MicroStrategy Will Not Die from This Decline: Reflexivity, STRC Re-anchoring, and the “Sell Stocks, Not Bitcoin” Self-Rescue Logic

TechFlow Selected TechFlow Selected

MicroStrategy Will Not Die from This Decline: Reflexivity, STRC Re-anchoring, and the “Sell Stocks, Not Bitcoin” Self-Rescue Logic

Selling tokens for cash is merely a short-term fix—like drinking poison to quench thirst—that resolves immediate issues but creates endless future problems.

Author: @bonnazhu, Bonna | U-Lacto

This recent STRC联动 (co-movement) and sharp decline may well be the best financial case study of this cycle.

Long-read warning applies—and the analysis carries a strong personal bias.

TL;DR

- If MSTR does ultimately fail, it will still fail due to reflexivity—but not this time.

- STRC’s return to its par value anchor is merely a matter of time—this is inherent to the nature of floating-rate bonds.

- Selling BTC to raise cash is akin to drinking poison to quench thirst: it solves short-term liquidity issues but creates long-term, systemic risks.

Detailed analysis follows:

First: How to understand this BTC price drop?

I personally believe this rapid BTC decline represents a targeted liquidity attack centered on MSTR. The trigger was MSTR’s use of its already-tight cash reserves—widely believed to serve as a buffer for preferred-share dividends—to repurchase some of its convertible notes. This reduced the coverage ratio of its cash reserves against preferred dividends from over two years’ worth down to roughly six months. Immediately afterward, MSTR sold 32 BTC.

The market instantly detected the scent of “cash flow distress” and launched a swift, coordinated attack. Broader sentiment—already weighed down by large IPOs draining liquidity, World Cup-related capital diversion, and rising inflation fears dampening rate-cut expectations—further enabled the attackers to reinforce this narrative on the order book, rapidly forcing asymmetrically informed capital either to capitulate or hesitate before stepping in to buy the dip.

This is classic reflexivity, as seen in traditional financial markets:

Market prices do not passively reflect reality—they actively reshape it.

In other words:

Expectations are contagious—and that contagion can alter reality itself.

George Soros’s 1992 sterling attack followed the same script: the Bank of England’s foreign exchange reserves may well have been sufficient—but market participants operated under information asymmetry. Once consensus formed that reserves were inadequate and collective shorting ensued, those reserves became insufficient in practice. Bank runs operate identically: if everyone simultaneously believes a bank will collapse and rushes to withdraw funds, the expectation becomes self-fulfilling.

Applied to MSTR, the attacker’s playbook looks like this:

Cash reserves decline → Market expects liquidity crisis and forced BTC sales → Panic-driven BTC selling pushes price lower → Lower BTC price further compresses mNAV and worsens the balance sheet → Expectation of “running out of runway” becomes increasingly validated by falling price → Fewer viable options remain → More participants join the short side → Expectation tightens further

BTC itself cannot generate sustainable cash flow to cover dividend obligations. MSTR’s flywheel depends entirely on continuous external financing—a structural vulnerability easily exploited by attackers.

Second: Why STRC declined alongside BTC—and why it will revert to par

STRC and MSTR common stock stand in a senior-junior relationship:

Common shares absorb most of the volatility from BTC price swings (junior tranche)

STRC, as the senior tranche, remains relatively stable under most conditions

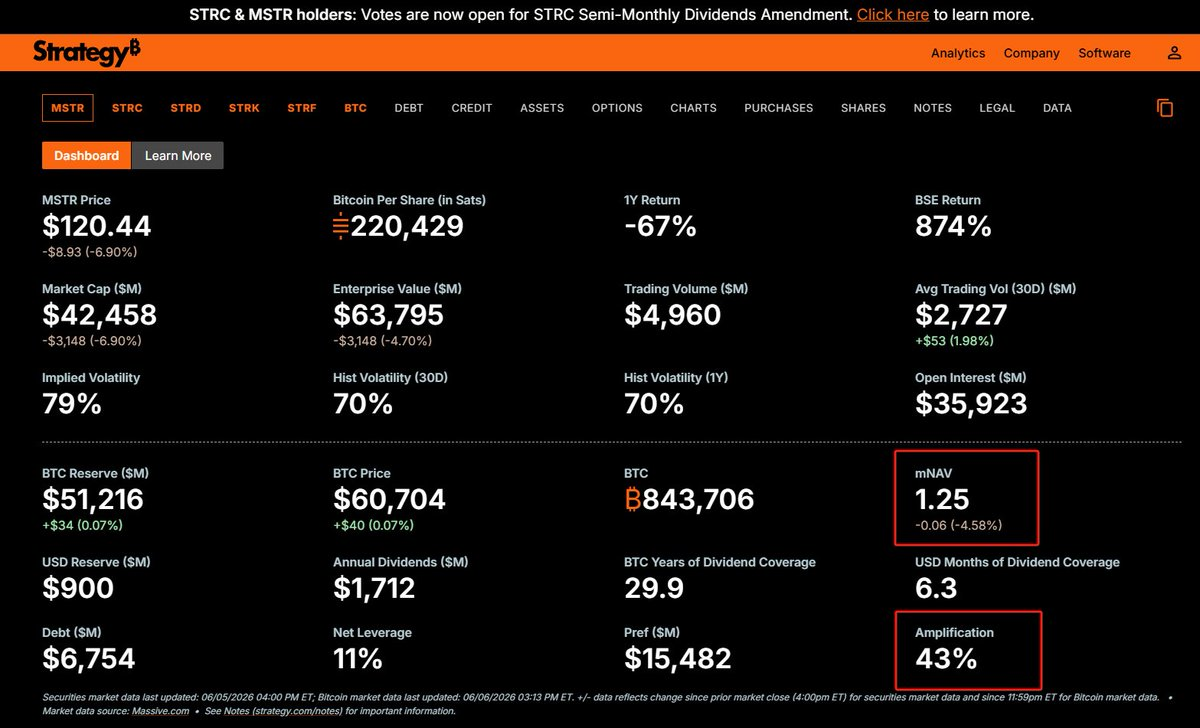

MSTR targets an overall debt-to-equity ratio of ~33–35% (currently elevated to ~43% due to BTC dropping to $61K). In theory, only if BTC falls below ~$26K would common equity be wiped out—and only then would STRC face real risk.

So why did STRC also decline?

This ties into fundamental bond pricing principles.

STRC is nominally a preferred share—but functionally a debt instrument: it pays a floating coupon and has no maturity date.

A bond’s price equals the present value of all future cash flows—periodic coupons (calculated at the stated coupon rate) plus principal repayment at maturity (par value = $100)—discounted at the market’s required rate of return (the discount rate).

When the stated coupon rate exactly matches the market’s required return, the discounted price equals par ($100). This typically occurs at issuance, when investment banks set the coupon based on prevailing market conditions and investor yield expectations.

But bonds have long lifespans. Over time, external interest-rate environments and issuer credit quality inevitably shift—both directly affecting the discount rate (the denominator). If the market’s required return rises while the coupon (numerator) stays fixed, the present value falls below par—resulting in discounting. Conversely, if required returns fall, the bond trades at a premium.

Thus, bond prices are never static—they continuously reflect the return the market demands to hold that instrument.

A price below par implies: “The market requires a higher yield than the stated coupon.” If you buy at that discount and hold to maturity, your realized yield will exceed the stated coupon—the difference between what you paid and par effectively compensates for the shortfall between the coupon and the market’s required return. In other words, the market uses discounting to extract compensation for risk it deems inadequately priced into the coupon.

STRC behaves similarly. Market concerns about MSTR’s cash flow have triggered a repricing of STRC’s payment capacity. As the “cash flow crisis” narrative spreads, investors demand a higher required return to hold STRC—rendering the 11.5% coupon insufficient.

Of course, from the attacker’s perspective, dragging STRC down alongside BTC completes the illusion: only with STRC falling too can the “cash flow crisis” narrative gain credibility amid information asymmetry—prompting you to wonder:

“Is there something I don’t know?”

For fixed-rate bonds, this story ends here: rising required returns can only be reconciled via price declines—and discounts may persist indefinitely without reverting to par. But STRC is not a fixed-rate bond—it’s floating-rate, meaning the numerator (coupon) can adjust.

For instance, if the market demands a 12% required return to hold STRC, MSTR’s management can raise the stated dividend from 11.5%. At that point, STRC’s price cannot stay persistently below $100—because buying at a discount would deliver a realized yield above 12%, drawing natural buyer interest until price rises to the level where implied yield equals 12%: i.e., par.

This is precisely why medium-to-long-term floating-rate bonds inherently trade at or near par: it’s an intrinsic property of their structure.

For MSTR, STRC’s return to par isn’t just desirable—it’s operationally essential. If STRC trades at a discount, MSTR nominally issues shares at $100 par but receives only $90 per share. It then pays dividends on the full $100 par obligation—effectively inflating its true cost of capital. Every such issuance would be economically loss-making. Is that plausible?

Third: When mNAV > 1, always sell equity—not BTC

So what breaks this cycle?

As outlined earlier, this entire decline is a self-fulfilling reflexive spiral built on information asymmetry and expectations of liquidity stress. To break it, one must credibly demonstrate that no liquidity crisis exists—that reserves are robust—and thereby remove the attackers’ foundation. Reflexivity collapses automatically.

How do we rebuild reserves?

As many X users suggest: could Saylor simply step forward and declare, “We sold more BTC during this dip—we now have ample cash, enough to last several years”? Yes—that would end panic immediately.

But it carries a hidden, second-order cost.

It forces the market to reprice MSTR entirely.

The cherished capital-market premium narrative—“continuous BTC accumulation, zero BTC sales, relentless growth in BTC-per-share”—would vanish. It would be replaced by: “BTC sales may occur at any time to shrink the balance sheet—and dilute BTC-per-share,” at best a compromised, three-steps-forward-one-step-back version of the flywheel.

The result? Uncertainty over how common shareholders will react—and whether mNAV will evaporate entirely. Even if it persists, narrowing is highly likely: the mNAV > 1 premium reflects an embedded call option on “future BTC-per-share growth.” Slower acceleration in BTC accumulation directly reduces that option’s value.

The importance of mNAV premium to MSTR cannot be overstated. Its expansion logic doesn’t rely solely on common equity or STRC-style debt—but on a virtuous cycle: “more water, add more flour; more flour, add more water”—keeping the overall debt ratio stable within its target 33–35% range. A narrowing mNAV premium directly constrains the size and timing of future equity offerings—an act of drinking poison to quench thirst.

A better path—given today’s mNAV = 1.25x and still-significant premium—is to conduct an equity offering to replenish cash reserves. MSTR’s existing SEC-registered shelf registration still holds substantial unused capacity. This is the only action that unequivocally satisfies both STRC holders (debt-like) and common shareholders—without triggering repricing risk.

The mechanism works as follows:

When mNAV >> 1, issuing new equity means every $1 raised and fully deployed into BTC purchases creates >$1 in shareholder value—precisely why investors entrust capital to MSTR. Crucially, you needn’t deploy all proceeds into BTC: retaining part as cash reserves for future debt service imposes no negative impact on shareholder value. More cash reserves also reassure STRC holders—lowering perceived risk, shrinking risk premiums, and accelerating STRC’s return to par. Subsequent STRC issuances remain viable too: win-win.

Conversely, selling BTC to raise cash is poison. If repricing causes mNAV to narrow—or vanish entirely—the equity issuance channel shuts down. At that point, investors see MSTR’s stock as fairly valued only at its underlying BTC worth—so why not buy BTC directly? Worse, if part of the proceeds must fund dividend payments, it becomes outright negative shareholder value: you’re using investor capital partly to buy BTC (value created = cost), and partly to pay dividends (pure erosion).

This is a net bloodletting structure.

Once equity issuance becomes unviable, STRC issuance also falters. The entire expansion flywheel stalls—and funding windows close. You’re left relying solely on cash reserves. Once those run dry, BTC sales become inevitable—and that’s the endgame.

Selling equity also directly improves the debt ratio. With BTC at $61K, MSTR’s debt ratio has risen from its 33–35% target to ~43%. Equity issuance adds both cash (asset side) and equity (equity side); even after reserving a small portion for dividends, the net effect is a lower debt ratio.

Selling BTC? Proceeds go straight to dividend payouts—reducing BTC holdings first, then cash outflows. Net effect: total assets shrink while debt remains unchanged—worsening the debt ratio slightly.

Sell equity: ✓ Improves debt ratio, ✓ Preserves BTC-per-share, ✓ Protects premium

Sell BTC: ✗ Worsens debt ratio, ✗ Dilutes BTC-per-share, ✗ Damages premium

The choice is unambiguous.

Finally—if, and I emphasize *if*,

MSTR does massively sell BTC to refill reserves?

Then—as many X commentators and firms like Delphi argue—the short-term crisis would indeed resolve, BTC would rebound, and STRC would return to par. That’s precisely why I say: if MSTR ever fails, it won’t be now. Whether via equity or BTC sales, immediate liquidity pressure *can* be relieved.

But personally, that would mark my disillusionment with both MSTR and Saylor.

And because the common equity thesis undergoes repricing, that “BTC-per-share growth” call option loses value—causing mNAV premium to fade. The result? A paradoxical divergence: BTC rallies, STRC returns to par—but MSTR common shares fall.

Next time, when cash reserves again dwindle and market expectations turn to BTC sales, the reflexive script repeats—and this time, it may signal the beginning of the end.

Honestly, I’d accept that outcome.

Perhaps “change” itself is an intrinsic part of this game.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News