On-Chain Options Sector Overview: From Opyn to Rysk, Who Has Successfully Navigated DeFi's Most Challenging Sector?

TechFlow Selected TechFlow Selected

On-Chain Options Sector Overview: From Opyn to Rysk, Who Has Successfully Navigated DeFi's Most Challenging Sector?

The Rebirth of On-Chain Options: After 11 Protocols Were Wiped Out, the Sector Finally Found a Way to Survive.

Author: Castle Labs

Compiled by: TechFlow

TechFlow Editor's Note: Options have become the dominant force in derivatives on global exchanges, with contract volume in 2024 being 4 times that of futures, and daily option premium trading volume in the US reaching $36 billion. However, on-chain options were once one of the most brutal failures in the crypto world, with 11 protocols such as Opyn, Hegic, and Ribbon failing one after another. Now, with improved infrastructure, growing institutional demand, and prediction markets educating users, on-chain options are finally rebuilding from the ruins, with 30-day notional trading volume reaching $1.44 billion. This ecosystem landscape explains why this time might be different.

Options in Financial Markets

Most people don't realize they are actually trading options their whole lives.

If you have bought insurance, you paid a premium in exchange for conditional compensation in the future. This is a put option, because you are protecting yourself against a decline in the value of the insured asset. If you have a mortgage, you hold the right to refinance early. This is a call option, because you have the exclusive right (but not obligation) to "redeem" or cancel the current debt contract.

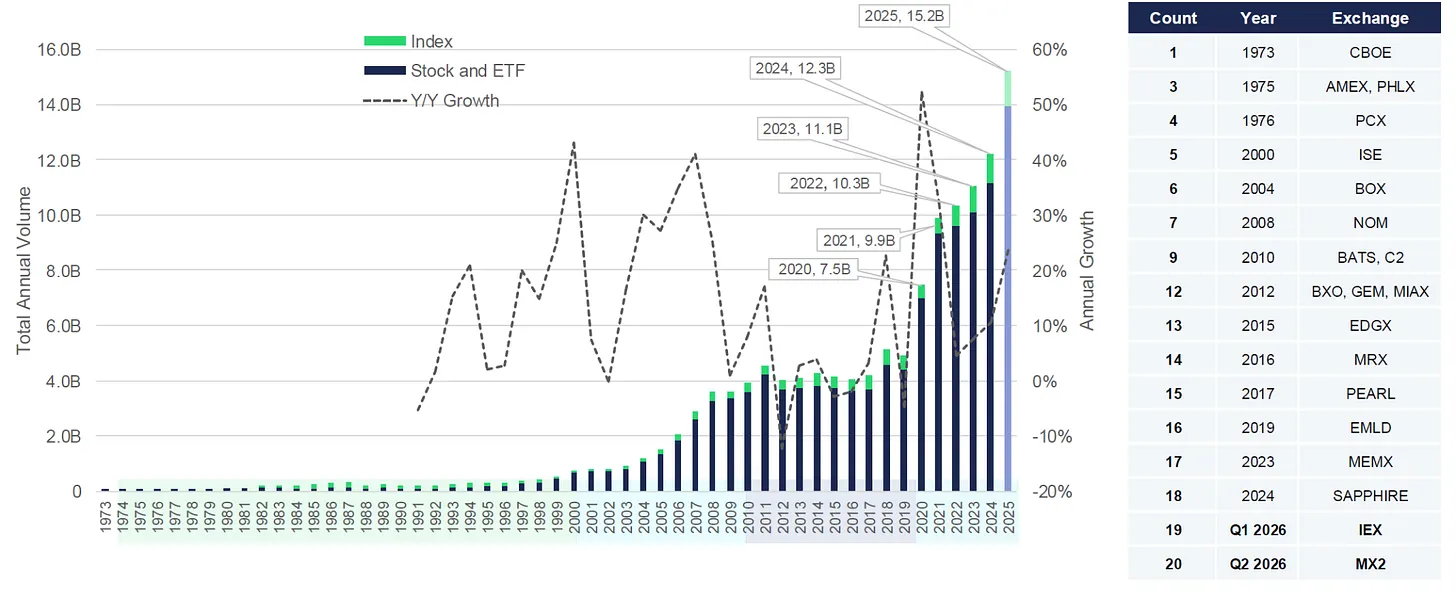

Options now far exceed futures in trading volume on global exchange derivatives. Option contract volume in 2024 was more than 4 times that of futures. Listed options in the US set records for the sixth consecutive year in 2025, with about 15.2 billion contracts traded, equivalent to about $36 billion in premium trading per day.

Zero Days to Expiration (0DTE) options for SPX alone broke $1 trillion in daily notional value at peak times, with an average of 2.3 million contracts per day, accounting for 59% of the product's total trading volume in 2025. 0DTE options expire on the trading day; they are used to chase huge quick returns from intraday stock volatility, but also carry the risk of losing 100% of the investment quickly.

In 2024, the National Stock Exchange of India (NSE) accounted for about 84% of global equity option contracts; but in terms of value, the total premium paid by US option buyers was still about 4 times that of India. This indicates that the Indian retail public is trading a large number of tiny contracts, while US participants trade fewer contracts, but with larger size and higher prices.

The appeal of options is also entering crypto products, although currently mainly from institutions.

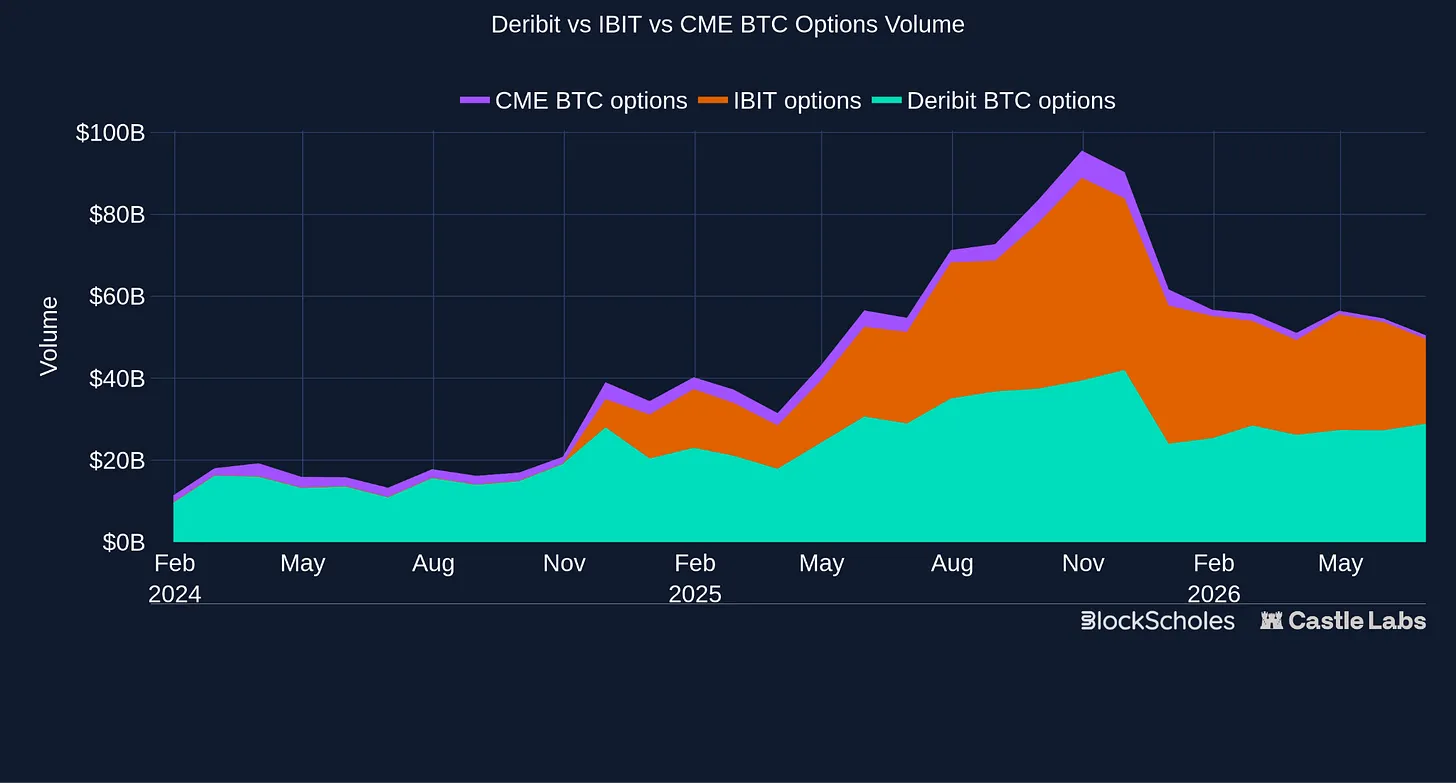

CME, the largest regulated derivatives exchange in the US, now offers 24/7 crypto options. This is an unprecedented shift by traditional exchanges to retain their user base, recognizing the appeal of the 24/7 crypto market. Additionally, in April, open interest in BlackRock IBIT options exceeded BTC on Deribit, rising from $26.9 billion to $27.6 billion, despite Deribit launching more than 10 years ago.

Options are extremely flexible tools that can play a role in a wide range of applications:

Hedging: Using options as insurance policies for price exposure (buying put options to lock in a hard floor on downside losses, or buying call options to prevent missing sudden upward moves)

Yield: Selling options to obtain stable cash premiums from the market. This is useful for non-directional users who can generate passive income with existing assets (covered calls), or get paid in advance while waiting to buy the dip (cash-secured puts)

Speculation: Expressing views on price or volatility without directly purchasing the asset, whether regarding direction, timing, or specific price moves (this can be achieved through a series of option strategies)

Customized Strategies: Combining multiple options into structured products, often used by banks and asset management companies to create yield products or downside protection notes

User profiles are widely distributed in financial markets. From institutional market makers hedging risk and banks packaging yield, to volatility funds trading market volatility and retail investors speculating on cheap intraday 0DTE volatility.

Early On-Chain Attempts

Given their prominent role in traditional markets, options were considered tools with natural product-market fit in the volatile on-chain crypto market. The result, however, was one of its most repeated failures.

This was certainly not for lack of experimentation, as seen from products launched in previous cycles:

Opyn tokenized vanilla options on Ethereum in 2019, but thin liquidity, high collateral requirements, and high fees on the mainnet hindered it.

Hegic attempted a pool-to-peer model in 2020, simplifying the buyer experience, but pooled LPs bore risks that were difficult to hedge.

Ribbon, Friktion, and Dopex opened vaults in 2021, creating simple deposit-and-earn structured products for users seeking yield without managing positions, but volatility was sold into thin cyclical demand, compressing yields until premiums could no longer exceed risk.

Lyra, Premia, Pods, and Siren experimented with option AMMs, attempting to provide continuous liquidity between strike prices and expiration dates, but encountered difficulties in pricing and hedging. LPs inherited complex volatility and inventory risks, while organic traffic remained thin.

In 2022, Opyn launched Squeeth, a perpetual contract tracking ETH squared exposure, allowing users to gain convexity without managing periodic options. Launched on Ethereum, fees were high, the product was difficult to explain, and holding costs were expensive when funding rates were high.

The industry was repeatedly hindered, mainly limited by structural constraints. Weak market maker participation made two-way liquidity at trading venues thin and pushed difficult-to-hedge risks onto passive LPs. Low capital efficiency accompanied unreliable volatility surfaces, while user experience was stuck in no man's land: too complex for retail, but lacking the professional architecture required by institutions.

New Infrastructure and Improvements

Since these early attempts, conditions have continued to improve:

Rollups and Ethereum scaling reduced gas fees, making complex on-chain operations affordable, while improving execution and settlement.

CLOBs and RFQs began to replace AMM models, creating a more natural environment for professional traders and market makers, enabling them to quote specific strike prices and expiration dates, update prices in real time, and control risk more effectively.

Simplified products target narrower audiences, as trading venues focus on launching specific products for specific users.

Prediction markets made option-like payoffs accessible to mainstream retail through binary outcomes, normalizing conditional yield trading

Institutional demand for crypto options has been steadily growing, mainly through Deribit, and recently through IBIT and CME.

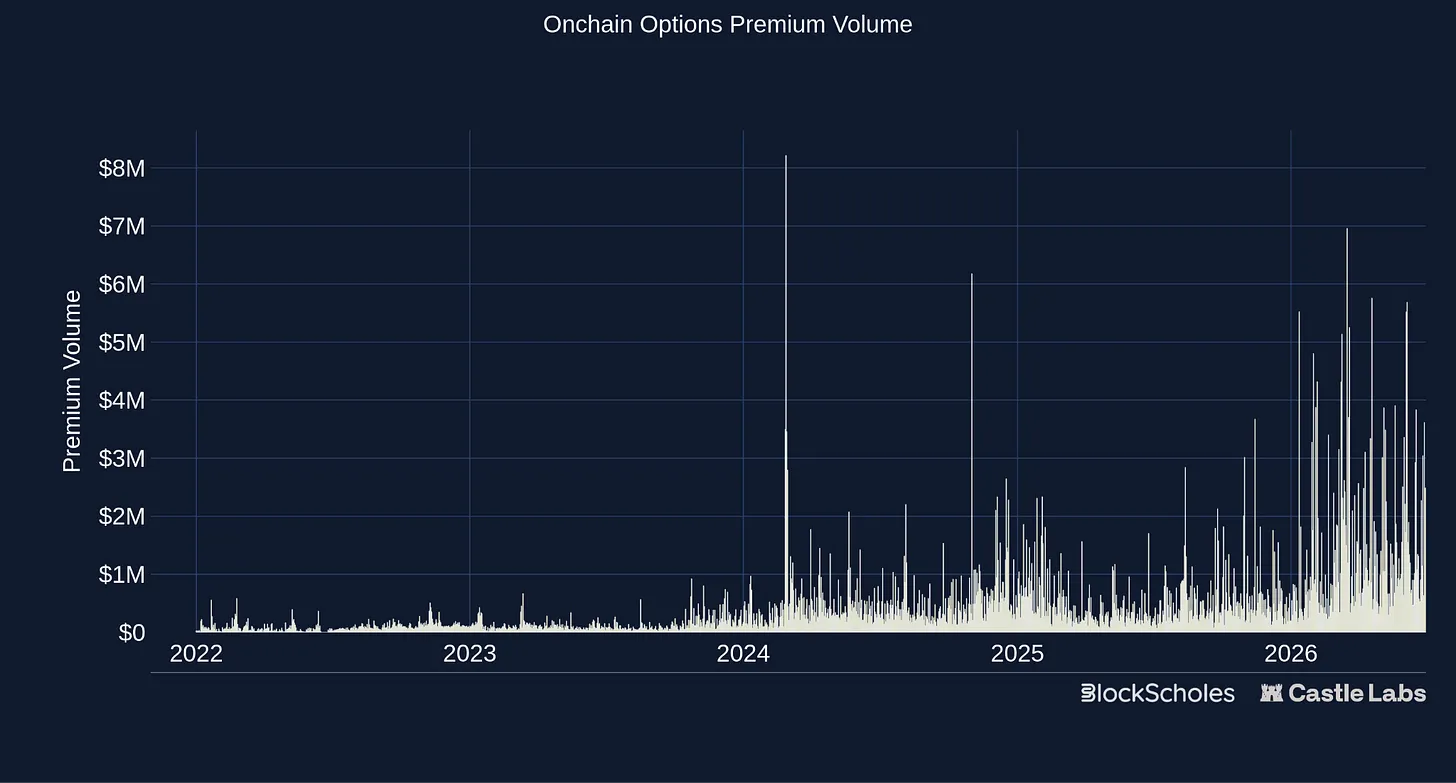

On-chain conditions have also improved, with stronger option markets beginning to form, 30-day notional trading volume reaching about $1.44 billion, and premium trading volume hitting record highs this year.

The resulting category looks very different from the first DeFi options cycle. Protocols are no longer simply trying to be on-chain Deribit; the ecosystem involves many participants ranging from institutional trading venues and ETF wrappers to on-chain vanilla options, novel exotic options, and binary options operating through prediction markets.

In the following sections, we will delve into the current options landscape, focusing on what is happening on-chain.

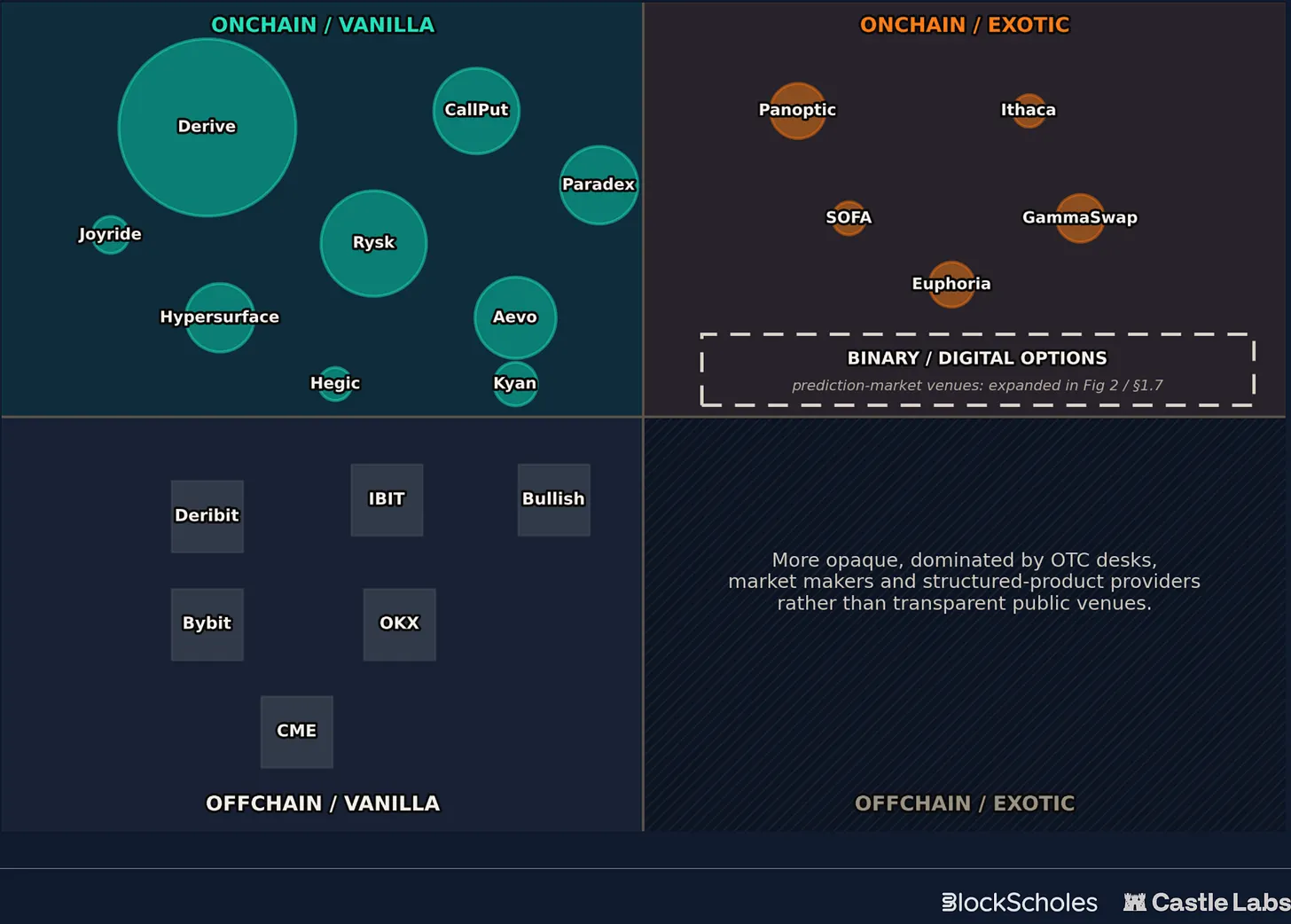

Crypto Options Ecosystem

The crypto options landscape is a set of adjacent markets with different settlement and payoff types. The map below divides the ecosystem from these two dimensions:

Settlement: On-chain to Off-chain

Payoff: Vanilla to Exotic

Off-chain vanilla options remain the clear leader, led by Deribit, IBIT, and CME, as well as CEXs like Binance and OKX. On-chain vanilla trading venues are beginning to rebuild liquidity around CLOBs, RFQs, and more simplified user-centric products, while settling trades on-chain.

More experimental products lie within on-chain exotic options, using option or option-like payoffs as building blocks, rather than simple listed calls, puts, and spreads. Examples include:

Perpetual Options: Replacing fixed expiration dates with streaming premium mechanisms. This allows traders to hold volatility positions indefinitely without the friction and gas costs of manually rolling contracts.

AMM Native Options: Creating option-like exposure from AMM liquidity positions rather than listed calls and puts. This allows advanced yield farmers to hedge impermanent loss, and allows long-tail asset speculators to buy calls and puts on newer unlisted tokens.

Short-Term Touch Options: Providing instant fixed payouts at the exact moment an asset touches or breaks through specific price targets. This structure is heavily used by retail intraday traders, scalpers, and event-driven news traders who chase quick feedback loops during brief bursts of extreme intraday momentum.

The fourth quadrant—off-chain exotic options—is more opaque, dominated by OTC desks, market makers, and structured product providers rather than transparent public trading venues.

This report focuses on the on-chain side of the map, covering vanilla option trading venues and exotic option primitives, then turning to binary option-like markets, most commonly expressed as prediction markets.

On-Chain Vanilla Option Venues

Recent on-chain vanilla options have made obvious progress, not by changing the payoffs themselves, but by refining surrounding infrastructure, product design, and user experience. These platforms generally shifted from passive LP pools to CLOBs and RFQs, leaving room for portfolio margin and yield-bearing collateral, while launching more targeted yield products to simplify outcomes for users.

This section will introduce several of the most prominent platforms currently.

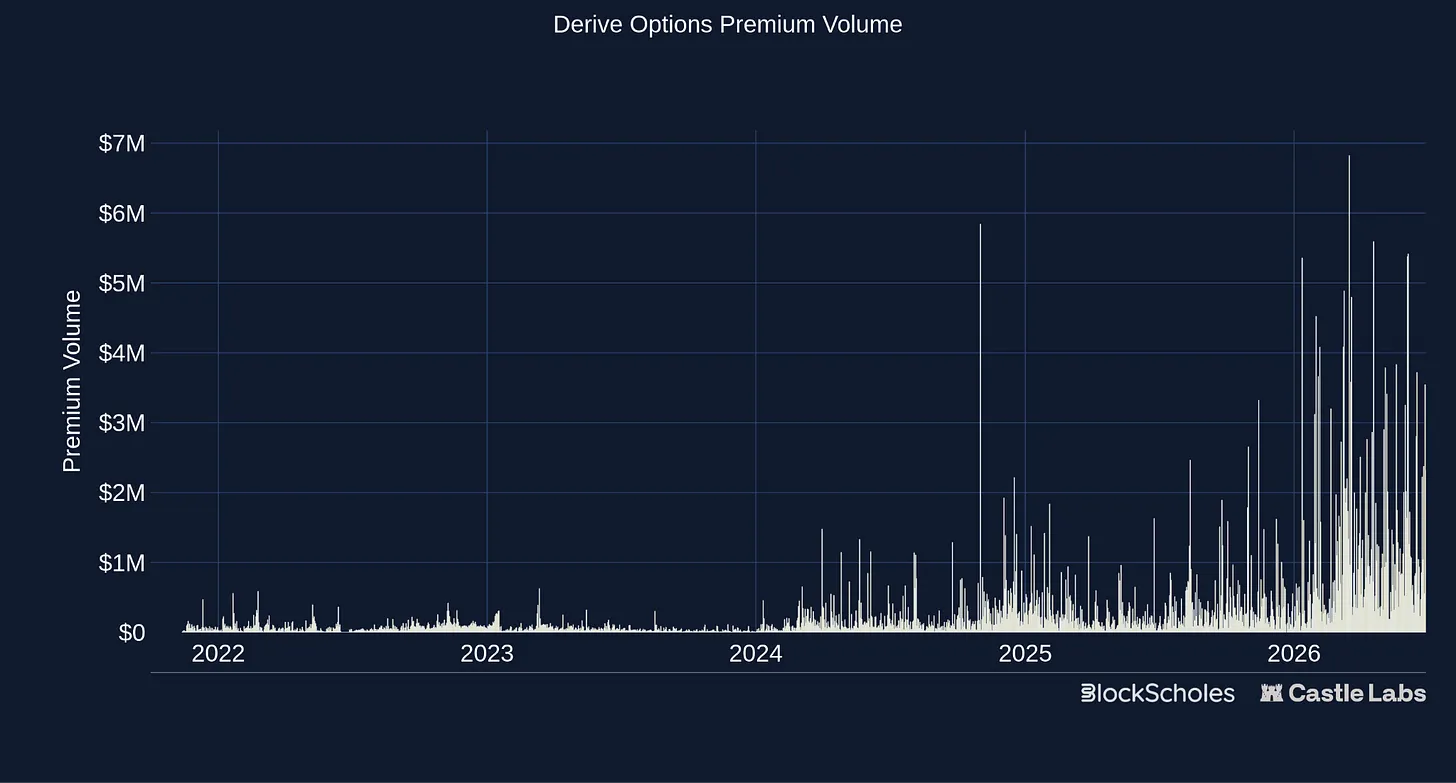

Derive

Derive is a typical example of this architectural shift. It evolved from Lyra, an option AMM, into the CLOB-based platform we see today. Nowadays, Derive runs on its own OP Stack L2, providing cross-margined options and contracts through a professional order book interface. Derive does not attempt to hide the complexity of options from users, so the target users are professional traders, market makers, institutional users, and other sophisticated volatility traders. It looks very much like a traditional option exchange, offering a range of assets, strike prices, and expiration dates that can be combined to create customized payoff structures.

Using an off-chain matching engine for instant execution, while using on-chain L2 for settlement, allows institutional allocators to trade at the speed of centralized exchanges (CEX) like Deribit, while maintaining non-custodial ownership of assets. Derive also offers a range of vault products; unlike previous attempts, these products utilize the underlying exchange to execute predetermined option strategies, aiming to earn yield for depositors.

Derive currently accounts for the majority of on-chain option activity, with 30-day notional value of $1.142 billion and premiums of $44.3 million, accounting for 79.2% and 87.2% of the category respectively. It should be noted that Derive uses market maker rewards, OP incentives, DRV rewards, and rebate programs to support liquidity.

Despite incentives for liquidity and participation, Derive still demonstrates the industry's development over the years; mature option exchanges now run on high-performance application chains accessible to institutions and market makers.

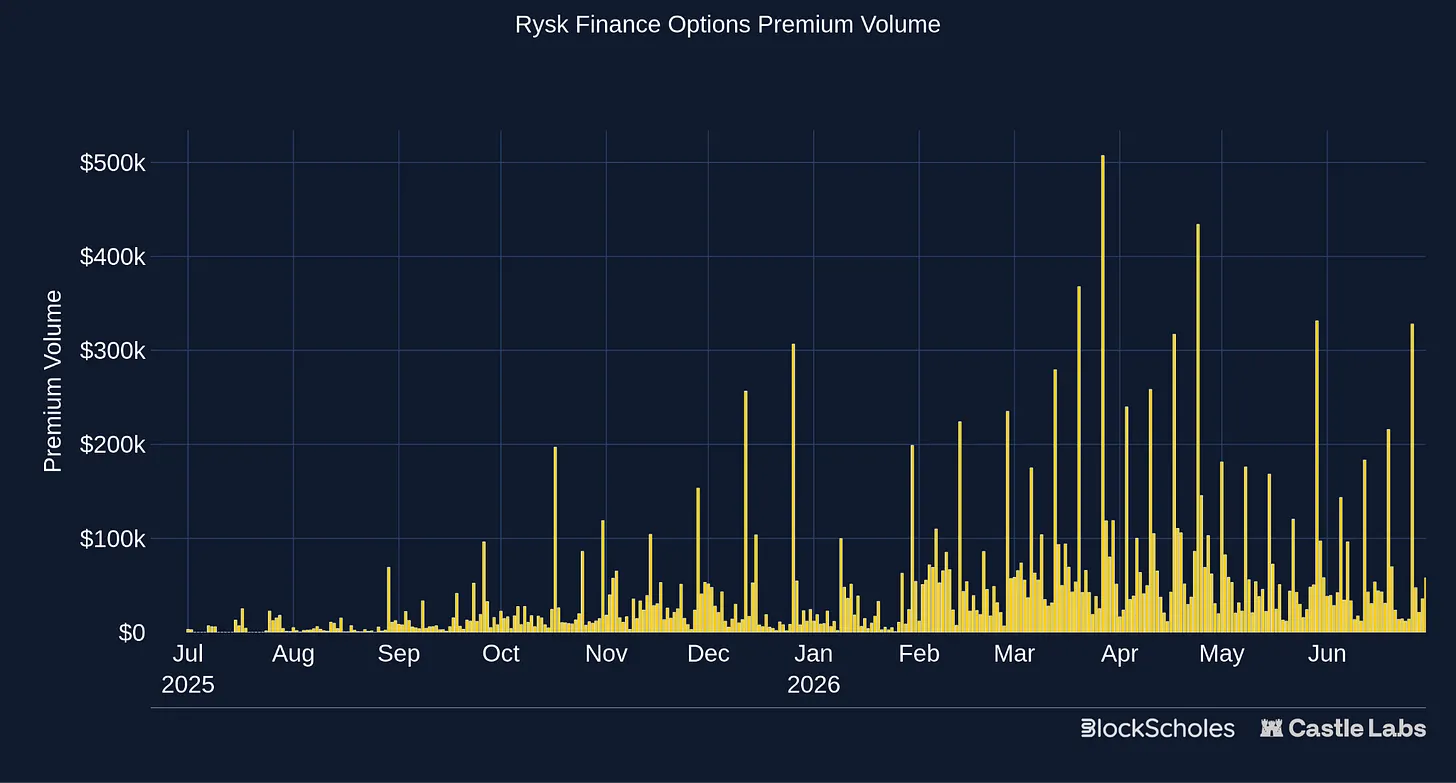

Rysk

Rysk takes a completely different approach from Derive. It is built around covered calls and cash-secured puts, using options as prepaid yield products while keeping strike prices and expiration dates optional, unlike past option vaults. It routes user demand through an RFQ system, where market makers quote on specific requests, purchase the option flow, and manage their own risk elsewhere. Rysk focuses on simplifying the complexity of option products, making them attractive to both retail and institutional investors through robust asset selection, clearly defined outcomes, and a seamless user experience.

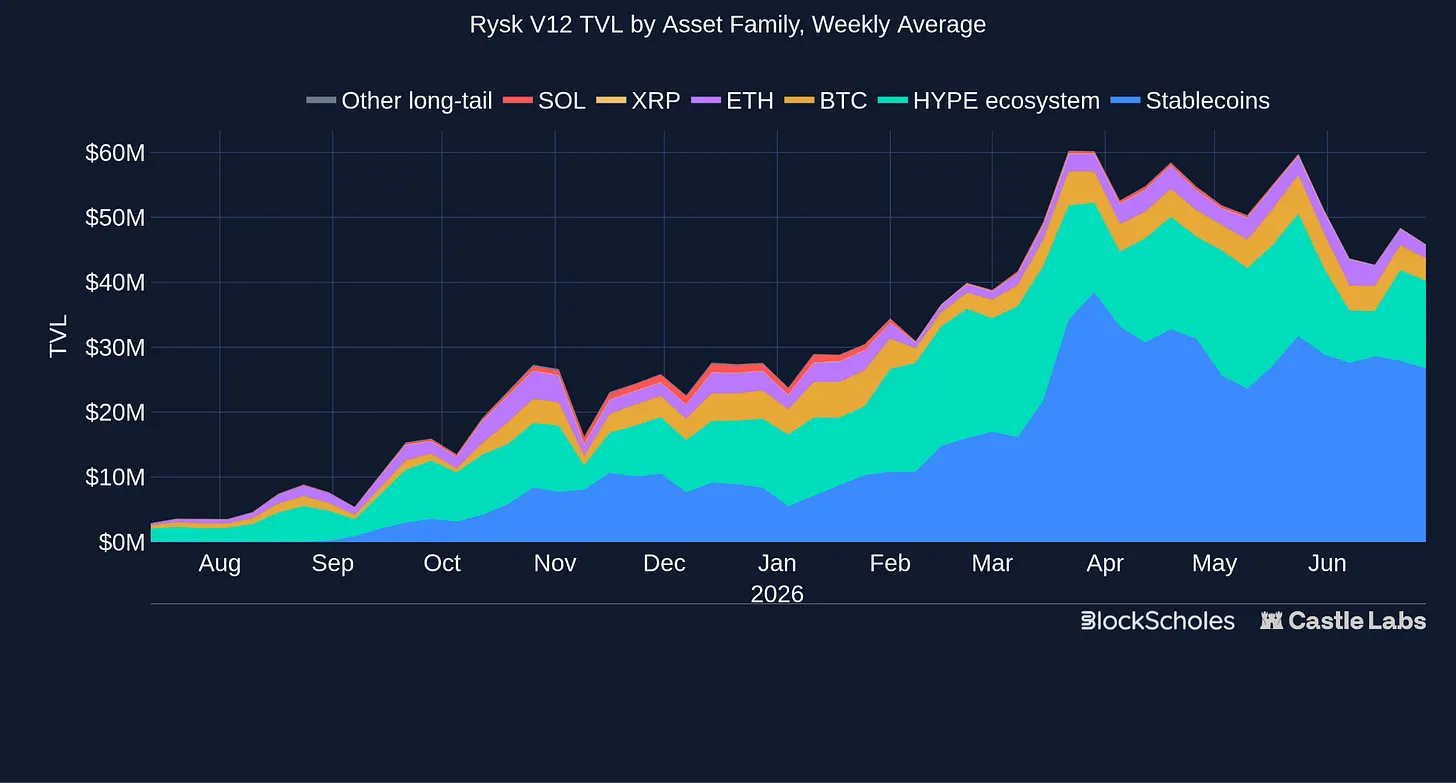

For users, the product is simple. Earn yield on your assets while agreeing on a price level at which you are willing to sell or buy. This is reflected in a broad base of actual users. They all want to earn yield, but achieve it in different ways and with different strategies. Treasuries, DAOs, and funds are long-term holders who already have views on what price level they are willing to buy or sell assets at; even if they don't want to do so, they can still earn yield on further out-of-the-money strike prices. On the other hand, institutional users, such as Hyperion, a Nasdaq-listed HYPE treasury company, run selected vault strategies on Rysk infrastructure. Its mission is to accumulate HYPE, so cash-secured put strategies are a natural choice, placing orders at lower price levels while earning yield for them.

Rysk generated $136.3 million in notional value and $1.94 million in premiums over the past 30 days, accounting for 9.5% of the category's notional value. Rysk's monthly notional trading volume grew from $50 million in January to $182 million in May, remaining above $175 million in March and April as well.

Unlike Derive, TVL is more relevant to Rysk, as the product is based on collateralized option selling strategies. To receive premiums, you need to deposit all collateral, whereas in Derive, users can buy cheap options with low premiums to pursue large gains.

Rysk found a different product-market fit in the options space, repositioning options from trading tools to yield products based on selling volatility. As yields across the industry compress, this has become highly competitive relative to lending, staking, and basis products, as proven by strong continuous growth since launch.

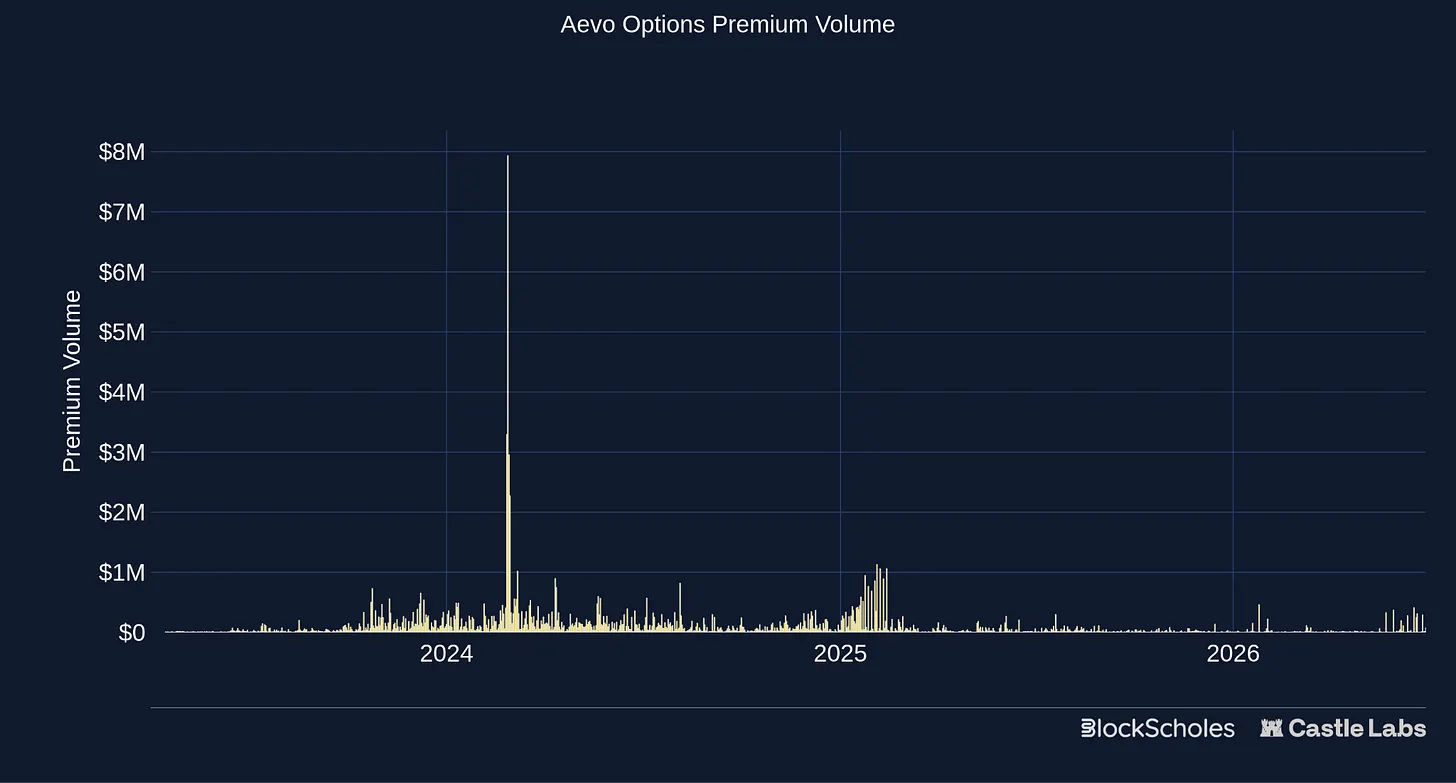

Aevo

Like Derive, Aevo evolved from an early option product into an order book exchange. It evolved from Ribbon Finance, one of the earliest major DeFi Option Vault (DOV) products, before shifting to a broader derivatives platform. Today, Aevo offers options as well as contracts, pre-launch markets, OTC, and automated strategies on a custom L2, using off-chain order matching and on-chain settlement. Orders are matched within microseconds via an off-chain Central Limit Order Book (CLOB) to replicate the CEX user experience, but user funds remain securely stored in on-chain smart contracts hosted on a custom OP Stack Ethereum L2 rollup.

Aevo launched in 2023 and saw the most active option activity during 2024. Since then, reported TVL and visible option activity have declined from early highs, although option premium trading volume has recently begun to rise again.

Aevo's main unique selling point is offering multiple products within a unified margin account. This includes pre-launch tokens, allowing users to trade highly leveraged options and contracts on these highly anticipated unreleased tokens before they enter the spot market.

Aevo generated $45.1 million in notional value and $2.52 million in premiums over the past 30 days, accounting for 3.1% of on-chain option notional value. Monthly notional value grew from $20 million in January to $50 million in May, but real-time option open interest is only about $3.6 million, far below Derive, and also below the open interest notional value proxy calculated by Rysk.

Incentives may support part of the activity. Aevo distributes 1 million AEVO weekly through trading rewards, with 30% reserved for options, which may partially explain the recent rise in option trading volume. Although Ribbon was one of DeFi's earliest option teams, focusing on option vaults, Aevo's migration to a broader derivatives exchange drew attention to contracts, pre-launch markets, and trading activity. Options now look more like a secondary product with lower focus rather than the core business; while the team is obviously working to boost activity there, whether these incentives can fully revitalize Aevo's option market remains to be seen.

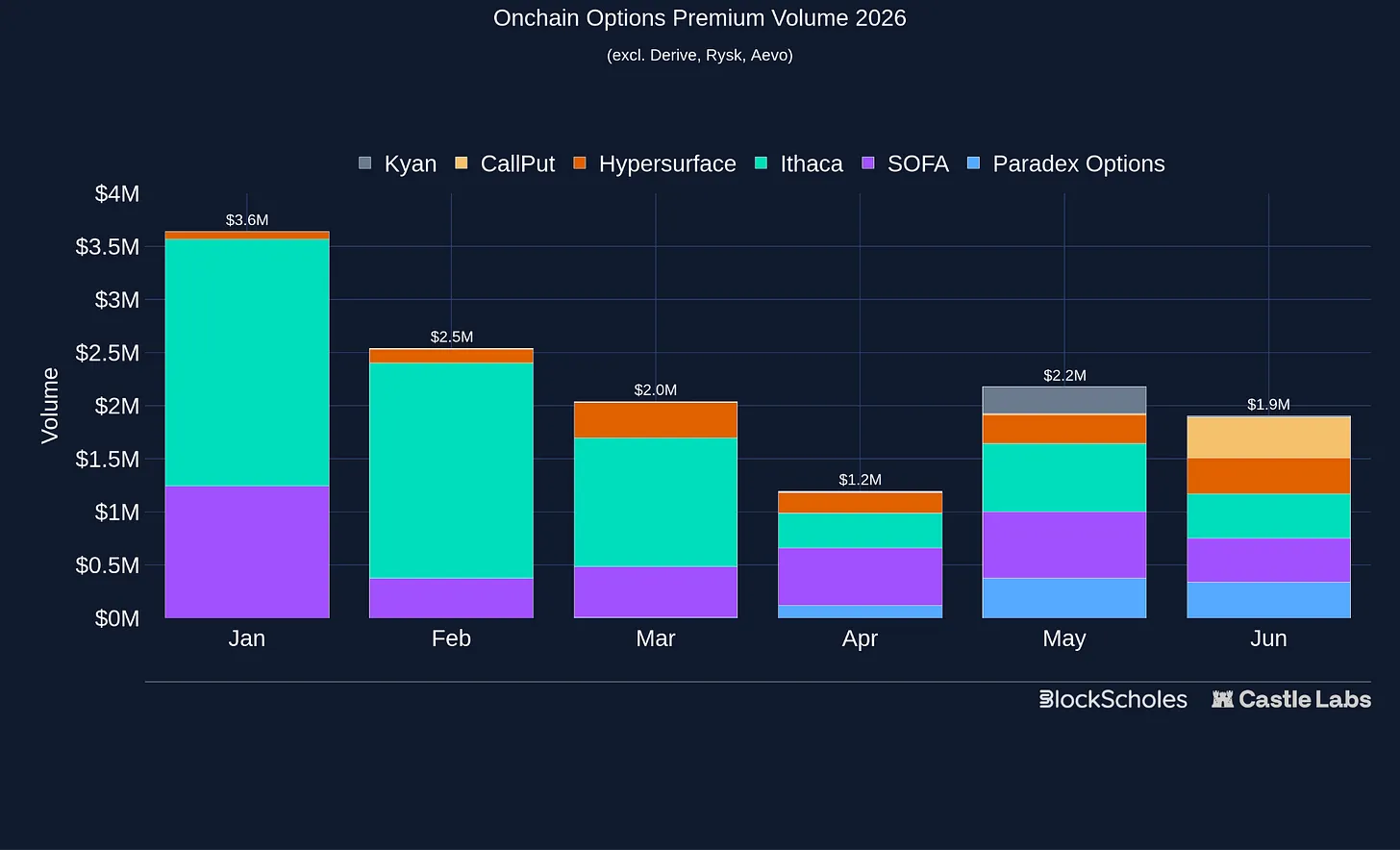

Other Platforms

Below Derive, Rysk, and Aevo, the rest of the market is smaller and fragmented.

Paradex is another broad derivatives platform built by the Paradigm.co team, which is a provider of institutional crypto derivatives liquidity. Currently offering contracts, options, and various Vault Traded Funds (VTFs), Paradex previously supported perpetual options but recently paused this feature, focusing on expiration options opened in April this year. To further encourage traders and gain market share, they reintroduced zero-fee trading for contracts, spot, and options.

Hypersurface looks more like Rysk, using covered calls and cash-secured puts to offer yield products on HyperEVM. CallPut's scope extends beyond crypto, distinguishing itself from other platforms by offering a range of stocks (including SPCX, TSLA, NVDA, and COIN) on its vanilla call and put option exchange, which operates through request-based execution and protocol-managed liquidity.

Kyan evolved from Premia into a broader derivatives exchange, using an order book-based model and supporting RFQ. It offers portfolio margin and multi-leg combination trading to build more customized positions.

Ithaca offers a wide range of options, strategies, and structured products, recently integrating AI agents into its protocol for managing option strategies.

SOFA.org offers structured products, packaging option-like outcomes into products like Earn and Surge, rather than letting users trade options directly.

The market is becoming more diversified at the lower end, with new entrants like Kyan, Paradex, and CallPut gaining shares of premium trading volume in recent months.

Many protocols are now building better infrastructure, but infrastructure is not enough. Order books, RFQs, cross-margin, and portfolio margin do not create demand by themselves. Users still need a reason to choose options over contracts for directional exposure, or prediction markets to trade events. Demand is most obvious when options are relevant to specific asset holders' problems, like the Rysk and HYPE example: they provide yield for newly wealthy HYPE holders, the ability to manage entry and exit, and a way to monetize exposure without simply selling assets. To achieve stronger growth, teams need to build user-specific products that contracts and prediction markets cannot easily replicate.

On-Chain Exotic Options and Short-Term Option Primitives

By exotic options and short-term option primitives, we refer to option-like products beyond simple listed calls, puts, and spreads. These products may remove fixed expiration dates, derive exposure from AMM liquidity, or settle based on whether prices reach specific areas within short time windows.

On-chain vanilla options are undoubtedly becoming more sophisticated and professional, but they still largely replicate familiar off-chain products. On the other hand, exotic options and short-term primitives expand the design space and use cases, attempting payoffs that are harder to achieve through standard listed options: perpetual convexity, AMM native exposure, and ultra-short touch markets. Most of these ideas are commercially unverified, often solving interesting payoff design problems before solving user need problems.

Perpetual Options

Perpetual options remove the expiration variable from the equation. Instead of choosing a fixed expiration date, traders hold continuous convexity exposure funded over time, much like perpetual futures contracts, but with greater upside potential. Squeeth is a historical example, providing users with exposure to ETH², and Paradex also tested perpetual options, although its current real-time option market only has expirations.

The problem is that, especially compared to traditional contracts, removing expiration dates does not eliminate complexity. Users still need to understand convexity, but now also need to manage continuous funding or premium costs, and decide when holding exposure no longer justifies the yield. This undermines one of the core advantages of standard options: knowing in advance the premium you will pay and the payoff. Perpetual options remain an interesting primitive, but have not yet made products simpler or more widely adopted.

AMM Native Options

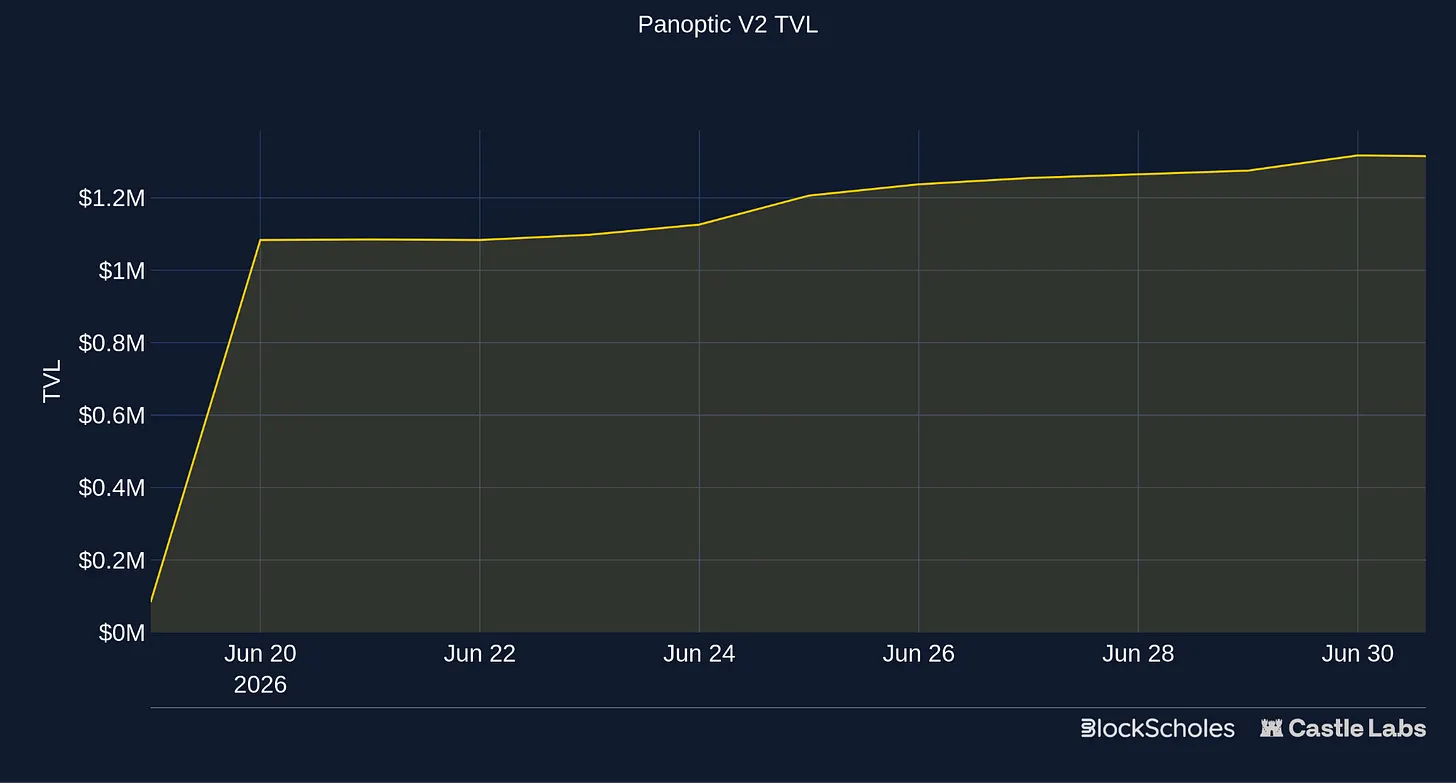

Traditional option platforms分散 liquidity across various strike prices and expiration dates, requiring market makers to update quotes after every price move. Despite improvements from faster, cheaper chains, this remains a daunting task, especially on Ethereum mainnet, and often relies on off-chain matching. Panoptic and GammaSwap instead use AMM liquidity to create option-like exposure.

Panoptic uses Uniswap V3-style liquidity ranges to create perpetual options. Instead of paying a fixed upfront premium for a fixed expiration date, buyers pay streaming premiums over time, while liquidity ranges serve as the basis for strike prices and option exposure. This way, options can be created for long-tail assets already trading on AMMs without a separate order book. Panoptic V2 just launched, offering perpetual option trading for ETH and SPCX. On the other hand, depositors can enter the Unicorn vault (keeping delta neutral and scalping gamma), or the PLP Vault (earning Uniswap fees, Panoptic premiums, and lending fees using deposited ETH liquidity).

GammaSwap took a different angle in its V1, allowing users to borrow AMM liquidity and create perpetual option exposure. This makes hedging impermanent loss or speculating on token volatility possible without oracles.

These products are the most complex DeFi native designs in the category. For example, Panoptic, while removing expiration fragmentation, also introduces streaming premiums, liquidity width, and AMM range mechanisms, meaning product users need to be familiar with Uniswap V3 and the complexities of providing liquidity. On the other hand, GammaSwap has now fully transformed, hoping to overcome its capital efficiency and complexity issues by using order books to create binary markets focused on crypto. This provides users with simple convexity trading without liquidation risk. In these markets, users either win if correct, or lose if wrong.

Short-Term "Touch" Options

This category may be furthest from standard calls and puts. Instead of buying upside or downside exposure at fixed strike prices and expiration dates, users choose a simple condition within a short time window: will the price enter this zone, will it end above this level, or will it settle in-the-money within the next few minutes?

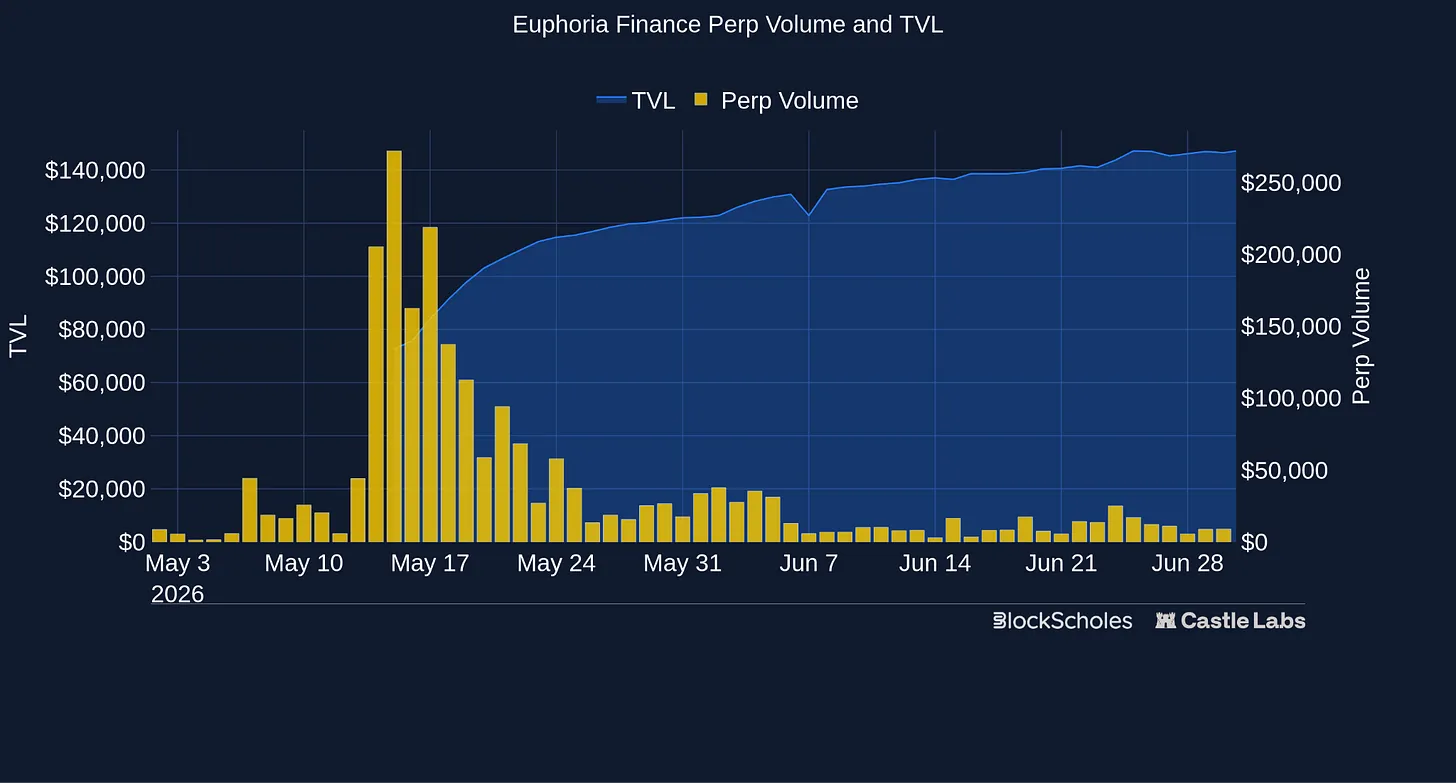

Euphoria's Tap Trading is the latest on-chain case of this design. Users select a grid square, representing a price range within a five-second window. Payouts are quoted in advance by professional market makers, varying based on distance from spot price, time to expiration, and volatility. If the price enters the selected area before expiration, the trade wins. If not, the trade expires worthless.

This product's direction is similar to GammaSwap V2's binary markets. Target users want to bet on crypto prices within increasingly short time frames, so the product competes less with traditional option exchanges and more with perpetual contracts, prediction markets, and mobile gambling. Its appeal lies in simplicity: users can quickly understand the trade, gain convexity exposure, without managing funding rates, liquidations, Greeks, or time value decay.

Why Options and Prediction Markets are the Same Tool

The emerging popularity of prediction markets among retail participants is the first real case of non-linear return products gaining significant attraction on-chain.

But users trading these products rarely know that prediction markets for financial assets, such as BTC up/down markets, are structurally identical to binary options, which are well-known and well-studied tools in traditional finance. Each contract pays a fixed amount if conditions are met at expiration, otherwise $0.

This article is excerpted from our research on the on-chain options renaissance, depicting options (and prediction markets) as an extension of trading tools, and the volatility pricing them, released in collaboration with Block Scholes.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News