model, diluting supply to delay sell pressure. While potentially beneficial short-term, it’s encouraging to see KGeN leverage non-inflationary staking incentives for tribal leaders and publishers.

4.5 Oracle Network

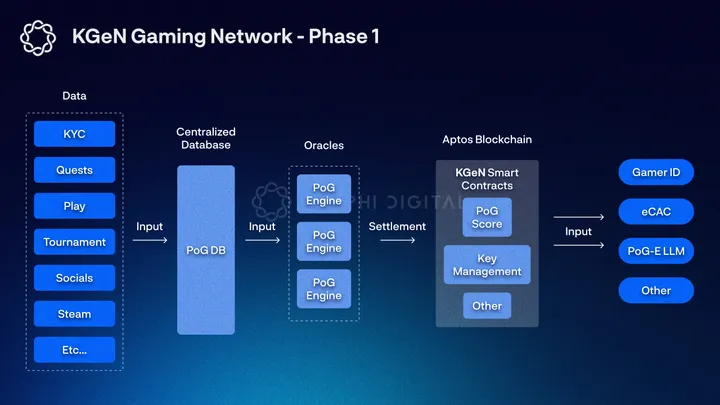

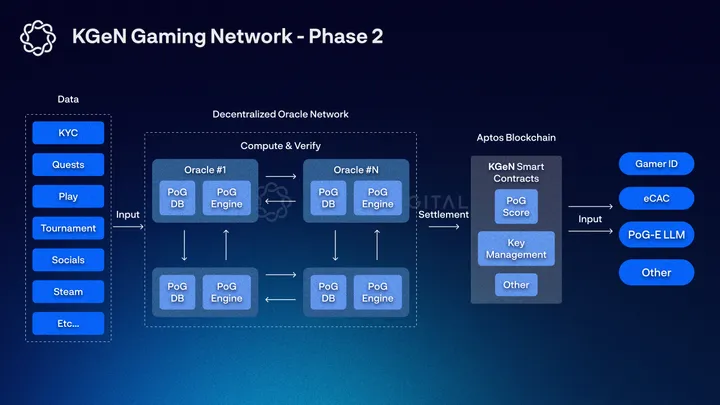

The KGeN oracle network is a distributed system composed of permissioned nodes that collectively form the backbone of the PoG engine. Each oracle stores PoG data, computes PoG scores (and jointly verifies their accuracy), and submits these scores to the Aptos blockchain for settlement. In return for this service, oracle operators receive fixed KGEN token rewards based on revenue projections, plus stablecoin yields proportional to the amount invested in the oracle.

The oracle network progressively decentralizes a process traditionally conducted centrally. This will be a gradual transition, expected to take at least three years. In Phase One, oracles will primarily retrieve PoG data from centralized servers and participate in computation, validation, and settlement—decentralized storage of PoG data begins in Phase Two.

Another core component is the oracle key. Keys are NFTs required to participate in the network. The more a licensed oracle operator spends on their license, the more keys they receive. KGeN has indicated that additional key sales may be opened to the public in the future.

Oracle keys will remain locked until the network transitions to Phase Two, after which they become tradable. Key holders can delegate their keys to oracle operators—a mechanism similar to standard staking, temporarily locking the key NFT in exchange for KGEN token rewards from a key reward pool.

An oracle’s weight in the key reward pool is calculated based on three variables: the number of delegated keys, the protocol’s base reward, and oracle performance. Performance only becomes relevant post-Phase Two, and the exact calculation method has not yet been determined. Base rewards are emission-based and reflect overall network health. Though details remain unconfirmed, the goal is for base rewards to increase for all oracles as network value grows.

The oracle network blends aspects of node and delegated proof-of-stake (DPoS) frameworks to decentralize the PoG engine. Under a fully centralized model, KGeN’s central data center represents a single point of failure for data corruption or deletion. Additionally, core stakeholders (players and publishers) must accept trust assumptions that PoG scores haven’t been manipulated.

In this context, the benefits of decentralization are somewhat subjective for users. In certain circles, it’s hard to imagine a player actively complaining about the centralized nature of their Xbox Gamerscore or Steam account. Similarly, publishers prioritize scalable UA over decentralization.

Yet this overlooks the potential network effects and aligned incentives enabled by a token model. By giving stakeholders a pathway to benefit from KGeN’s growth, you create brand advocates who support the project. If KGeN’s growth flywheel translates into positive token price action, more stakeholders will be drawn in, accelerating network effects further.

5. Competitive Landscape

KGeN is not the only company pursuing this vision. As previously discussed, distribution is widely seen as one of the gaming industry’s greatest current challenges. Whether scaling user acquisition (UA) profitably or optimizing core engagement metrics through improved player liquidity, multiple players are tackling these issues with varying degrees of success.

Next, we analyze key companies operating in both Web2 and Web3 markets, compare their business models, identify potential opportunities, and highlight critical considerations.

5.1 The Kings of AdTech: Past and Present

In the Web2 space, two notable examples exhibit strong synergies with KGeN’s current business model while revealing key growth opportunities. The first is Facebook, whose strength lies in deep user profiling and behavioral analytics. The second is Applovin, a sophisticated

Bienvenue dans la communauté officielle TechFlow

Groupe Telegram :https://t.me/TechFlowDaily

Compte Twitter officiel :https://x.com/TechFlowPost

Compte Twitter anglais :https://x.com/BlockFlow_News