Arthur Hayes: I almost stopped trading in Q1 this year; AI-induced job losses and the Iran war made me adopt a wait-and-see stance.

TechFlow Selected TechFlow Selected

Arthur Hayes: I almost stopped trading in Q1 this year; AI-induced job losses and the Iran war made me adopt a wait-and-see stance.

AI will destroy white-collar jobs in the U.S., triggering a deflationary collapse; an Iran war could fundamentally rewrite dollar hegemony. Bitcoin may fall first—but ultimately outperform all major assets.

Author: Arthur Hayes

Translated and edited by TechFlow

TechFlow Intro: Arthur Hayes, founder of BitMEX, rarely admits to trading almost nothing in a quarter. He believes markets now stand on the edge of two cliffs: AI-induced destruction of white-collar jobs in the U.S., triggering a deflationary collapse; and an Iran war that could fundamentally rewrite dollar hegemony. Bitcoin may fall first—but will ultimately outperform all major asset classes.

(This article reflects solely the author’s personal views and should not serve as the basis for investment decisions or be construed as investment or trading advice.)

Want to learn more? Follow the author on Instagram, LinkedIn, and X.

Because Maelstrom Fund traded extremely lightly in Q1, several brokers occasionally reached out to ask for my market outlook—and what they could do for us. My reply: “This is an untradeable zone.” Aside from gradually increasing our long position on Hyperliquid, we executed virtually no trades in Q1. Two converging forces created this trading dead zone—at least for our pure long-only portfolio.

The explosive rise of AI agents will destroy the career prospects of ordinary knowledge workers in flexible labor markets across Western developed economies—primarily the U.S.—triggering a deflationary financial collapse. I wrote about this in my piece “This Is Fine.” Since its publication, U.S. President Trump—backed by Israeli Prime Minister Netanyahu—has launched a selective war against Iran, aiming to turn it into the latest dumpster fire. The war has now lasted nearly seven weeks; the only critical question remaining is how goods and shipping traffic through the Strait of Hormuz will be managed.

I always preface geopolitical or war-related commentary by stating that I’m merely a casual skier and a house-music-loving crypto enthusiast. I have no insider information on wars or what global leaders intend to do. But I can read mainstream narrative propaganda—and use AI agents to perform simple calculations based on publicly available data. I strive to cut through the noise and focus only on what matters for my portfolio. Fortunately, I don’t live in the Levant or the Middle East, so my life and liberty face no direct risk.

In my simplified worldview, there are three plausible scenarios to consider—actually four, but the fourth (nuclear war) is uninsurable and thus unworthy of discussion. I’ll outline each scenario and then examine how it might impact Bitcoin’s price. I don’t know the probability of any given scenario. What I want to determine is whether there exists a portfolio allocation that—under the best-case scenario—outperforms hydrocarbons and their derivatives (e.g., food and fuel), and—under the worst-case scenario—while underperforming hydrocarbons, still outperforms all major asset classes.

Scenario One: Return to Normal

In this case, the war ends immediately, reverting to the pre-war status quo. However, the long-term trend of replacing expensive, symbolic-digit-manipulating knowledge workers with cheaper, more efficient AI agents continues unabated. The U.S. economy is most vulnerable, given that ~70% of its GDP is driven by consumer spending. Consumers finance materialistic consumption via bank credit—loans that appear as assets on banks’ balance sheets. If ordinary knowledge workers lose their ability to service debt, those banks become effectively insolvent, requiring massive central-bank money printing.

Scenario Two: Tehran Tollbooth

In this scenario, the U.S. military is either unwilling or unable to prevent Iran from restricting vessel passage through the Strait of Hormuz. Iran follows through on its pledge to allow “friendly” vessels to transit—for a fee of $2 million in RMB, cryptocurrency, sanctioned USD, or other diplomatic arrangements. The worst-case outcome for U.S. financial hegemony is that countries must now scramble to acquire RMB. Given that most nations run trade deficits with China, the only way to raise large-scale RMB is to sell dollar-denominated assets (e.g., U.S. Treasuries or U.S. tech stocks), buy physical gold, then sell that gold for RMB on Shanghai or Hong Kong gold markets. Among the world’s top-10 GDP economies, only Brazil and Russia run trade surpluses with China—and they rank ninth and tenth, respectively. By contrast, the U.S. runs the largest trade deficit of any economy—financed by an equally massive capital-account surplus. Yet when countries dump dollar assets to raise RMB—or bid up commodity prices in spot markets to cover shortages—the empire’s capital surplus mathematically shrinks. A financialized U.S. economy depends on foreign capital to fund government spending; without it, the arithmetic simply doesn’t add up. Ultimately, bond prices fall (or yields rise), equity prices decline—and money printing becomes necessary to finance government operations.

Scenario 2.5: Stars-and-Stripes Blockade

Interestingly, after U.S. and Iranian negotiators failed to reach a permanent ceasefire agreement, President Trump announced on Sunday, April 12, that the U.S. Navy would blockade all vessels entering or exiting the Strait. Perhaps this blockade evolves into a robber-baron toll booth—where ships pay double fees, one to Iran and one to the U.S., followed by shouts of “Allahu Akbar” and “Hallelujah.” Or perhaps so many exemptions are granted post hoc—to this or that country—that the blockade resembles moldy Swiss cheese. Either way, the core logic remains: if holding dollars no longer guarantees pirates won’t sink your ship, why hold dollars at all?

Scenario Three: Empire Strikes Back

In this scenario, the U.S. Air Force and Navy do what they’re supposed to do: cripple the Islamic Revolutionary Guard Corps’ (IRGC) ability to disrupt shipping in the Strait via punitive long-range bombing. The Strait reopens; vessels pass freely and safely—no extra fees required. Restoration of robust imperial hegemony eliminates the need for any country to transact in currencies other than the dollar—and removes the pressure to bid up commodities in spot markets—at least for a few days. The problem? Ending Iran’s control over the Strait likely means the country’s total annihilation—or, as Trump put it, “sending them back to the Stone Age.” Many Americans—raised since birth to believe Iran is the most evil nation on Earth—cheer this hardline posture toward their archenemy. Yet destroying Iran in this fashion ensures that, in its dying breath, Iran fulfills its vow to drag the entire Gulf region’s commodity and energy production into the grave with it. Spices will absolutely cease flowing—and global central banks will have no choice but to print money to save the global financial system amid broad-based commodity spikes.

If you live in certain broken-down countries, your local currency will hyperinflate versus the dollar—or even the ruble. Only the U.S. and Russia will remain large swing producers capable of filling the void left by a scorched-Middle-East. Famine and widespread social unrest will follow. So while your Bitcoin may be worth infinite units of some worthless fiat paper, your well-being faces severe risk—if you can’t escape in time.

Before diving into Bitcoin’s performance under each scenario, let’s quickly review some chart porn—visual evidence supporting my arguments.

Return to Normal

Given that I detailed this scenario extensively in “This Is Fine,” let me repost some charts and tables from that article:

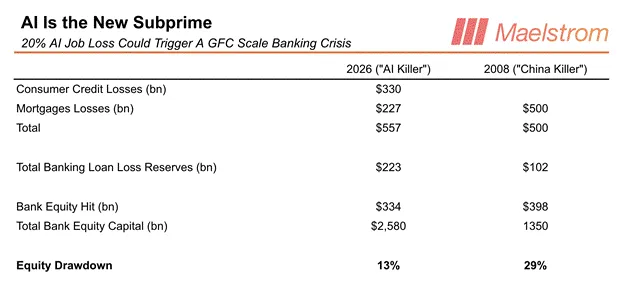

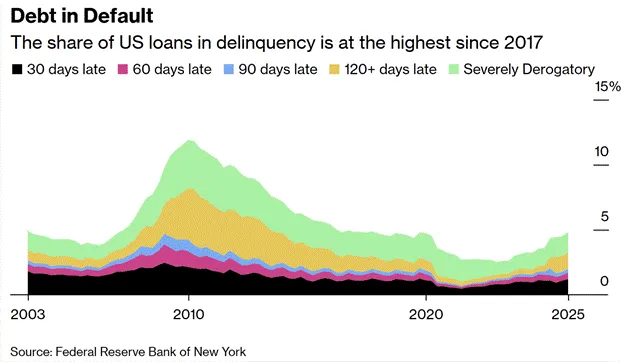

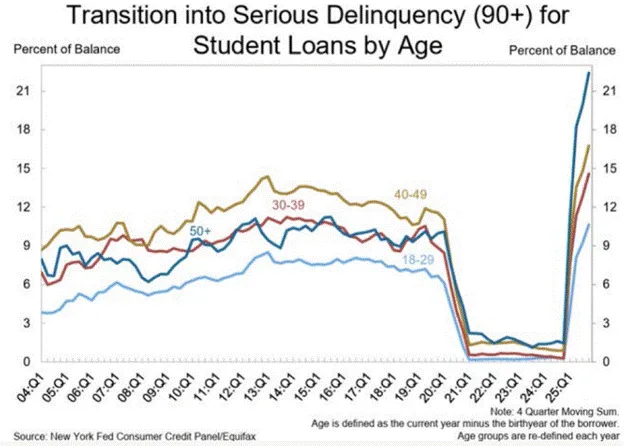

In summary, the severity of the AI-agent-driven deflationary collapse rivals the 2008 U.S. subprime crisis.

Consumer credit delinquency rates are already rising—even before mass layoffs truly begin.

Tehran Tollbooth

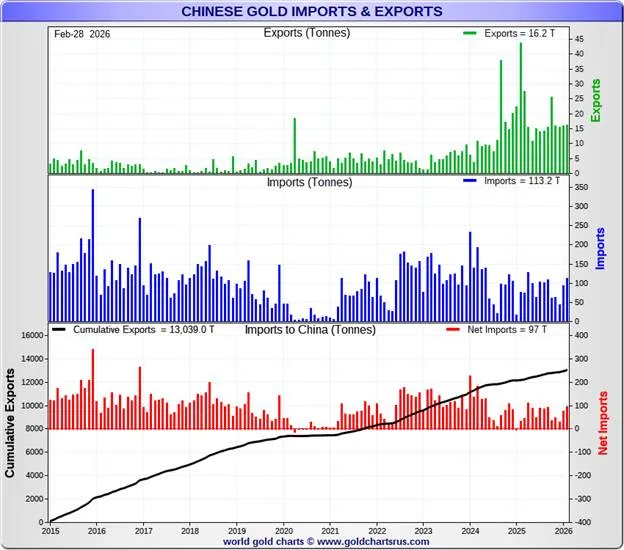

Essentially, if this scenario unfolds, it marks the end of the petrodollar—and the emergence of a new global reserve currency, or a basket of currencies. Currently, the IRGC is highly flexible on payment terms. But if they consolidate control over the Strait, why continue accepting USD payments—when the U.S. is doing everything possible to restrict their access to dollars? Ultimately, I believe they’ll stop accepting USD altogether. RMB and gold will likely become the two dominant currencies for sovereign trade.

If you can’t ship goods without paying in RMB, why hold USD savings? Given that most major economies run trade deficits with China, the only way to raise RMB is to sell dollars, buy gold, then buy RMB. Going forward, countries must hold trade surpluses in gold—not U.S. Treasuries or equities.

To highlight the growing use of RMB in trade, I’ll spotlight several charts published by Luke Gromen—illustrating how a quasi-RMB–gold standard is quietly emerging.

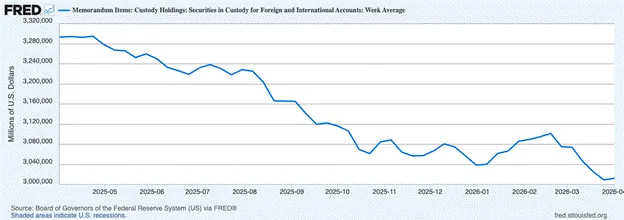

Step One: Sell dollar assets (Treasuries) and buy gold

Since the war began, foreign holdings of securities at the Fed have net declined by $63 billion. I use this as a directional proxy for foreign holdings of Treasuries and other dollar-denominated securities (e.g., equities).

What did sellers do with those dollars?

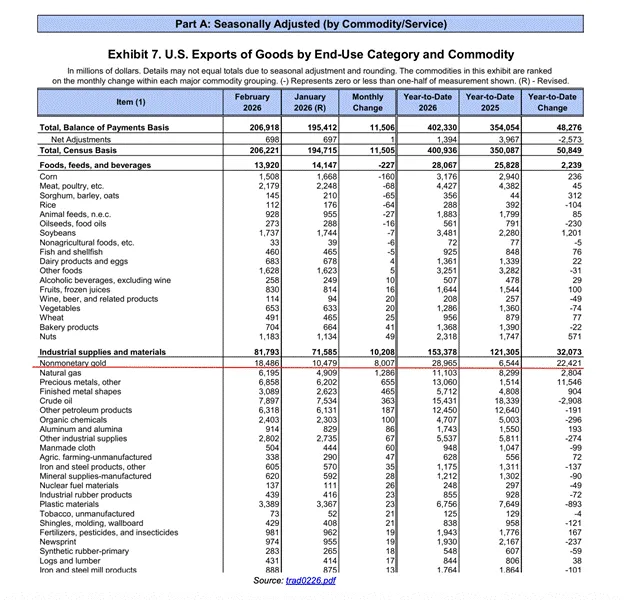

Non-monetary gold ranked as the U.S.’s top export commodity in four of the past five months—up 342% year-on-year.

They bought gold with those dollars—and shipped it out of the U.S. That’s the “U.S. manufacturing renaissance”: the only thing leaving America is barbarous relics. Sorry to all Trump supporters who thought high-paying factory jobs were coming back. Another presidential term has just screwed blue-collar workers—dry and without lube.

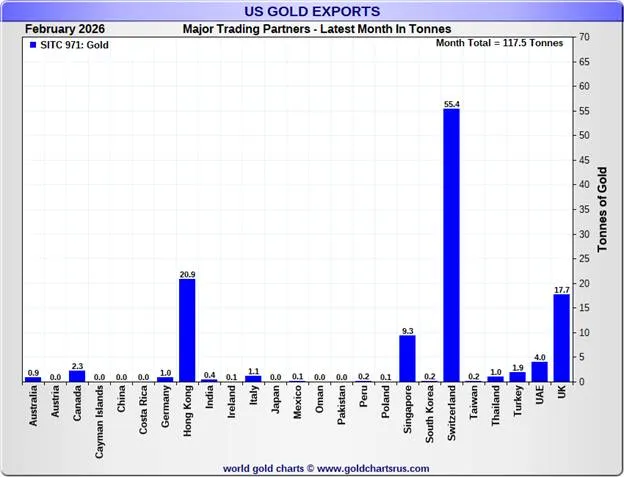

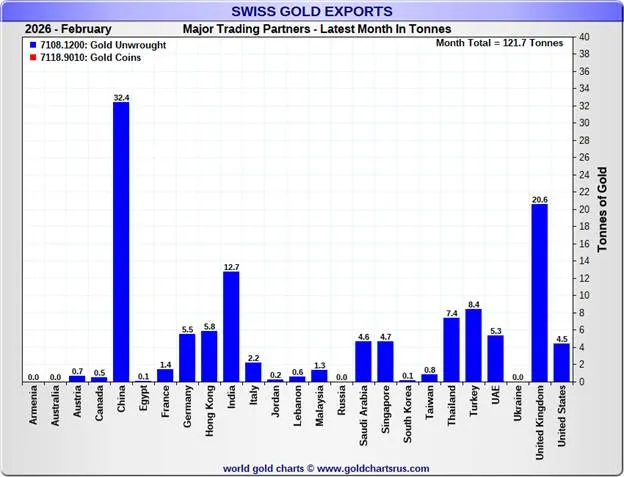

Step Two: Sell gold for RMB

Swiss refineries receive U.S. gold and recast it into bars suitable for delivery to China.

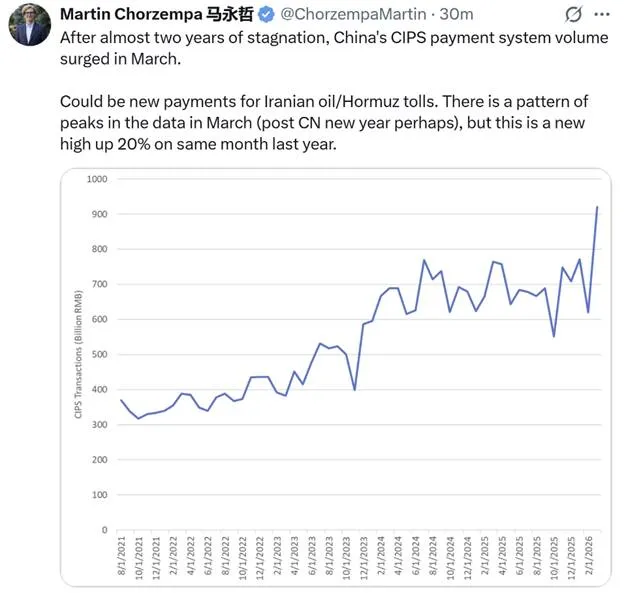

Step Three: Pay the Tehran toll

Treasury Secretary Bessent was serious when he said, “Pay in dollars—or face sanctions again.” Due to U.S. sanctions imposed roughly fifteen years ago, Iran cannot use the SWIFT payment network. Transferring RMB into the IRGC’s grubby hands requires using China’s domestic CIPS messaging system. As you can see, transaction volumes surged after the war began.

This series of charts traces the flow—from dollar-asset sales to gold purchases—ultimately funding RMB payments to Tehran or other suppliers. It doesn’t matter that the dollar remains the dominant currency used in trade. Markets are forward-looking—so the acceleration of RMB usage in global trade matters more than its low absolute share relative to the dollar. Investors who abandon dollar assets before consensus accepts a new monetary system can protect their portfolios. The pound remained the official global reserve currency technically until the 1944 Bretton Woods Agreement—but the dollar effectively replaced it as the world’s reserve currency in the early 20th century, as the U.S. economy became the globe’s most productive. In 2026, the U.S. runs trade deficits with the world’s most productive economies: China, Japan, South Korea, Germany, Taiwan, etc. Most countries run trade deficits with China. Let me emphasize this once more: if you must pay RMB to those stone-age turban-wearers to receive your goods—what the hell is the point of holding dollars?

Stars-and-Stripes Blockade & Empire Strikes Back

To gauge whether the Strait is open or closed, consult the chart above—or generate a similar version using your preferred charting tool. The top panel shows WTI futures prices for May 2026 (CL1, white line) vs. October 2026 (CL6, gold line). I use WTI because this benchmark is most relevant to U.S. gasoline consumers. Trump will only de-escalate if gasoline prices stay stubbornly high ahead of the November midterm elections. The bottom panel shows the spread between the two contracts (far-month minus near-month); the curve is inverted. Because far-month oil prices rose less than near-month ones, the market expects a sharp increase in Strait throughput. If that happens, the spread widens—as near-month prices crash. But if the spread narrows due to rising far-month prices, the global economy will descend into chaos. Ignore the rhetorical sparring between Trump and the IRGC—focus on this chart.

Quantity vs. Price of Money

After the war began, the two-year Treasury yield (white line) spiked far more sharply than the effective federal funds rate (gold line). This signals market expectations that the Fed will hike rates to combat rising energy-driven inflation.

Making sense of this is crucial—because I believe we may enter a regime where major central banks—including the Fed—raise rates while simultaneously printing money, either directly or via the commercial banking system. As war drives food and energy prices higher, politically capable leaders will subsidize key economic inputs. Failure to do so risks social unrest—or famine. Yet to prevent inflation from spreading to all goods and services, central banks must hike rates to crush demand—and suppress activity in credit-sensitive sectors of the economy. Any entity borrowing to purchase goods or services will cut spending if credit costs rise.

If central banks stop there, my Bitcoin forecast becomes straightforward. In an environment where people slash all spending except on food and energy, Bitcoin’s price falls. But every nation—whether ally or adversary of Pax Americana—must ramp up defense spending and stockpile critical commodities. Do you want your country to resemble Australia—nearly 100% dependent on Chinese imports for refined hydrocarbons? When China halted all exports at the war’s outset, Australia’s reserves lasted less than a month. They had to beg Singapore for jet fuel—paying exorbitant prices, I’m sure; otherwise, all those Aussie yobbos would’ve been stuck indefinitely at home! I know some of you will cheer this outcome—especially Japanese skiers.

Manufacturing bombs—especially nukes—to protect yourself from being turned into a dumpster nation by skinny-tie prophets, plus stockpiling commodities, both require massive government borrowing. If domestic private investors can’t—or won’t—buy these junk government bonds, central banks and/or commercial banks will print money to buy them—expanding the fiat money supply.

Keep this dynamic in mind while reading my Bitcoin forecasts for each scenario. You must decide whether money’s quantity—or its price—matters more. Otherwise, you’ll fail to understand seemingly contradictory price action across different risk assets.

Return to Normal

After reverting to pre-war conditions, Bitcoin may post a modest rebound. Yet the AI-agent deflation bomb continues ticking beneath the surface. Bitcoin won’t rally meaningfully until the Fed provides sufficient liquidity to fill the black hole left on banks’ balance sheets by consumer-credit defaults. That’s not to say it couldn’t spike to $80K–$90K—but for me, deploying fresh fiat capital requires a clear, full-throated green light from the Fed. Given that I’m already heavily long—running a pure long-only book—a higher NAV on screen would feel good—but the risk-reward ratio isn’t compelling enough to go all-in and max out portfolio risk exposure.

I don’t know how long the banking system will hold. But every week, I read stories about companies firing huge swaths of knowledge workers—because AI agents outperform humans—and about rising consumer-credit delinquencies.

Here’s an anecdote. I recently chatted with an entrepreneur friend who runs a successful crypto gaming company. He’s OG. We started discussing how AI affects his business. Trained in computer engineering, he sat down during the 2025 Christmas holidays and experimented with the latest Claude model. He was stunned by how quickly he produced shippable code—so much so that months later, he brought his top engineers to an offsite meeting to discuss AI’s impact on operations. He tasked them with designing a workflow enabling AI agents to code around the clock. They automated every step—including code review—so each morning, senior engineers wake up to tested, production-ready code awaiting final review. With AI-agent support, one person completed six months of roadmap work in four days. After that meeting, my friend decided his company must overhaul workflows immediately. So 50% of his staff will be laid off within weeks. In the AI-agent era, average engineers are redundant—but elite talent’s productivity multiplies 10x to 100x with AI-agent assistance.

As models gain deeper domain expertise, all mediocre knowledge workers face unemployment risk. Unfortunately, despite unemployment insurance, BLS and St. Louis Fed data show median annual state UI payouts hover around $28,000—dwarfed by knowledge workers’ median salaries of $85K–$90K. With no alternative but to default on bank consumer-credit repayments, the fraudulent fractional-reserve fiat banking system collapses.

Bitcoin (gold line) vs. U.S. Software SaaS ETF IGV (white line)

That said, after the ceasefire, U.S. SaaS software stocks resumed their relentless downtrend—but Bitcoin held its ground and rebounded. This is a welcome break in correlation—but it’s too early for me to claim Bitcoin has already priced in AI-driven knowledge-worker deflation and is poised for a major rally.

Tehran Tollbooth

As countries sell dollar assets to raise RMB for toll payments, Treasury and equity prices will fall. This may unfold slowly—given other payment options currently exist. But embedded leverage in the system means a single snowflake can trigger a financial avalanche: selling begets more selling, volatility spikes, markets freeze—and monetary authorities must step in with money printing. The key indicator to watch is the MOVE Index, measuring U.S. bond-market volatility. Once it climbs above 130, some form of money printing inevitably follows.

As volatility rises, U.S. mega-cap tech stocks fall—and Bitcoin struggles to rally meaningfully. As investors de-risk portfolios amid higher volatility and lower prices, they sell Bitcoin to meet margin calls. Bitcoin only rallies when things get bad enough—and bailout expectations become consensus.

Wait for Bessent—and/or whoever chairs the Fed—to press the money-printing button. Front-running this scenario carries a risk-reward ratio not worth the effort. I hope Bitcoin holds $60,000 through any full-blown TradMarket financial collapse. If Bitcoin tests and holds that level a second time, I’d generally lean toward increasing risk exposure.

Stars-and-Stripes Blockade & Empire Strikes Back

As back-month oil futures surge to catch up with spot or front-month prices, the global economy suffers severe damage. At some point, demand destruction hits Treasury and U.S. equity prices. As before, the initial reaction is Bitcoin weakness. Once the over-leveraged Western financial system implodes, the money printers activate. If the blockade ends via punitive bombing of Iran—followed by Iran’s destruction of all Gulf energy production—this could mean the annihilation of the Iranian state. A money-printing-fueled Bitcoin rally may prove short-lived—because Iran’s destruction dramatically raises the odds of World War III.

Portfolio Construction

As a lever-free, pure long-only investor, Maelstrom can let time and compounding work in its favor. Bitcoin’s recent slight outperformance versus IGV has been highly encouraging. This will prompt me to reassess my bearish Bitcoin price stance—even as AI-driven knowledge-worker deflation accelerates. Right now, the only assets I’m willing to increase risk exposure to are gold and $HYPE (Hyperliquid’s governance token). HIP-4 launches in weeks—and I predict it will capture significant market share from Polymarket and Kalshi in the prediction-market vertical.

Beyond that, I’ll pray daily to Satoshi—hoping they infect the minds of our global political elite and convince them to take psychedelics instead of dropping bombs.

Want to learn more? Follow the author on Instagram, LinkedIn, and X.

Visit the Korean version: Naver

[1] Trade data cited covers 2024–2025.

[2] IRGC – Islamic Revolutionary Guard Corps

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News